If you’ve ever walked through an older neighborhood and felt drawn to a home that looks balanced, practical, and quietly confident, you were likely looking at an American Foursquare. Sometimes called a Prairie Box or Prairie Cube, this architectural style is one of the most straightforward designs in the American architectural tradition, and one of the most enduring.

Popular from the late 1890s through the 1920s, the Foursquare emerged during a time when ornateVictorian homesdominated the landscape. In contrast, these homes favored simplicity, efficiency, and sold craftsmanship. Influenced by the Prairie and Arts and Crafts movements, the Foursquare prioritized thoughtful design over decoration, making it both practical and approachable.

A Shape That Works

True to its name, the Foursquare is defined by its box-style construction. The home’s nearly square footprint creates a symmetrical form, with rooms occupying each quadrant. Most Foursquares are two to two-and-a-half stories tall, with the half story tucked into a spacious attic. This efficient layout was intentionally designed to make the most of smaller lot sizes while still providing generous living space.

Rooflines, Porches, and Presence

A low-pitched hipped roof is one of the most recognizable features of a Foursquare home. The roof slopes evenly on all four sides, often forming a pyramid shape, and is frequently paired with a central dormer window that brings light and air into the attic level.

Many Foursquares also feature a covered front porch—sometimes spanning the full width of the home—supported by simple columns. These porches extend the living space outdoors and give a home a welcoming, grounded presence on the street.

Materials and Details

Building materials for Foursquare homes vary by region, with brick and wood being the most common. While the exterior design remains restrained, later models often incorporate Arts and Crafts details, especially inside the home. Built-in shelves, benches, bookcases, and window seats add warmth and function without excess ornamentation.

Inside the Foursquare

The interior layout reflects the same efficiency seen on the exterior. Traditionally, the main floor contains shared living spaces such as the living room, dining room, kitchen, and entryway, while bedrooms are located on the second floor. Hallways are minimal, and because each room typically sits at a corner of the home, natural light enters from multiple directions, a detail that homeowners still appreciate today.

Why Foursquare Homes Still Matter

More than a century later, American Foursquare homes remain highly desirable for their smart layouts, timeless proportions, and understated character. They’re homes designed to work well, on their lots, in their neighborhoods, and in everyday life. That kind of thoughtful simplicity never goes out of style.

This is a recurring series of blog posts taking a closer look at the U.S. economy and several major regional markets in Windermere’s nine-state footprint. Updates will be released on a quarterly basis.

Economic Overview

Last year did not deliver the hoped-for breakout from the low-sales housing market that has persisted since interest rates skyrocketed in 2022. Just over four million existing homes sold in 2025 – nearly identical to the totals in 2023 and 2024.

Mortgage rates edged lower in the fourth quarter, falling from an average of 6.35% in September to 6.19% in December. That downward trend continued into early 2026, particularly following the announcement that Fannie Mae and Freddie Mac would purchase additional mortgage-backed securities.

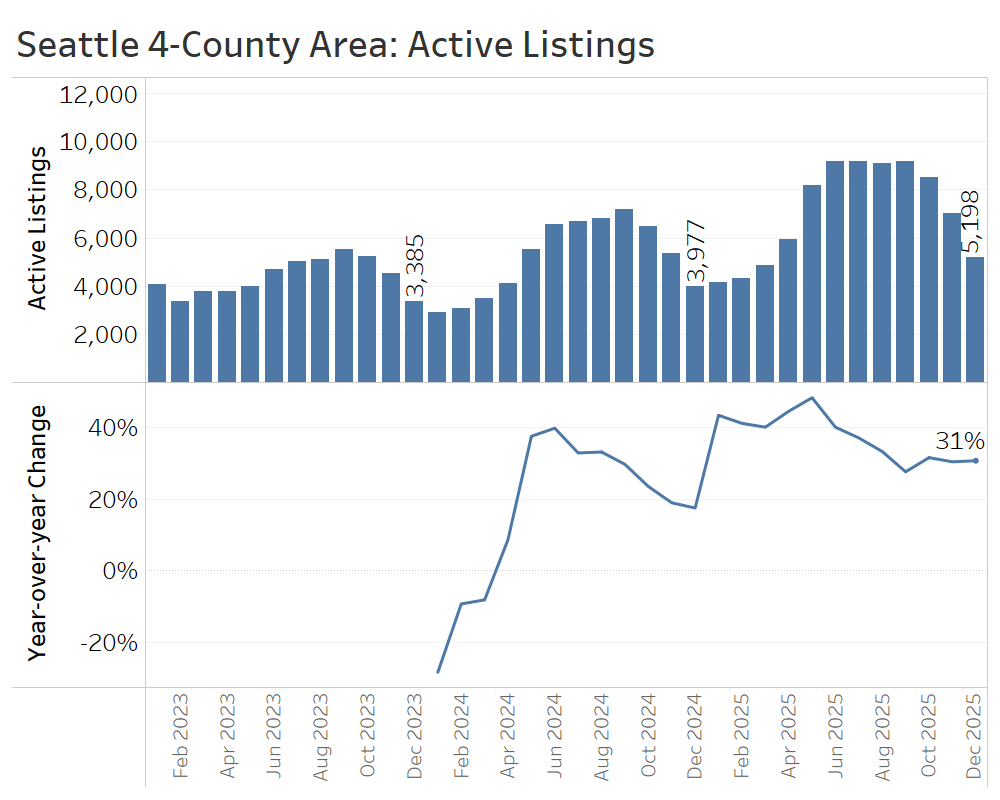

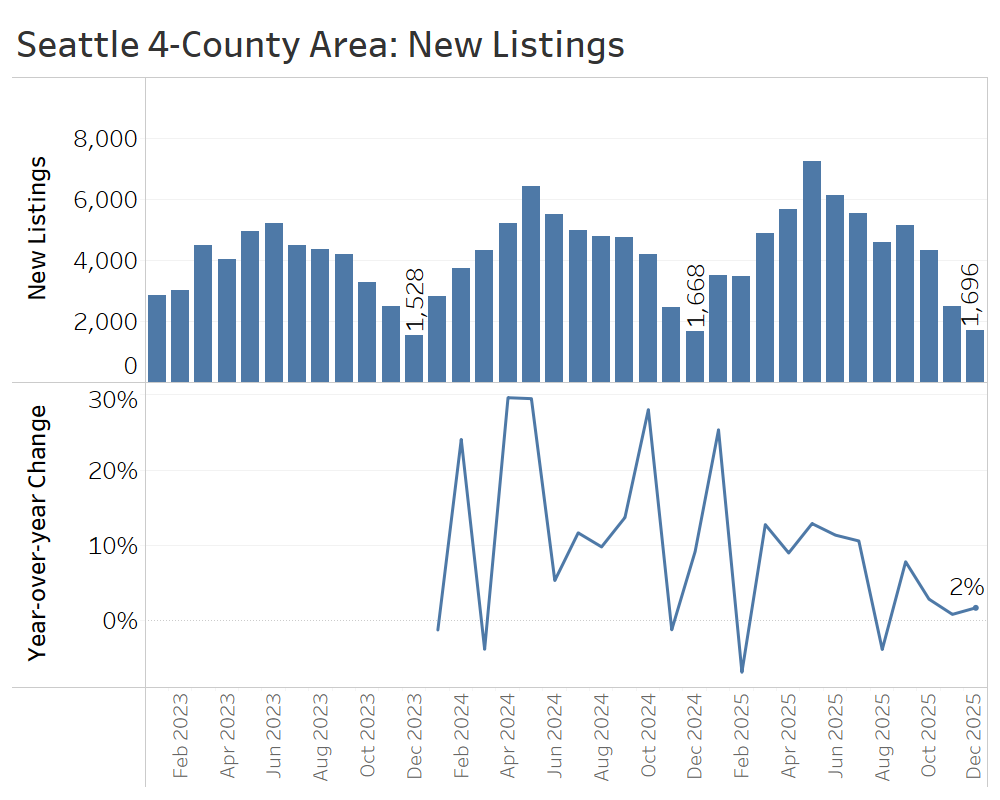

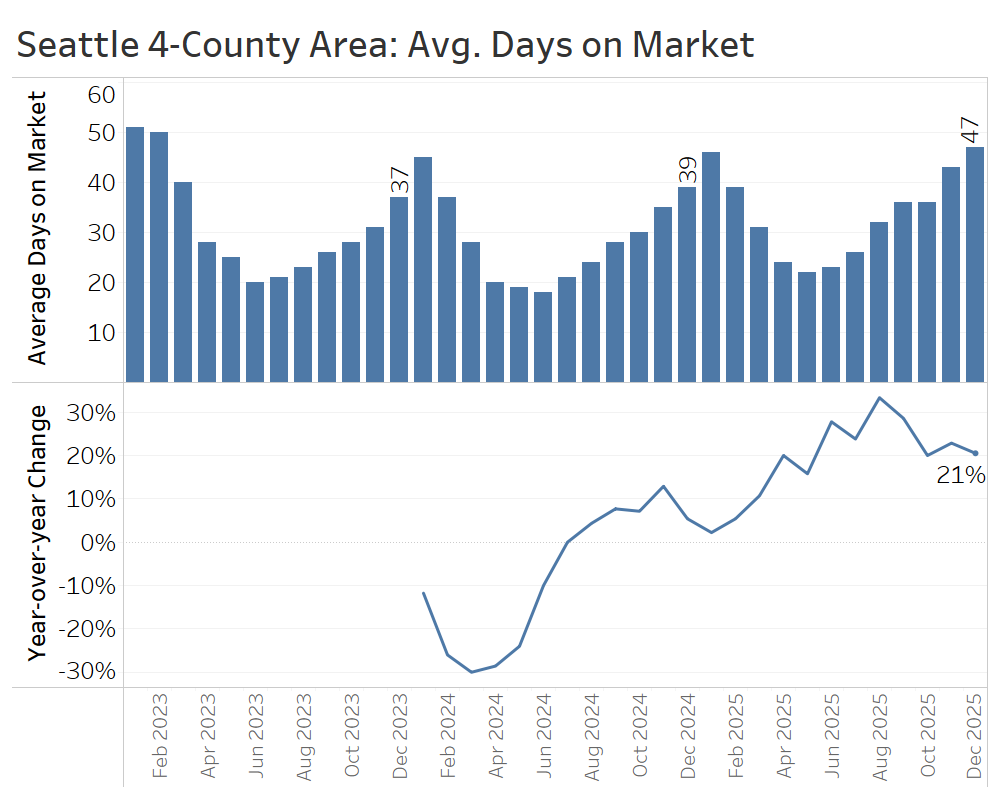

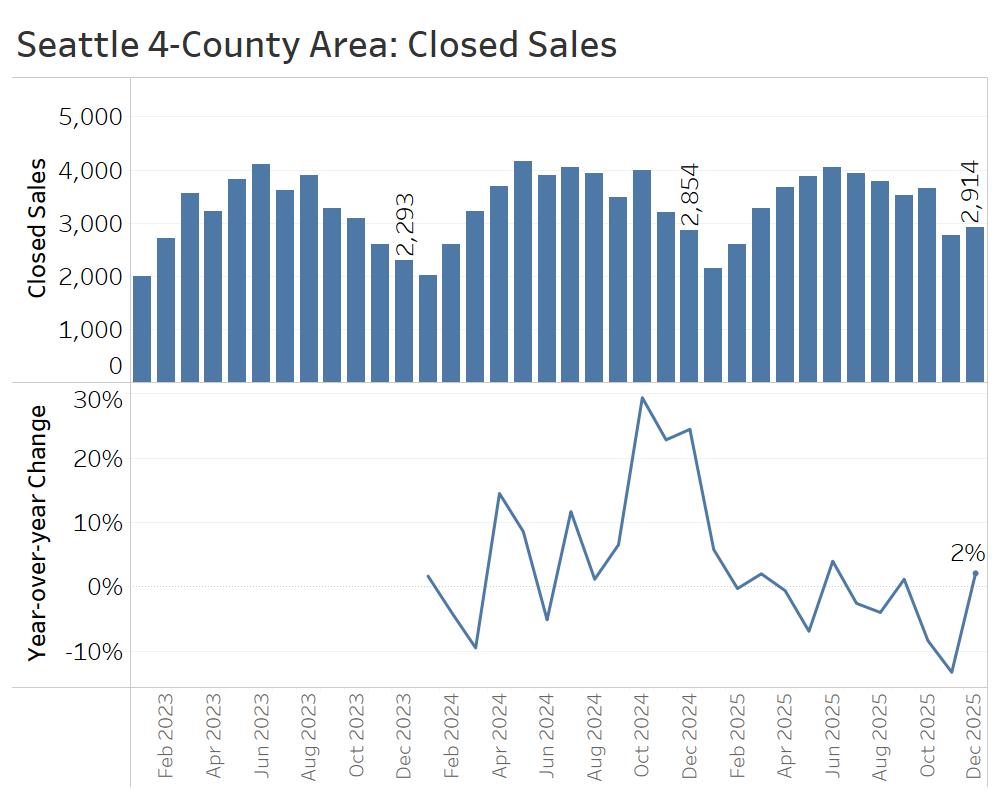

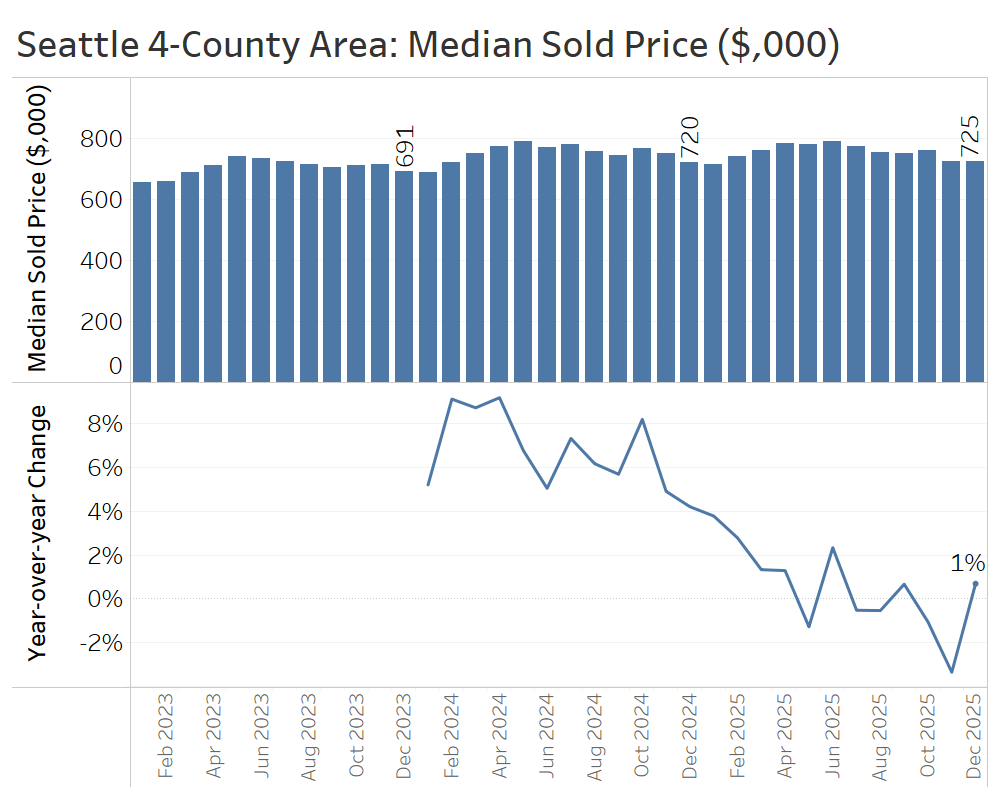

Greater Seattle Area (King, Snohomish, Pierce, and Kitsap Counties)

The fourth quarter cemented the defining themes of 2025 for the Seattle-area housing market: higher inventory and more negotiating power for buyers. Active listings totaled nearly 5,200 at year-end, which was 31% higher than at the end of 2024, yet well below the more than 9,000 listings on the market as recently as September, reflecting the typical seasonal pullback in the fall.

The fourth quarter is typically the low-water mark for new listings, and 2025 was no exception: just under 1,700 new listings hit the market in December, barely 2% more than a year earlier. That modest year-over-year increase marked a major cooldown from the faster pace of new-listings growth seen earlier in the year.

Listings continued to linger on the market longer in the fourth quarter compared to the prior year. In December, homes averaged 47 days on market, up from 39 days in December 2024. January will likely mark the seasonal high-water mark before time on market plunges with the onset of the spring selling season later in the first quarter.

Closed sales in the fourth quarter generally fell short of fourth-quarter2024 levels, which were boosted by a frenzy of buyer activity following the Federal Reserve’s initial interest rate cuts in September of that year. Closed sales year over year declined 8% in October and 13% in November, before rebounding to a 2% year-over-year increase in December.

Cooler demand this quarter showed up in prices, too. October and November saw median sale price drops of 1% and 3% from 2024, before ending the year at $725,000, about 1% higher than the end of 2024. High inventory tends to depress price growth, as sellers are forced to compete for limited buyers.

The fourth quarter brought 2025 to a subdued close in the Seattle-area housing market, with no surge of activity to rival the fourth quarter of 2024 and higher inventory continuing to weigh down prices. That said, the new year is kicking off with much lower interest rates than a year ago, which may be enough to jump-start buyer demand after a quiet winter.

