You may have noticed some changes here on the Windermere Blog and the Windermere Foundation Blog; the blogs are now fully integrated into the Winderemere Real Estate website! This means that the blog posts are easier to find from the website than before, you will be able to see feature articles on the buying and selling pages, and you can utilize social share tools to save or share articles on Facebook, Twitter, Pinterest or Google+.

Commenting on blog posts is a little easier as well. You don’t need to be signed in to leave us a comment, just fill in the form with your name and comment.

Social Share

We have also expanded our Social Share options over the last few months, so now you can email, Facebook, Tweet, Pin and Google+ interesting articles, listings and blog posts.

If you like bookmarking, you may want to explore “myWindermere”. You can create an account on Windermere that enables you to store your favorite home listings, save your searches, receive automatic email notifications on saved searches, and connect with an agent.

We hope you are enjoying the new features on Windermere.com. If you have feedback, you are welcome to send us an email at friend [at] Windermere [dot] com

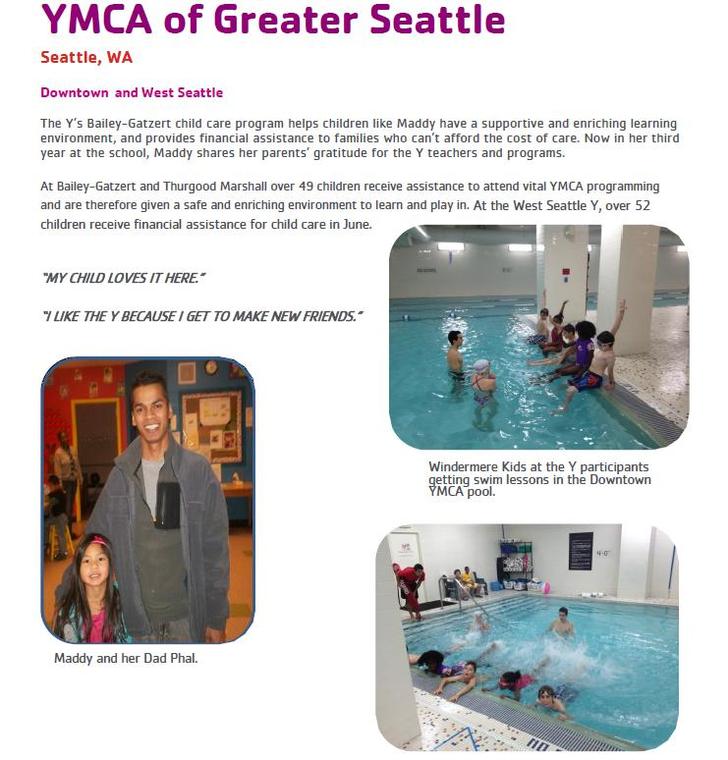

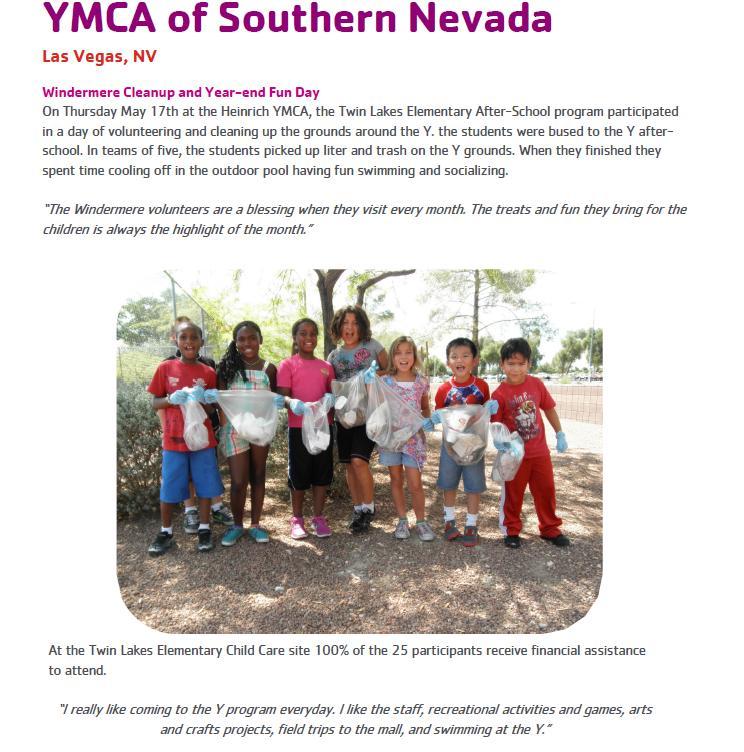

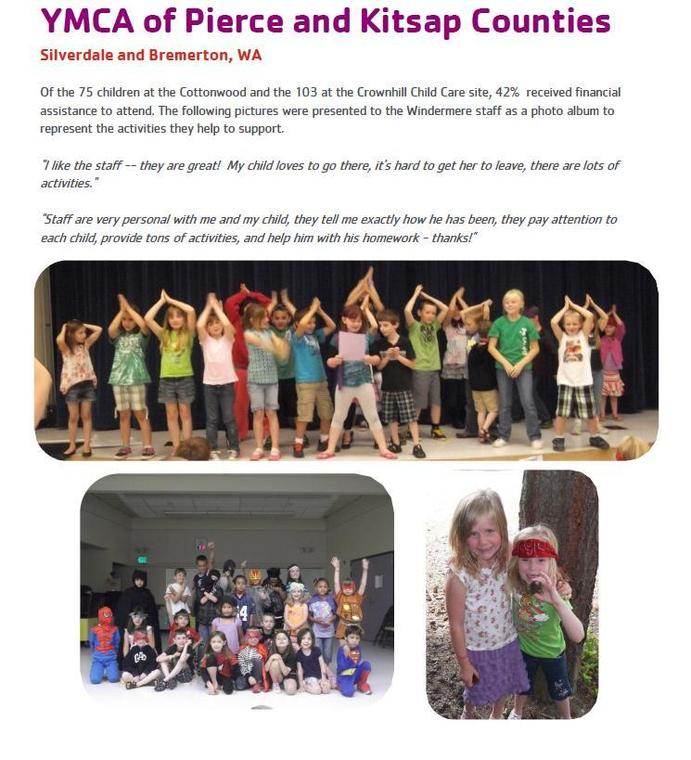

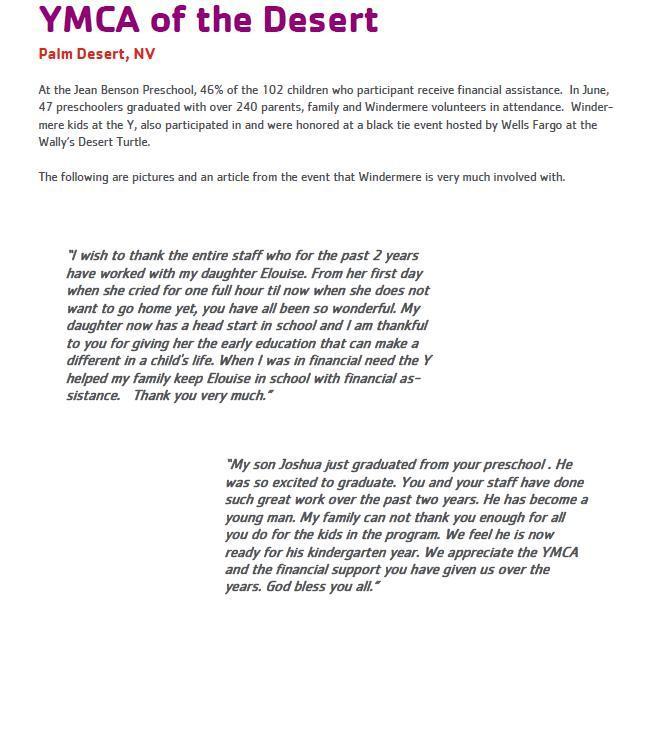

In 2006, the Windermere Foundation and the YMCA partnered to create Windermere Kids at the Y, a tuition-assistance and volunteer program that provides low-income children with quality after-school enrichment programs and the all-important summer camp experience.

The Windermere Foundation has dedicated over 1.2 million dollars to this important cause—helping hundreds of kids through our first network-wide program. This unique partnership provides the YMCA with much-needed funds, as well as support from Windermere agents, who volunteer their time to assist with the summer camps and other kids’ activities.

Moving is stressful, whether it is across town or cross-country. Once you have closed on your house, the reality of packing, moving, and setting up a new home can become overwhelming. While no list can make a move “stress-free”, planning ahead and staying organized can help make your move a little smoother. Here is our list of tips:

Getting started:

· Once you know your prospective move date set up a quick timeline to make sure you can get all the important tasks done and ready in time for your move.

· Consider how much stuff you have by doing a home inventory. This can help you decide whether you need to hire movers to help you or if you will be managing your move on your own. Many moving companies supply inventory lists to help you assess the size of truck you will need. You can use your list as double duty for insurance purposes later.

