Hi, I’m Jeff Tucker, principal economist at Windermere Real Estate, and these are the numbers to know, right now.

The first number to know this month: $78.

That is the current price of a barrel of oil as of June 16, after falling about $30 in just the last month. Much of that decline follows from the signed memorandum of understanding between the US and Iran, hopefully marking the beginning of the end of the war that has closed the straits of Hormuz.

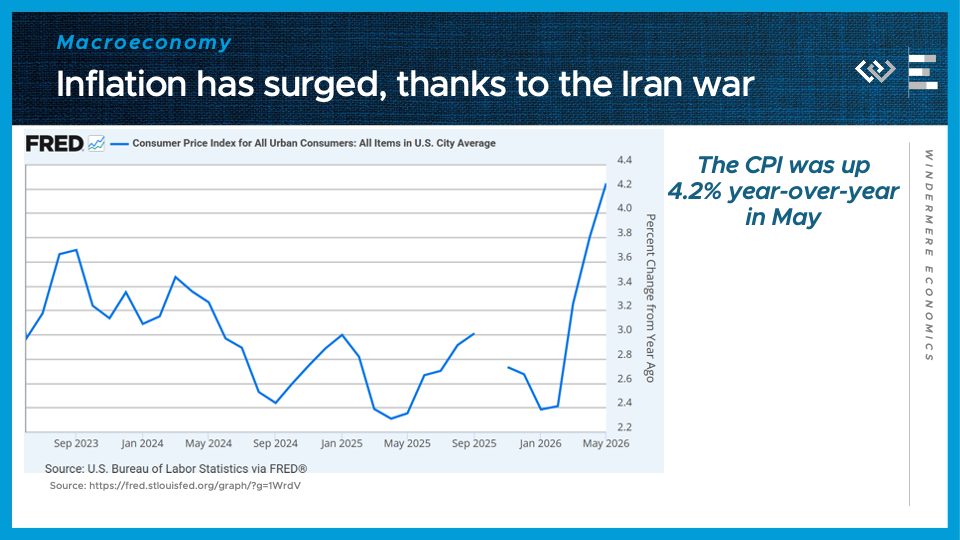

The second number to know this month: 4.2%.

That is the current year-over-year pace of inflation as of May, and it’s the highest annual rate of inflation in over 3 years. It reflects the cost pressures from the Iran War disruptions still rippling out through the economy.

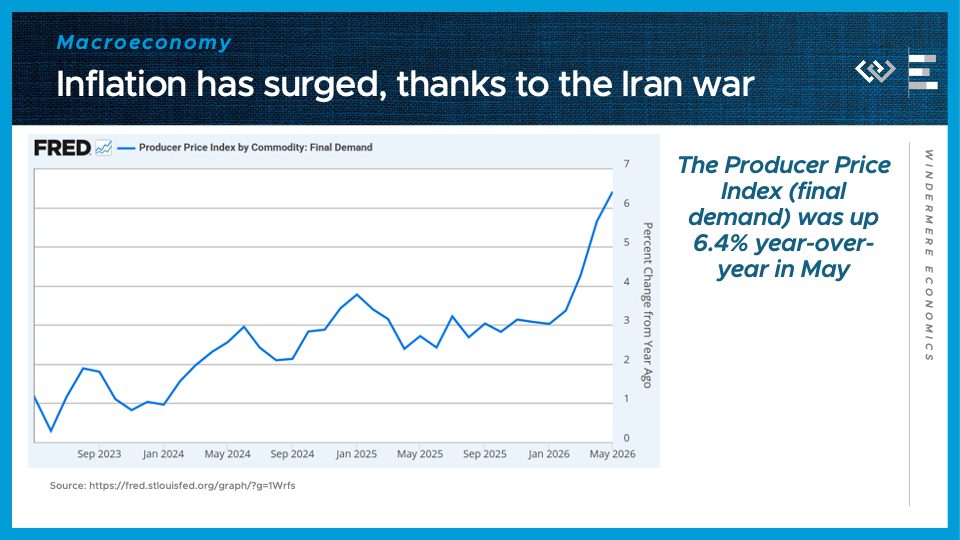

The Producer Price Index, which measures cost pressures further upstream in the supply chain, also continued accelerating in May, to 6.2%. Hopefully, this should begin to decelerate as lower oil prices bring down costs in the economy.

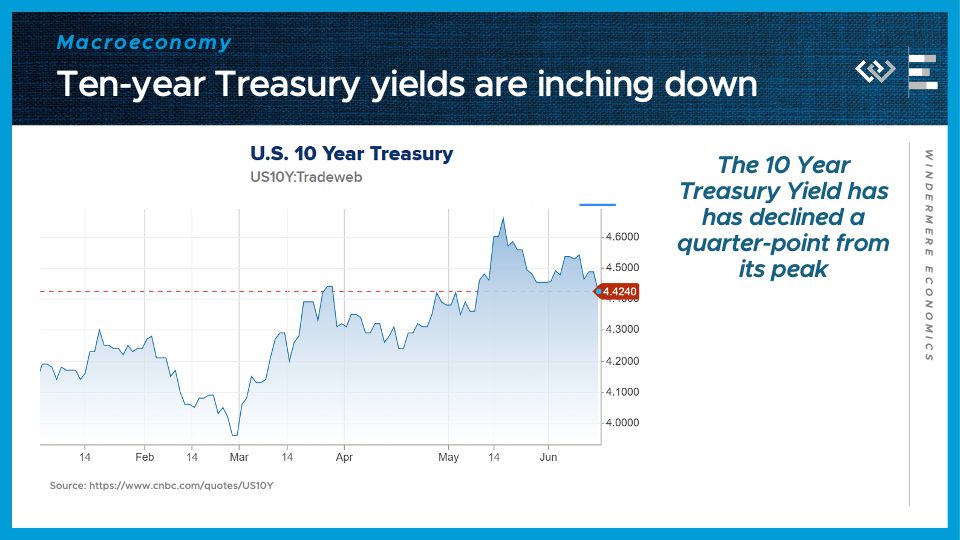

Bond yields are still elevated but they’ve begun to decline – the Ten-year Treasury yield has come back down about a quarter point from its peak in mid-May.