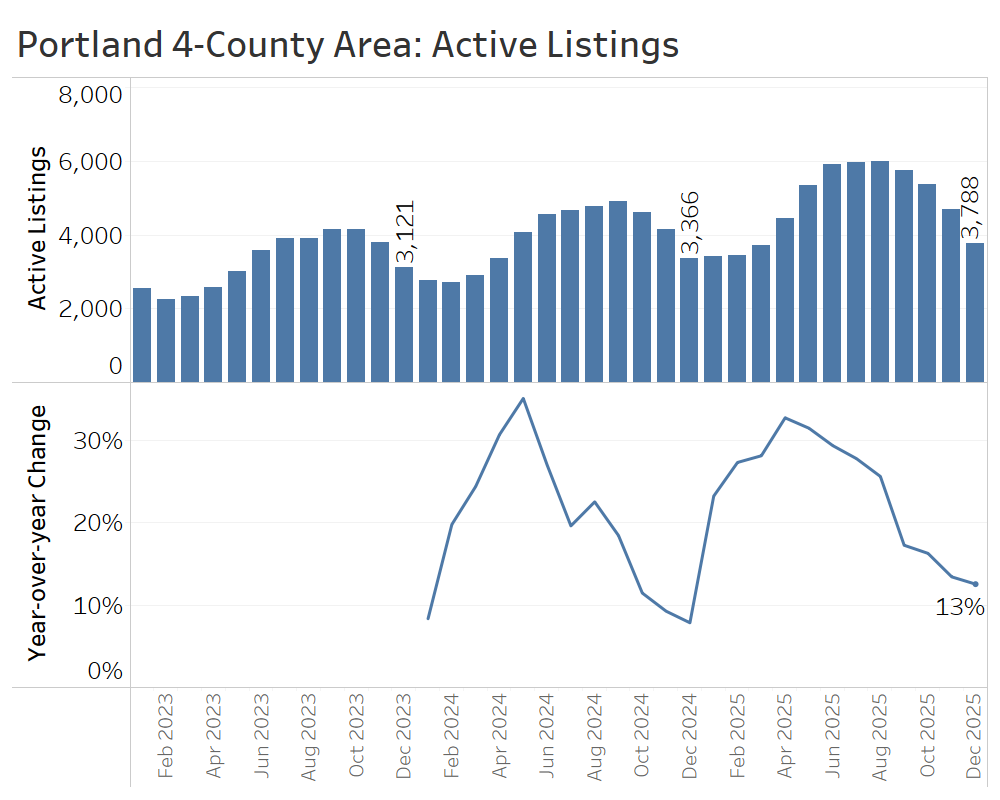

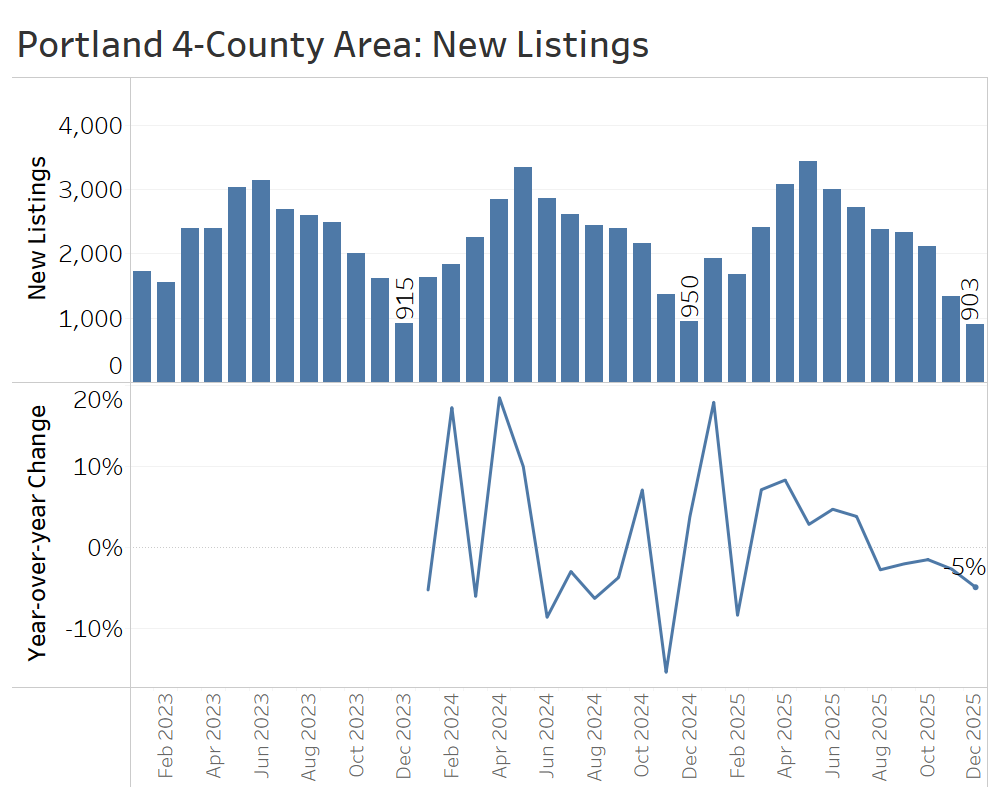

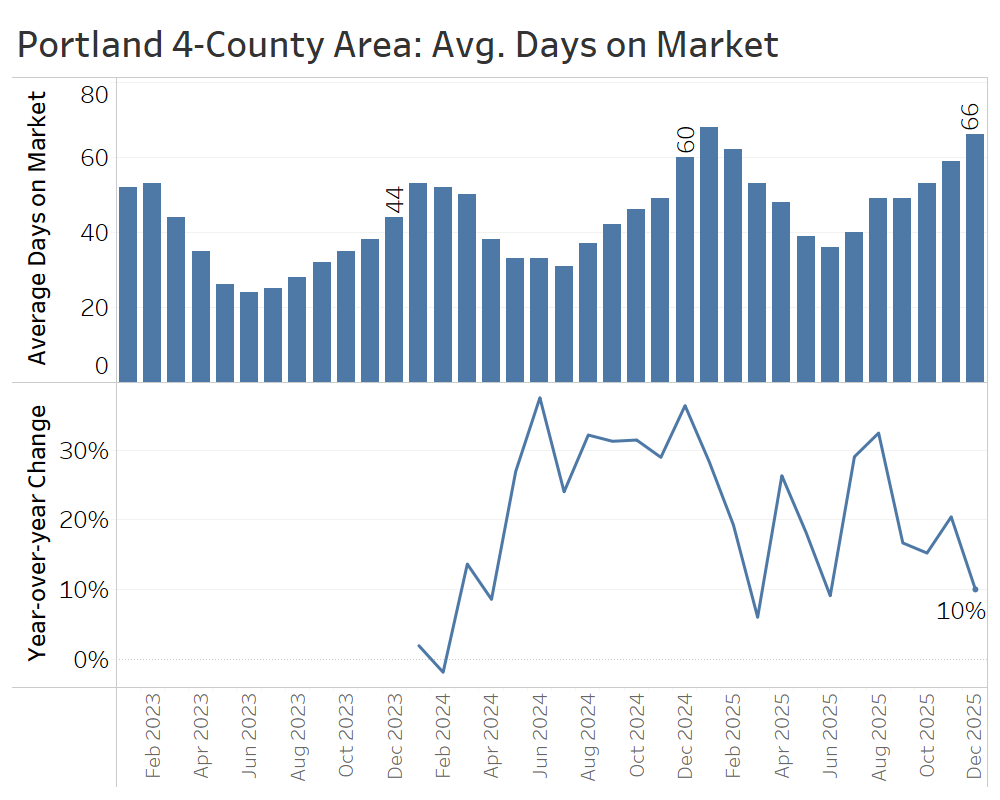

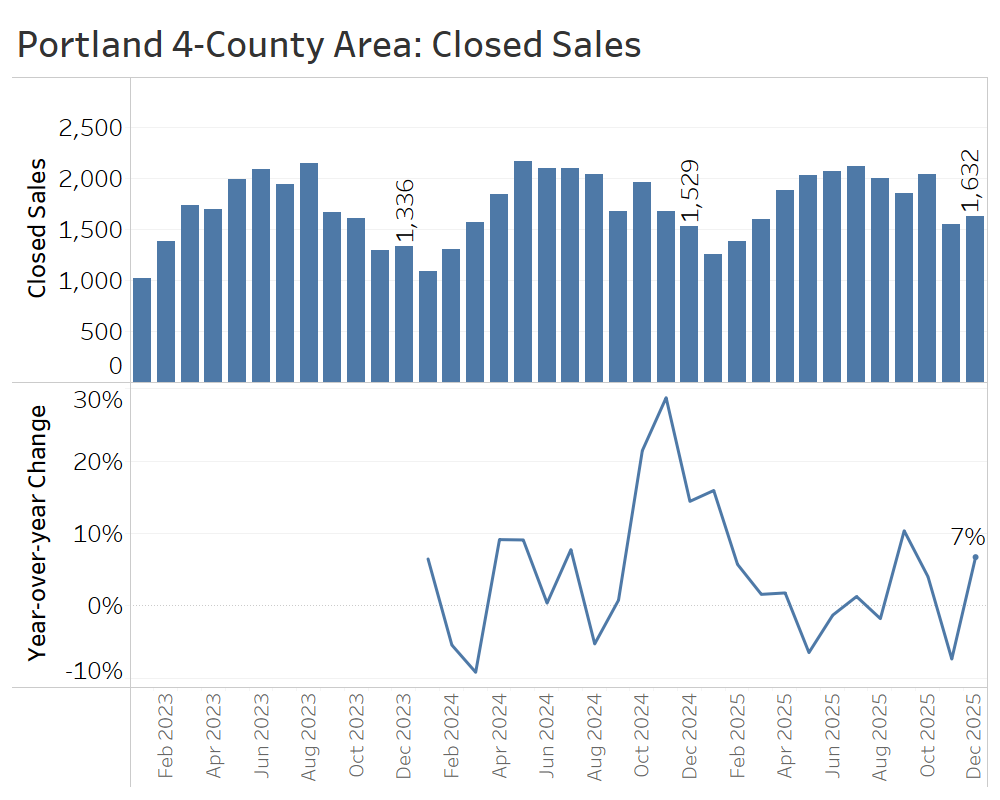

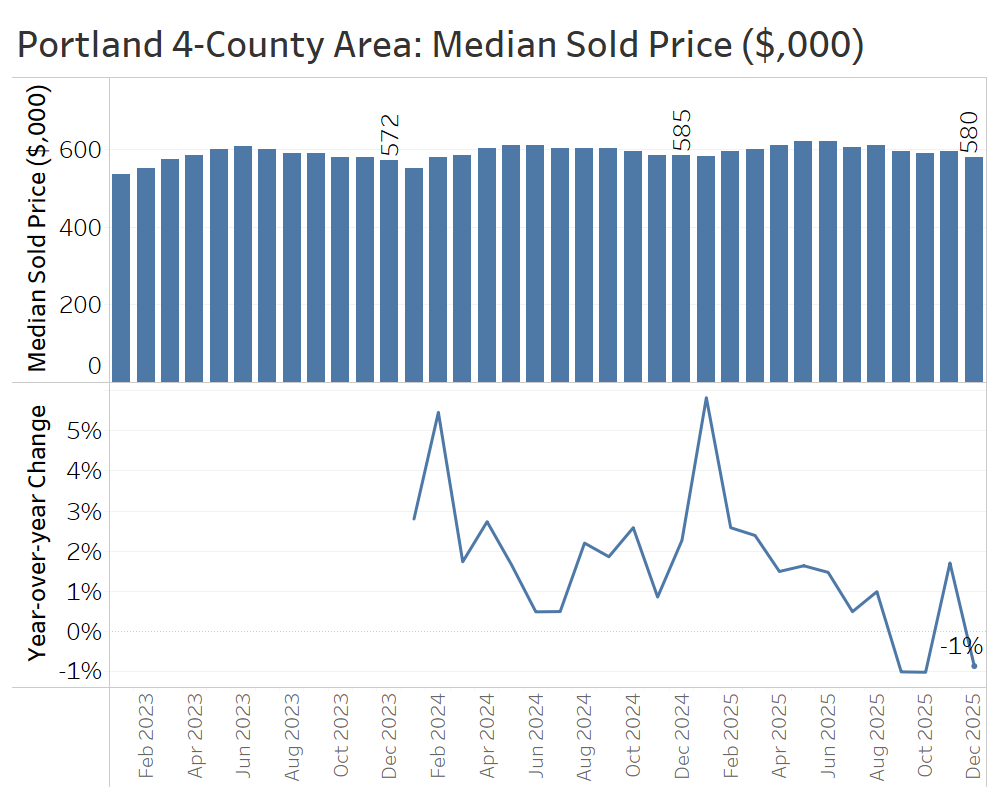

Greater Portland Area (Multnomah, Washington, Clackamas, and Clark Counties)

The Greater Portland Area notched another quiet quarter of normalization to round out 2025, with modestly rising inventory and slightly lower prices than 2024.

Active listings ended the year at 3,788, or 13% higher than the previous year. That continues a trend of decelerating inventory growth since May.

New listings in the fourth quarter of 2025 remained below fourth-quarter 2024 levels for the third straight month, capped by a 5% decline in December, traditionally the quietest month for new listings. The slower inflow of listings to the market has contributed to the more modest inventory growth seen above.

The average home sold after 66 days on the market—about six days longer than December 2024. Homes that linger for several months often end up selling below their original asking price, a trend that has increasingly worked in buyers’ favor in the fourth quarter.

Closed sales of single-family homes rose 7% year over year in December, following a significant dip in November. Overall, the 5,221 closed sales in the fourth quarter narrowly exceeded the 5,162 sales recorded in the final quarter of 2024, suggesting that more buyers were motivated to get off the fence this fall.

Median home sale prices in the Portland area edged down slightly, ending the year at $580,000 – about 1% below December 2024. Paired with the rebound in sales, this suggests buyers were able to negotiate for some deals at the end of 2025.

The fourth quarter continued to demonstrate the downstream effects of higher inventory in the Portland area: it helped attract buyers and support affordability, while also discouraging some sellers who are likely waiting to list.