· As soon as you decide how you will be moving, make your reservations. In general, moving companies and truck rental services are over-booked at the beginning and very end of the month. If you are planning on hiring a moving company, contact a few in your area for a price quote. To find companies ask your real estate agent, family, or friends, and consult online reviews. It is also a good idea to request a quote and compare companies.

Preparing for your move:

· Moving is a great opportunity to get rid of clutter, junk, or outdated items. Set aside some time to sort through your closets, storage spaces, files, drawers, and more. Go through cluttered areas and organize items by “keepers”, “give-aways” and “garbage”. You will have less to pack and an opportunity to update after you move. Contact a local nonprofit organization for your donations; some will arrange to pick up larger donations like furniture. If you have items of value, eBay or craigslist are good options.

· Before you start packing, it may help to visualize where everything you have will go. Perhaps furniture will fit better in a different room? Consider the floor plan of your new home and figure out what will go where. This will aid in packing and labeling as you box everything up.

· Use a tool like floorplanner.com to plan where furniture and items will go.

· When it comes to packing you have some options. You can work with a service that provides reusable boxes for moving or you can reuse or purchase cardboard boxes. Make sure you have enough boxes, packing tape, dark markers, and packing paper.

· Pack rooms according to your floor plan. Label boxes with contents and room. This will make it easier to unpack your home, knowing where everything is going.

· If you have to disassemble any of your furniture, make sure you keep all the parts and directions together.

· Make sure you set aside your necessities for the day you move. Being tired and unable to take a shower or make your bed can be hard at the end of a long moving day. Here are some ideas of what you may like to pack in your “day-of-move” boxes.

· Clean linens for the beds, pillows and blankets

· Clean towels

· Shower curtain, liner and hooks

· Toiletries, hand soap, tooth brush, etc.

· Disposable utensils, cups, napkins, etc

· Rolls of toilet paper

· Snacks and water

· Change of clothes

· Tools for reassembling furniture, installing hardware, and hanging photos

Making your move

· Come up with a game plan with your family, so everyone has a role and a part to play

· Once the house is empty, do a once over on your old place to make sure it is clean for the next owners/occupants. Here is a useful checklist for cleaning.

Warming your new home

· Once you have settled into your new home, warm it up by inviting friends and family over to celebrate. Here is a great infographic about housewarming traditions and symbolism.

· Announce your move to far-away friends and family through moving announcements to make sure you stay on the holiday card mailing list.

Do you have any other tips or advice for achieving a smooth move?

