Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This is the latest in a series of videos with Windermere Principal Economist Jeff Tucker, where he delivers the key economic numbers to follow to keep you well-informed about what’s going on in the real estate market.

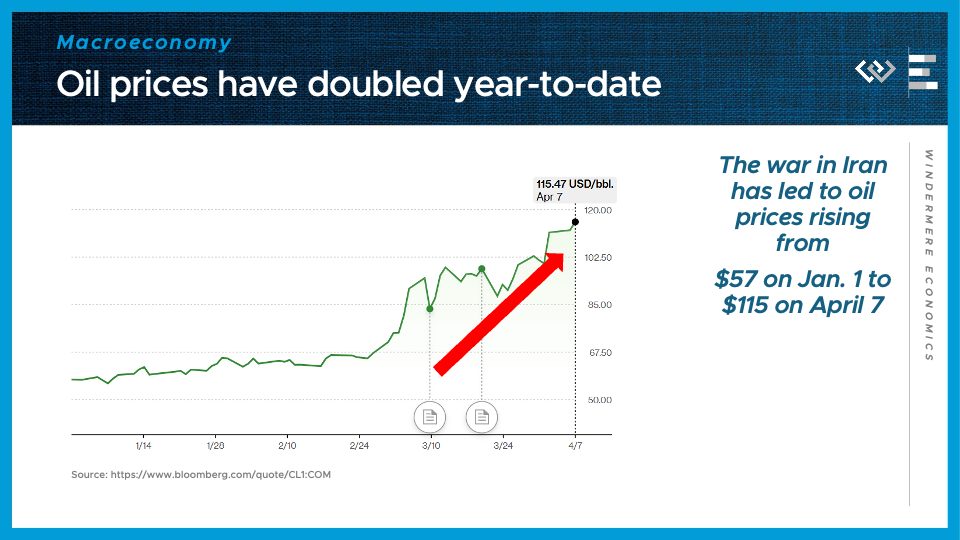

The first number to know this month: $115. That was the level that price of a barrel of oil reached on April 7, and it happens to be exactly double the price of oil at the start of 2026. The war in Iran has dragged on into its second month now, and it’s continuing to cause an energy crisis that’s rippling out through the global economy. An energy shock like this raises the costs of making and transporting almost everything, so the longer this goes on, the more inflationary pain it will inflict this year.

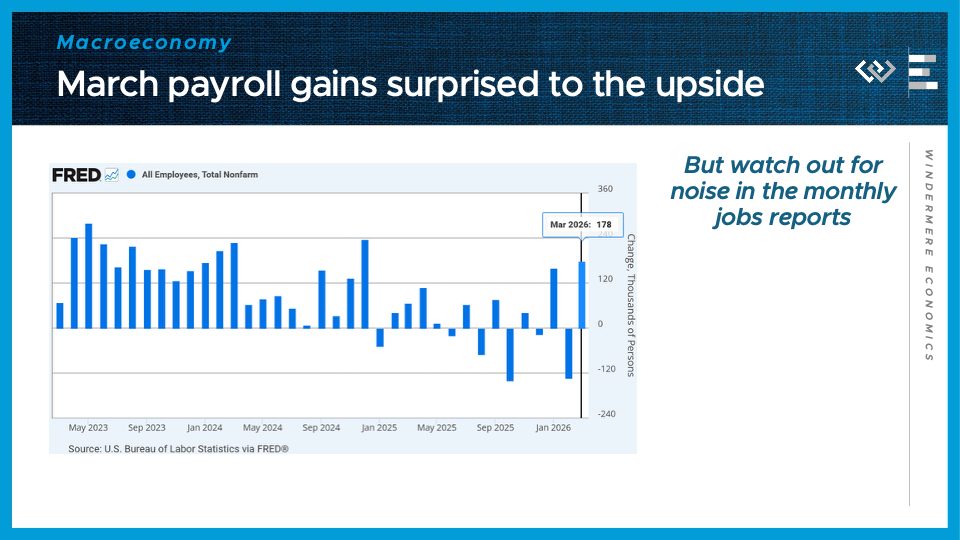

The second number to know this month 178,000. That was the number of jobs added in the economy in March, which would make it the single best month for job gains since late 2024, if it survives the usual rounds of revisions. If we look at the trend of the last 15 months, though, it’s pointing both toward a slowdown in job gains, and a increasing month-to-month volatility, as we’ve now swung between job gains and job losses for 11 months in a row. One upshot of this strong jobs report is that it provides further cover for the Federal Reserve to keep interest rate cuts on hold for now – if the labor market isn’t looking too distressed, they don’t need to be rushing to the rescue.