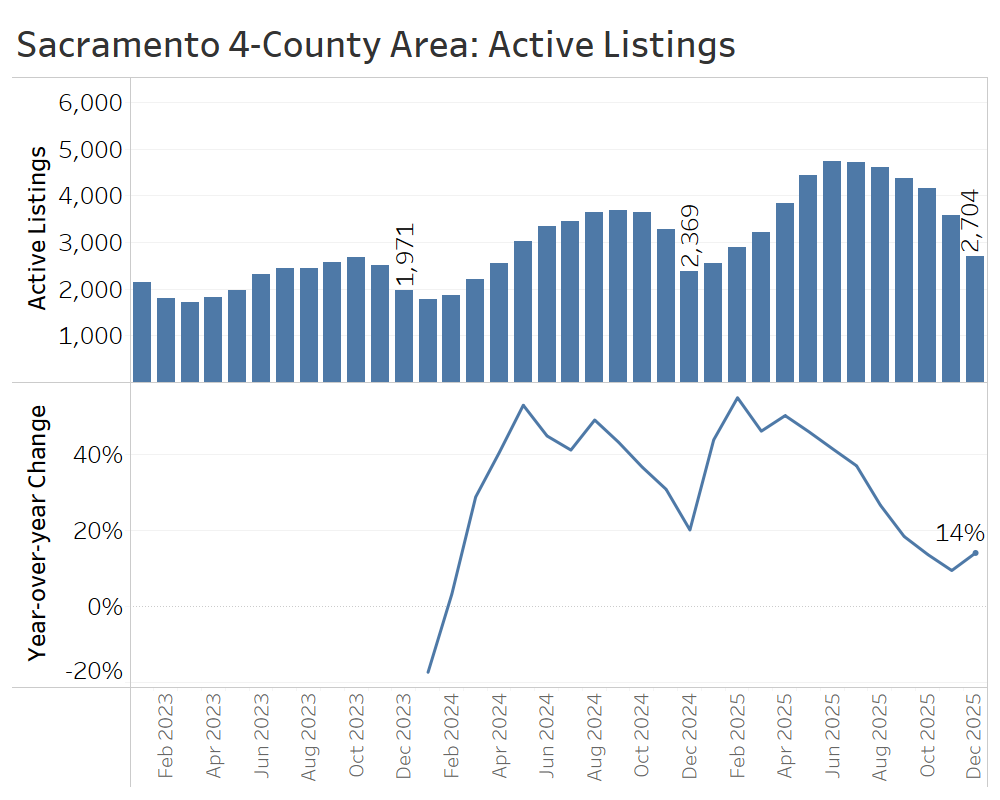

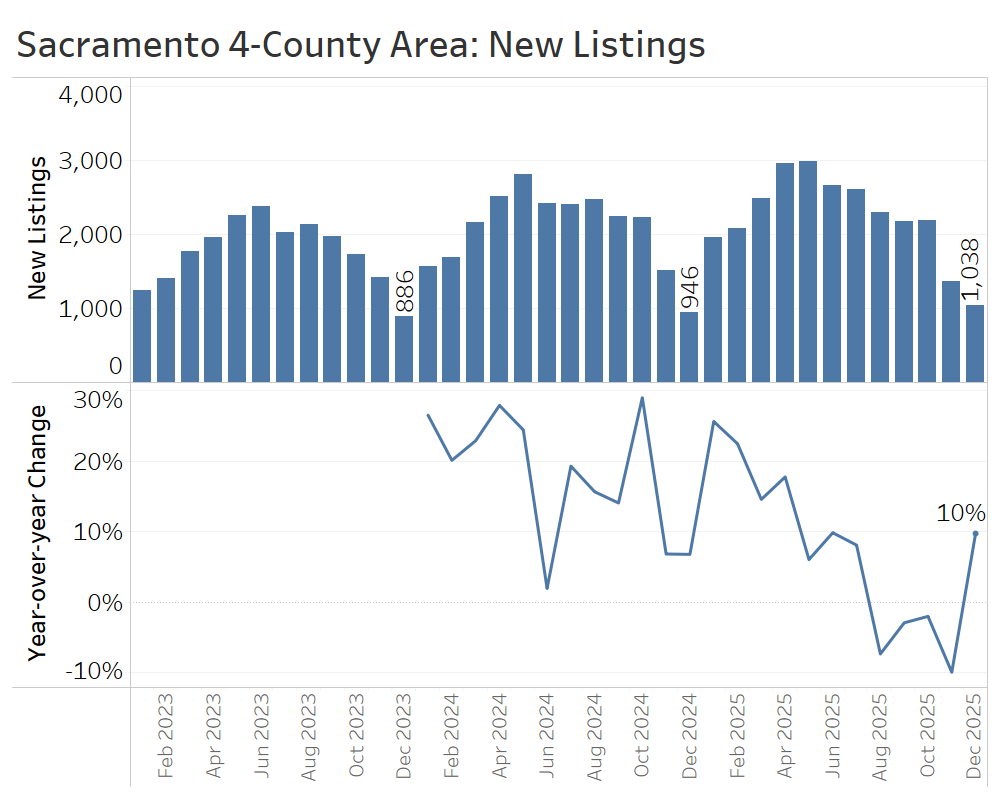

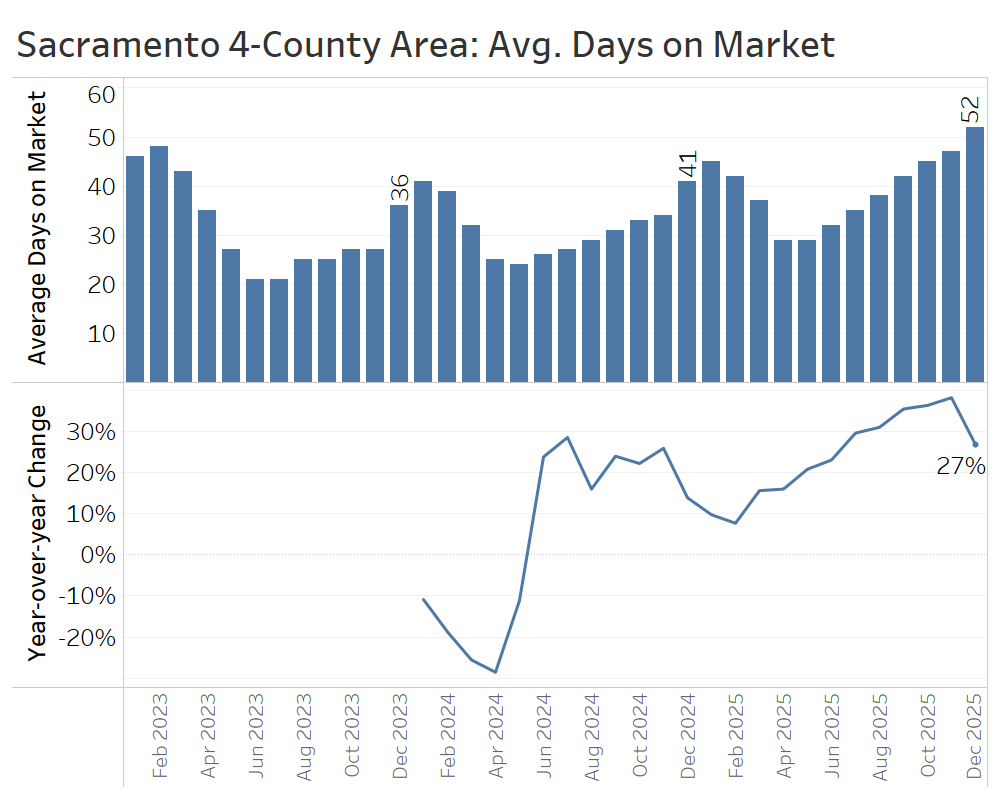

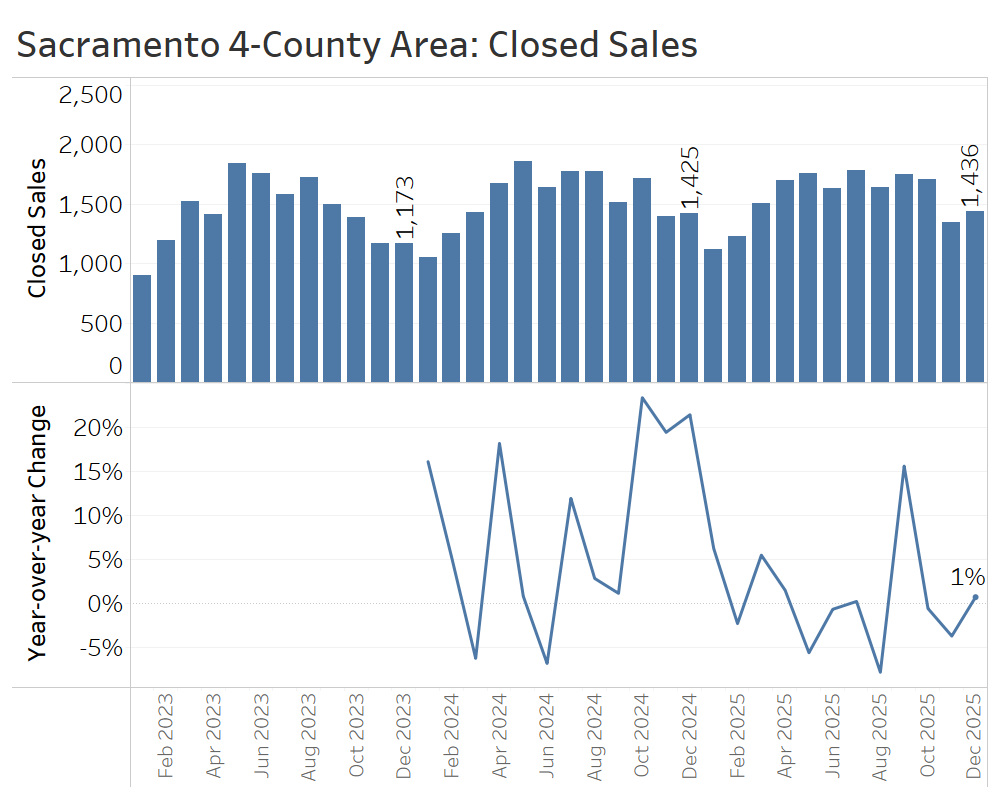

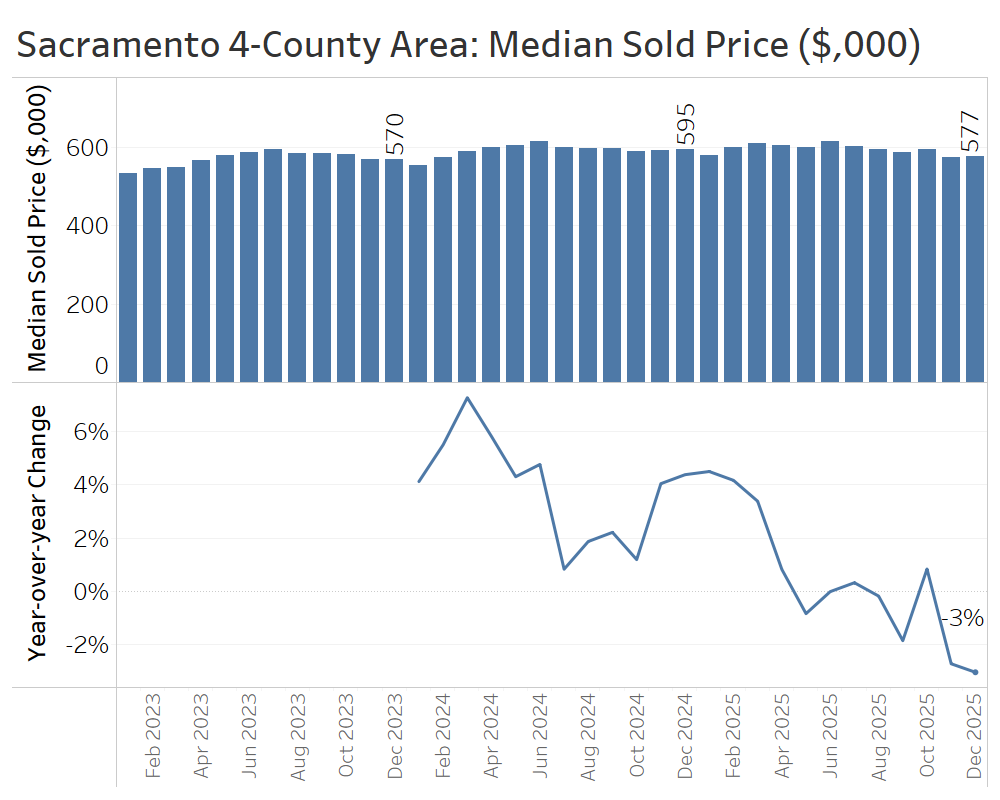

Greater Sacramento Area (Sacramento, Yolo, El Dorado, and Placer Counties)

The Greater Sacramento Area is another market where the advantage has decisively shifted in favor of buyers. Inventory has climbed, prices have cooled, and sales activity has remained relatively flat.

At the end of December, there were about 2,700 active listings—an increase of 14% compared to the end of 2024. Overall, inventory growth in the fourth quarter was much more modest than in early 2025, when listings were up 50% or more compared with 2024.

New listings ran below December 2024 levels for four straight months, before ticking up 10% in December 2025—a modest boost to end the year.

Average days on market rose by about 11 days compared to December 2024, reaching 52 days. While this eases some of the pressure on home shoppers, seasonal trends are likely to bring the number down later in the first quarter.

Sales activity in the fourth quarter of 2025 was remarkably similar to the fourth quarter of 2024, with nearly 4,500 homes sold in 2025 compared with just over 4,500 the year before.

Median sale prices fell 3%, from around $595,000 in December 2024 to $577,000 in December 2025. The main causes of the softer pricing were higher inventory and longer time on market.

The fourth-quarter takeaway in the Greater Sacramento Area is that buyers came to appreciate and act on their greater negotiating power, winning some bargains while sales volume remained basically flat.