Summer has flown by and it is hard to believe school will be starting for most students in the next few weeks. For many of us, we have special memories associated with the start of a new school year. From seeing our friends for the first time all season, to a new fall wardrobe and all new school supplies to start the year. Unfortunately, many of the kids in our communities will not be so lucky this year.

Please help us get some of our local students off to a good start this new year. Windermere offices throughout the network have been collecting backpacks, school supplies and healthful snacks for local low-income and homeless students.

If you don’t see your local Windermere office listed below, contact us on Facebook at www.facebook.com/WindermereFoundation, and we are happy to help you connect with a local office or organization.

· Windermere Eastside offices, Redmond, Bellevue West, Bellevue Main, Yarrow Bay, Kirkland Central, and Kirkland NE are collecting backpacks and supplies for low-income and homeless youth with the Kirkland Interfaith Transitions Housing program (KITH).

· Windermere West Seattle is supporting local students through Neighborhood House.

· Windermere Issaquah has partnered with the local YMCA backpack drive.

· Every Tuesday in August Windermere Bainbridge has partnered with local businesses to host the 10th annual Windermere Classic Car Cruise-in. 100% of the donations and proceed will benefit Project Backpack, providing essential school supplies, clothing and school fees for students in need.

· Windermere West Sound offices are collecting backpacks at Windermere Poulsbo, Kingston and Silverdale locations.

· Windermere Snohomish is teaming up with the Boys & Girls club to ensure local youth get the school supplies they need.

· Windermere Bay Area properties has partnered with HOPE’s Children to make sure local low-income kids are getting “whatever they need” to get the school year started right.

· Windermere Whidbey Island is partnering with the Readiness To Learn Foundation in the Coupeville School District. Over the last eight years the Windermere backpack dirve has helped serve over 1,000 students.

· Windermere Sun Valley in Idaho is working with the Hunger Coalition to supply local students with the nutrition they need to excel in school.

· Windermere Relocation helped purchase backpacks for the Ruth Dykeman Children’s Center.

· Portland offices are working with Lift Urban Portland. Every weekend the organization sends backpacks with food home with the kids to make sure they are getting the food they need. More than 80 students will benefit each month from this year-round program.

· Seattle area offices, Greenlake, Lakeview, Northgate, Northlake, Sand Point, and Wedgwood donated 391 backpacks and supplies to local elementary schools.

Thank you to all of our offices and everyone who contributes to make sure local children are getting the resources they need for success.

Windermere Real Estate is proud to partner with Gardner Economics on this analysis of the Oregon and Southwest Washington real estate market. This report is designed to offer insight into the realities of the housing market. Numbers alone do not always give an accurate picture of local economic conditions; therefore our goal is to provide an explanation of what the statistics mean and how they impact the Oregon and Southwest Washington housing economy. We hope that this information may assist you with making an informed real estate decision. For further information about the real estate market in your area, please contact your Windermere agent.

REGIONAL ECONOMICS

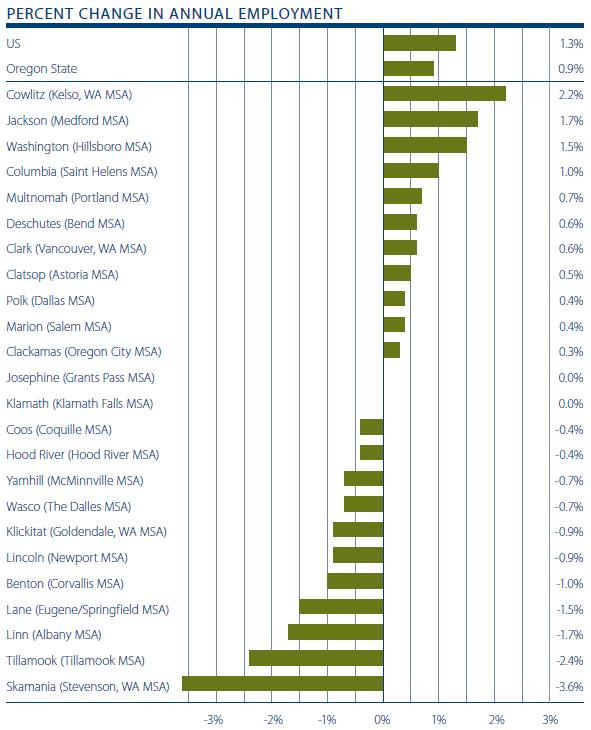

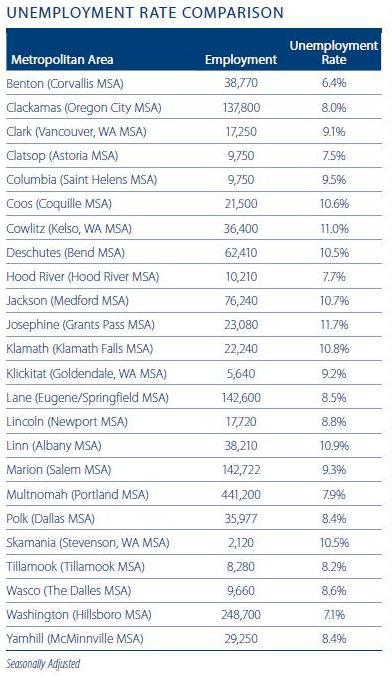

There are two ways to look at the current employment report for the market. The first is that job growth remains painfully slow, with 13 of the 24 counties shedding jobs year-over-year, and an overall expansion of the job base by a meager 7,232 or 0.4%. The other—and certainly more positive way—is to compare this report with the prior quarter where just two counties lost jobs and we experienced an overall growth rate of 26,439 or 1.6%. I prefer the latter and will focus on that!

As stated previously, 22 of the 24 counties covered in this report improved their job base over the past quarter, with the greatest gains being found in Klickitat (+6%), Lincoln (+5.7%), and Clatsop (+5.4%) Counties. On an absolute basis, Washington County saw the largest increase over Q1 with 4,100 additional jobs, followed by Lane (3,100), Jackson (2,930), and Deschutes (2,270) Counties.

