Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The following analysis of select counties of the Utah real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

Though Utah is still feeling a significant economic hit, the jobs losses in March and April have certainly turned around. The pandemic caused the loss of more than 144,000 jobs in the state, but the most recent figures show that Utah has now recovered 95,900 of them. Although that still leaves a shortfall of 48,700 jobs, the numbers are promising. The unemployment rate, which peaked at 10.4% in April, has dropped and now stands at a very respectable 4.1%. If a headwind exists, it’s that new COVID-19 infection rates started to rise pretty aggressively again in September, and this has the potential to significantly slow Utah’s economic recovery.

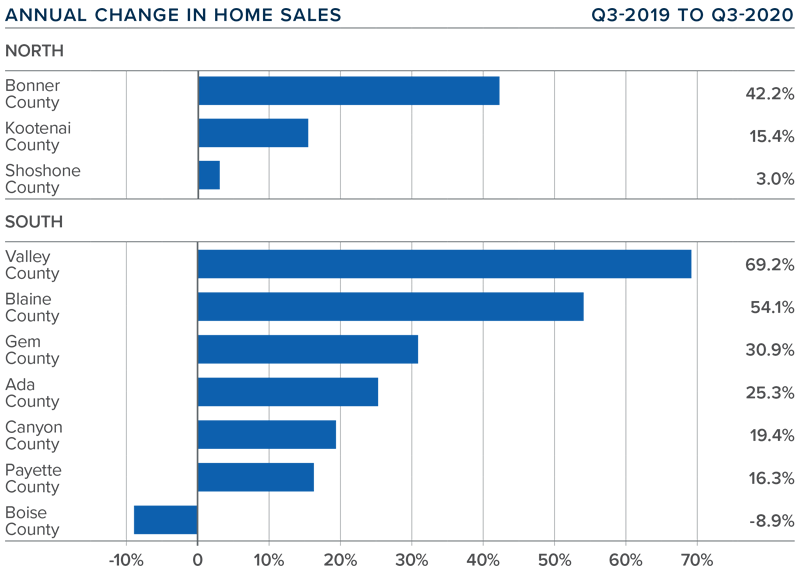

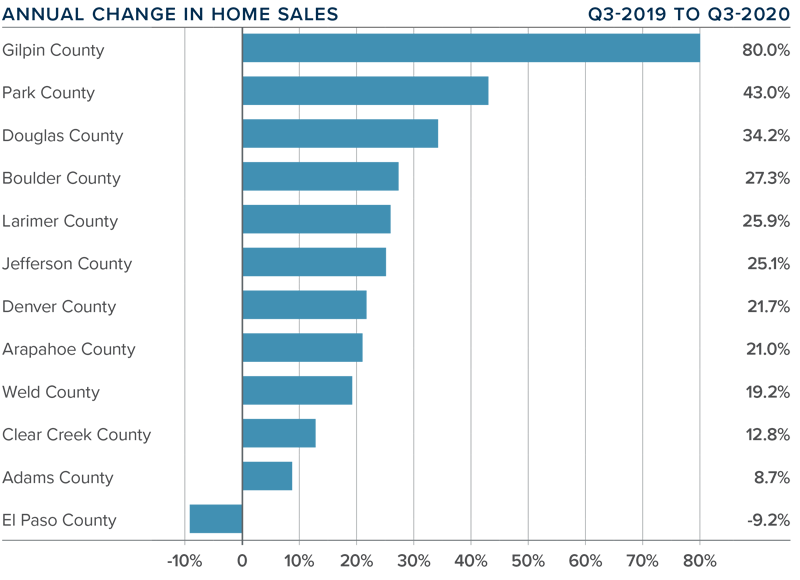

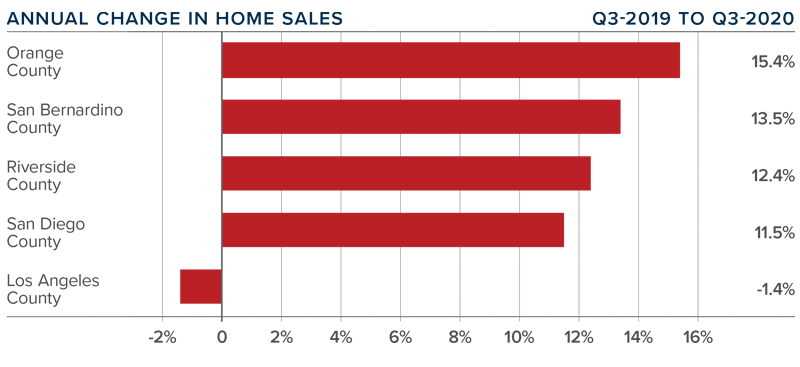

HOME SALES

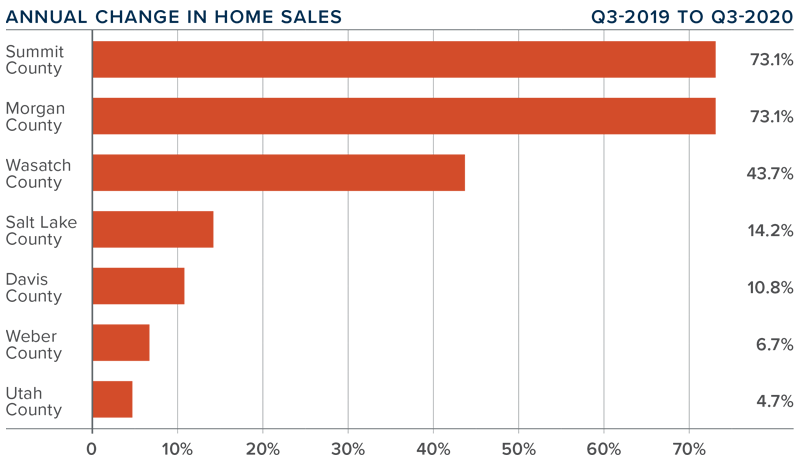

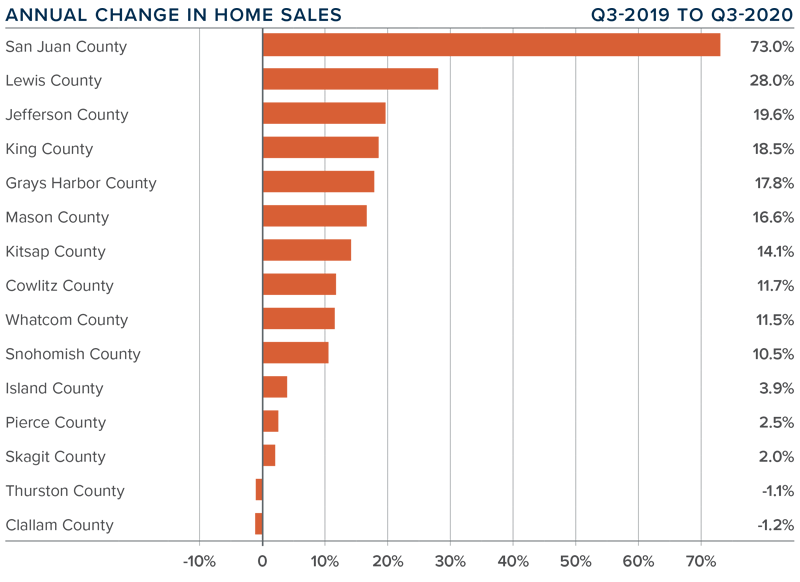

❱ In the third quarter of 2020, 11,623 homes sold, an increase of 11.3% compared to the same period in 2019. Sales were 24.7% higher than in the second quarter—on the back of a significant increase over the first quarter.