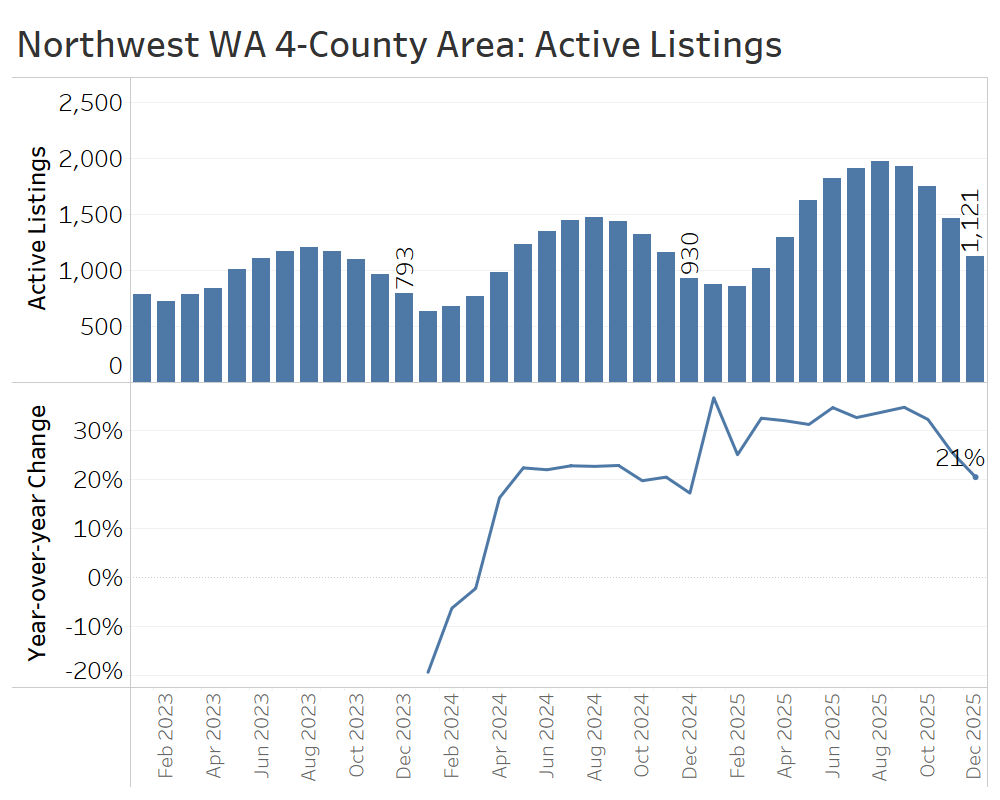

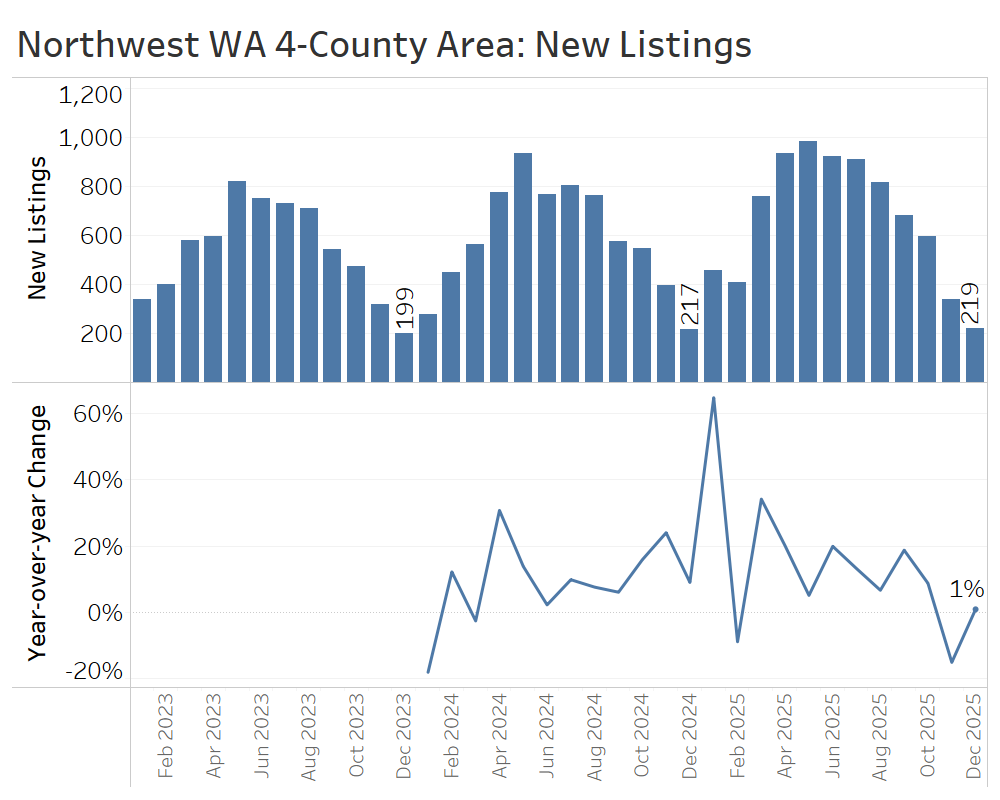

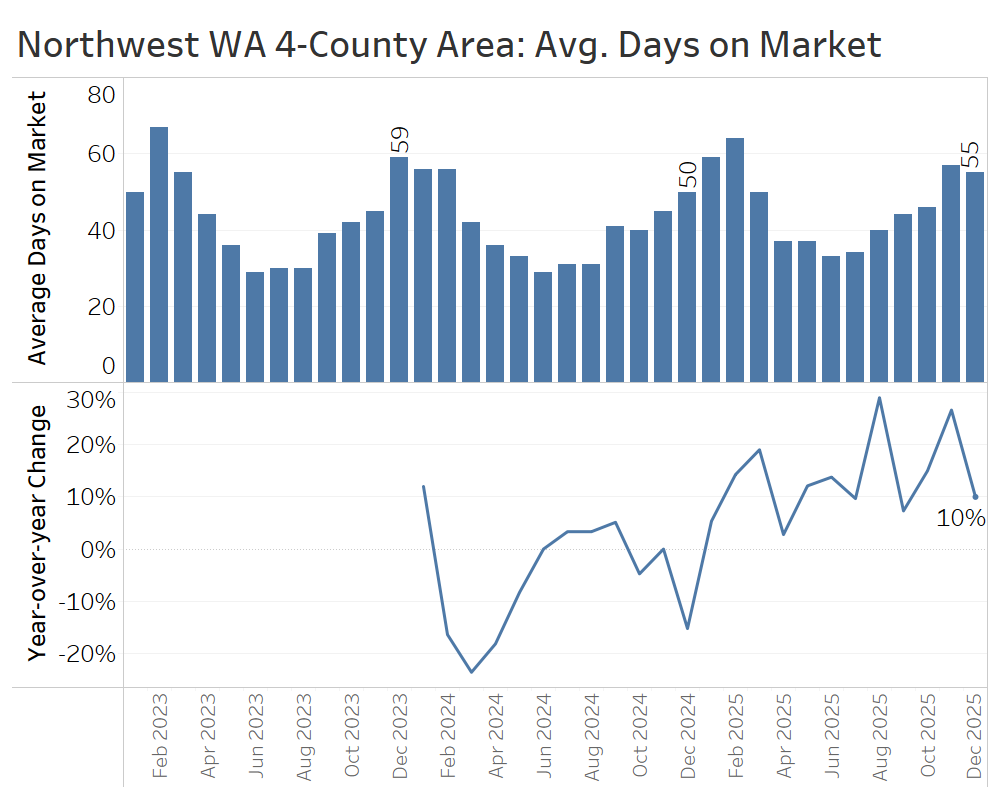

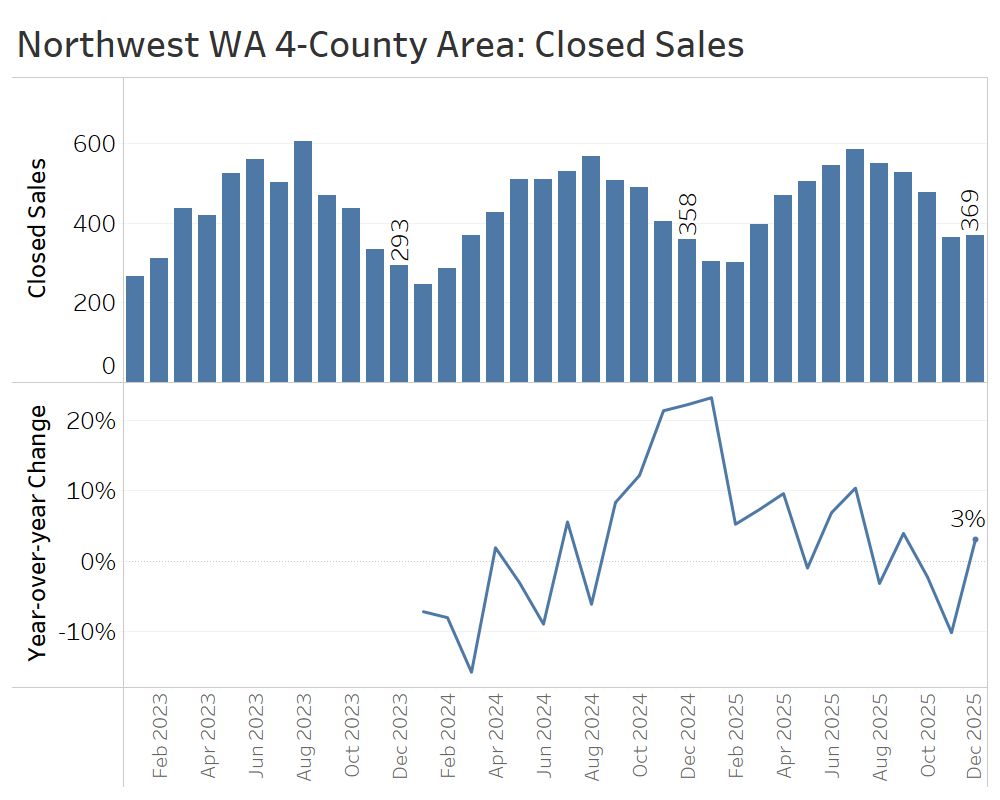

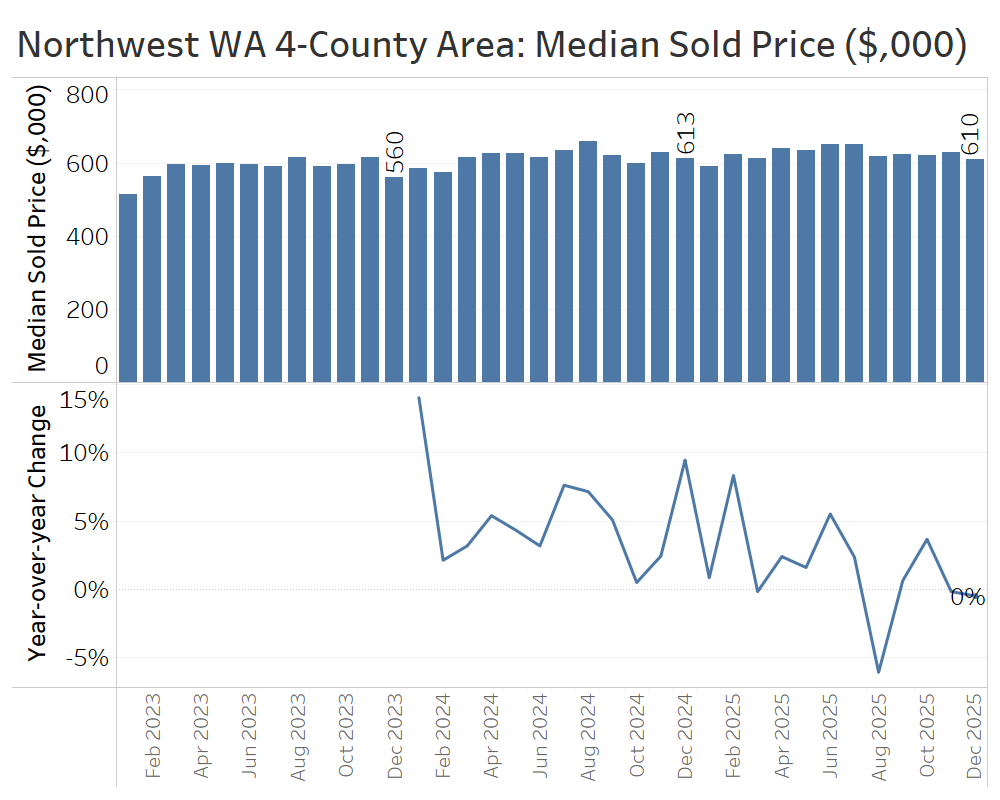

Northwest Washington (Skagit, Whatcom, San Juan, and Island Counties)

The market conditions in the four northernmost counties of Western Washington are experiencing a major shift in favor of buyers.

At the end of December, there were 1,121 active listings, up 21% from a year earlier. That marked a slowdown in inventory growth in the fourth quarter, down from increases of 30% or more in the middle of the year.

The flow of new listings fell sharply in the fourth quarter, even by seasonal standards. Some listings may have been affected by flooding during the atmospheric rivers that slammed Washington State; others may have been withheld by sellers clued into the cooler selling conditions.

Days on market continued to climb compared to a year earlier, with homes in December taking about five days longer to sell than they did at the same time a year earlier.

Closed home sales in the fourth quarter of 2025 generally trailed fourth-quarter 2024 levels, except for a modest uptick in December. In total, the 1,210 closed sales for the quarter fell about 4% short of the 1,251 homes sold in the fourth quarter of 2024.

Compared to the same time the previous year, median home prices were virtually flat in November and December, after a brief bump in October. This marks a continuation of the cooldown of price growth that had characterized 2024 and early 2025.

Fourth quarter confirmed that higher inventory levels finally gave buyers more negotiating leverage in Northwest Washington.

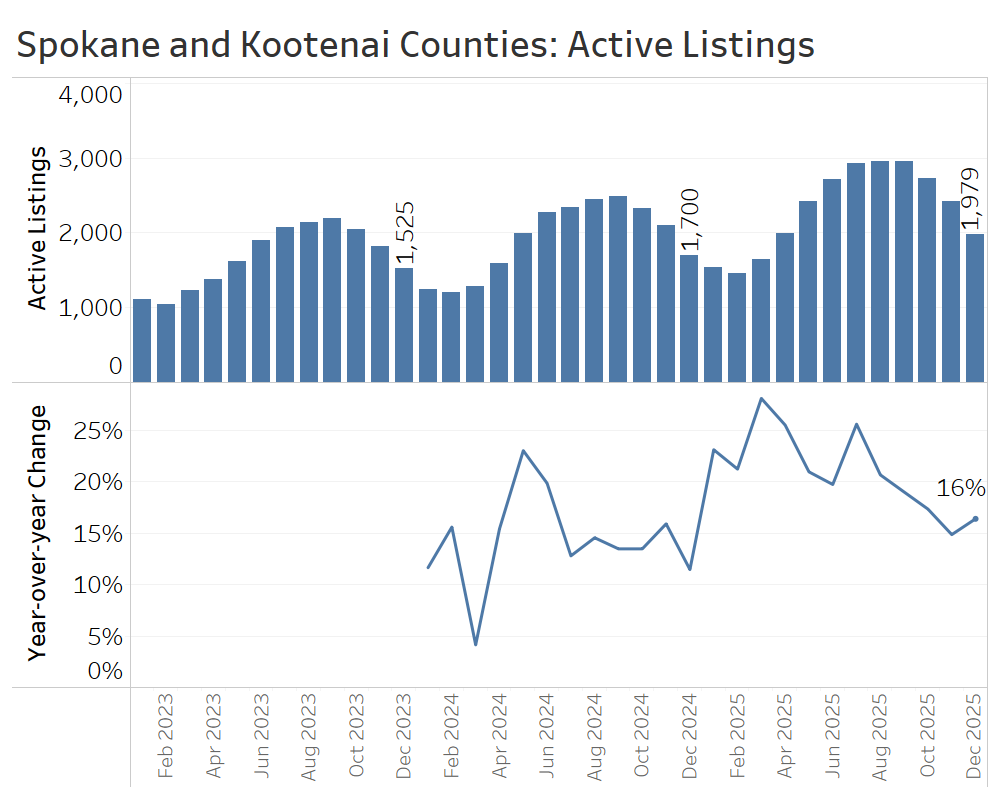

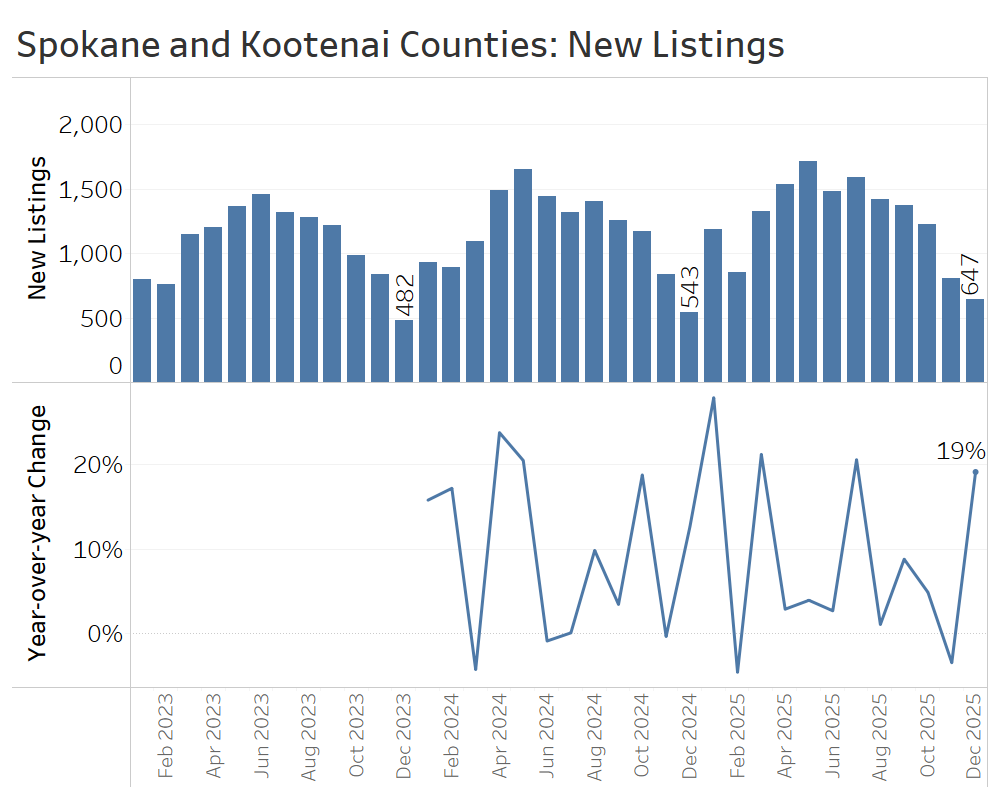

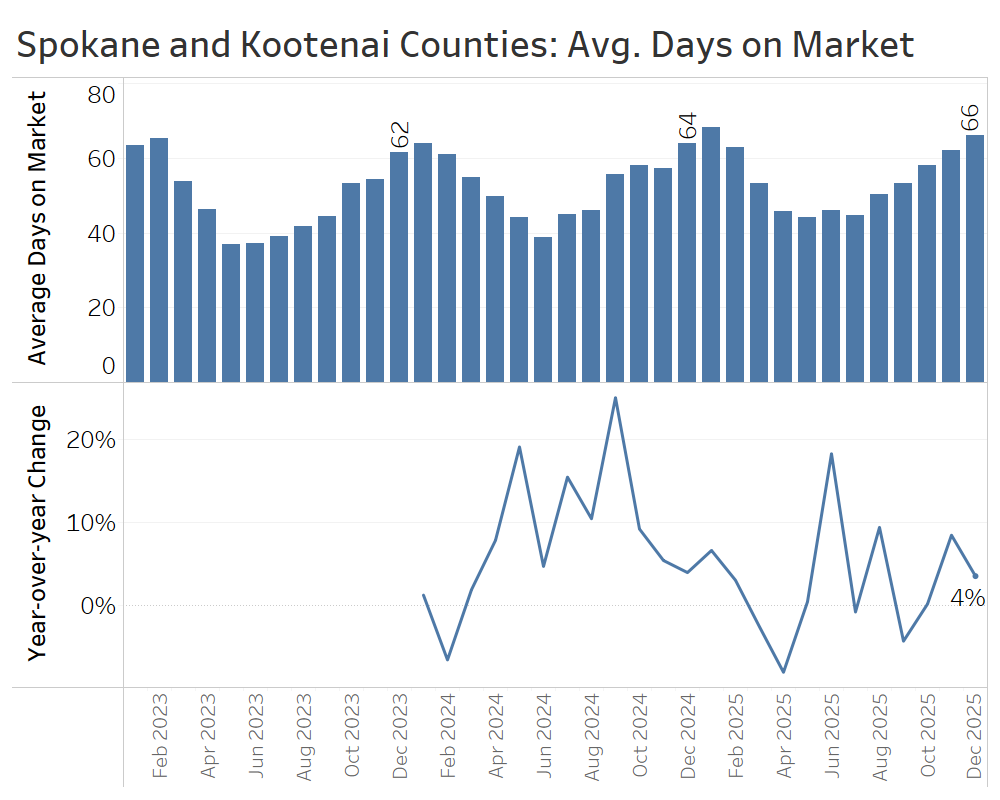

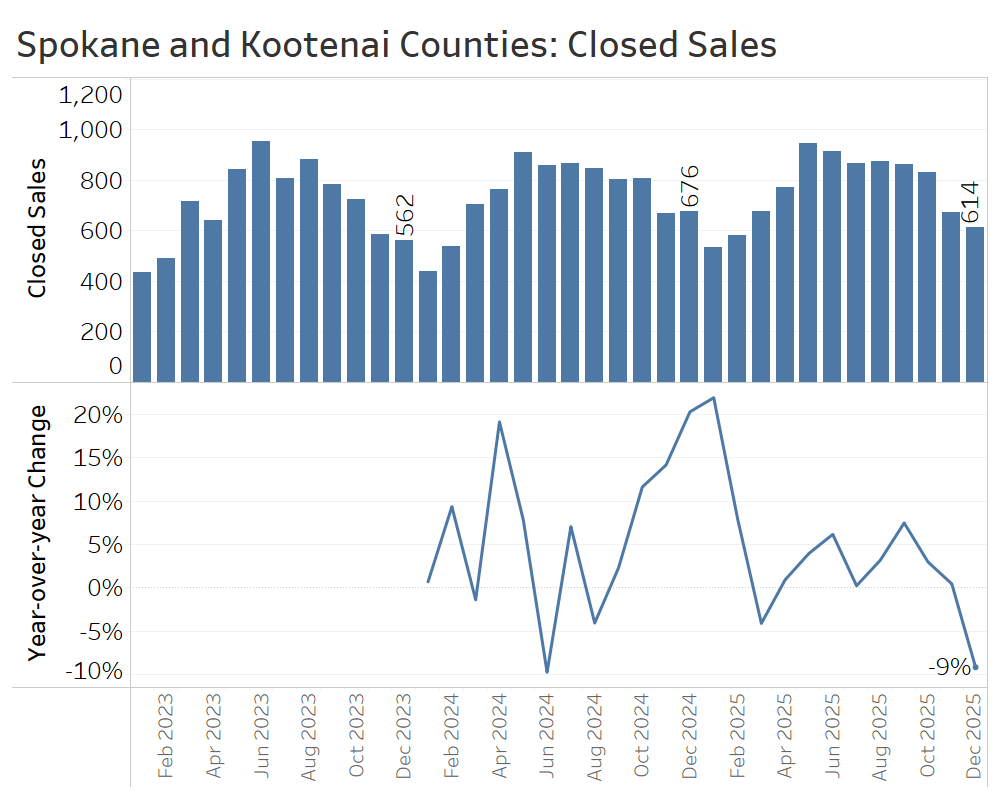

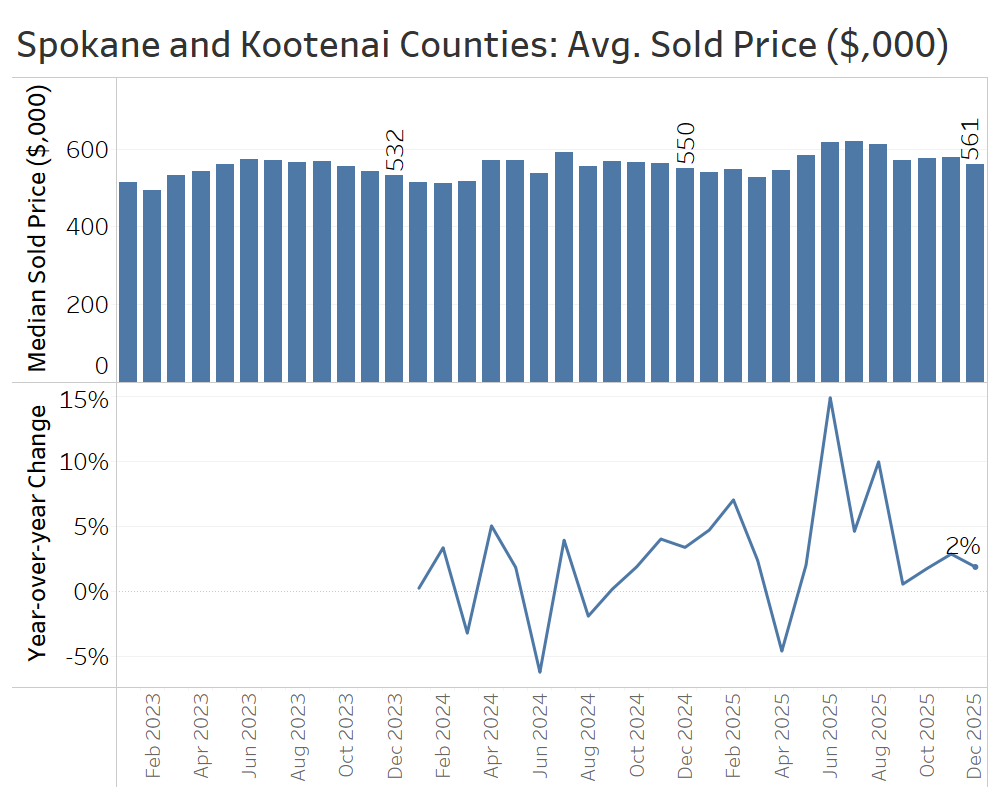

Spokane, WA and Coeur d’Alene, ID Area (Spokane and Kootenai Counties)

The greater Spokane-Coeur d’Alene region, spanning the Washington-Idaho border, is experiencing many of the same market trends seen in Western Washington, including higher inventory, softer buyer demand, and flattening home prices.