On the negative side, job losses were only found in Yamhill County where 650 jobs were shed (-2.2%) and Hood River County where 30 jobs were lost (-0.3%).

It is interesting to note that the overall unemployment rate declined across the board when compared to a year ago. This tends to be a function of a decline in the participation rate, which represents the number of people who are either employed or are actively searching for work. During periods of contraction, many workers get discouraged and stop looking for work which actually (and artificially) improves the unemployment rate.

I am giving the employment situation a “C” grade this quarter, up from the “D” that I gave it in the prior quarter. I had expected to see an improving job market in the first quarter, but it looks as if perhaps I was just a little premature in my forecast.

The numbers look pretty good, but I want to see consistent quarterly improvements before I start to feel comfortable with stating that we are in full expansion mode.

REGIONAL REAL ESTATE

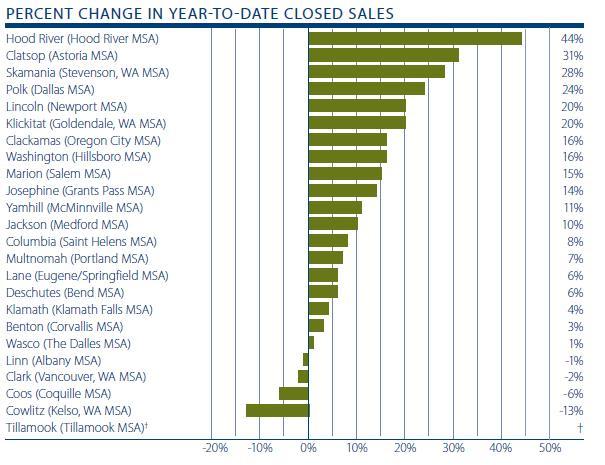

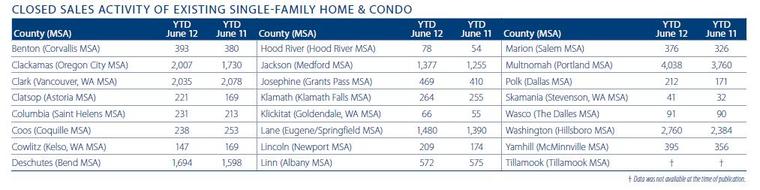

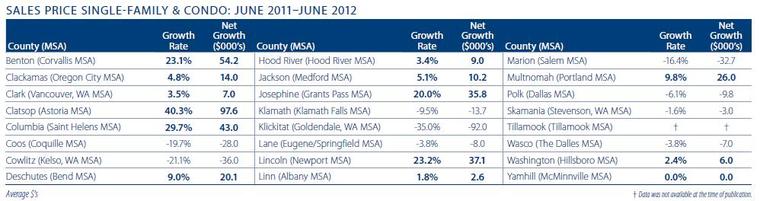

Home sales continued to expand with 19,394 transactions—an increase of 8% from the same period in 2011. Year-over-year we note that all but four counties saw improving sales.

When we compare sales velocities over the previous quarter, all but one county exhibited improvement, suggesting that the spring market did arrive; it was just a little late! The only market where sales slowed was in Skamania County and the drop was marginal.

Year-over-year, the greatest improvement was seen in Hood River (+44%), Clatsop (+31%), Skamania (+28%), and Polk (+24%) Counties. There was only one county where declines were in the double digits, and that was in Cowlitz County where sales were 13% lower than during the first half of 2011 but, even here, the market has showed dramatic improvement over the first quarter of 2012.

From a transactional standpoint, the data shows solid improvement, but there is a caveat: units available for purchase declined across all the counties surveyed—and this is a concern. Although most markets saw a modest uptick in listings during the quarter, the number of units for sale is down substantially from a year ago, as well as the long-term trend.

Much of this can be attributed to the slowdown in banks listing foreclosed homes for sale, as well as homeowners with negative equity waiting to list their homes until prices rise sufficiently to enable them to sell and not owe money to their mortgage holders.

Choice in many markets has become limited which, if it does not improve, will likely lead to a slowdown in transactions in the second half of 2012.