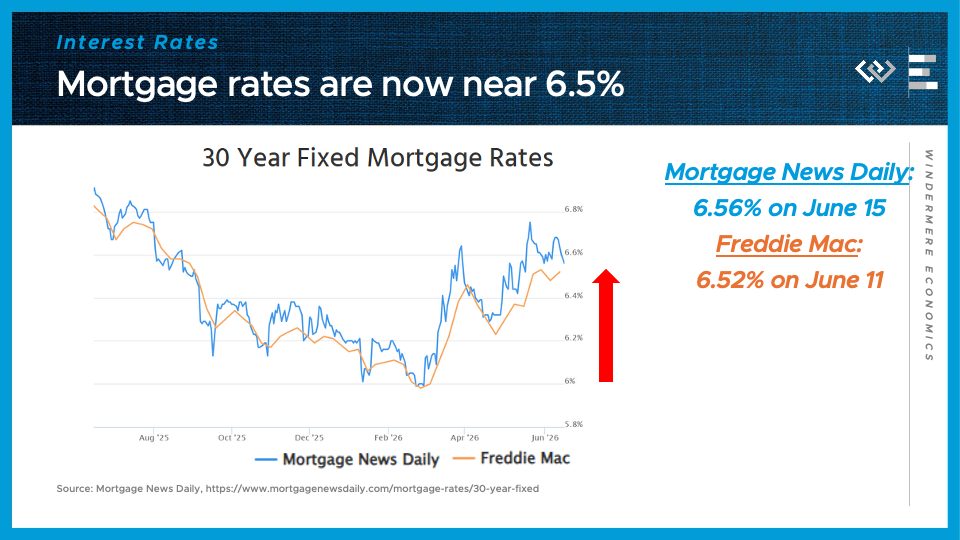

Similarly, 30-year mortgage rates are starting to come back down, but remain much higher than earlier this year: both Mortgage News Daily and Freddie Mac report average mortgage rates slightly above 6 and a half percent.

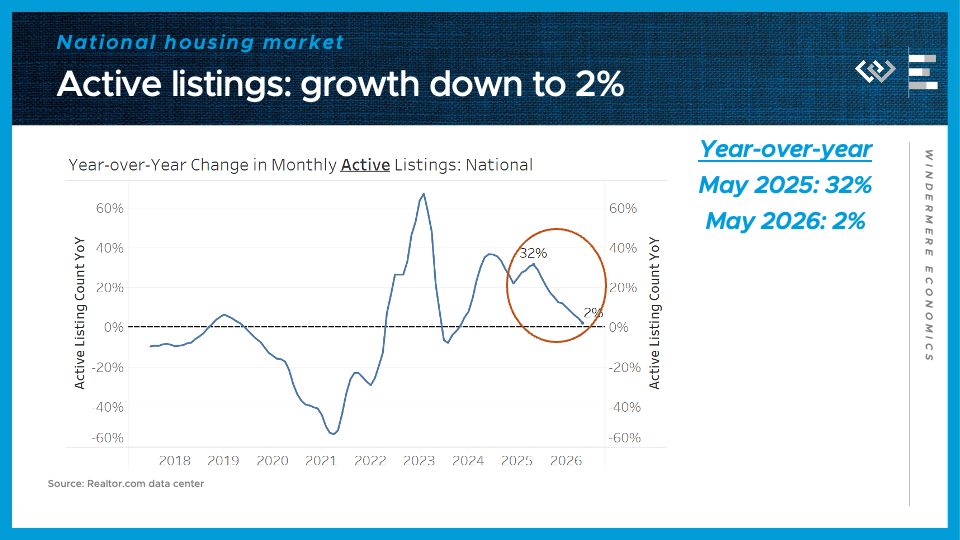

Speaking of the housing market, inventory growth slowed down again in May, which ended with just 2% more active listings than this time last year.

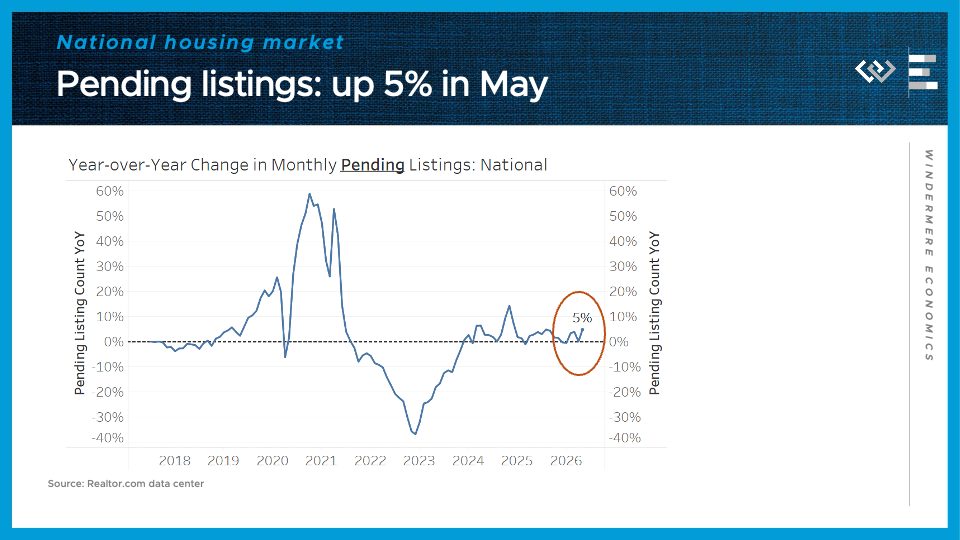

And most surprisingly, pending sales in May were up 5% year-over-year, according to Realtor.com, which marks a belated pickup in demand to close out the spring selling season on a higher note.

If mortgage rates continue to come back down, that strength in sales activity could continue into the summer.

There are a variety of reasons that a homeowner may decide to remodel their bathroom; they could be looking to increase the value of their home for a future sale, they may have discovered repairs that need to be made, or perhaps they’re simply looking to maximize their enjoyment of the space. Whatever your motivation may be, consider the following information before the hammer hits the tile to make sure your bathroom remodel turns out as successful as you’d hoped.

A Guide to Remodeling Your Bathroom

Which bathroom remodel projects have the highest ROI?