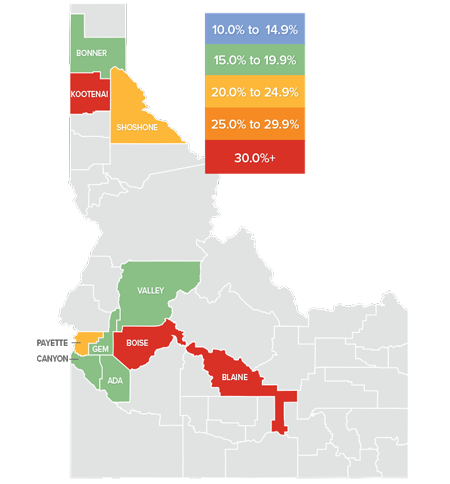

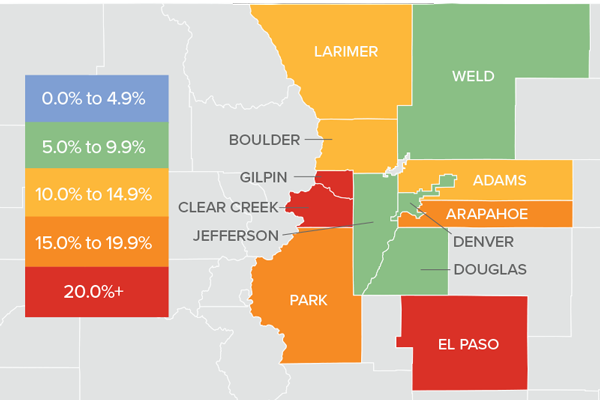

❱ Total sales activity rose in all counties covered by this report, with significant gains in the small counties of Summit and Morgan.

❱ In less positive news, the number of homes for sale in the quarter was 56.4% lower than during the same period a year ago and down 38.6% from the second quarter of this year.

❱ Pending sales in the third quarter were up 1.9% compared to the second quarter, suggesting that closings in the final quarter of 2020 will be positive. As I have stated in past reports, sales are only limited by the number of homes on the market.