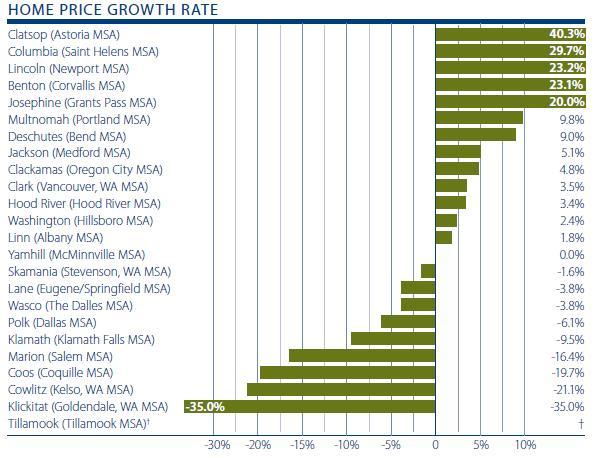

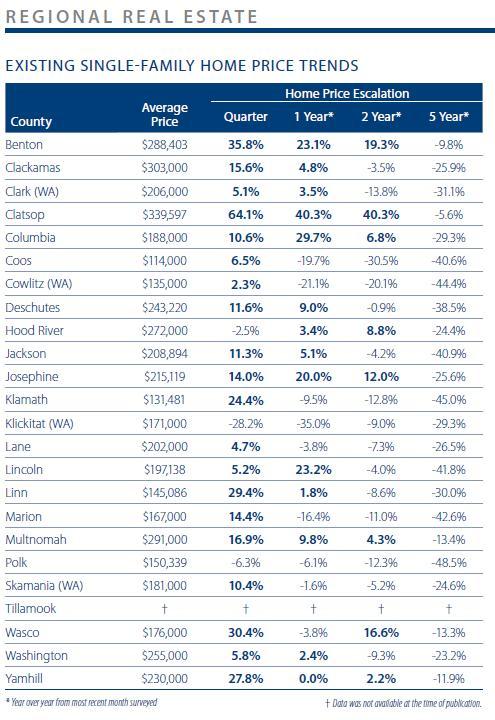

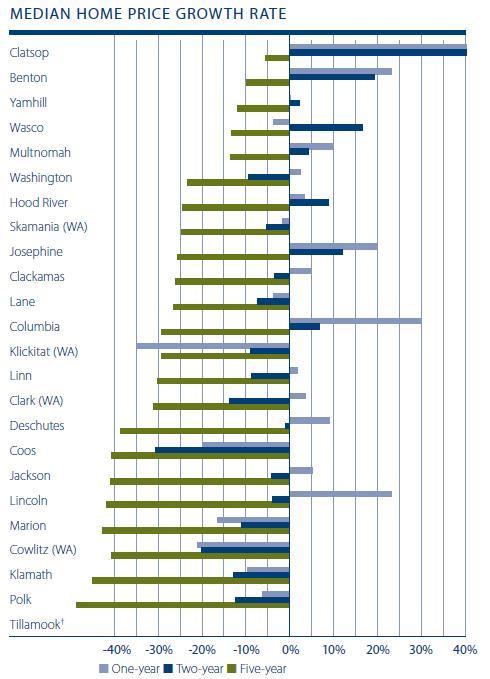

Turning our attention to home prices, 14 of the markets analyzed registered year-over-year price increases (up from nine in the last report) with nine showing declines in values from a year ago. In aggregate, the markets surveyed saw values increase by 2.8% over the same period in 2011.

Other than the substantial 40% growth in the relatively small Clatsop County market, four other counties registered double-digit gains from June 2011. When compared to prices seen in the first quarter of the year, 21 counties are higher with just three declining.

Overall, I give the real estate market a “C” grade this quarter. This is up from the “D” that I gave it last quarter, but the concern discussed above—and its potential to negatively affect sales volumes as well as price—are still weighing on the grade.

CONCLUSIONS

The Oregon economy showed much-needed improvement this quarter, which is encouraging. As I have stated before, home values and employment growth are intertwined and as one goes, so the other will follow.

Employment growth picked up quite nicely in the last quarter and I am looking for this to continue at a modest pace through the balance of the year. It will not be easy though, as I anticipate that the government sector will continue to shed jobs, therefore putting the onus on the private sector to create a vast majority of the expected job growth.

The housing market appears to be starting to find its legs but I remain cautious as to exactly what direction it will take. Distressed listings have taken a breather, but there are still significant headwinds as the proportion of homeowners with negative equity remains high and, if we see a pickup in repossessions, the recent increase in home values will, no doubt, be dampened.

That said, the spring market for jobs and housing has arrived—albeit a little late. I will be very interested to see if the recent improvement that is evidenced by this report continues through the summer.

ABOUT MATTHEW GARDNER

Mr. Gardner is a land use economist and principal with Gardner Economics and is considered by many to be one of the foremost real estate analysts in the Pacific Northwest.

In addition to managing his consulting practice, Mr. Gardner is a member of the Pacific Real Estate Institute; chairs the Board of Trustees for the Washington State Center for Real Estate Research; the Urban Land Institutes Technical Assistance Panel; and represents the Master Builders Association as an in-house economist.

He has appeared on CNN, NBC and NPR news services to discuss real estate issues, and is regularly cited in the Wall Street Journal and all local media.

Windermere Real Estate is proud to partner with Gardner Economics on this analysis of the Western Washington real estate market. This report is designed to offer insight into the realities of the housing market. Numbers alone do not always give an accurate picture of local economic conditions; therefore our goal is to provide an explanation of what the statistics mean and how they impact the Western Washington housing economy. We hope that this information may assist you with making an informed real estate decision. For further information about the real estate market in your area, please contact your Windermere agent.

REGIONAL ECONOMICS

There’s an old saying in Western Washington that you have to wait until the 5th of July for summer to start and that, after a prolonged period of tedium, light starts to shine. In reviewing the latest data on the economy and real estate markets, I believe the same can be said about them.

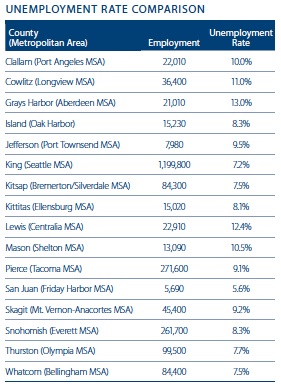

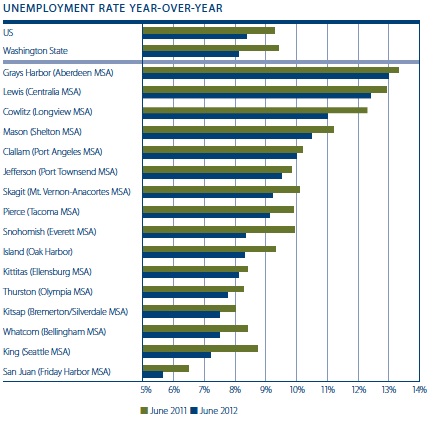

In aggregate, the job market in our region now appears to have come out of the darkness and is showing solid gains across a majority of the counties surveyed within this report. Between June of 2011 and June of 2012, the area added 58,070 jobs—a 2.7% growth rate, which exceeds both Washington State as a whole, as well as the United States. In our region, ten counties expanded their employment base with just six showing modest contraction. If we compare the data to the first quarter of this year, just one county, Grays Harbor, did not add jobs.

