Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The following analysis of select counties of the Idaho real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere Real Estate agent.

Regional Economic Overview

The Idaho economy continues to impress with employment growing by 2.1% over the past year. Comparatively, the country as a whole has grown by 4.2% during the same period; however, the U.S. still needs to recover more than 3.7 million jobs that were lost due to COVID-19, while Idaho has already fully recovered. Moreover, state employment levels are 14,500 jobs higher than the pre-pandemic peak. Given the robust employment growth, it’s not surprising that the unemployment rate was a very impressive 2.8% in November (the most recent data available). New COVID-19 cases started rising again at the start of 2022, but it’s still unclear whether that will have an impact on the economy. Instinctively, I do not see it as a significant impediment, as the latest data suggests that infection rates may have already peaked.

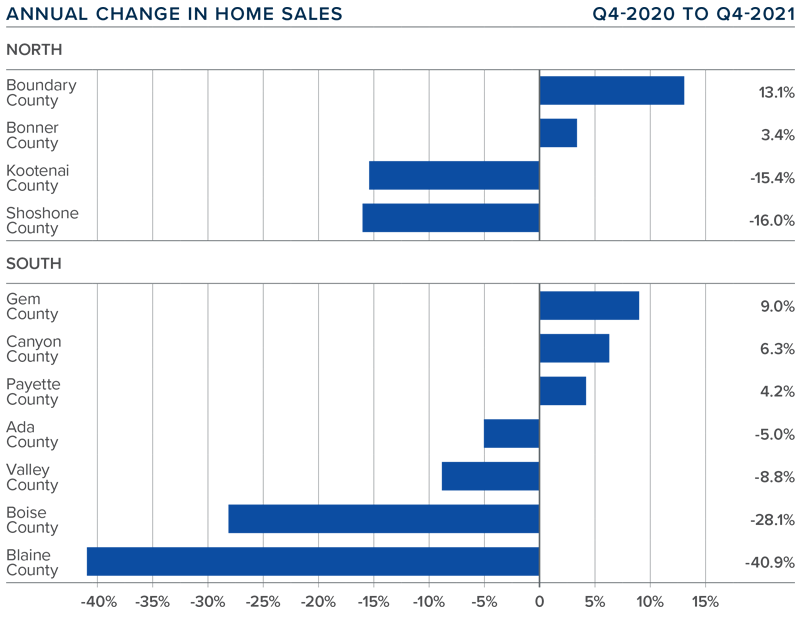

idaho Home Sales

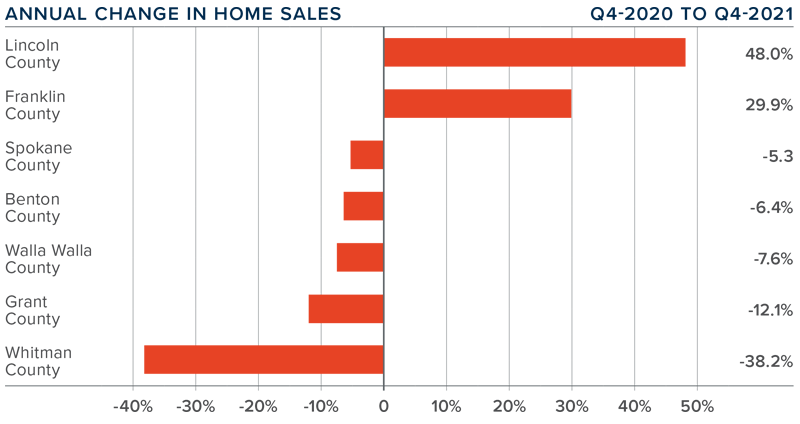

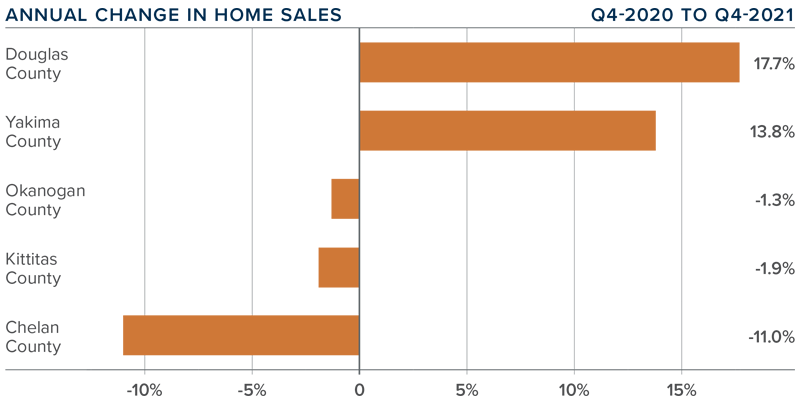

❱ In the final quarter of 2021, 6,887 homes sold. This was 5.7% lower than a year ago, and down 6.4% compared to the third quarter of last year.

❱ Quarter-over-quarter, sales rose in Bonner and Payette counties, but fell in the rest of the market areas covered by this report.

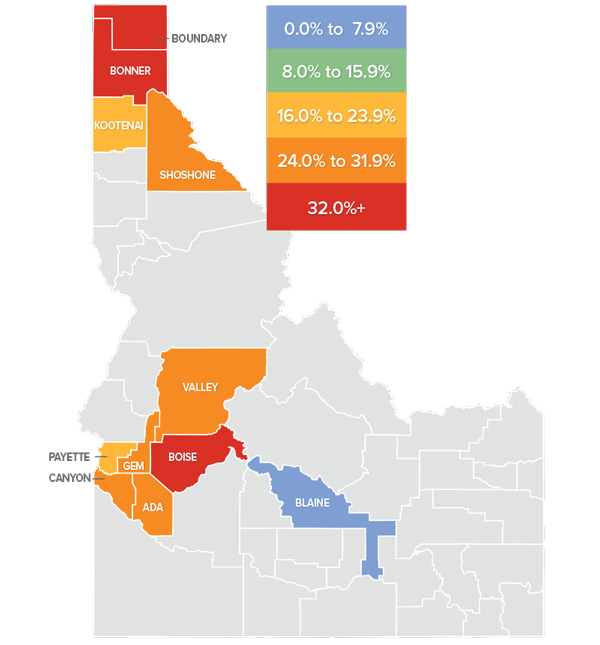

❱ Year-over-year, sales improved in Boundary and Bonner counties in the northern part of the state. Sales rose in Gem, Canyon, and Payette counties in Southern Idaho.

❱ Pending sales were 14% lower than in the third quarter, which suggests a slowing market, but this can be attributed to seasonality. Listing activity was up 41% compared to a year ago but fell 25.5% from the third quarter. The market remains very tight on the supply side.