At the end of December, there were 1,979 active listings, up 16% from December 2024. That represented a modest slowdown in inventory growth from the year-over-year increases of more than 20% seen earlier in 2025.

New listings jumped 19% compared to December 2024, but month-to-month changes in new listings were quite volatile. During the quarter as a whole, there were 2,681 new listings, up from 2,549 in the fourth quarter of 2024, representing a 5% increase.

The pace of home sales, which is measured by days on market, only crept up modestly in the fourth quarter, ending the year at 66 days in December. However, that average obscures a wide divide across the state line, with homes averaging 47 days on market in Spokane County compared with 106 days in Kootenai County.

Closed sales in December were down 9% year-over-year, and the quarter also saw a modest decline. Sales slipped from 2,152 in the fourth quarter of 2024 to 2,117 in the fourth quarter of 2025.

Because of challenges associated with combining data from multiple MLSs, we report average sale prices rather than medians for the Spokane-Coeur d’Alene area. Compared with December 2024, the average sale price in December rose about 2%, from $550,000 to $561,000. For the quarter as a whole, average prices also increased 2%, rising from $560,000 in the fourth quarter of 2024 to $572,000 in the fourth quarter of 2025.

That increase was driven entirely by higher average sale prices in Kootenai County, where prices climbed 8%, while average prices in Spokane County fell 2%.

Altogether, the shift towards a buyer’s market in the greater Spokane-Coeur d’Alene area began to flatten prices without yielding an increase in sales. Many metrics diverged across the Washington-Idaho border, with evidence of resilient demand for homes at Coeur d’Alene’s higher price points, while demand lagged in Spokane County.

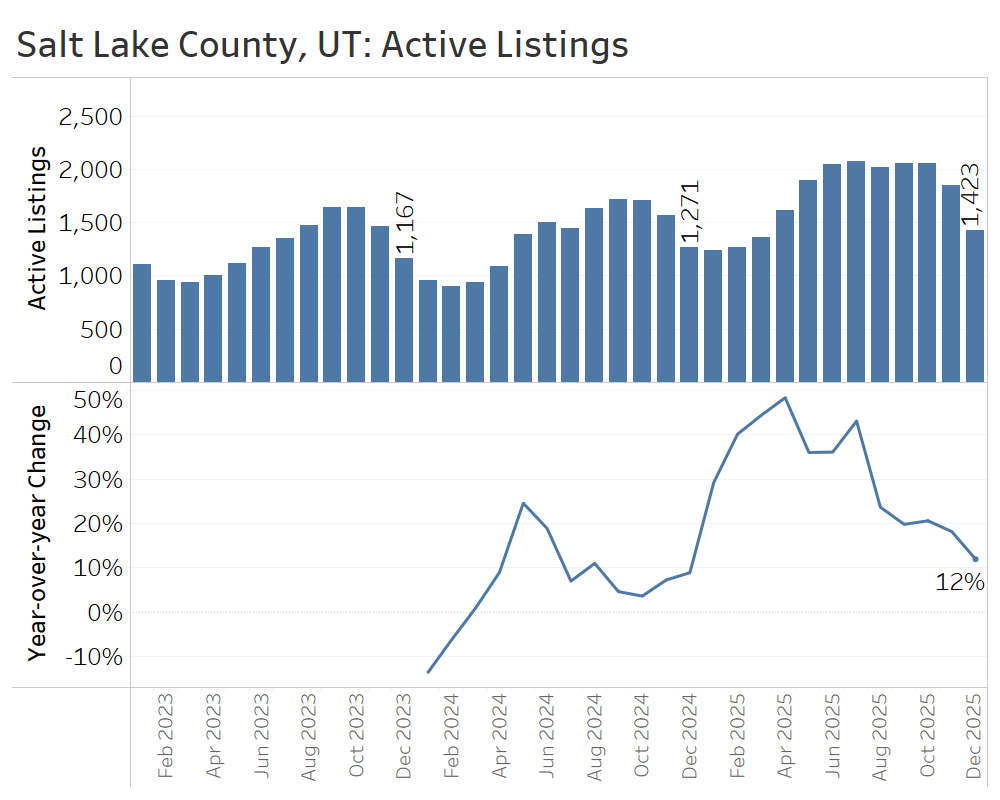

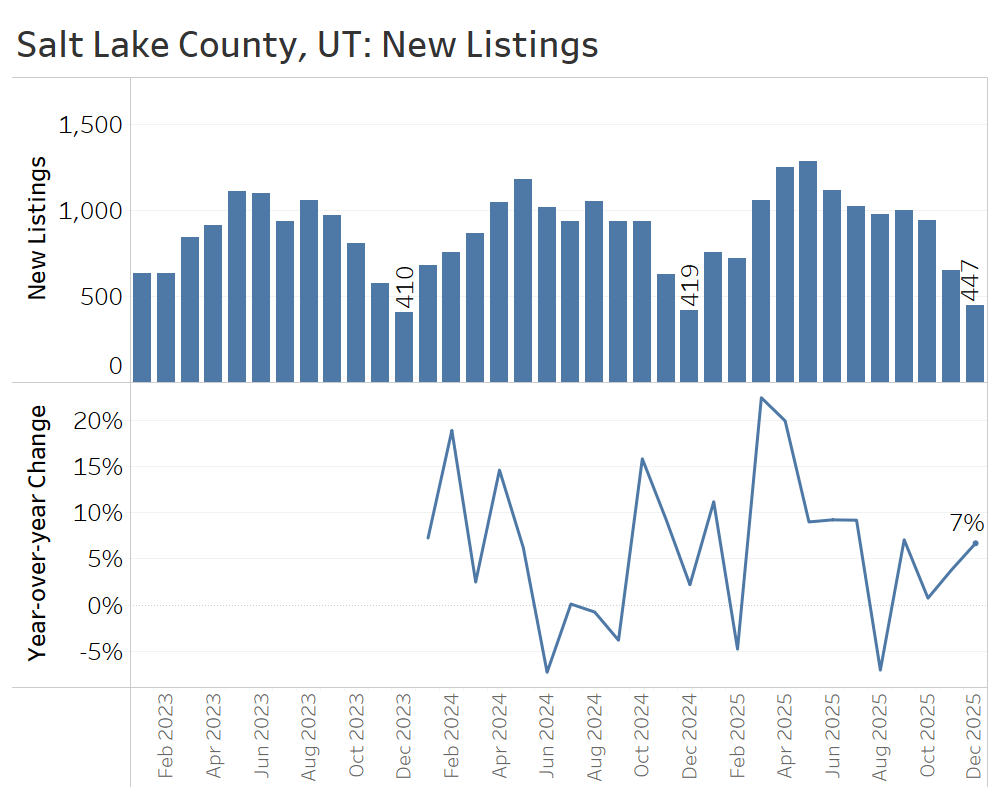

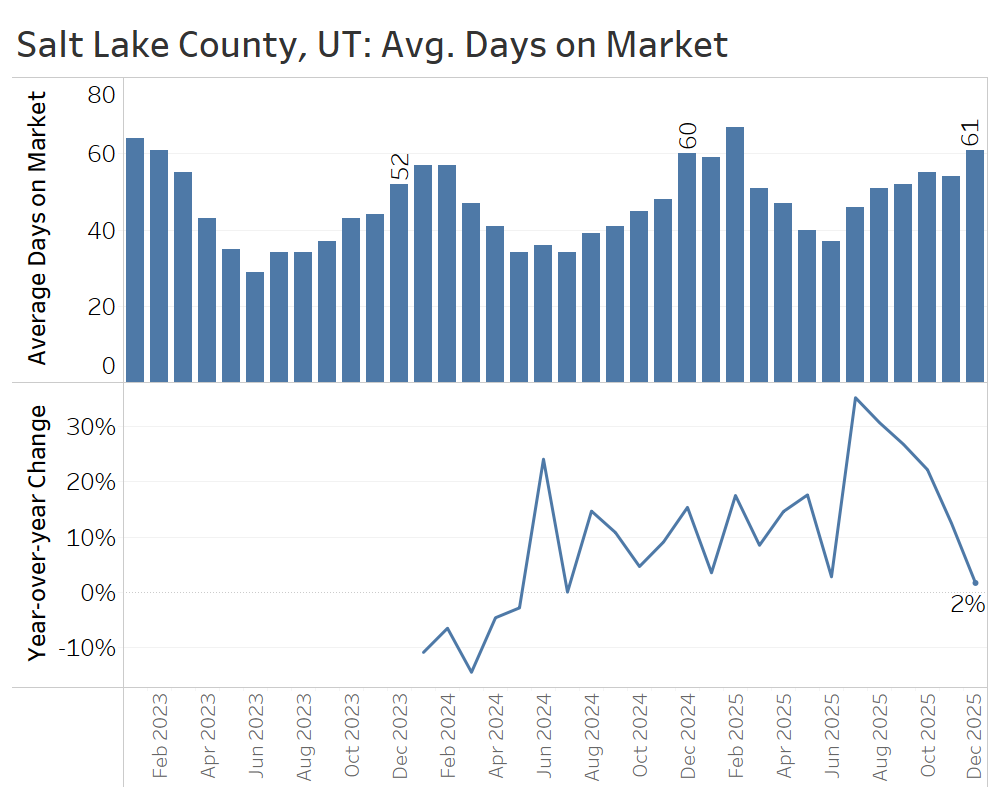

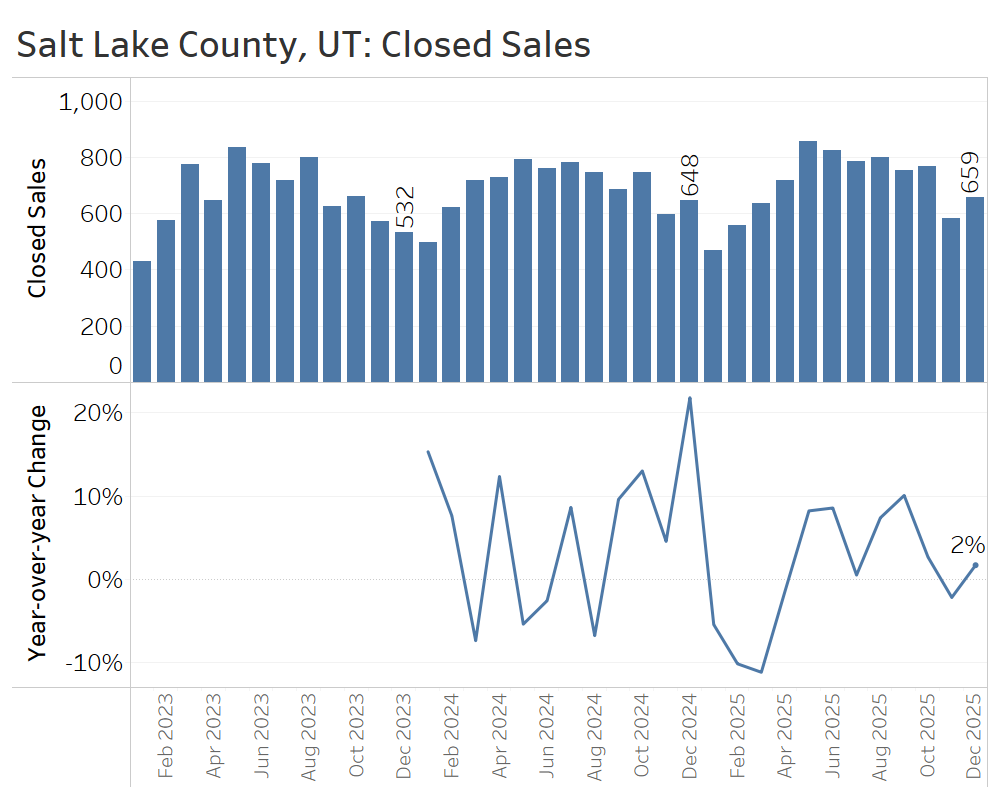

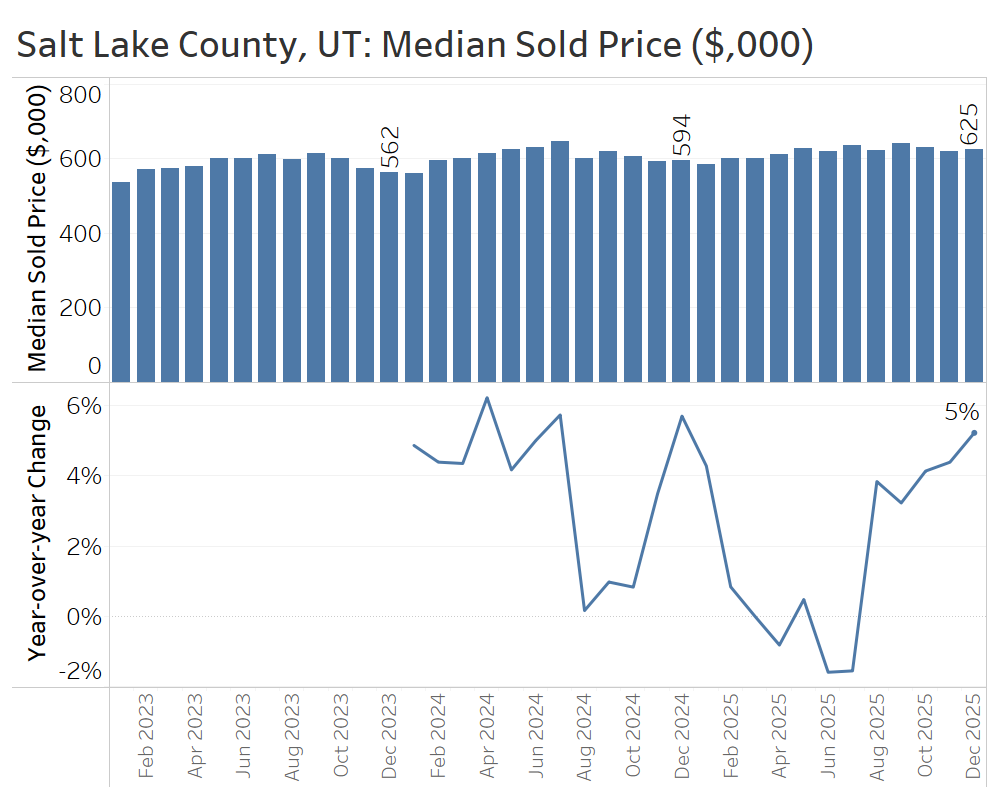

Salt Lake County, Utah

Market conditions in Salt Lake County swung sharply in buyers’ favor early in 2025, as rapid inventory growth led to modest price declines. More recently, however, the market has begun to look more balanced rather than distinctly a buyer’s market.

Active listings at the end of December stood at 1,423 homes, up 12% from a year ago—a major slowdown from the 43% inventory growth seen in July of last year.

Salt Lake County experienced strong year-over-year growth in new listings early in 2025, exceeding 20% in March and April, but slowing to just 7% growth in December. The waning seller enthusiasm is helping to rebalance the market.

The average number of days it took to sell a home in Salt Lake County ended the year at 61 days, just slightly longer than the 60-day average at the end of 2024.

Closed home sales in December 2025 rose 2% compared to December 2024, capping a fourth quarter that roughly matched the strong sales seen in the same period the year before.

In December, the median sale price in Salt Lake County rose 5% year over year—from $594,000 to $625,000. That marked the fifth straight month of price gains, reversing a trend of modest price declines in mid-summer.

All in all, Salt Lake County has shifted into a more balanced market, driven by modest price growth and a slowdown from the significant inventory buildup seen earlier in 2025.