Year-over-year, Snohomish County continues to grow at the greatest rate—a function of the buoyant aerospace industry. This was followed by Whatcom (3.9%) and King (3.3%) Counties. Job losses were relatively modest with Grays Harbor (-4.4%), Kittitas (-3.3%), Jefferson (-2.9%), and Clallam (-1.5%) Counties suffering the largest job losses.

Looking at unemployment, all areas saw the rate improve when compared to a year ago.

The latest data is impressive indeed and has exceeded my expectations. As a result, I am going to give the current employment situation a solid “B” grade, up another notch from the last quarter.

The region has seen notable gains for several quarters now, and what is most impressive is that it has come despite continued reduction in government employment. The private sector in our region has taken the bull by the horns and continued to grow despite the uncertain macroeconomic and political environment.

Growth in our region has become the envy of the West Coast and I hope that this can be sustained.

REGIONAL REAL ESTATE

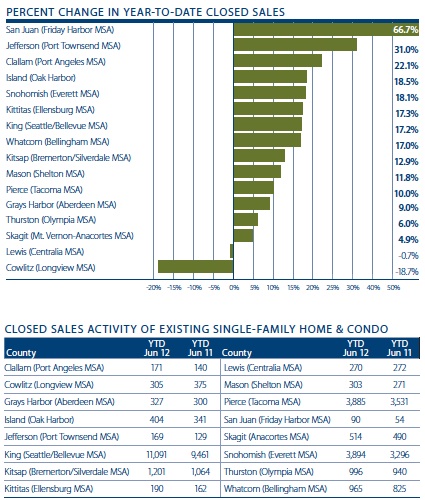

The Western Washington market registered 21,651 transactions of resale housing units in the second quarter of this year—another impressive increase of 14.4% from the same period a year ago.

The spring market may have come late, but it certainly arrived with a vengeance with all but two counties exhibiting improving sales velocities over the same period in 2011. The counties where there were sales declines are somewhat of an anomaly, as both are small areas and the absolute losses were equally small.

That said, the late spring market was clearly evident with all counties surveyed improving in home sales when compared to the previous quarter.

From a transactional standpoint, the data shows solid improvement, but there is a caveat: units available for purchase declined across all the counties surveyed and this is a concern. Although most markets saw a modest uptick in listings during the quarter, the number of units for sale is down substantially from a year ago, as well as the long-term trend.

Much of this can be attributed to the slowdown in banks listing foreclosed homes for sale. Another factor is that homeowners who are marginally underwater are waiting to list their homes until prices rise sufficiently to enable them to sell and not owe money to their mortgage holders.

Choice in many markets has become limited which, if it does not improve, will likely lead to a slowdown in transactions in the second half of 2012.

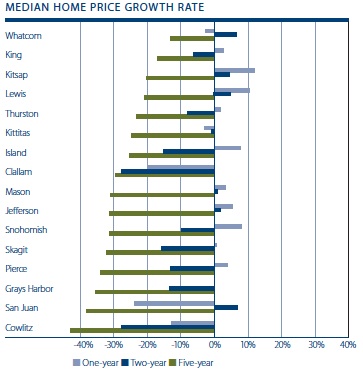

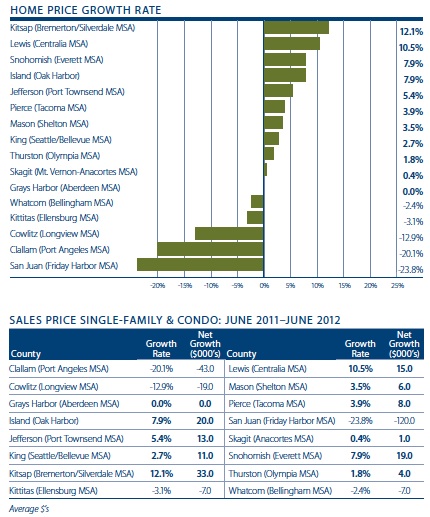

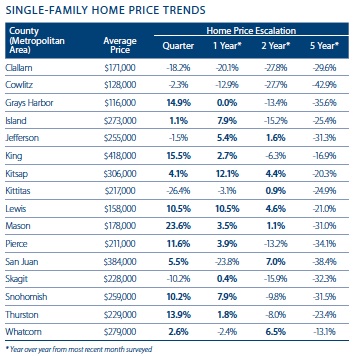

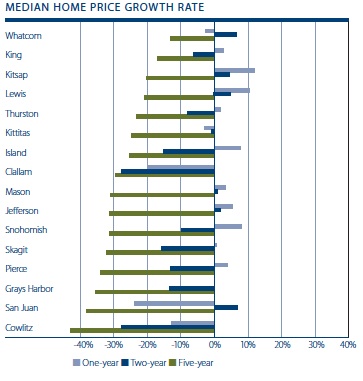

As is shown in the chart to the right, ten counties saw the average sales prices at levels above those of a year ago, five counties are at lower price levels, and one was static. Prices of home sales in the counties analyzed have turned around with aggregated prices 1.6% higher than seen in June of 2011. The disclaimer remains that this figure excludes the highly volatile San Juan County. If we include it, prices paid for homes dropped by a modest 1.7% year-over-year.

Of the counties that saw appreciation, the most pronounced gains were seen in Kitsap (+12.1%) and Lewis (+10.5%), followed by Snohomish and Island which both saw 7.9% growth. The greatest declines were seen in the previously mentioned San Juan County (-23.8%), followed by Clallam (-20.1%) and Cowlitz (-12.9%) Counties.

Previously in this report, I mentioned my concern with the low level of inventory in almost all of the counties surveyed and that it will likely have a negative effect on overall sales as we move forward. This not only has an effect on the number of sales in an area, but also home prices.