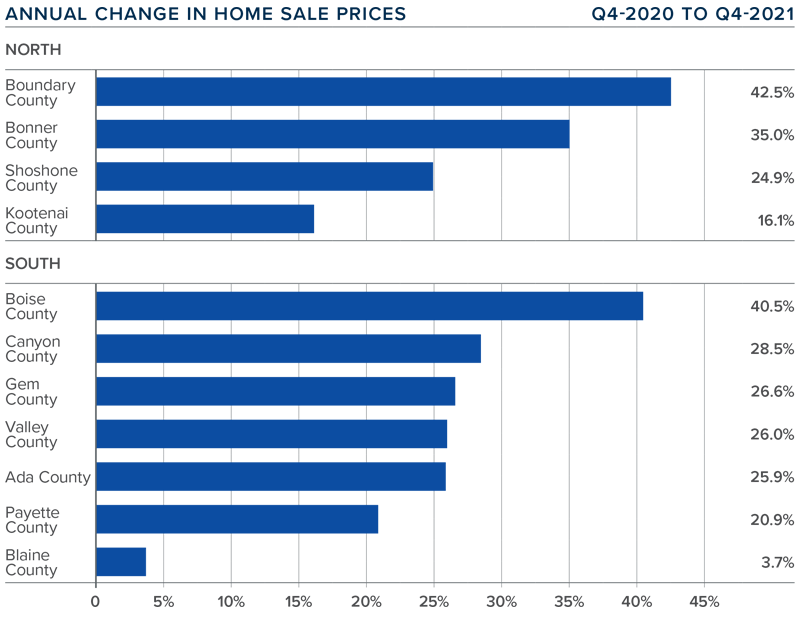

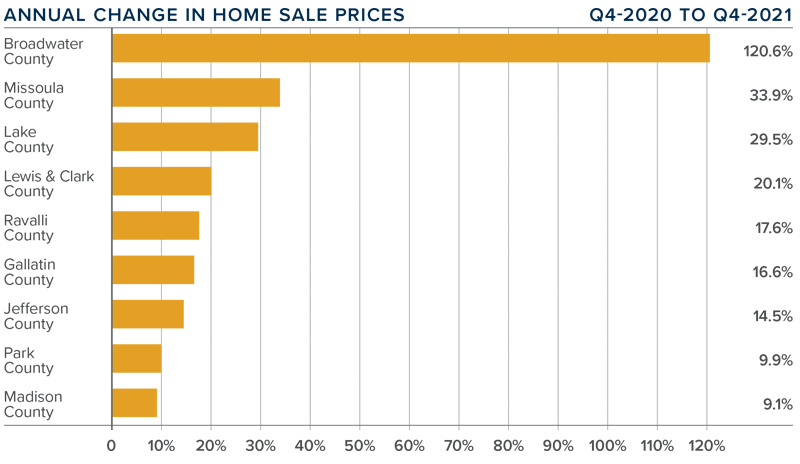

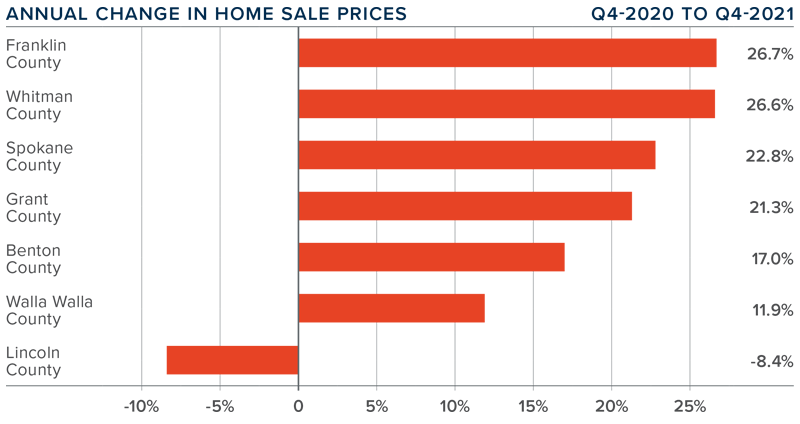

idaho Home Prices

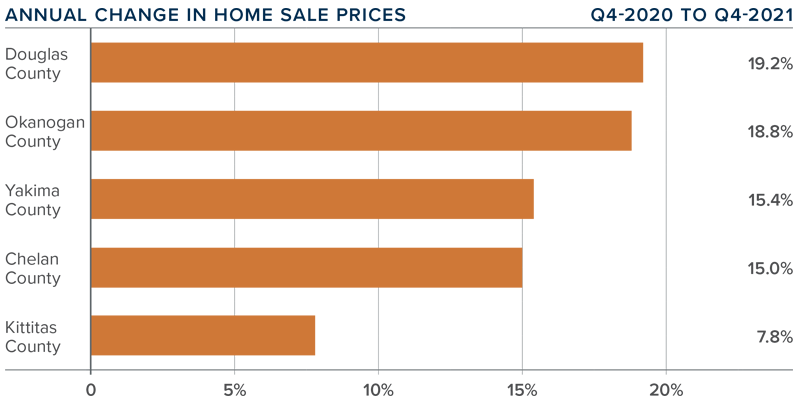

❱ The average home price in the region rose 19.6% year-over-year to $593,868 but fell 1.5% compared to the third quarter.

❱ When compared to the third quarter of 2021, prices were higher in Bonner and Boundary counties in the north, and in Payette, Canyon, and Gem counties in Southern Idaho.