Before you decide which projects to tackle, it’s worth your while to identify which bathroom remodeling projects have the highest ROI. This can be especially helpful if you’re thinking about selling your home in the near future. According to the National Association of REALTORS’ 2025 Remodeling Impact Report (www.nar.realtor.com), bathroom renovations are still a worthwhile investment, but homeowners should have realistic expectations about the return. On average, a bathroom renovation recoups about 50% of its cost at resale, while adding a new bathroom can recover approximately 56%. While these projects can make your home more functional and appealing to buyers, they’re often approached with long-term enjoyment in mind rather than the expectation of recovering ever dollar spent. If you’re preparing to list your home, talk with your agent about which bathroom projects are seeing the highest return in your local market.

How can I save on my bathroom remodel?

There are various ways to keep your costs down when remodeling your bathroom, but it depends on the scope of your project. If, while preparing to sell your home, you identify a handful of outstanding repairs that need to be fixed before you list, it may be difficult to pull off a low-budget bathroom remodel while still fetching a competitive sales price. Neglecting these issues can be a costly mistake, and in some cases can even jeopardize a sale.

One way to save money on your bathroom remodel is to do it yourself. Identify the pros and cons of either doing a project DIY or hiring a professional. Though you may save money on labor, if you get in over your head on a project the costs can add up quickly, and you may end up having to hire a contractor to remedy the situation. If you decide to hire a contractor, thoroughly research multiple companies, ask for referrals from family and friends, and get multiple quotes before deciding which is best for the job.

Simple Bathroom Upgrades

As the scope of a bathroom remodel changes, so does the overall cost. Simple cosmetic updates like replacing fixtures, painting cabinets, or installing new hardware can often be completed on a modest budget, while full renovations that involve moving plumbing, expanding the space, or installing high-end finishes require a much larger investment. Fortunately, you don’t have to spend a fortune to make a meaningful impact. Thoughtful, budget-friendly updates can go a long way in refreshing the look and feel of your bathroom. Here are a few ideas for budget-friendly bathroom upgrades.

Refinish Your Tub: Remove all hardware from your tub and sand the entire surface smooth, evening out any chips or cracks and filling them with epoxy. Once the epoxy has dried, sand those areas one more time. Apply multiple layers of primer and topcoat as advised and buff the surface to finish off the job.

Add Décor: A well-decorated bathroom can revitalize the space. Add a fresh coat of paint to the walls, install a new faucet and shower head, and match your towel rods and shower curtains for a quick bathroom refresh.

Finishing Touches: The right bathroom lighting can make all the difference. Experiment with softer light bulbs or dimmers to create a sense of calm and relaxation. Add candles, scented oils, and new towels to make your bathroom feel like your own personal spa.

For more ideas on remodels, décor, and all things home design, visit the design page on our blog.

Moving is an exciting milestone, but it also comes with a long list of tasks and deadlines to manage, especially if you’re buying and selling a home at the same time. Whether you’re moving across town or across the country, staying organized can help make the process significantly less stressful.

From hiring movers and transferring utilities to packing essentials and settling into your new home, this step-by-step moving checklist will keep your move on track from start to finish.

A Step-By-Step Guide to the Moving Process

We’ve included a comprehensive checklist below of all the steps you’ll need to complete to ensure a smooth, successful move. This list is also available as an interactive web page and downloadable PDF here: Moving Checklist

Twelve Weeks Before:

Get estimates from professional movers or truck rental companies if needed.

Once you’ve selected a mover, discuss insurance, packing, loading and delivery, and the claims procedure.

Six to Eight Weeks Before:

Use up things that may be difficult to move, such as frozen food.

Sort through your possessions. Decide what you want to keep, what you want to sell, and what you wish to donate to charity.

Record serial numbers on electronic equipment, take photos (or video) of all your belongings and create an inventory list.

If you are moving yourself, use your inventory list to determine how many boxes you will need. Stock up on the items you’ll need from our “Moving Essentials” list.

Submit a change of address request through the USPS and update your address with banks, employers, insurance providers, subscription services, and other important accounts.

If you believe your move may qualify for tax-related benefits or deductions, consult a qualified tax professional.

If you’re moving to a new community, contact the Chamber of Commerce and school district and request information about services.

Make reservations with airlines, hotels, and car rental agencies, if needed.

Begin packing nonessential items.

Two to Four Weeks Before:

Arrange for storage, if needed.

If you have items you don’t want to pack and move, hold a yard sale.

Update the address listed on your car registration, license, and insurance.

Transfer your bank accounts and safe-deposit box items to new branch locations if needed. Cancel or redirect any direct deposit or automatic payments from your accounts.

Make special arrangements to move your pets, including updating identification tags and microchip information, gathering veterinary records, and creating a travel plan that keeps them comfortable throughout the move.

Have your car checked and serviced if you’ll need to drive it a long distance.

Change your utilities, including phone, power, and water, from your old address to your new address.

Digital Moving Checklist:

Transfer internet and streaming services.

Update your address for online shopping accounts and subscriptions.

Update banking, insurance, and employer records.

Back up important digital files and documents before your move.

Week of Moving Day:

Defrost your refrigerator and freezer.

Have movers pack your belongings.

Label each box with the contents and the room where you want it to be delivered.

If you’re using a moving company, arrange to pay for their services in full, or the remainder of what you owe, upon delivery.

Set aside legal documents and valuables that you do not want packed.

Pack clothing and toiletries, along with extra clothes in case the moving company is delayed.

Give your travel itinerary to a close friend or relative so they can reach you as needed.

Pack a first-day box with items that you’ll want accessible before other boxes are unpacked. See our list of suggested items on the right and add any others you’ll want to include.

Moving Day:

Old Home

Pick up the truck as early as possible if you are moving yourself.

Make a list of every item and box loaded on the truck.

Let the mover know how to reach you.

Double-check your closets, cupboards, attic, basement, yard, and garage for any left-behind items.

New Home

Be on hand at the new home to answer questions and give instructions to the mover.

Check off boxes and items as they come off the truck.

Confirm that the utilities have been turned on and are ready for use.

Unpack your first-day box.

Unpack your children’s toys and find a safe place for them to play.

Examine your goods for damage.

FAQs About Moving:

When Should I Start Preparing for a Move?

Most moving professionals recommend beginning preparations at least six to eight weeks before moving day.

Should I Hire Movers or Move Myself?

The right choice depends on your budget, timeline, distance, and the amount of belongings you need to transport.