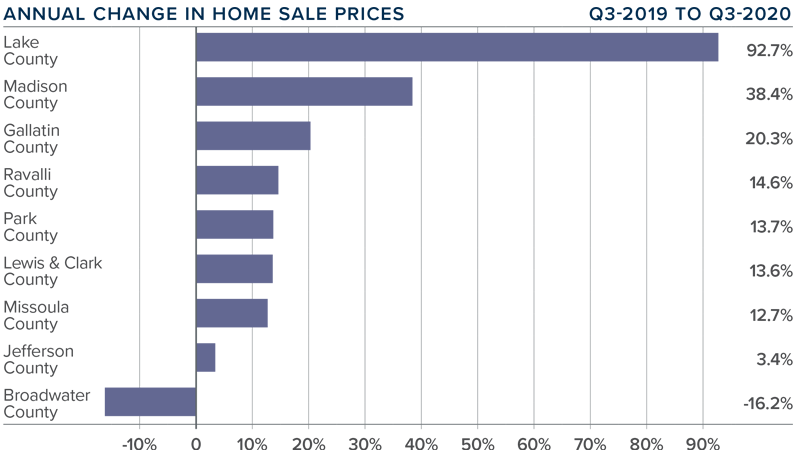

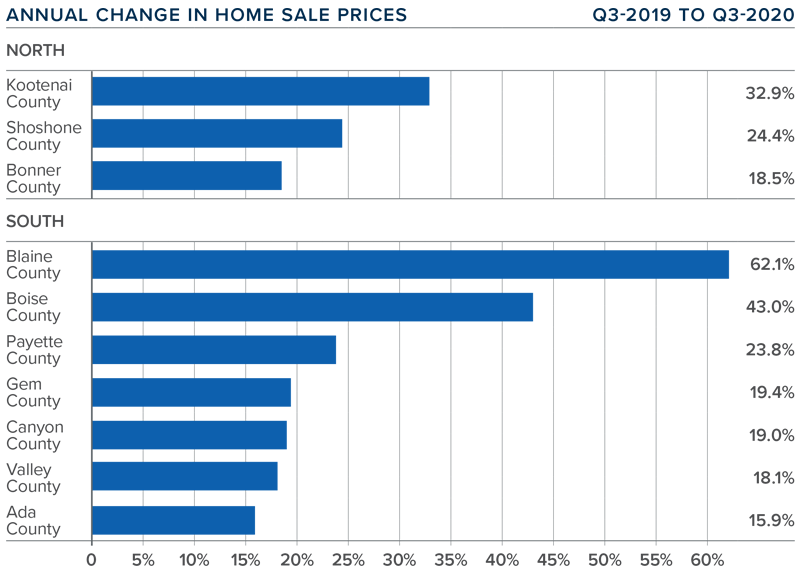

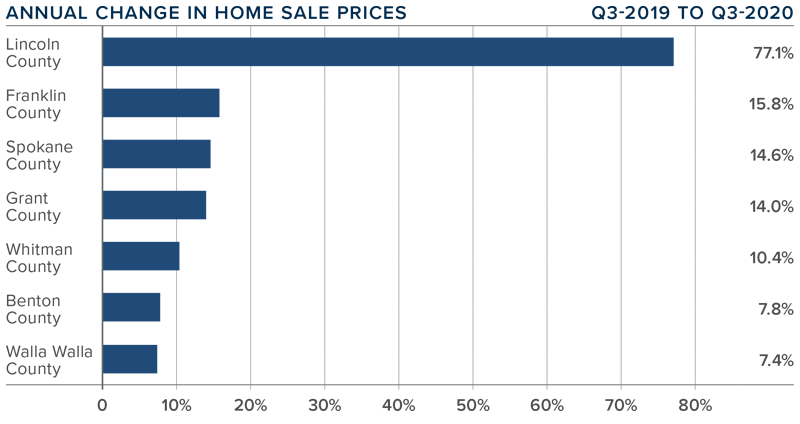

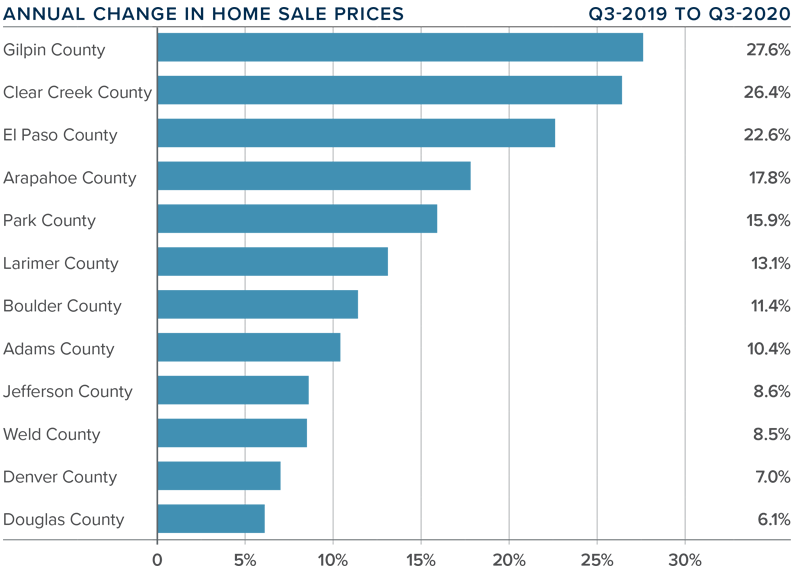

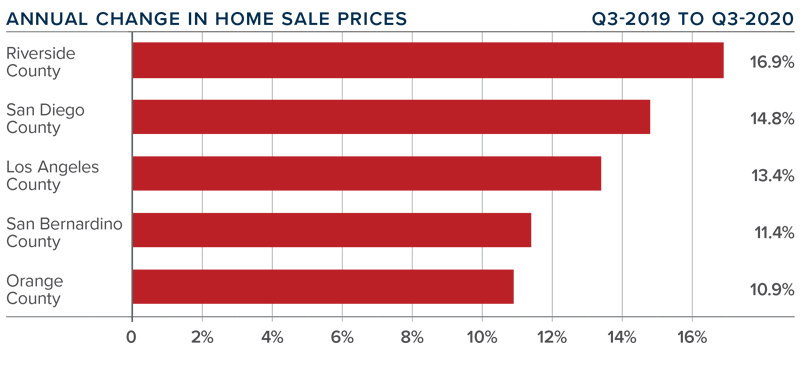

HOME PRICES

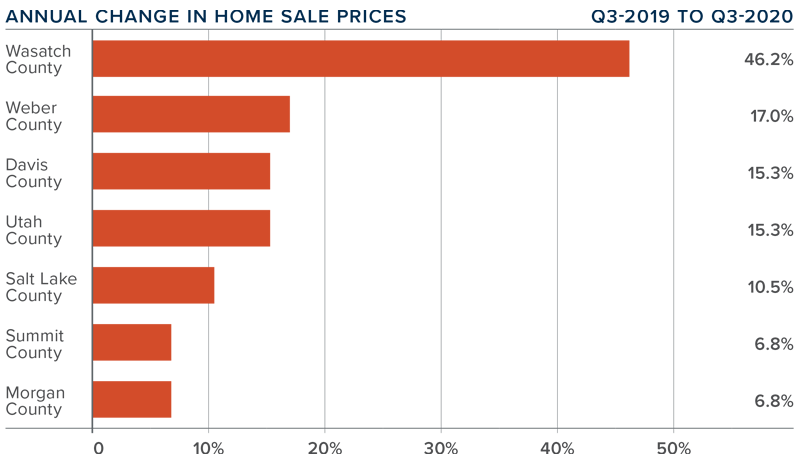

❱ The average home price in the region continued to rise in the third quarter, with a year-over-year increase of an impressive 15% to $432,640. Home prices were also 5.9% higher than in the second quarter of 2020.

❱ The average home price in the region continued to rise in the third quarter, with a year-over-year increase of an impressive 15% to $432,640. Home prices were also 5.9% higher than in the second quarter of 2020.

❱ Outside of Wasatch County, every county covered by this report saw solid price appreciation compared to the same period

a year ago.

❱ Price growth was strongest in Wasatch County, where prices rose a remarkable 46.2%. This is clearly an anomaly, and I expect to see price growth pull back in the fourth quarter.

❱ Home prices are appreciating at significant rates, demonstrating faith in the concept of home ownership, but also showing that buyers are taking advantage of historically low mortgage rates.