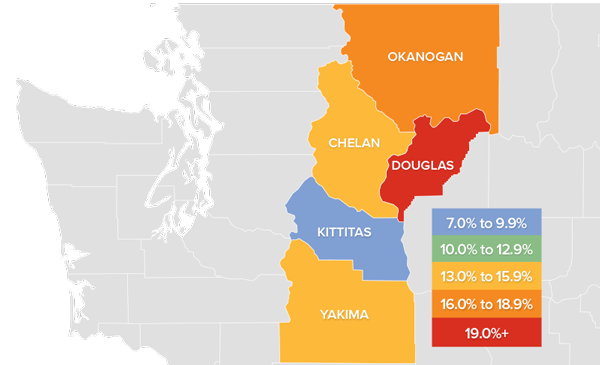

❱ Prices rose by double digits in all of the northern counties in this report, while in the southern counties, all but Blaine County saw sale prices rise by more than ten percent. In aggregate, prices rose 29.1% in the Northern Idaho counties and were up 20.1% in the southern counties.

❱ Such aggressive price appreciation is impressive given that mortgage rates rose .3% during the quarter. It’s clear the housing market is still out of balance, even as sales growth slowed. This pace of appreciation can’t go on indefinitely, and it seems we’ve reached that end. I expect price growth will trend lower as we move through 2022 due to affordability constraints and rising mortgage rates.