What Should I Pack in a First-Day Box?

Include toiletries, medications, chargers, important documents, snacks, basic cleaning supplies, and a change of clothes.

When Should I Transfer Utilities?

Most utility transfers should be scheduled two to four weeks before moving day to help avoid service interruptions.

Our Moving Checklist page has all the information above, plus helpful lists for Moving Essentials and which items to pack in your First-Day Box available as a downloadable PDF.

For additional information on the selling process from start to finish, tips on working with an agent, and more, visit our Home Selling Guide:

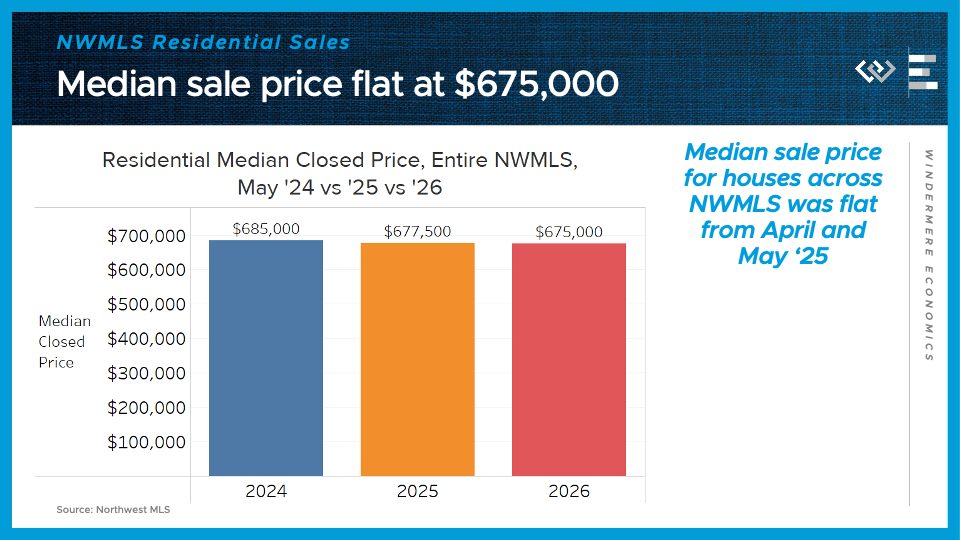

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the May 2026 data from the Northwest MLS.

As we approach the end of the spring selling season, we can now say it was a bit disappointing for sellers. On the flipside, that means this summer will likely provide some bargains for buyers who are in a position to act.

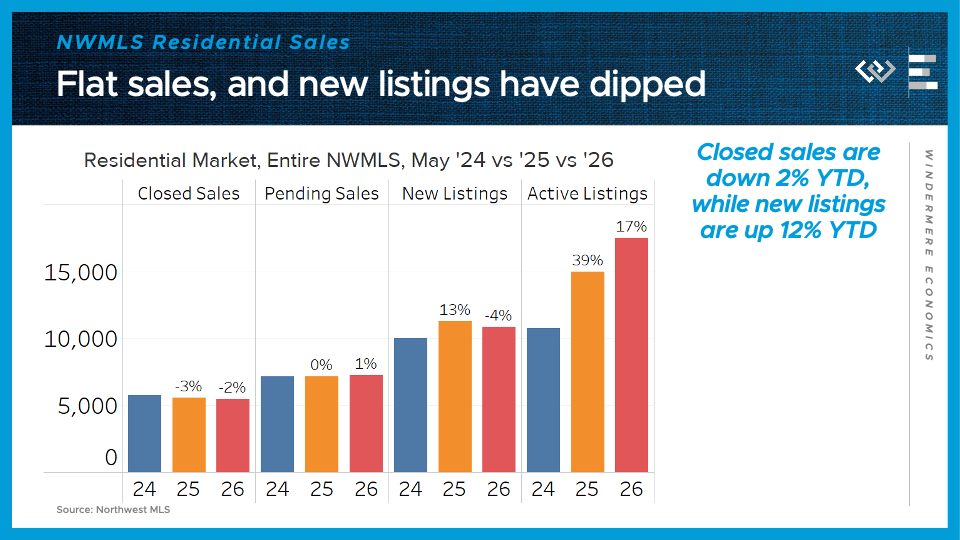

Across the entire Northwest MLS, there were 2% fewer closed sales in May 2026 than in May of last year – the same drop we saw in April. Pending home sales ticked up by 1% from last year.

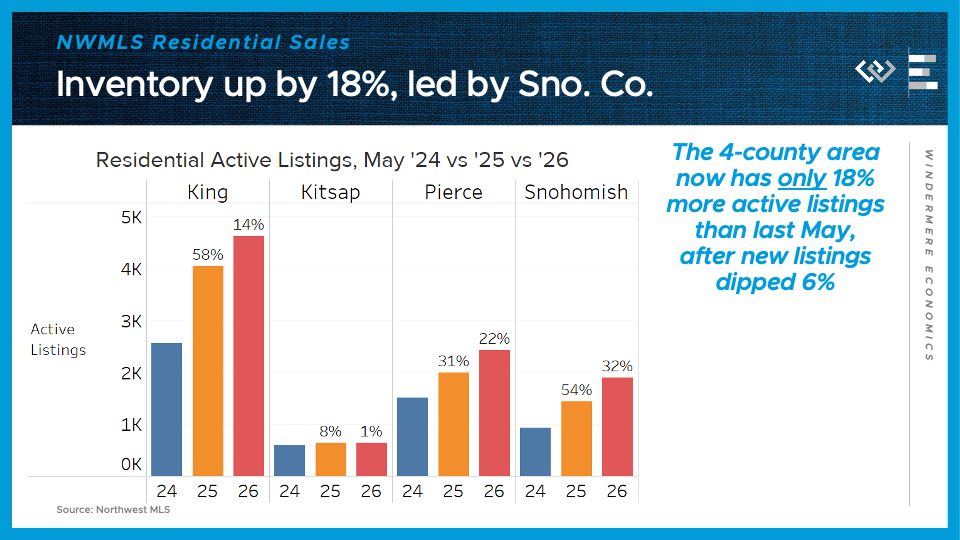

The big news in this month’s release was on the supply side, where the flow of new listings was 4% less than in May of 2025 – that’s the first slowdown in new listings all year. Finally, the month ended with just over 17,500 active listings around the MLS, or 17% more than last May, after it was up 30% in April. That tells me sellers have picked up on the softer demand signals this spring and they’ve begun to pull back. That’ll be an important trend to track in the months ahead to see if it continues.