Conclusion:

All of the markets covered in this report shifted in buyers’ favor in 2025, though some, like Salt Lake County, show that the pendulum can—and will—begin to swing back toward more balanced conditions.

Going forward, buyers should be aware that in most markets, there are more listings than in recent years, home prices have remained roughly flat for at least a year, and mortgage rates are near three-year lows. Together, these factors create a strong opportunity to buy. That said, buyers should also be mindful of the usual spring surge in competition, which will accelerate home sales and push prices higher, as it does every year. Savvy buyers can try to get ahead by shopping earlier, but they should also be prepared to write a competitive offer if their ideal home hits the market this spring.

For sellers, the peak selling season is fast approaching. But even in a more balanced market, homes do not sell themselves. The best outcomes still depend on presenting the home well, setting the right list price, and marketing effectively to the right buyers. With the right strategy, this spring presents a great opportunity to sell for the best possible price, especially as lower mortgage rates bring more buyers off the fence.

Sources: TrendGraphix analysis of NWMLS, RMLS, Spokane MLS, MetroList MLS, and Wasatch Front MLS data.

Buying a home is a major milestone, and it comes with a lot of decisions, details, and moving parts. While online searches and market headlines can offer helpful context, there’s no substitute for having a knowledgeable real estate professional by your side.

The right agent does more than show homes. They help you understand the market, weigh opportunities, and make informed choices at every stage of the process. Asking thoughtful questions early on can set the tone for a smoother, more confident homebuying experience.

Here are some of the most important questions every buyer should ask their real estate agent, and why they matter.

Ask Them About Themselves

Choosing a real estate agent is about more than credentials and experience; it’s also about fit. Before deciding who to work with, take time to get to know your agent as a person.

Ask them about their background, how they work, and what drew them to real estate. Having an agent with a similar communication style, lifestyle, or understanding of your priorities makes the process feel more comfortable and collaborative. At the end of the day, this is someone you’ll be working closely with during one of the most important life decisions, so feeling aligned and understood matters.

What Services Do You Provide Me as My Agent?

Real estate agents offer a wide range of services, and not all approaches look the same. That’s why it’s essential to understand exactly how an agent will support you throughout the buying process.

Ask what services they provide from start to finish–such as market research, property tours, negotiation, inspection, and coordination through closing. You may also want to ask what tools or resources they use, and how involved they are at each stage.

In addition, it’s helpful to ask whether your agent can recommend trusted service providers—such as lenders, inspectors, contractors, or other professionals who can assist with financing, repairs, and other tasks that come up before closing. Having access to a reliable network can help streamline the process and reduce stress.

What’s Happening in the Market Right Now?

Real estate markets are constantly evolving, and what’s happening nationally doesn’t always reflect what’s happening locally. Ask your agent:

How is the market performing in the areas I’m considering?

Are homes selling quickly, or are buyers taking more time to decide?

What trends should I be aware of at my price point?

What strategies are working well for buyers right now?

A strong agent will provide local insight and context, helping you understand not just the numbers, but what they mean for you as a buyer.

How Should I Prepare Financially Before I Start Making Offers?

Being financially prepared goes well beyond getting pre-approved. While your lender will guide you through financing specifics, your real estate agent plays a key role in helping you understand how those details shape your overall buying strategy.

Your agent should help you think through what sellers are typically looking for in an offer, how loan terms, contingencies, and timelines can influence negotiations, and how to plan for additional costs before, during, and after the purchase.

What Should I Prioritize and Where Can I Be Flexible?

Most buyers begin their search with a list of wants and needs, but flexibility can often open the door to better opportunities.

A knowledgeable agent can help you identify which features are essential and which are optional, understand how factors like location, layout, and condition affect a home’s value, and balance your lifestyle preferences with long-term considerations. An experienced agent brings perspective, helping you see the bigger picture while keeping your goals front and center throughout the process.

What’s Your Approach to Pricing and Making an Offer?

Every offer should be strategic and tailored to the situation. Your agent should be able to clearly explain how they evaluate pricing and market value, what factors influence offer terms beyond price, and how inspections, contingencies, and timing play a role in negotiations.

Having this conversation early helps ensure you’re aligned and confident when it’s time to move forward, with a clear understanding of how your agent will advocate for you in a competitive and nuanced market.

How Will We Communicate Throughout the Process?

Clear communication is essential during a home purchase. Be sure to ask:

How often can I expect updates?

What’s the best way to reach you with questions?

How do you handle time-sensitive situations?

You should also ask what will be included in your written buyer agreement so you can have a clear understanding of roles and responsibilities. The right agent will set expectations early and make sure you feel informed and supported at every stage, from start to finish.

What Should I Know About a Home Before Making a Decision?

Once you’ve found a home you’re excited about, your agent’s guidance becomes even more important. They should help you understand:

How the home compares to similar properties.

What to expect during inspections.

Any potential considerations that could impact your decision.

This step isn’t about creating doubt; it’s about ensuring clarity, confidence, and peace of mind.

If you’re considering buying a home, start with a conversation. Asking the right questions and working with an experienced real estate agent can help you navigate the homebuying process with confidence.

This is the latest in a series of videos with Windermere Principal Economist Jeff Tucker, where he delivers the key economic numbers to follow to keep you well-informed about what’s going on in the real estate market.

2026 is already proving to be a busy news year for the housing market, starting with our first number to know:

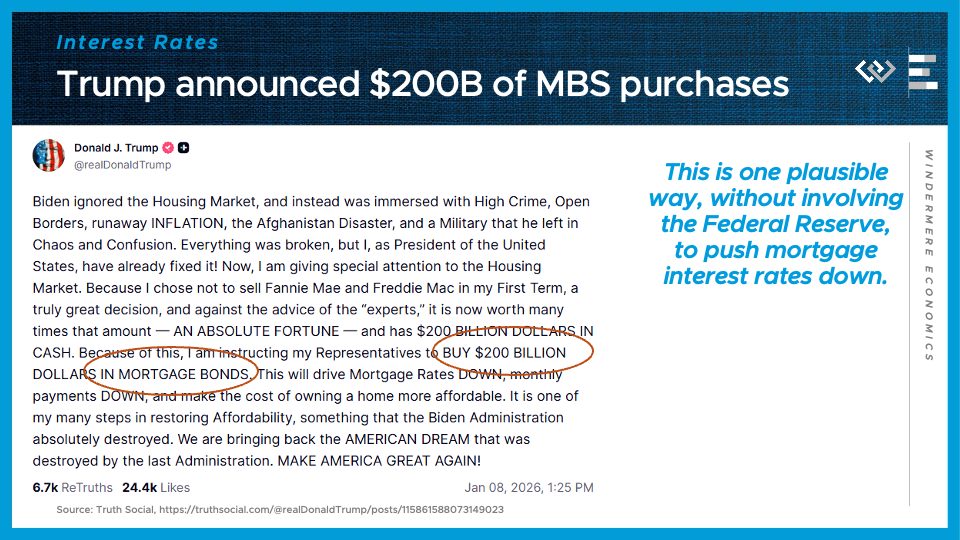

$200 billion

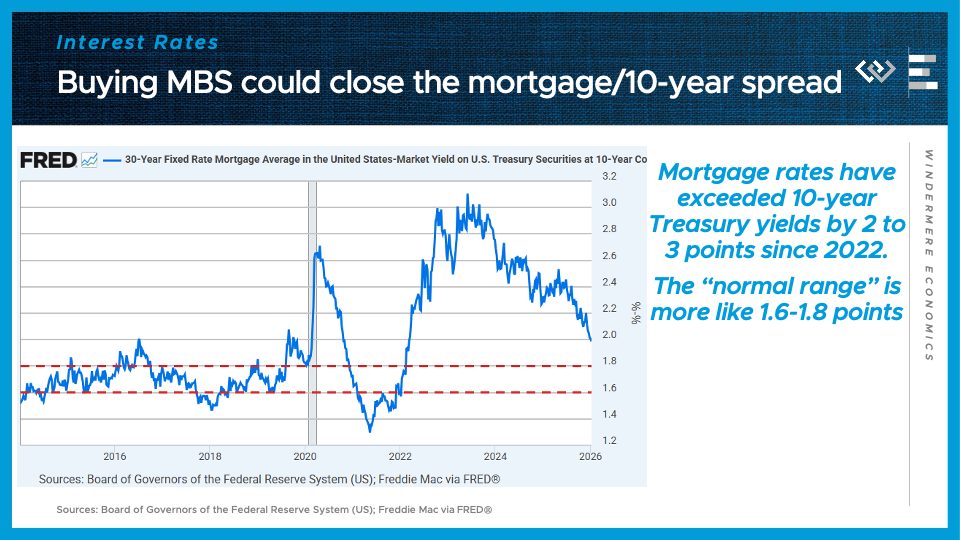

That’s the total value of mortgage-backed securities that President Trump announced on January 8th he’s directed “his Representatives” to purchase, with a stated goal of reducing mortgage interest rates. A big new buyer of mortgages will tend to bid their prices up, which – for bonds – means pushing interest rates down.

For the last 3 years, mortgage rates have been unusually high relative to the benchmark 10-year Treasury rate, which has been gradually compressing back to a normal range, and this buying spree, evidently by Fannie Mae and Freddie Mac, should accelerate that process of shrinking the spread.

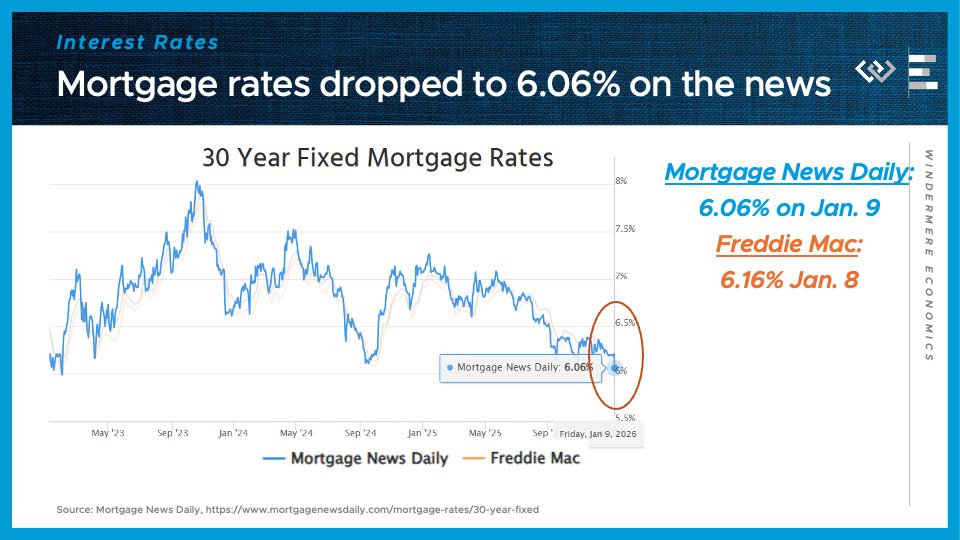

Markets have taken this announcement quite seriously. In just the first day of trading after Trump’s announcement, mortgage rates dropped 15 basis points, bringing us to our second number to know right now:

6.06%

That was Mortgage News Daily’s average 30-year mortgage rate on Friday, January 9th, and that marks the lowest mortgage rate they’ve reported in almost 3 years. Now – trading has been unusually volatile, and there are still a lot of unanswered questions about this new program, but there’s no doubt that in the short term, it has begun moving markets, and I think SOME highly qualified buyers and sellers who start to see mortgage rates in the 5% range will be more motivated to transact this spring.

Another number to know right now:

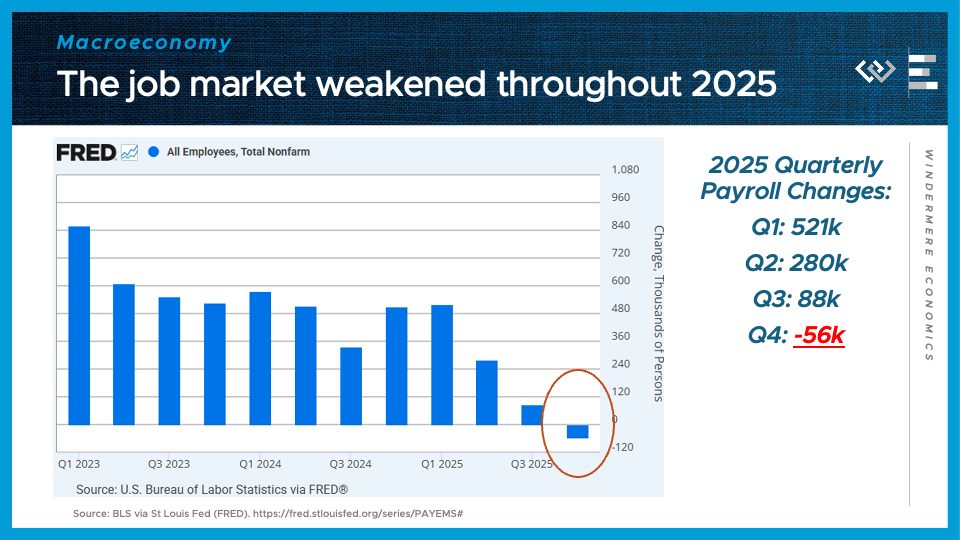

56,000

That’s the number of jobs lost on net over the fourth quarter of 2025, capping a year of slowing, and finally shrinking, payrolls in the U.S. economy. Now, other data shows economic activity held up fine in the fourth quarter, so this is not the beginning of a recession, but slowing job growth could help explain why home purchases disappointed in the fourth quarter, despite lower mortgage rates than in late 2024.

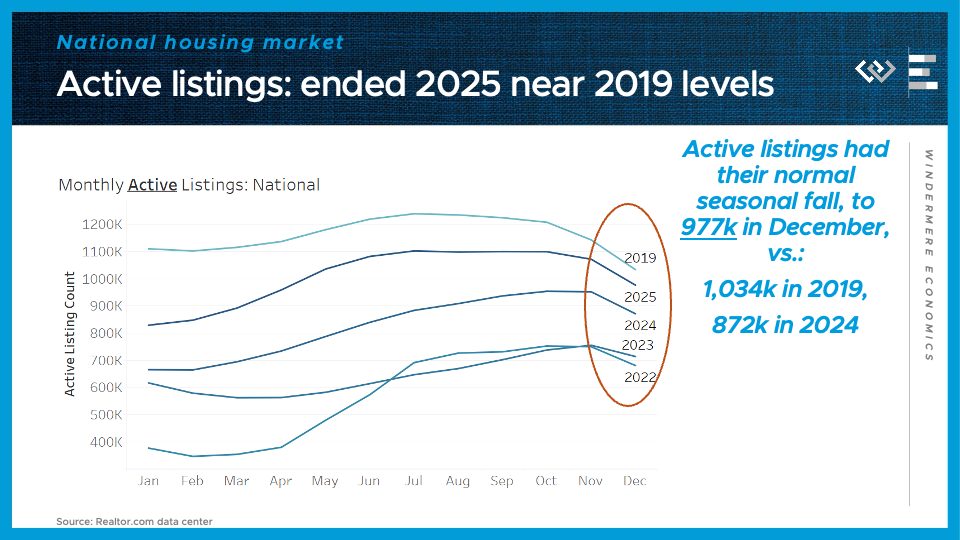

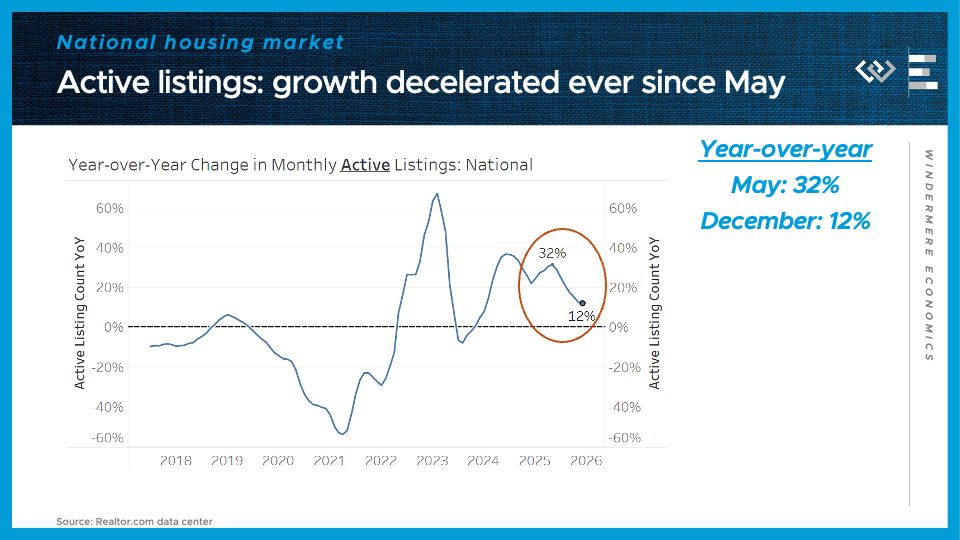

Speaking of housing, 2025 ended with the housing market still just shy of an important benchmark I’ve been watching: the moment when active inventory recovers to its pre-pandemic, 2019 levels. The year ended with just under a million active listings, vs just over a million 6 years ago on the eve of the Covid pandemic.

That is still up substantially from this time last year, but the trend of year-over-year listing growth clearly slowed over the course of 2025. That helps explain why 2025 went down as the year of cooling and normalization, but NOT anything like a fire sale or glut of unsold homes. Rather, it’s a market that made a lot of progress back toward normalcy, foretelling a healthy, balanced market in the year ahead.