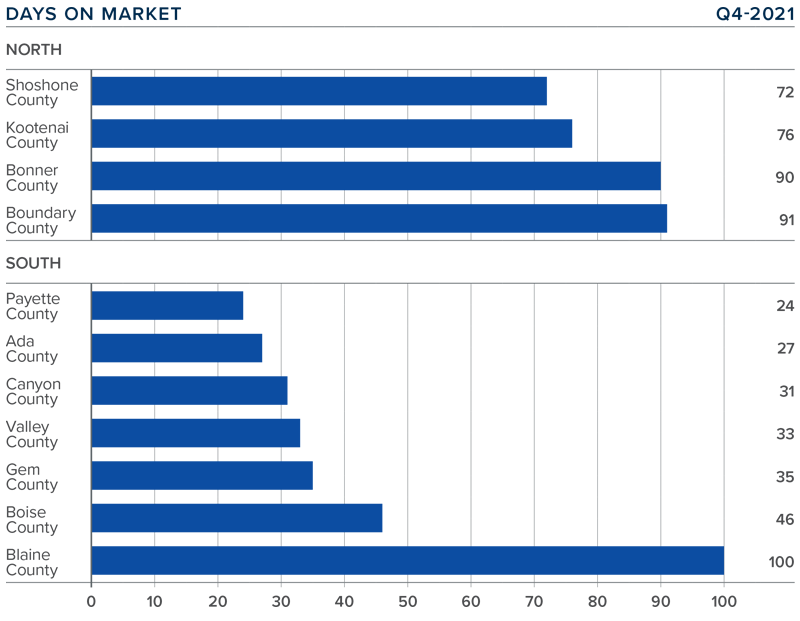

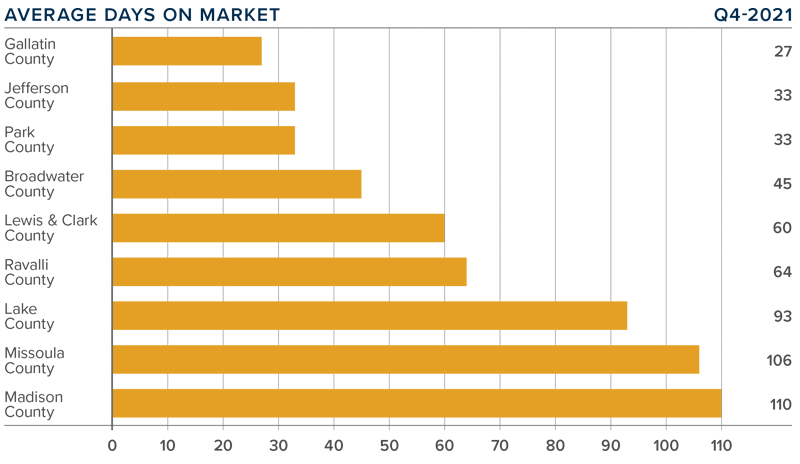

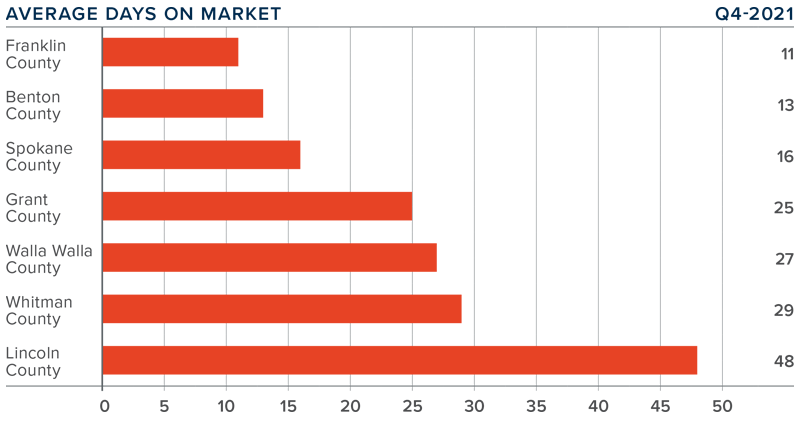

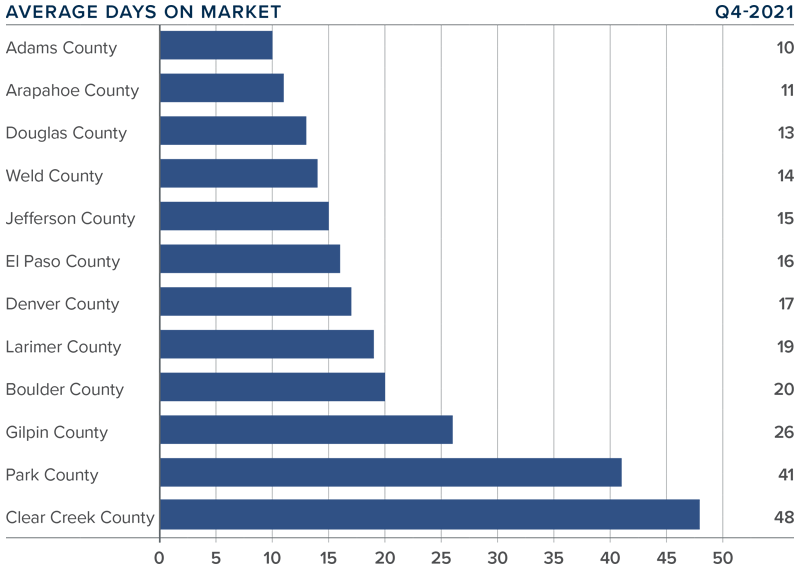

Days on Market

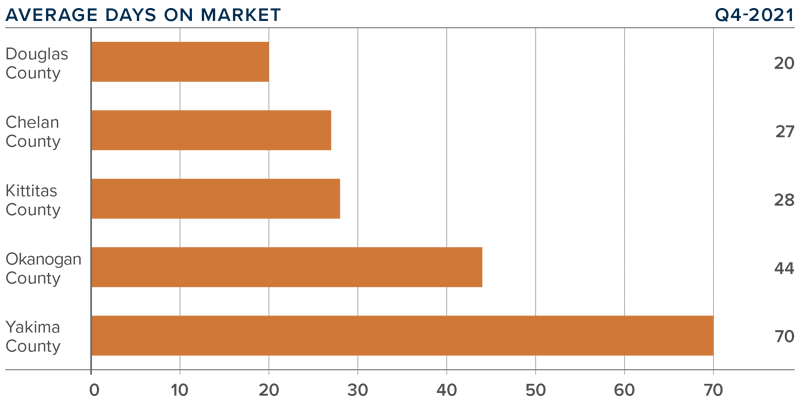

❱ It took an average of 82 days to sell a home in Northern Idaho and 42 days in the southern part of the state.