The median sale price ticked down from last May, by just $2500, leaving it basically flat at $675,000.

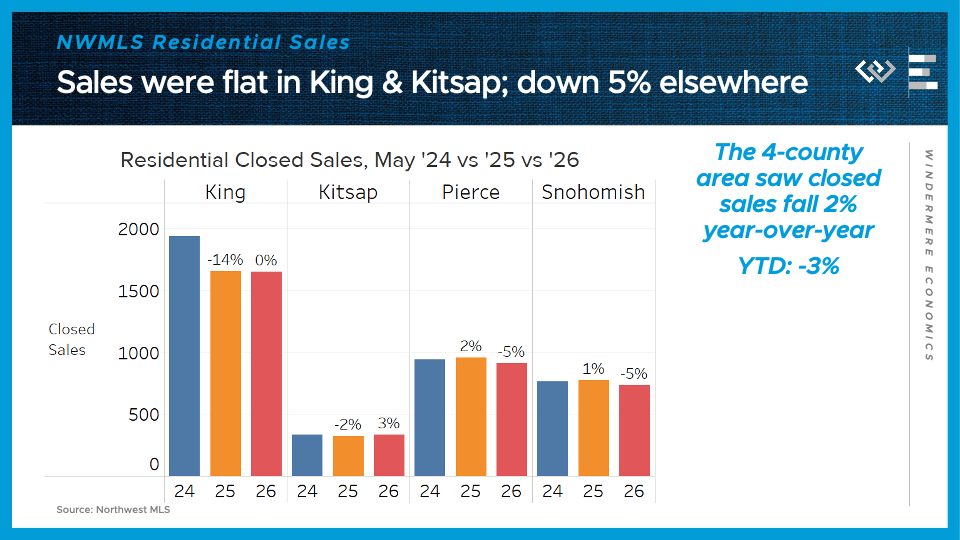

Now I’ll take a closer look at the four counties encompassing the greater Seattle area.

Closed sales declined by 2%, or about 80 homes, from last May around the region. Snohomish and Pierce Counties led that decline by 5% each, while King County was flat and Kitsap saw sales pick up a bit. Still, that left King County well below 2024’s sales volume.

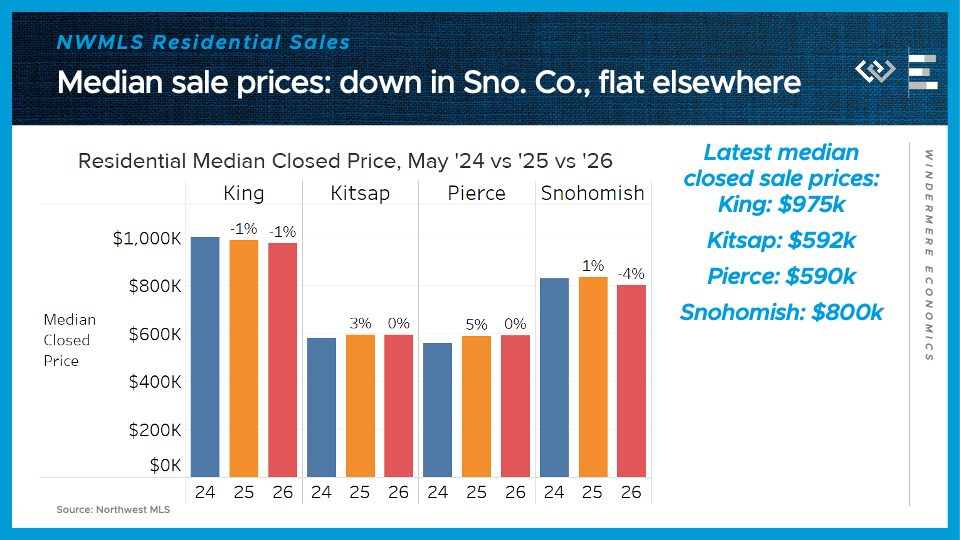

Median sale prices were flat, or down slightly, all around the region – down the most, by 4%, in Snohomish County to $800,000, while they’ve inched down to $975,000 here in King County.

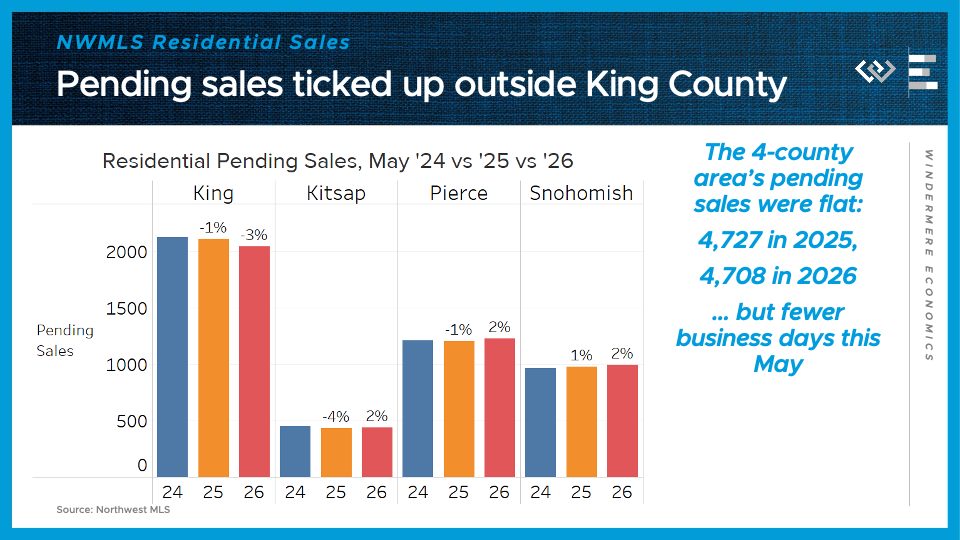

Looking ahead, pending sales were flat around the region, with a drop of 3% in King County. That’s a little ambiguous, though, because this May did end on a Sunday, when pending sales are rarely recorded. For that reason I expect a little pickup in pending sales in June.