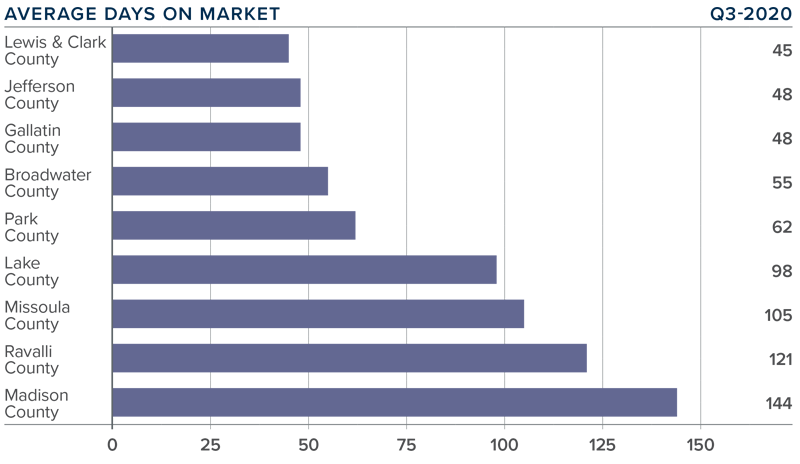

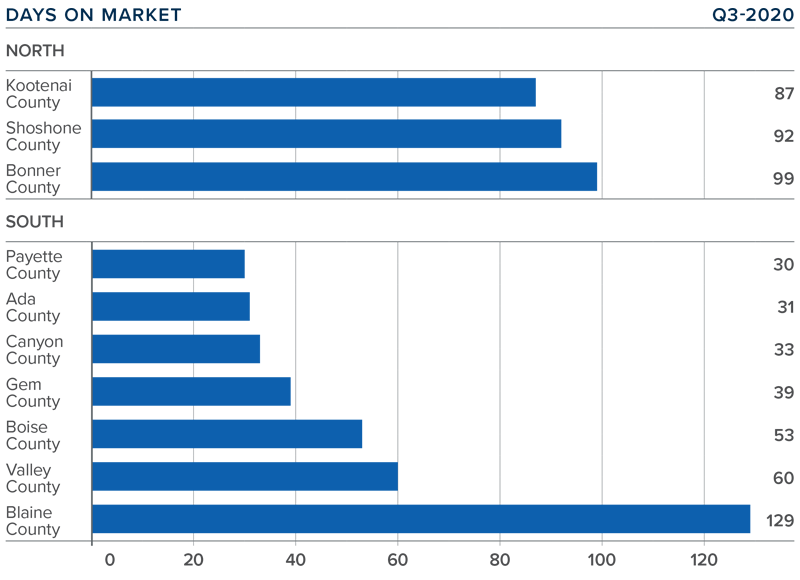

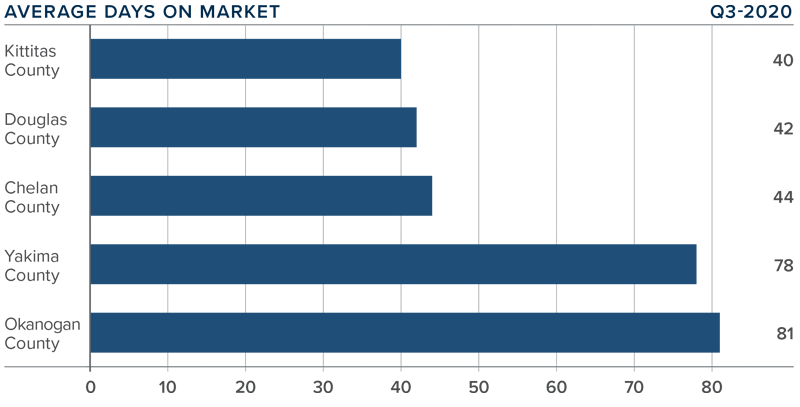

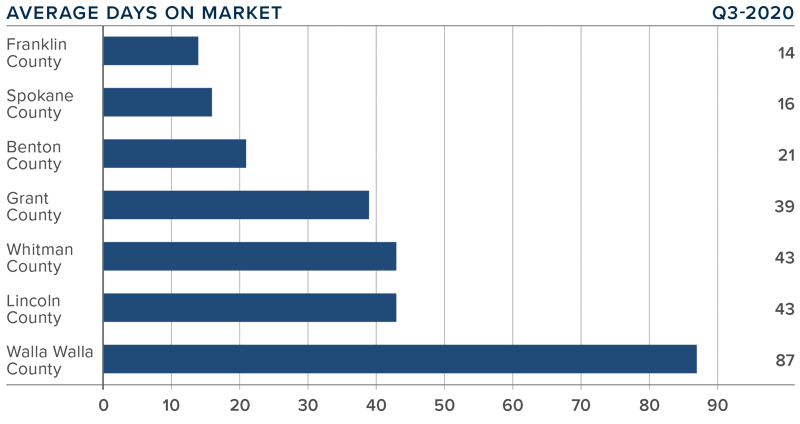

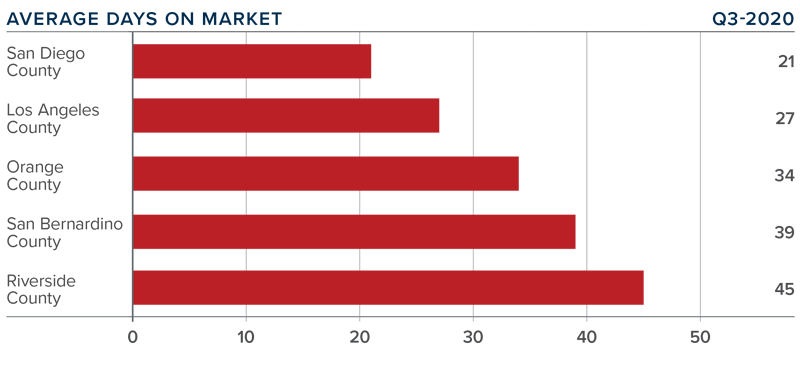

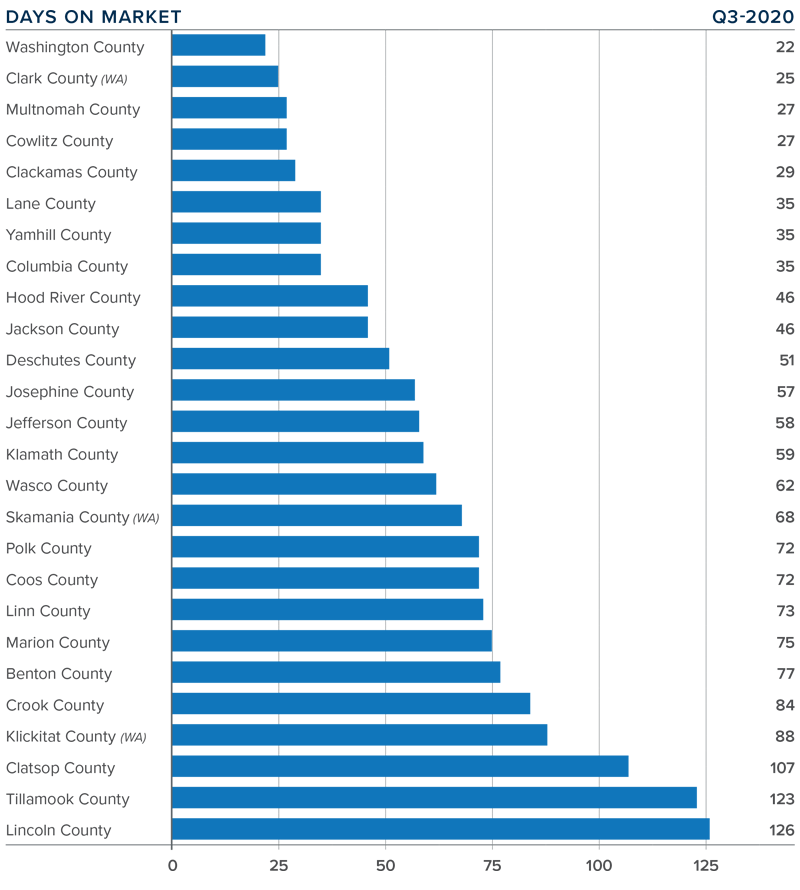

DAYS ON MARKET

❱ The average number of days it took to sell a home in the counties covered by this report rose one day compared to the third quarter of 2019.

❱ Homes again sold fastest in Davis and Salt Lake counties. The longest time it took to sell a home was in Wasatch County. It took less time to sell a home in all counties other than Morgan, Wasatch, and Summit.

❱ During the third quarter, it took an average of 40 days to sell a home in the region, down 7 days from the second quarter of this year.