If we do see an increase in distressed units coming to market—and I have no doubt that we will—this is likely to cause the growth in prices to slow down, or even decline. This is due to the fact that distressed homes usually sell for less than market which can drag the overall average down, especially if we do not see a large increase in non-distressed listings to offset it.

I am actually going to hold the grade for home values at a “C” this quarter. It would be easy to get caught up in the long-awaited improvement in prices that we saw in the quarter, but due to the factors previously mentioned, I am adopting a “wait-and-see” attitude.

CONCLUSIONS

Summer has appeared in Western Washington and this has, so far, been reflected in our economy, as well as our housing market.

Businesses have been adding staff at a fair clip and, to a degree, this has influenced people’s decision making when it comes to buying a home. The two are, indeed, intertwined.

Even with this positive data, I am still suggesting that we be a little cautious regarding the housing market. Not because I believe that we are going to see any sort of rapid decline in values, rather that the long-awaited improvement that is shown here may still have some hurdles ahead.

The wait for summer has been worth it—as has the very long wait for recovery/stability in our regional economy real estate markets. The glass is definitely half full right now, but it remains too early to call for a certified recovery in home prices. Enjoy the weather while it is here!

ABOUT MATTHEW GARDNER

Mr. Gardner is a land use economist and principal with Gardner Economics and is considered by many to be one of the foremost real estate analysts in the Pacific Northwest.

In addition to managing his consulting practice, Mr. Gardner is a member of the Pacific Real Estate Institute; chairs the Board of Trustees for the Washington State Center for Real Estate Research; the Urban Land Institutes Technical Assistance Panel; and represents the Master Builders Association as an in-house economist.

He has appeared on CNN, NBC and NPR news services to discuss real estate issues, and is regularly cited in the Wall Street Journal and all local media.

Summer is finally here, and like many of you, when the weather turns nice we find ourselves smiling a little more. Our whole mood changes for the better. Maybe it’s the much-needed dose of vitamin D – or perhaps it’s that we’re finally getting some good news about the local housing market. Case in point: the most recent housing stats from the Northwest Multiple Listing Service reported gains throughout the Puget Sound region, including a ten percent increase in home prices in Seattle. Appreciation is usually an indicator of a strengthening housing market, so we’re cautiously optimistic about where things are heading.

Understanding the ups and downs of real estate can be quite challenging, so several years ago Windermere partnered with economist Matthew Gardner to get the most current, relevant data about the Western Washington housing market into the hands of our agents and their clients. Unlike the Case-Shiller Home Price Index, which defines “Seattle” as King, Pierce, and Snohomish Counties, the Gardner Report dives into housing data on a far more local level and explains in detail what the numbers really mean. It analyzes employment figures, population growth, local business activity, and other factors that affect the housing market, such as distressed property sales.

Foreclosures and short sales have had a significant impact on the nation’s housing market, and Seattle is no exception. But, as the most recent Gardner Report points out, there is a light at the end of this tunnel in the form of “cash buyers”. A recent spike in the number of cash buyers in Seattle strongly indicates that real estate investors have returned to the market – and this helps deplete distressed inventory, resulting in less downward pressure on prices. And in the long run, both buyers and sellers benefit from a more stable, balanced market.

We’re proud to be able to offer a study of the Western Washington housing market through the Gardner Report, but ultimately all real estate is local. Hyper local. Market conditions can vary drastically within a single neighborhood. That’s why it’s important to always look to your real estate agent for expert insight. No one knows the local market like they do – or understands how those conditions can, and should, impact your long-term home buying and selling decisions.

Right now, the talk around Seattle, where I live and work, is all about the long-awaited rise in home prices.

On a local, as well as national, basis there is clear evidence of home values rising so far this summer. Several data sources that look at national price levels are all showing roughly the same, but there was one that stuck out. Clear Capital published a report suggesting that sale prices were up by 1.7% across the U.S. during the second quarter, and that “the West led the regions in price recovery and forecasted growth.”

They even went as far as to suggest that the Seattle-Bellevue-Tacoma market should exhibit annual price growth of 14.4% by year’s end, and that this market ranked first out of all the metropolitan areas analyzed.

But before we start celebrating the long awaited return of the market, I want to add a few words of caution to this very rosy story.

The data that I am looking at does, indeed, show several regions that have seen an extraordinarily good second quarter, but there is also data that suggests that we should not get too excited too quickly – and it’s all about foreclosures.

Whilst it’s undoubtedly true that foreclosures brought home prices down initially, they actually then started driving them up due to rabid demand from both investors and first-time buyers who were looking for bargains. (This has certainly been the case here in Seattle where over 30% of all transactions in 2011 were all-cash, investor purchases.)

Supplies of these cheap homes have now started to dwindle as banks continue their efforts to modify many underwater loans. Additionally, states that require a judge in the foreclosure process are facing a huge backlog that is dramatically lowering — albeit temporarily — the number of distressed units for sale.

Additional scrutiny on how lenders and servicers process foreclosures, along with aggressive foreclosure prevention efforts by the federal government, and several state governments, continue to hobble the foreclosure market at a national level.

Combining these two things indicates that prices are now being driven higher by the sale of more expensive, non-distressed units.

“So it’s all good”, I hear you way. Well hold on just a minute.

Overall foreclosure activity was down in the second quarter of this year, driven primarily by a drop in bank repossessions (REO’s). But according to RealtyTrak, 311,010 properties started the foreclosure process during second quarter, which represents a nine percent increase from the previous quarter and a six percent increase from the second quarter of 2011. This marks the first year-over-year increase in quarterly foreclosure starts since the fourth quarter of 2009.

It looks to me as if lenders are now, slowly but surely, catching up with the backlog of delinquent loans, which is why the average time to complete the foreclosure process started to level off, or decrease in some states, in the second quarter.

I believe that the increases in foreclosure starts in the first half of this year will likely translate into more short sales and bank repossessions in the second half of 2012 and into next year.