Homeownership isn’t a one-size-fits-all, and neither are the financial decisions that come with it. At some point, many homeowners reach a familiar fork in the road: Should I refinance my mortgage, or is it time to sell?

The right answer depends on a mix of factors, including your financial health, today’s interest rate environment, your home’s equity, and where you see yourself and your household in the next few years. Let’s walk through both options so you can decide what makes the most sense for you, not just on paper, but in real life.

Refinancing vs. Selling

If your current mortgage no longer feels like the right fit, you generally have two paths forward: refinancing or selling. Refinancing your home allows you to renegotiate the terms of your existing loan, potentially changing your interest rate, loan term, or monthly payment. Selling, on the other hand, can free up equity and open the door to your next chapter. So, how do you decide between the two? The key is to understand what each one offers and what it requires so you can move forward with confidence.

Refinancing Your Home

There are a few reasons homeowners typically refinance their mortgages, the most common being falling interest rates. Lower interest rates after a mortgage reassessment translate into lower monthly payments and significant savings over the life of the loan. If your finances have improved since you initially secured your mortgage—for example, your debt-to-income ratio has improved, or you’ve bumped up your credit score—you may be able to lock in a better rate with your lender. Refinancing your home could also put cash in your pocket. “Cash-out refinancing” allows you to accept a mortgage for more than your principal balance and use the extra money at your discretion. Typically, homeowners will use such funds for significant expenses, such as a major renovation or home improvement project.

Homeowners with Adjustable-Rate Mortgages (ARMs) often refinance into a Fixed-Rate Mortgage to lock in a stable rate for the remainder of the loan term.

Refinancing can also change the length of your loan. Moving from a 30-year mortgage to a 15-year term may reduce the total interest you pay over time, while extending a loan term can lower monthly payments if cash flow is a concern. As with most financial decisions, it’s about balance and knowing the tradeoffs.

Keep in mind that refinancing your home involves getting a new mortgage, so you’ll have to go through the qualification process again. Assess your financial health and equity before you apply. Once you’re ready to move forward, your Windermere agent can recommend a few trusted lenders or mortgage brokers to provide you with a quote.

Selling Your Home

Selling your home is a bigger shift—but sometimes it’s the right one. If your home no longer fits your lifestyle, or if you’re sitting on significant equity, selling can provide financial flexibility to move forward on your terms. Your agent will start by conducting a Comparative Market Analysis (CMA) to determine your home’s value, taking into account current market conditions, location, seasonality, and your home’s unique features.

Although you stand to receive a lump-sum cash payment, selling your home comes with its own set of costs. Paying for repairs, home inspections, staging expenses, agent commissions, not to mention buying or renting your next home, as well as moving fees. This can add up, so it’s important to budget appropriately. Selling your home also means you’ll be uprooting the life you and your household have established there, so it’s necessary to have a plan for your next steps before the “For Sale” sign goes in the ground.

For personalized guidance on selling or refinancing, connect with a Windermere agent today:

This fall, two cities, two stages, and hundreds of supporters of the Windermere Foundation came together for one incredible purpose: to raise funds and awareness for youth and families experiencing housing instability and hardships in our communities.

In both Portland and Seattle, Windermere agents, clients, partners, and guests gathered for evenings filled with laughter, heartfelt stories, and a shared mission to give back. With standout performances, powerful testimonials, and an outpour of generosity, the 24th annual Steve Allen Comedy Show and the 3rd annual Windermere Foundation Comedy Night raised a combined total of nearly $1 million in support of local New Avenues for Youth and the YMCA of Greater Seattle.

24 Years of Laughter and Legacy in Portland, Oregon

For more than two decades, the Steve Allen Comedy Show, founded by Windermere Real Estate, has been a beloved tradition in Portland. This year marked the 24th annual event, once again benefitting New Avenues for Youth, a nonprofit committed to preventing and ending youth homelessness through housing, education, job training, and wraparound services.

More than 520 guests gathered at the Portland Art Museum on October 28th for an unforgettable evening starring Emmy- and Oscar-nominated actor and comedian Kumail Nanjiani. Known for his roles in Silicon Valley, Only Murderers in the Building, and Welcome to Chippendales, Kumail brought the house down with his signature mix of sharp wit and relatable storytelling.

Windermere agents and their guests helped raise $580,000 in support of New Avenues for Youth and its vital work helping young people experiencing homelessness overcome the many barriers to stability, well-being, and success.

3rd Annual Windermere Foundation Comedy Night in Seattle, Washington

Back for its 3rd year, the Windermere Foundation Comedy Night in Seattle brought together 350 guests at Fremont Studios on November 7th for an evening that blended humor, heart, and high-impact giving.

The night began with cocktails and a silent auction, followed by a warm welcome from emcee and auctioneer Nelson Jay, who kept the energy high and the giving spirit alive throughout the program. Guests enjoyed a festive dinner, cheered during the paddle raise, and shared plenty of laughs thanks to a hilarious live performance from Kevin Nealon—all while raising more than $415,000 for the Windermere Foundation and the YMCA of Greater Seattle.

These unforgettable nights did more than just entertain—they helped strengthen the work of New Avenues for Youth and the YMCA of Greater Seattle by expanding access to housing, stability, and life-changing resources. Thanks to the generosity of our community, the impact of these events will be felt long after the final curtain call.

A huge thank you to all the sponsors for making these events possible:

24th Annual Steve Allen Comedy Show Sponsors

Windermere Foundation, US Bank, Joan & Brian Allen, Lucky Transportation, Mitch & Elisa Hornecker, The Greenbrier Companies, Ashley & Matt Semler, The Standard, Propel Insurance, TMT Development, Paul & Lory Utz, Ferguson Wellman Capital Management, Casparian, Colas Construction, Legacy Health, Washington Trust Bank, KGW8, Howard S. Wright, Perkins & Co., Bill Kehman & Kari Nelsestuen, Alan Cahn Consulting

3rd Annual Windermere Foundation Comedy Night Sponsors

Stone Insulation, Morgan Stanley Private Wealth Management, Seabrook WA, Sentry Computing, Miller Nash LLP, Wilson Tile, Symetra, Healthy Paws, NWMLS, Albert Lee, Generations Home Loans, Moreland Insurance, Move Forward Financial, XpressDocs, Gentle Giants Moving Company, Clarity Northwest, SignPros, and Fremont Studios

To support the Windermere Foundation, click the donate button below and help continue our ongoing mission to help low-income and homeless families in need.

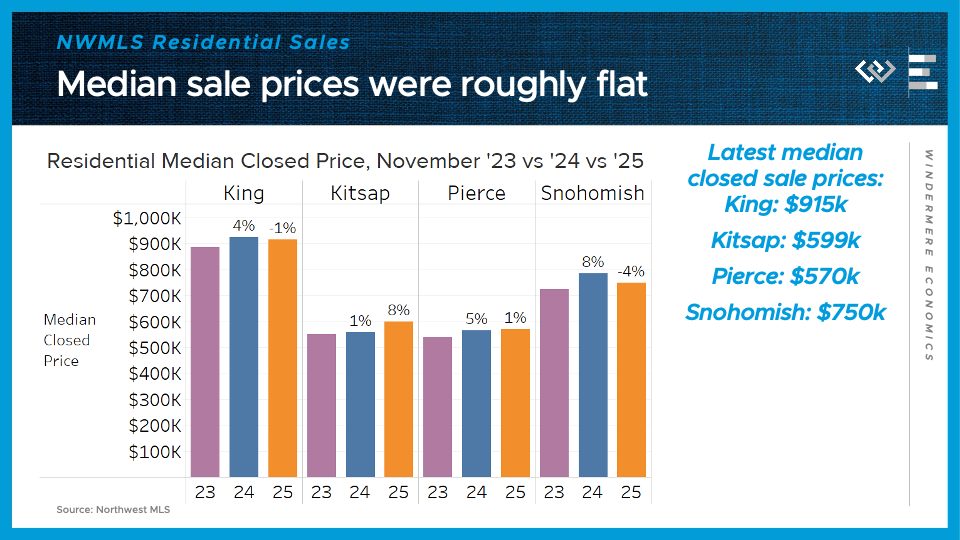

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the November 2025 data from the Northwest MLS.

This November, the Washington housing market continued with its normal seasonal cooldown. And compared to last year, this month looked particularly cool, because 2024 featured an especially strong fourth quarter, which has NOT been repeated this year.

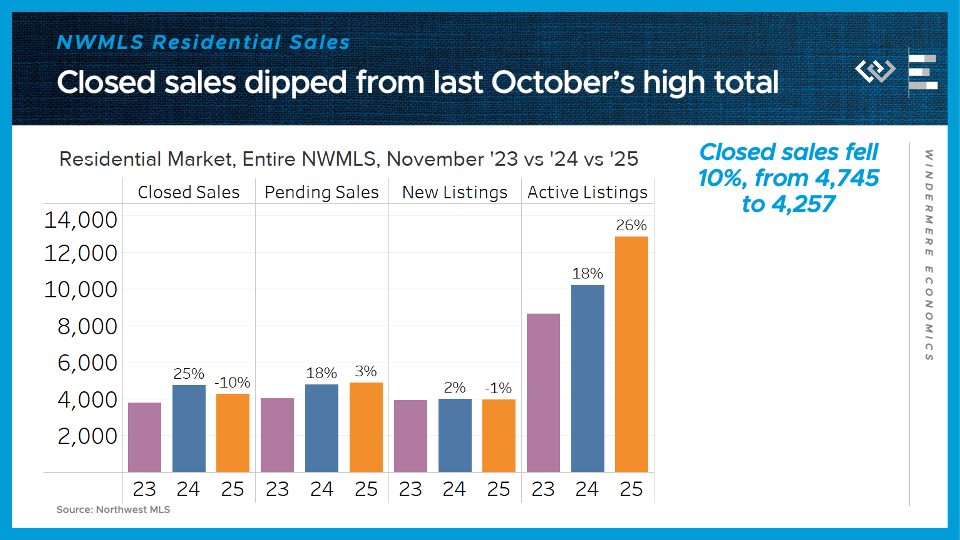

Across the Northwest MLS, closed home sales came in 10% below last November’s total. And pending sales, which give some signal about next month’s sales, actually inched up by 3% from the same time last year.

On the supply side, the flow of new listings was almost identical, or down just 1%, from last November’s pace. Finally, the month ended with 26% more active listings than last November, swinging negotiating power in buyers’ favor .

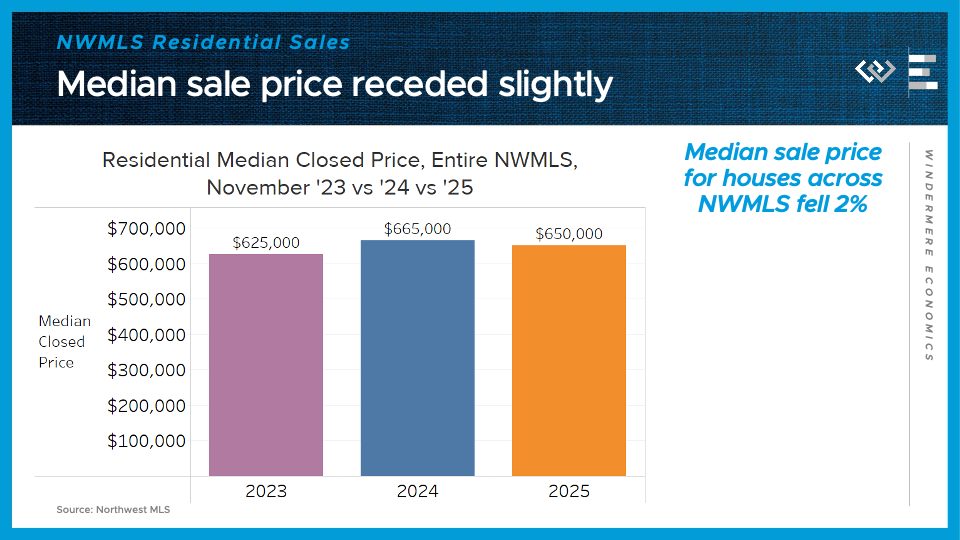

Those higher inventory levels are starting to put some downward pressure on prices, which dipped by $15,000, to a median of $650,000 for a residential home sale in November.

Now I’ll turn to a closer look at the four counties encompassing the greater Seattle area.

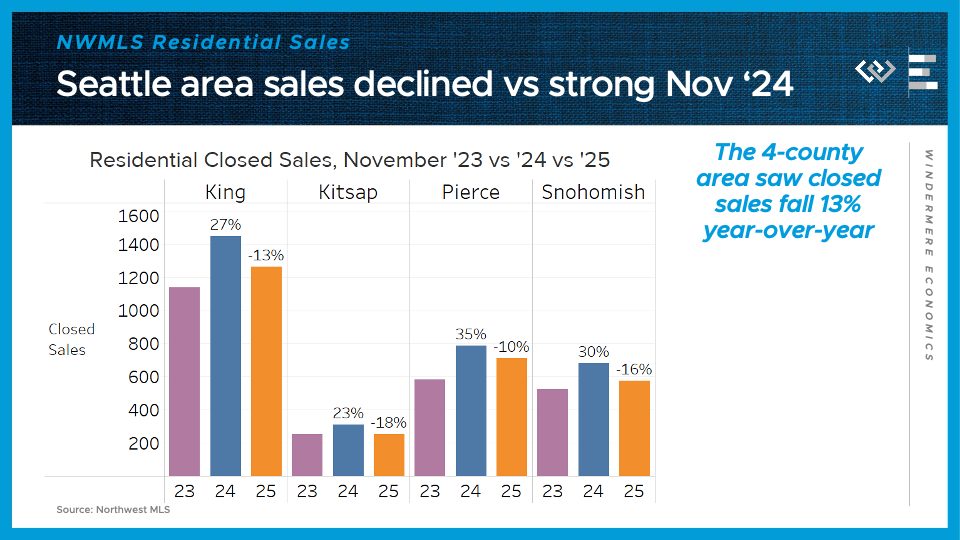

Closed sales dropped by 13% from last November, and none of the four counties was spared from double-digit declines, led by an 18% drop in Kitsap County.

Median sale prices showed roughly no gains around the region: 1% lower in King; 8% higher in Kitsap; 1% higher in Pierce, and 4% lower in Snohomish County. It seems clear now that inventory growth this year has dragged price appreciation down to about 0 for the time being.

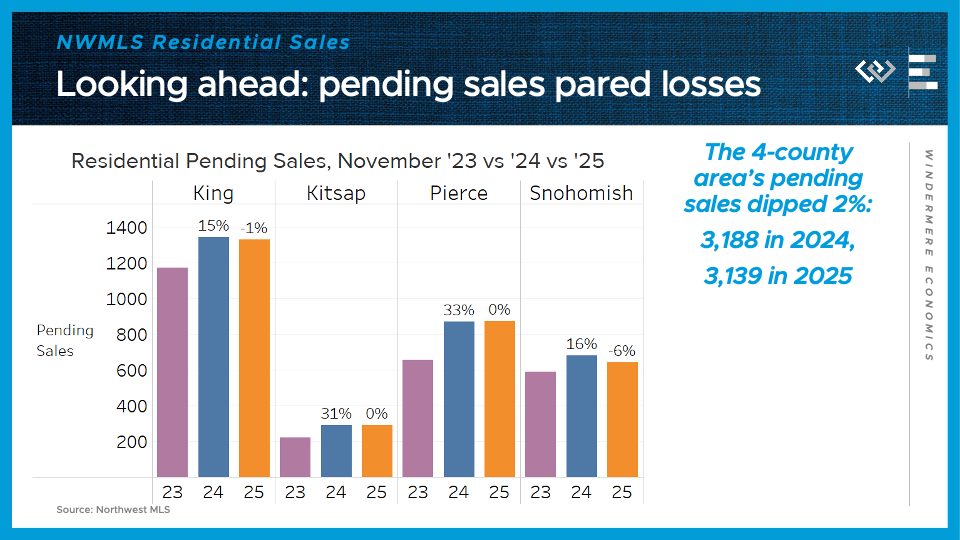

Looking ahead, pending sales dipped only 2% across the region in November, thanks mainly to Snohomish’s 6% decline, while the other 3 counties were nearly flat.

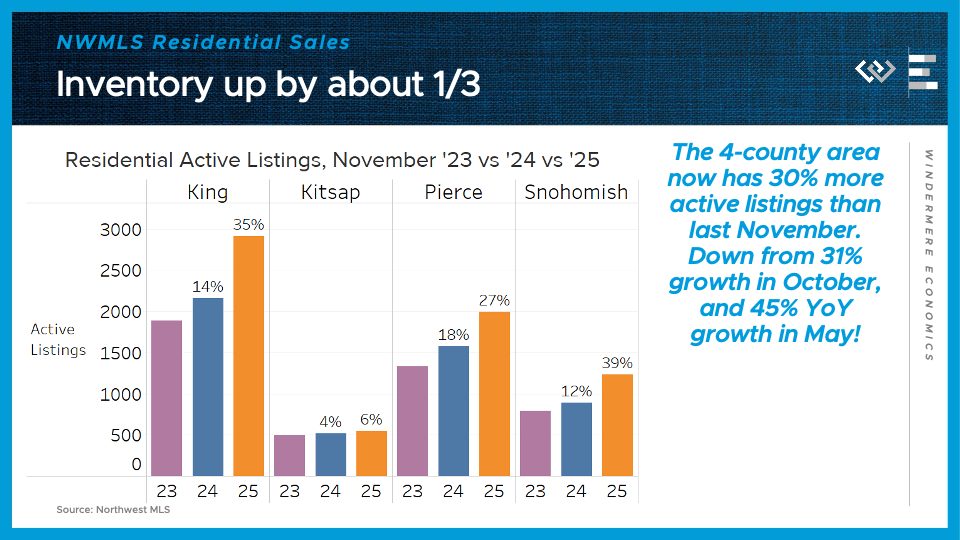

On the supply side, the 4-county greater Seattle area had 30% more active listings than at the end of November 2024. I’ve highlighted before that this pace of growth is decelerating, but that deceleration itself may have stalled out: October had a nearly identical 31% growth rate of inventory.