❱ Market time was essentially static compared to a year ago, but significantly lower than in the spring of 2020. This is likely due to the lack of inventory, making the housing market more competitive.

CONCLUSIONS

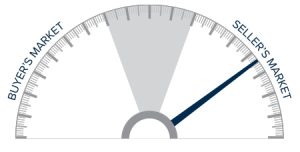

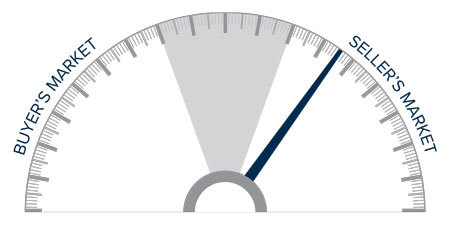

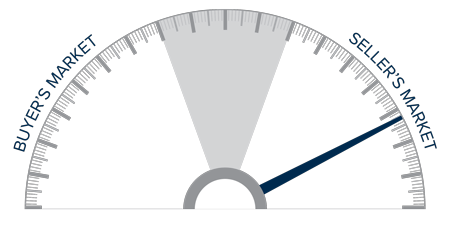

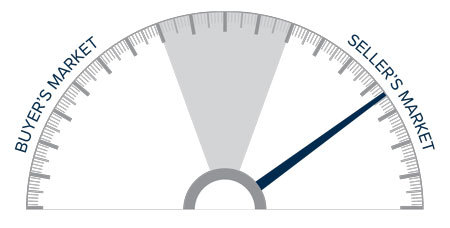

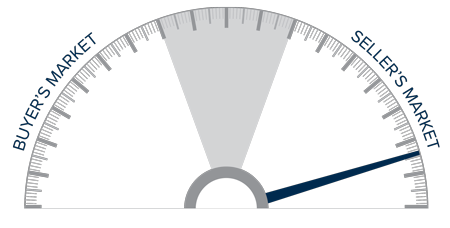

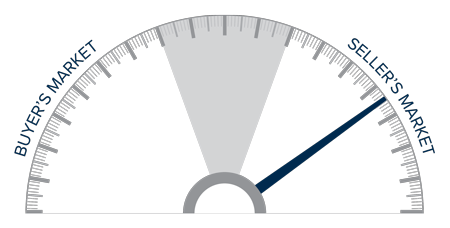

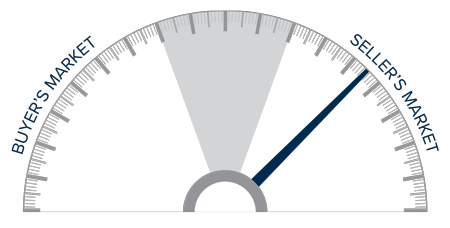

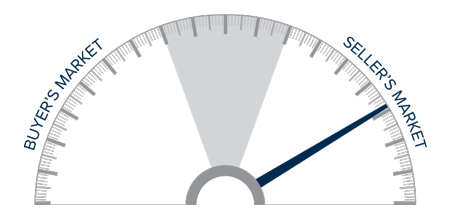

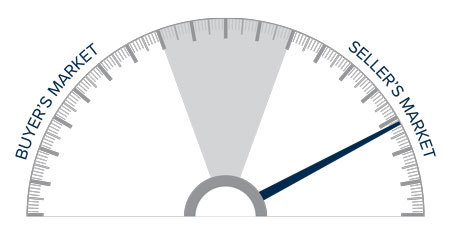

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

We know we have demand in the region, and that limited supply is heating up the housing market as demonstrated by reduced market time and significant price appreciation.

Listing activity is unlikely to improve as we round out the year, and buyers keen on taking advantage of historically low mortgage rates will be competing for the limited number of available homes. As such, I am moving the needle a little more in favor of home sellers.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national

level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.  As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real

This speedometer reflects the state of the region’s real

")