On the supply side, the 4-county greater Seattle area ended the month with only 18% more active listings than last May, a sharp slowdown from the 37% growth in April. Every county saw a sharp slowdown in the growth of active listings, which could mark an inflection point in this cycle.

All in all, the local housing data painted a picture of an unusually buyer-friendly spring selling season this May here in the greater Seattle area, as prices cool down slightly and sales activity falls short of last year’s. Now we are approaching the time of year with peak inventory, and near-peak buying activity, so I still expect plenty of time for more buyers to find the right home, amid a slightly less frenzied setting. If geopolitical news improves and mortgage rates come back down toward 6%, the market could even catch a second wind; but in the meantime, the data suggests that sellers benefit now more than ever from a professional, polished listing when they go to sell their house in this quiet late spring market.

Buying a home comes with plenty of exciting milestones like touring properties, envisioning your future space, and making an offer. But before you get the keys, there’s one piece of the process that often feels the most intimidating: financing.

From fixed-rate loans and adjustable-rate mortgages to FHA and VA programs, today’s buyers have more financing options than ever before. Understanding the basics can help you feel more confident when it’s time to talk with a lender and determine what loan best aligns with your goals.

Whether you’re preparing to buy your first home or simply looking to refresh your knowledge, consider this your guide to mortgage basics.

What Is a Mortgage?

A mortgage is a loan used to purchase a home. Instead of paying the entire price of the property at once, homebuyers typically finance the purchase through a lender and make payments over time. Those payments typically principal and interest on the loan, property taxes, homeowners’ insurance, and, in some cases, mortgage insurance. The home serves as security for the loan until the borrower fully repays it.

Why Mortgage Choice Matters

Not all mortgages are created equal. The type of loan you choose can affect everything from your monthly payment and interest rate to your required down payment and long-term borrowing costs. Some loan programs may offer lower upfront costs, while others provide greater payment stability or flexibility down the road. That’s why working with both a trusted lender and a knowledgeable real estate professional can help ensure that you’re evaluating options that fit your financial picture—not just today, but years down the road.

Fixed-Rate vs. Adjustable-Rate Mortgages

One of the first decisions many buyers face is whether they prefer a fixed or adjustable interest rate. Let’s break them down.

Fixed-Rate Mortgage

Fixed-rate mortgages offer long-term consistency because the interest rate stays locked in for the duration of the loan, resulting in more stable monthly payments. This predictability makes fixed-rate loans especially appealing for buyers who plan to stay in their home for many years or simply prefer the peace of mind that comes with stable monthly housing costs. While fixed-rate mortgages can carry slightly higher initial rates than some adjustable-rate options, they offer protection against future rate increases and make long-term budgeting much easier.

Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage starts with a fixed interest rate for a set period, then transitions to a variable rate that can change with market conditions. You may see ARMs described as 5/1, 7/1, or 10/1 loans, with the first number representing the length of the introductory fixed-rate period and the second indicating how often the rate can adjust afterward. Because ARMs often begin with lower interest rates than fixed-rate mortgages, they can provide lower initial monthly payments. However, buyers should be aware that payments may increase if interest rates rise. For homeowners who anticipate moving, selling, or refinancing before the adjustment period begins, an ARM may be worth considering.

Understanding the Most Common Loan Programs

Beyond choosing between a fixed-rate and an adjustable-rate mortgage, buyers can select from several loan programs based on their financial situation, credit history, and homeownership goals. While a lender can help determine which option is best for you, understanding the basics can make conversations about financing feel much less overwhelming.

Conventional Loans

Conventional loans are one of the most common mortgage options and are typically provided by private lenders, including banks, credit unions, and mortgage companies. They are often a strong choice for buyers with solid credit, stable income, and funds available for a down payment. While some conventional loan programs allow down payments below 20%, borrowers may be required to pay private mortgage insurance (PMI) until they build enough equity in the home.

FHA Loans

Backed by the Federal Housing Administration, FHA loans help make homeownership more accessible for qualified buyers. Because they offer lower down payment options and more flexible credit requirements, these loans are a popular choice among many first-time homebuyers. Borrowers should keep in mind that mortgage insurance is typically required for the loan.

VA Loans

VA loans are available to eligible military service members, veterans, and certain surviving spouses. One of the program’s biggest advantages is that qualified borrowers can purchase a home with no down payment. VA loans also typically offer competitive interest rates and do not require private mortgage insurance.

USDA Loans

USDA loans are intended for eligible buyers purchasing homes in designated rural and suburban communities. Qualified borrowers may be able to purchase a home with no down payment and favorable financing terms, though income and location requirements apply.

Jumbo Loans

Jumbo loans are used when a home’s purchase price exceeds the loan limits established for conventional mortgages. These loans are often common in higher-cost real estate markets and may require stronger credit qualifications, larger down payments, and additional financial documentation during the approval process.

Choosing a Loan Term

In addition to selecting a loan type, buyers will also choose a loan term. The most common options are 15-year and 30-year mortgages. A 30-year mortgage often comes with lower monthly payments because the loan is repaid over a longer period, while a 15-year mortgage can offer lower interest rates and help homeowners build equity more quickly. Although monthly payments on a shorter-term loan are often higher, borrowers typically pay significantly less interest over the life of the loan.

Which Mortgage Is Right for You?

The best mortgage isn’t necessarily the one with the lowest rate—it’s the one that aligns with your budget, financial goals, and long-term plans. Factors such as your down payment, credit profile, anticipated homeownership lenght, and monthly budget can all influence which loan type makes the most sense. A trusted lender can help you compare options and understand how each program may impact your monthly payment and overall cost of homeownership.

How Much House Can You Afford?

While online calculators can provide a starting point, affordability involves more than a monthly mortgage payment. Buyers should consider existing debt obligations, emergency savings goals, everyday living expenses, future financial plans, property taxes, insurance costs, and ongoing home maintenance. Understanding the full picture can help ensure your home purchase supports your lifestyle rather than stretching your budget too thin.

The process of gradually paying off a loan through scheduled payments over time.

APR (Annual Percentage Rate)

A broader measure of borrowing cost that includes interest and certain lender fees.

Closing Costs

Expenses associated with finalizing a home purchase, often include lender fees, title services, escrow fees, and other transaction-related costs.

Down Payment

The portion of a home’s purchase price paid by the buyer upfront.