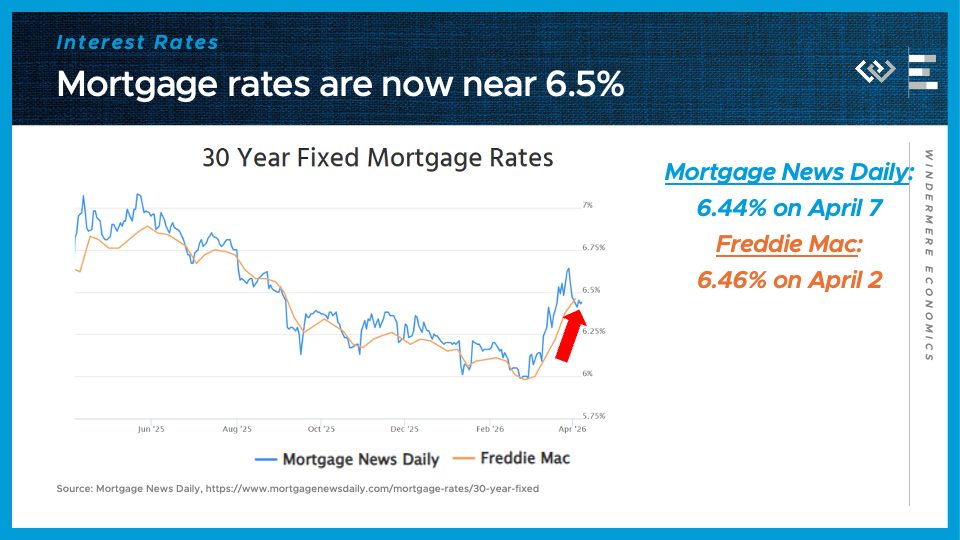

The third number to know this month: 6 and a half percent. That’s the ballpark of where 30-year mortgage rates are now bouncing around, after jumping almost half a point from multi-year lows they reached just back in late February. The combination of higher inflation and tighter monetary policy triggered by the war in Iran has set interest rates back up to where they were last summer, and frankly into the range of where they stood last spring. This is undermining homebuyer demand in what should be the busy spring buying season, leading instead to more balanced conditions in the housing market.

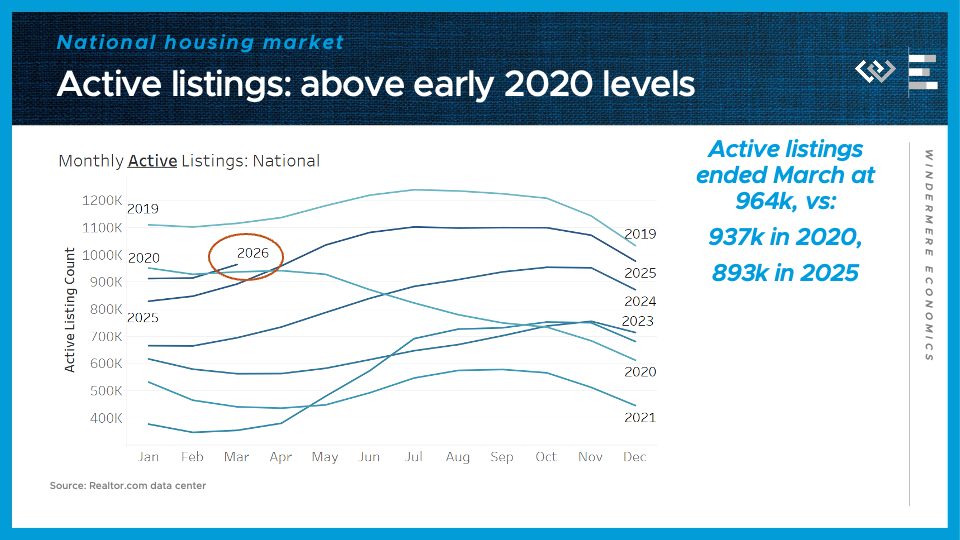

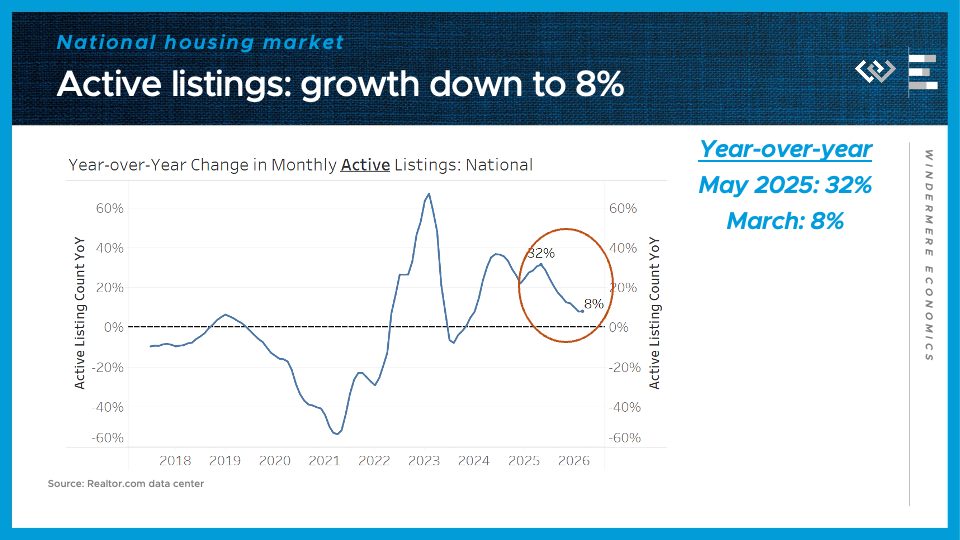

Finally, turning to the housing market, we saw 964 thousand active listings at the end of March—somewhat more than at this time in 2020, and about 8% more than last year.

That 8% year-over-year gain basically matches what I reported in February, bringing an end to a trend of decelerating inventory growth since last May. It’s a little early to call this a turning point, but it may be an indication that inventory gains are picking back up. If that continues, buyers could really see a plethora of options on the market this summer. In the meantime, sellers should be aware that buyers are comparison-shopping, so it still pays to put your best foot forward, listing with an agent you trust, even in the busy spring selling season right now.

")