What does this mean? If we see a dramatic increase in distressed listings, in concert with a persistently low level of non-distressed homes coming to market, we are sure to lose the price gains that we have been seeing recently.

That said, I would add that not all markets are equal, and some will certainly do better than others, but I am afraid that it is still too early to call a bottom on the U.S. housing market just yet.

Have you ever wondered if your real estate agent understands what you are going through? They come into your house speaking confidently about your neighborhood and market trends. They have vendors ready to help you prepare your home for sale. But do they really think it’s that easy? Do they understand the conversations that follow once they’ve left your dining room table? Have they lain awake at night in worry?

You might be surprised.

I’ve been a real estate agent for eight years and recently attempted to sell my condo. My income hadn’t been what I’d planned; I was upside down and worried about the risks of holding onto it. I wanted less stress, so after months of consideration, I decided to sell.

Here’s how it went down:

-I chose my agent and sat down for a meeting. “Are you willing to meet the market?” she asked? That wasn’t easy to answer! The choices I’d made at purchase (lay out, upgrades, etc.) weren’t as valuable in her eyes as I had anticipated. I tried to fight the urge to feel that my home was worth more than she did.

-We moved out of the condo and hired a great stager to “edit” what we’d left behind. What?! You don’t like the black and white poster of John Lennon from my mother’s Let It Be album?!

-We had handiwork done and a professional photographer shot some great images. My agent listed the property, but after only one day on the market without an offer, I was already anxious.

-Then the Homeowners Association sued the developer (long story, but in short: not good for sales) and convinced me that I was definitely not prepared to meet the market. So, we removed the home from the market, and moved back in.

-Then, the phone rang. Agents wanted to show it, earnestly offering “My clients aren’t concerned with litigation.” Surprise: I didn’t believe it. Right or wrong, I suspected that these well-meaning people would not make it all the way to closing. I wasn’t ready to board that roller coaster.

And, it felt like the market was finally turning.

A property that had once seemed like a heavy weight began again to look like home; like a place that – from a post-tax perspective – is only marginally more costly than renting. So, here I am, happy with my decision to stay in my home and reminded what it’s like to walk in my sellers’ shoes – a win-win situation all the way around.

Michael Doyle is an agent with Windermere Real Estate’s Lakeview office in Seattle, WA.

Q: How does a short sale affect a homeowner’s credit score as compared to a foreclosure?

A: If the homeowner is participating in the federal government’s Home Affordable Foreclosure Alternatives (HAFA) Program, there are definite credit benefits to choosing a short sale over foreclosure. Recent changes to the HAFA Program dictate what the lender can state on the borrower’s credit report after a short sale, and lessens the impact on the borrower’s credit rating. Credit bureau reporting of HAFA transactions where the deficiency is forgiven is now to be reported as “Paid or closed account/zero balance” or “Account paid in full/a foreclosure was started”, as applicable. A short sale is usually reported as “Account paid for less than the full balance”, or similar statements which have a negative affect on the homeowner’s credit score.

While doing a short sale will negatively affect credit, short sales by their very nature may well have a lesser effect on credit than foreclosures. For instance, a completed foreclosure means the borrower has, at a very minimum, missed six months of payments (often considerably more). The property has also gone through a completed foreclosure sale. So while a short sale negatively impacts credit, the effect has been shown to be less than a full blown foreclosure which followed months, if not years, of missed payments.

Some people feel there is a much stronger social stigma attached to foreclosure as compared to a short sale. With a short sale, the homeowner is in control of the sale, not the bank. In fact, today cash incentives may be available to homeowners who decide to do a short sale instead of foreclosure. When the consumer wants to obtain a loan to purchase a property in the future, more opportunities will be available to them sooner if they do a short sale. For example, contrary to popular belief, one can be current on their payments and still do a short sale. And if a homeowner is current on their mortgage through a short sale, they can qualify for an FHAloan afterwards without any waiting periods. The same option is not available following a foreclosure.

Every homeowner’s situation is different, so we always recommend speaking with a real estate attorney who can offer advice on the legal and tax implications for each individual’s circumstances.

What are your real estate questions?

By Martin Goldberg

Martin Goldberg has been successfully negotiating short sales since 2003. Martin is a Windermere broker and partner in Washington Property Solutions, a company that helps brokers and homeowners successfully negotiate short sales. A Washington native, Martin graduated with honors from the University of Washington Law School and worked as an attorney at the Seattle law firm of Perkins Coie, was pioneering technology company Real Networks’ first lawyer, and then worked as in-house legal counsel for an Internet startup before making real estate his career. His 15 minutes of fame (actually 30 seconds) was as an extra on the TV show Northern Exposure. Martin lives in Bellevue with his wife and two children, who he takes on road trips whenever possible. He loves to explore the nooks and crannies of the United States, and has logged trips to 49 states.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Summer is finally here, and like many of you, when the weather turns nice we find ourselves smiling a little more. Our whole mood changes for the better. Maybe it’s the much-needed dose of vitamin D – or perhaps it’s that we’re finally getting some good news about the local housing market. Case in point: the most recent housing stats from the Northwest Multiple Listing Service reported gains throughout the Puget Sound region, including a ten percent increase in home prices in Seattle. Appreciation is usually an indicator of a strengthening housing market, so we’re cautiously optimistic about where things are heading.

Summer is finally here, and like many of you, when the weather turns nice we find ourselves smiling a little more. Our whole mood changes for the better. Maybe it’s the much-needed dose of vitamin D – or perhaps it’s that we’re finally getting some good news about the local housing market. Case in point: the most recent housing stats from the Northwest Multiple Listing Service reported gains throughout the Puget Sound region, including a ten percent increase in home prices in Seattle. Appreciation is usually an indicator of a strengthening housing market, so we’re cautiously optimistic about where things are heading.

")

{kind=link}

{kind=link}