Escrow

An account used to hold funds for property taxes, homeowners’ insurance, and other transaction-related expenses.

Mortgage Insurance

Insurance that protects the lender if a borrower defaults on the loan. It may be required for certain loan types or lower down payment programs.

Preapproval

A lender’s preliminary review of your finances that estimates how much you may qualify to borrow.

Principal

The original amount borrowed before interest is applied.

The Bottom Line

Choosing a mortgage isn’t about finding a universally “best” loan—it’s about finding the option that best supports your financial goals, timeline, and homeownership plans.

The good news? You don’t have to navigate the process alone.

Ready to take the next step toward homeownership? Connect with a Windermere agent today to begin building your homeownership roadmap.

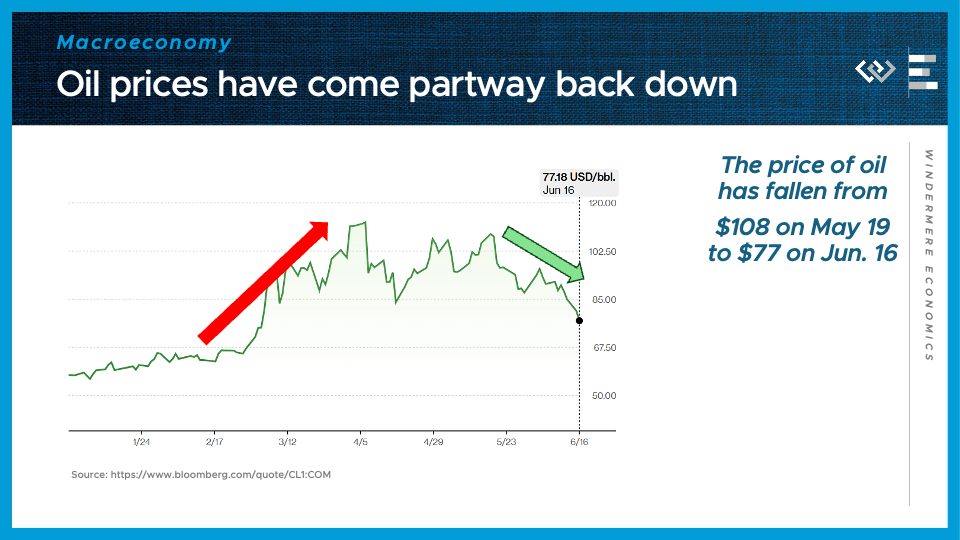

Hi, I’m Jeff Tucker, principal economist at Windermere Real Estate, and these are the numbers to know, right now.

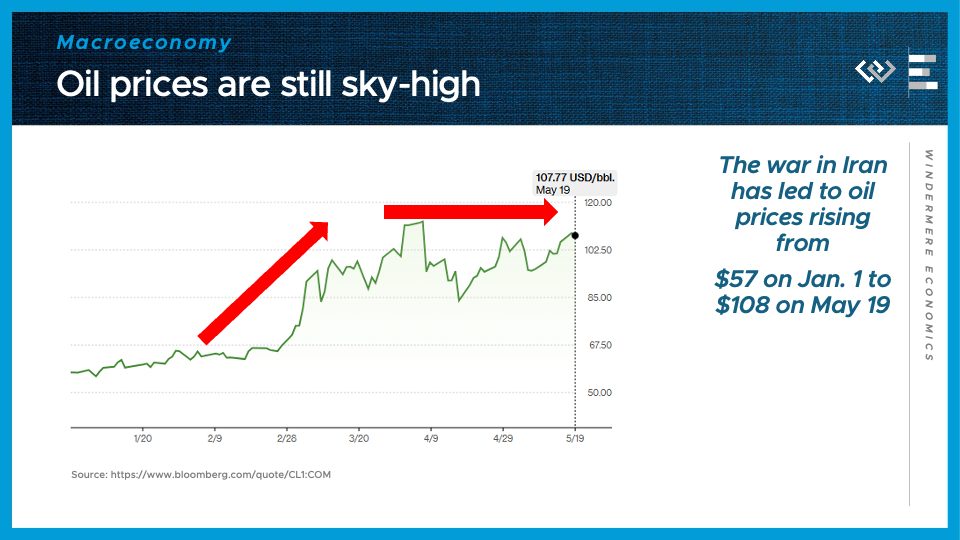

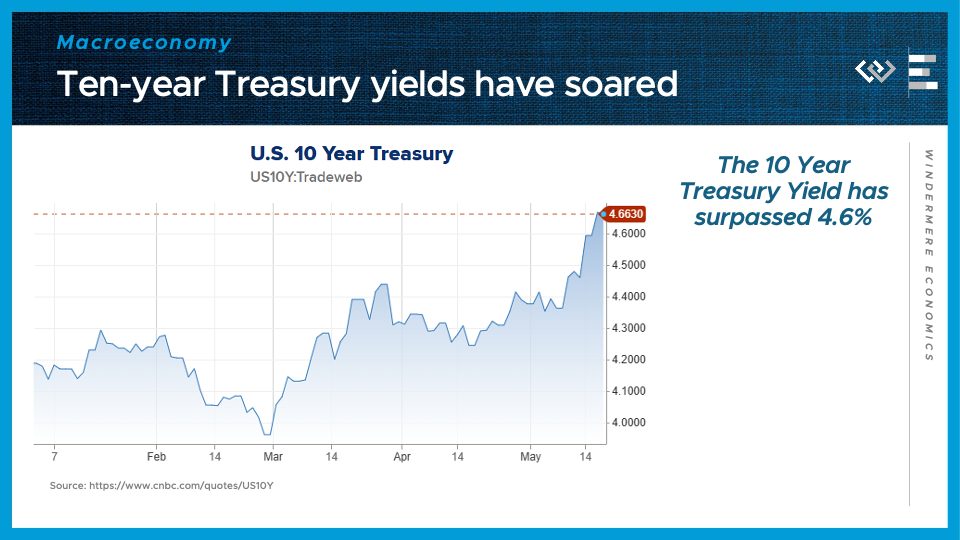

The first number to know this month: $108. That is the current price of a barrel of oil as of May 19, and it is still dramatically elevated from its price range below $60 before the U.S. launched a war on Iran this year. In fact, despite several tantalizing hints of the end of the hostilities tying up the Strait of Hormuz, prices have been over $85 a barrel pretty consistently for over two months now. As long as the flow of oil is constricted, those price pressures will stay elevated.