❱ The average number of days it took to sell a home in the region dropped 9 days compared a year ago but rose 11 days compared to the third quarter of 2021.

❱ In Northern Idaho, days on market dropped in all counties compared to a year ago but rose in all counties compared to the third quarter of 2021. In Southern Idaho, market time also dropped in Valley, Payette, and Blaine counties but rose in the other markets covered by this report.

❱ Homes sold the fastest in Payette County in the southern part of the state, and in Shoshone County in Northern Idaho.

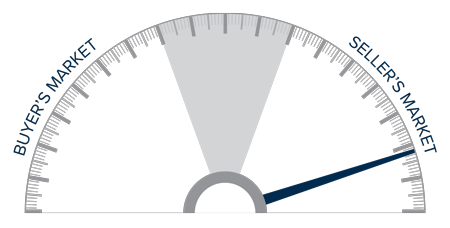

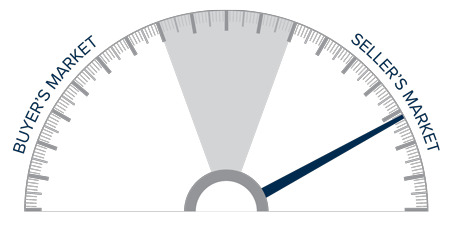

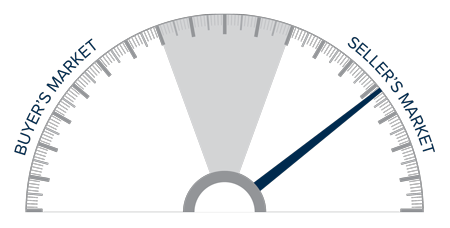

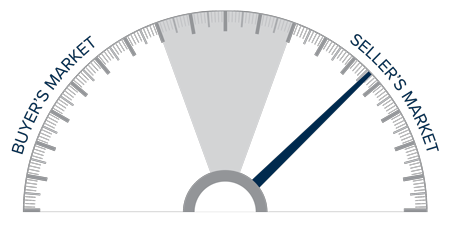

Conclusions

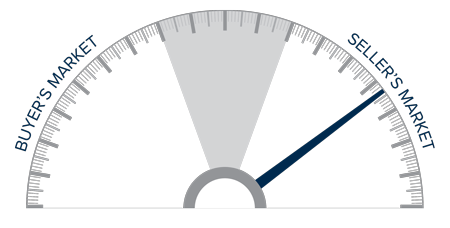

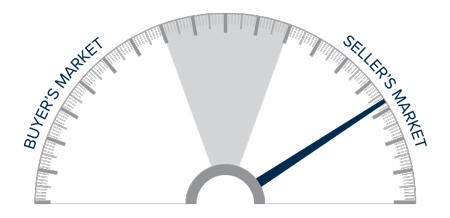

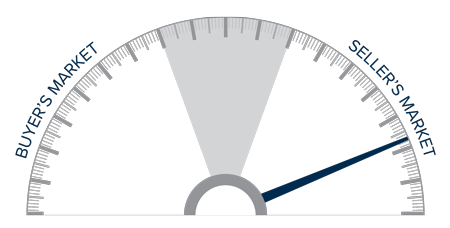

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

Idaho’s economy continues to fire on all cylinders. Such robust growth has caused the housing market to perform extremely well—as demonstrated by the rapid pace of home price appreciation.

In-migration to Idaho has been impressive. Much of this has been driven by the ability for employees to continue working remotely. For many workers leaving more expensive markets, price points in Idaho are a major draw. Although mortgage rates will continue to climb higher in 2022, my forecast calls for home prices in Idaho’s southern counties to see low double-digit percentage gains while the northern part of the state can expect increases in the high teens. Good news for sellers, but buyers will likely not be so happy.

Even with the prospect of more homes coming to market in the spring, Idaho remains staunchly a seller’s market and I am moving the needle a little more in their favor.

About Matthew Gardner

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

")