This continues to bode well for buyers, who are now set up to approach the new year with more inventory and bargaining power than they’ve seen in years. For anyone who can squeeze house hunting in between their holiday gift shopping this month, they’ll be well-positioned to find a bargain, even now that Black Friday deals are gone from the stores!

The following is a summary of Windermere Principal Economist Jeff Tucker’s six predictions for the U.S. housing market and economy in 2026. He goes into more detail about his predictions in the video below.

1. Existing Home Sales Will Pick Up (Barely)

Home sales have hovered near generational lows for three years. While a sharp rebound is unlikely, conditions point to a modest uptick in 2026. Inventory levels are higher than they’ve been since 2019, and mortgage rates are lower than they’ve been since 2022. Together, those factors should lift existing home sales—but not by much.

2. Home Prices Will Be Roughly Flat

Home prices are likely to remain flat in 2026, largely due to higher inventory putting downward pressure on values. The Case-Shiller Home Price Index showed small declines last summer, though that trend faded by fall. Sellers have been highly responsive to market shifts, often de-listing when offers fall short or holding off on listing altogether. That restraint has kept prices from falling further despite growing supply

3. Inventory Will Climb to Pre-Pandemic Levels

The number of homes for sale will likely return to pre-pandemic levels in 2026, possibly as early as spring. Inventory rose sharply in 2025, and a “shadow supply” of homes—those whose owners are waiting for better conditions—remains in the wings. Many “discretionary sellers” will continue testing the market, holding out for the right price. That behavior should extend average time on market and boost total listings, giving buyers more options and negotiating power.

4. The Homeownership Rate Will Decline

At current prices and interest rates, homeownership remains out of reach for many middle-class Americans who would have bought in different conditions. Slower rent growth has also reduced urgency among would-be buyers, encouraging them to stay put. More renters are opting for single-family homes to enjoy the space and lifestyle of ownership without a mortgage, a shift that will help push the overall homeownership rate slightly lower.

5. Mortgage Rates Will Decline Slightly

Mortgage rates should remain below 6.25% for most of 2026 and could briefly dip under 6%. The Fed’s rate cuts and slower growth have brought 10-year Treasury yields near 4%, while the spread between Treasuries and mortgage rates has narrowed toward its normal range of 2% or less. That trend is expected to continue as refinance risk on mortgage-backed securities gradually fades, but much of the improvement is already reflected in current rates, so significant declines are unlikely.

6. We Will Avoid a Recession in 2026

The U.S. economy weathered several shocks in 2025 but avoided a downturn. Payroll gains have slowed, though more due to shrinking labor supply than weak demand, and unemployment claims have remained stable. After early trade policy turbulence, corporate earnings rebounded strongly, and tariff concerns have faded as court challenges and new trade deals rolled back some of the costliest restrictions.

Color has a way of reshaping the way a home feels, and for 2026, Behr has introduced a shade that truly sets the tone. Hidden Gem N430-6A, a smoky jade with an air of quiet confidence, is rich, refined, and just mysterious enough to keep your rooms interesting long after the paint dries.

As homes continue shifting toward more personal, expressive spaces, this jewel-toned green blue arrives right on cue. Whether you’re updating a single room or planning a top-to-bottom refresh, here’s how to embrace Behr’s Hidden Gem and blend it seamlessly into 2026’s biggest interior design trends.

Behr Color of the Year: Hidden Gem

Each year, Behr’s color experts look to lifestyle trends, design movements, and cultural moods to select a single shade that reflects how people want to live. For 2026, the demand is clear: homeowners are craving comfort, character, and a stronger connection to the natural world. Hidden Gem brings all three into perfect balance, offering a sophisticated, versatile tone that feels intentional without overpowering a space.

With its deep teal base and soft smoky undertones, it offers a calm, eye-catching depth that shifts effortlessly with the light, perfect for layering with the color and design trends shaping homes in 2026.

Source: Behr 2026 Color of the Year – Hidden Gem

Balancing Hidden Gem with 2026 Color Trends

Color forecasters agree that 2026 will be defined by rich, soothing, nature-inspired hues that help homes feel more grounded and expressive. Hidden Gem fits neatly into this movement, especially as tranquil teals rise in popularity.

This year’s trend reports also point to the growing appeal of warm blacks and mellow reds. These deeper tones bring drama and intimacy into a space, particularly in small rooms or architectural moments. Hidden Gem pairs beautifully with warm blacks like Behr’s Cracked Pepper and earthy reds such as Terra Cotta Urn, creating a thoughtful contrast that feels modern and moody.

Uplifting yellows and soft neutrals will also remain strong throughout 2026. Subtle creams and warm whites help brighten teal-based palettes, while tones like Wheat Bread provide a soft foundation that allows Hidden Gem’s depth to shine. Pairing it with sunny tones like Beehive or 2025’s butter-yellow trend adds a fresh lift, keeping the look balanced and inviting.

Just like Pantone’s color stories, Behr’s 2026 palette is designed to influence cohesive, livable color combinations around its Color of the Year. And the good news? Hidden Gem is unusually flexible. If you are looking for more combinations, explore Behr’s full list of 2026 color trends for additional inspiration.

Source: Behr 2026 Color Trends

How to Align Hidden Gem with Other 2026 Home Trends

Beyond color, the home trends emerging in 2026 offer even more ways to weave Hidden Gem into a refreshed modern space.

Color Drenching and Moody Palettes

One of the biggest design shifts heading into 2026 is the rise of color drenching, where a single shade covers the walls, trim, ceiling, and sometimes even furniture in a room. The look creates a fully immersive, moody atmosphere that feels polished and cohesive. Hidden Gem is especially well-suited for this approach because of its depth and richness.

Alongside this trend, deeper, moodier palettes are also becoming more popular. Saturated hues like greens, ochres, burgundies, and tobacco-inspired tones are appearing more often in homes, reflecting a growing desire for warm color and expressive style.

Hidden Gem’s serene, smoky character makes it an ideal backdrop for these spaces. It brings a quiet sense of balance to reading nooks when paired with warm wood or soft, textured fabrics. In bathrooms, it complements natural materials and warm metals, creating the same soothing quality you’d expect from a spa.

Sustainability Remains a Priority

Sustainability continues to influence how people design and renovate their homes. From natural materials to energy-efficient upgrades and EV-friendly features, homeowners are seeking ways to make their spaces both stylish and environmentally conscious.

Hidden Gem’s nature-inspired tone fits comfortably within these choices. It pairs effortlessly with organic textures like stone, linen, clay, and reclaimed wood, creating a look that feels grounded and connected to the environment.

With Hidden Gem leading the way, 2026 offers endless opportunities to create a home that feels expressive, grounded, and beautifully your own.

This is the latest in a series of videos with Windermere Principal Economist Jeff Tucker, where he delivers the key economic numbers to follow to keep you well-informed about what’s going on in the real estate market.

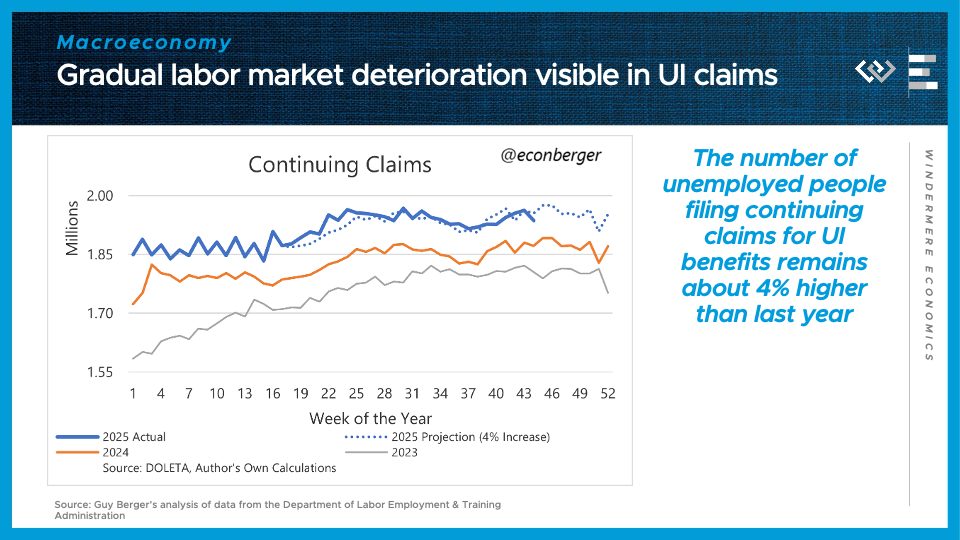

The first number to know this week: 4%. That is how much higher unemployment claims are than this time last year. We don’t actually know the unemployment rate due to the government shutdown, which suspended collection of the household survey it’s based on, so instead economists have turned to state-level data sources. Labor economist Guy Berger shared this chart comparing continuing unemployment claims in 2025, in blue, to the last two years, showing a consistent, gradual 4% year-over-year increase. That’s not great news, but it still doesn’t indicate a sudden breakdown in economic growth. We’ll get a better picture of the economy as the Bureau of Labor Statistics resumes publishing data in the remainder of 2025.

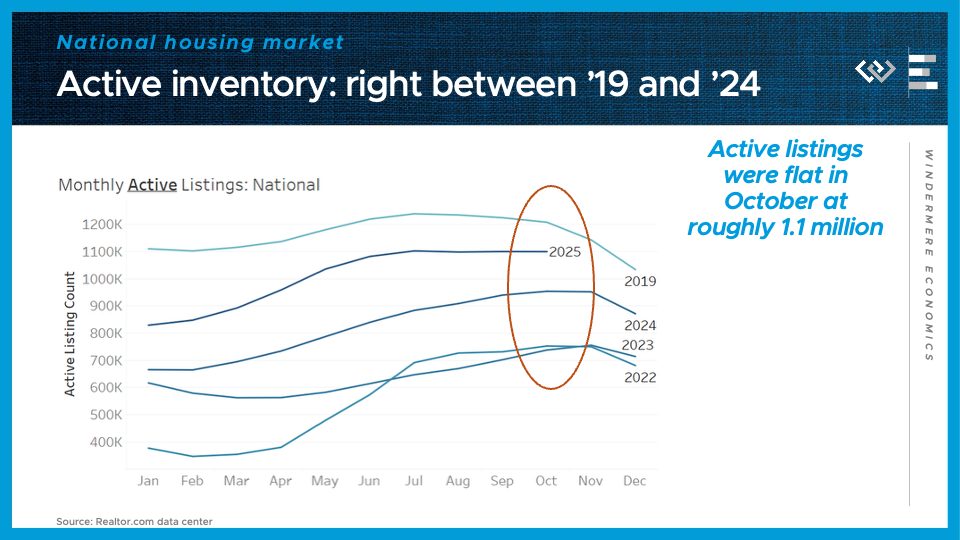

Turning to the housing market: Realtor.com reported almost exactly 1.1 million active listings for sale at the end of October, for the third month in a row. One interesting trend this chart makes clear is that, since 2020, sellers have been more willing to keep listings up later into the fall than they tended to in 2019. That means we are closer now to 2019 inventory levels than at any other time since the pandemic began.

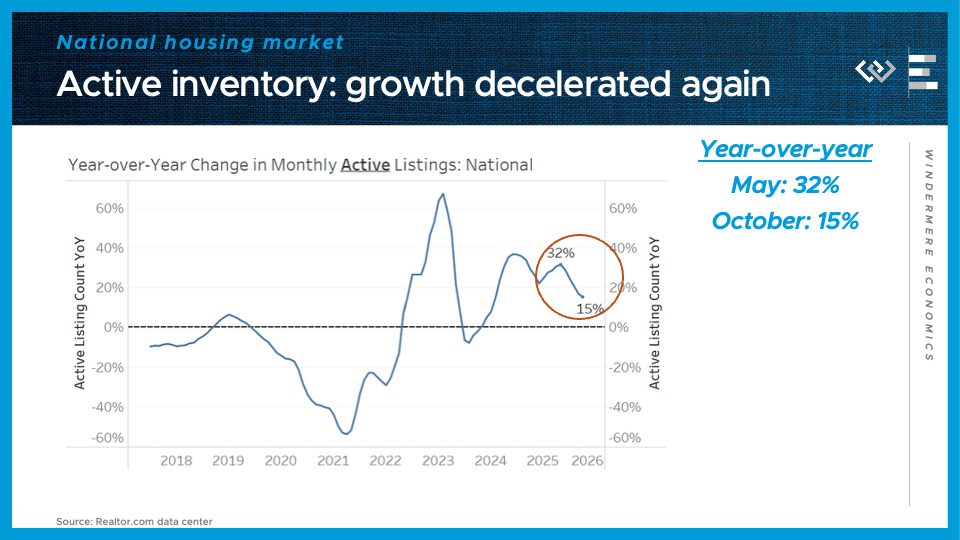

But for the fifth month in a row, the pace of growth of inventory has fallen yet again, now down to just 15% year-over-year. The big growth of active listings this spring and summer helped throw some cold water on price appreciation, pushing it down near to 0, but that inventory growth has slowed down enough that nationally, prices look most likely to flatline next year rather than plunge into negative territory.

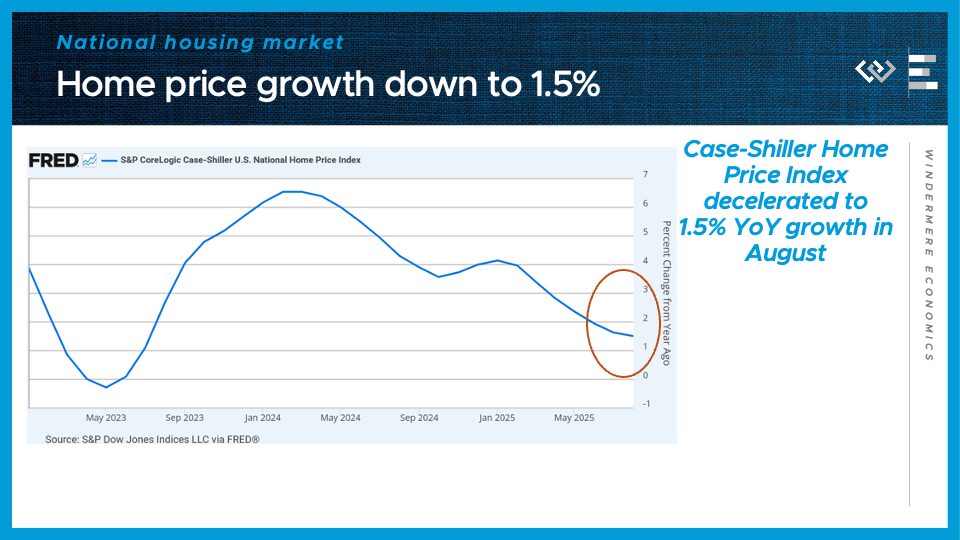

That brings me to the next number to know: 1.5%. That’s the most recent year-over-year change in the Case-Shiller Home Price Index, and the slowest pace of home price appreciation since early 2023.

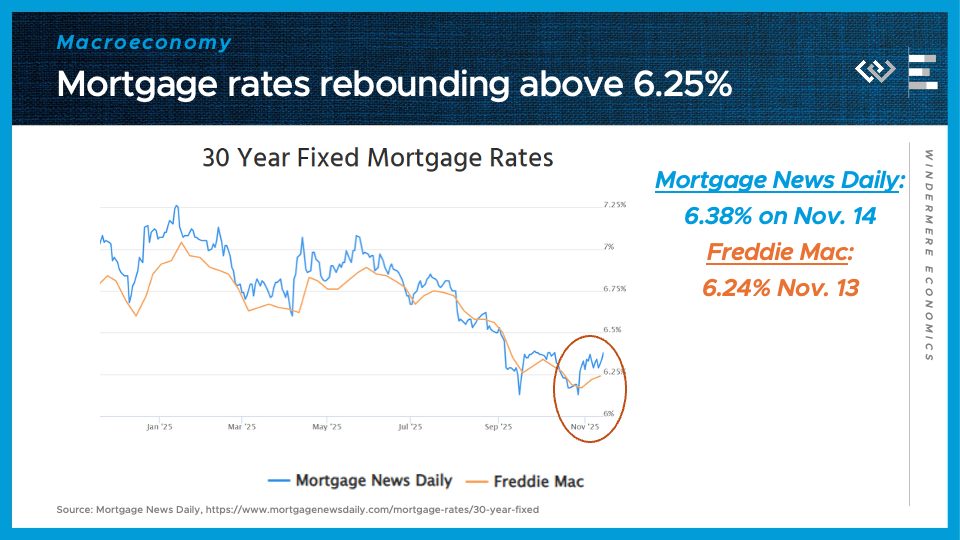

The other puzzle piece for home purchase affordability took a little step in the wrong direction last month: Mortgage rates rebounded from below 6.25% to more like 6 and 3/8, according to Mortgage News Daily. That’s still lower than they were last winter, and it just goes to show that mortgage rates rarely stick to the script and follow a predictable long-term trend.

That is all for this month; I look forward to more economic data in December, and thanks as always for watching!

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

")