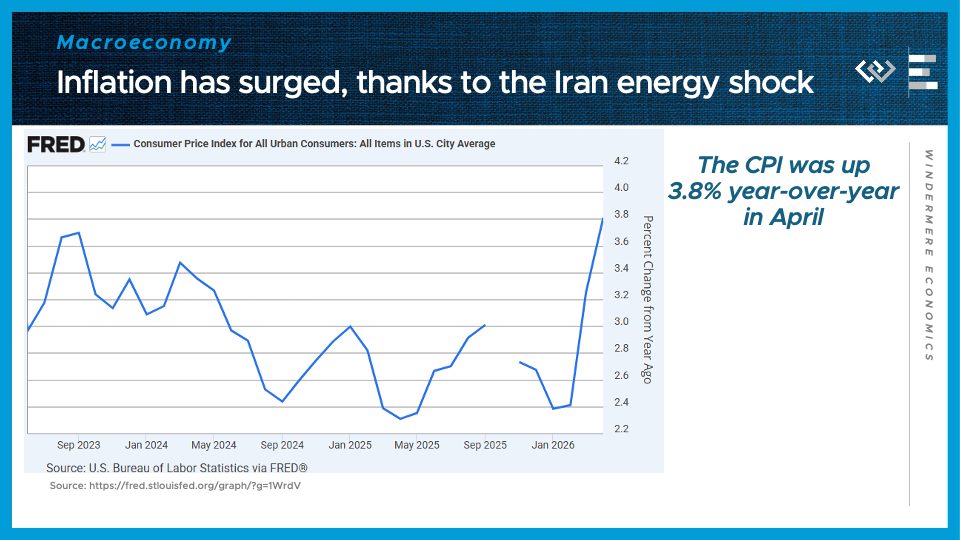

The second number to know this month: 3.8%. That is the year-over-year change in the consumer price index, representing a sharp acceleration of inflation from the 2.4% pace as recently as February. It reflects the higher costs of energy rippling through supply chains, and now inevitably raising prices for consumer products and services.

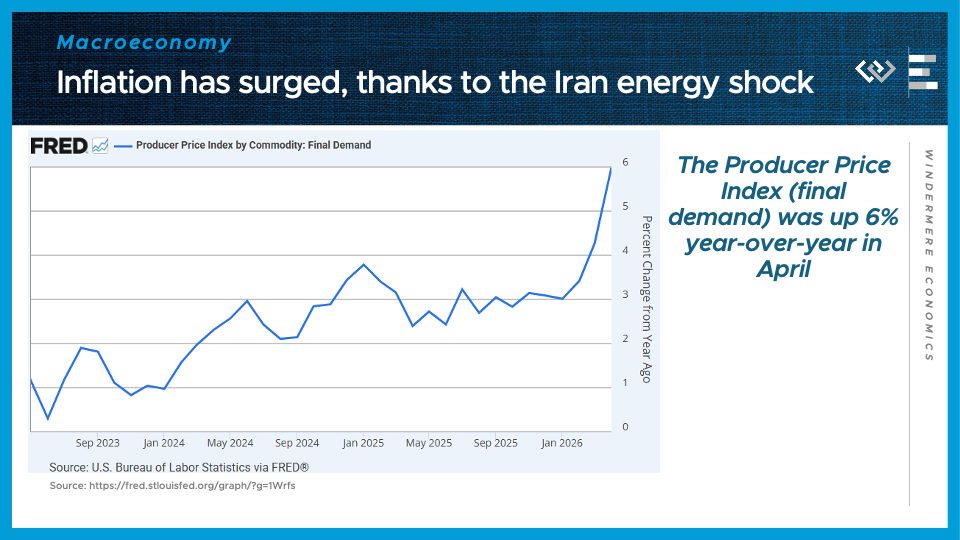

Moreover, the producer price index also just jumped sharply, to a 6% year-over-year gain, well above the consensus forecast, which is a good indicator of even more pain coming for consumers.

Higher inflation also tends to feed into the interest rates on bonds, and this spring has been no exception: now the ten-year Treasury bond is yielding around 4.6%, after dipping just under 4% on the eve of the Iran war.

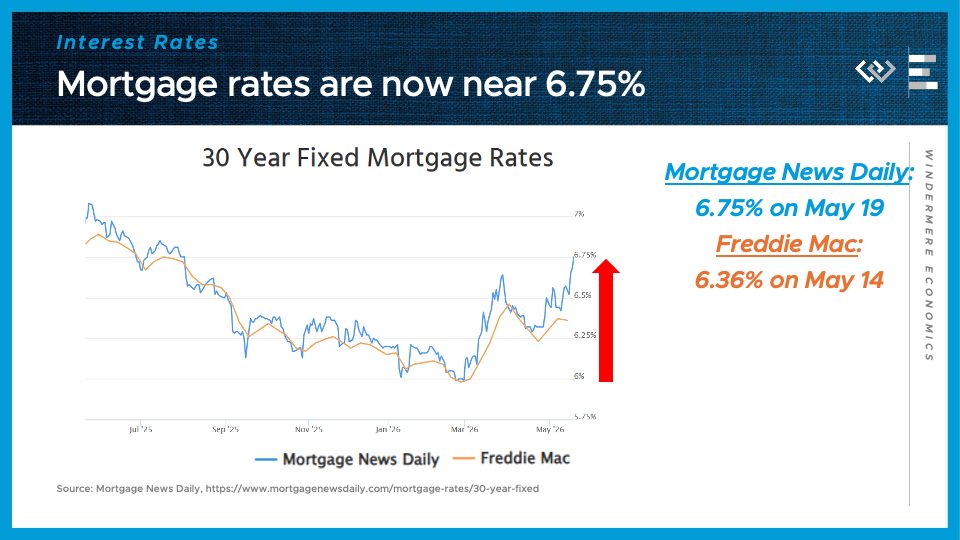

And we know higher Treasury yields usually mean: higher mortgage rates. After some volatility and false starts downward last month, mortgage rates have surged up even further in mid-May, approaching 6 and three quarters percent according to Mortgage News Daily. That will help to dampen homebuyer demand in the spring buying season, which is in full swing.

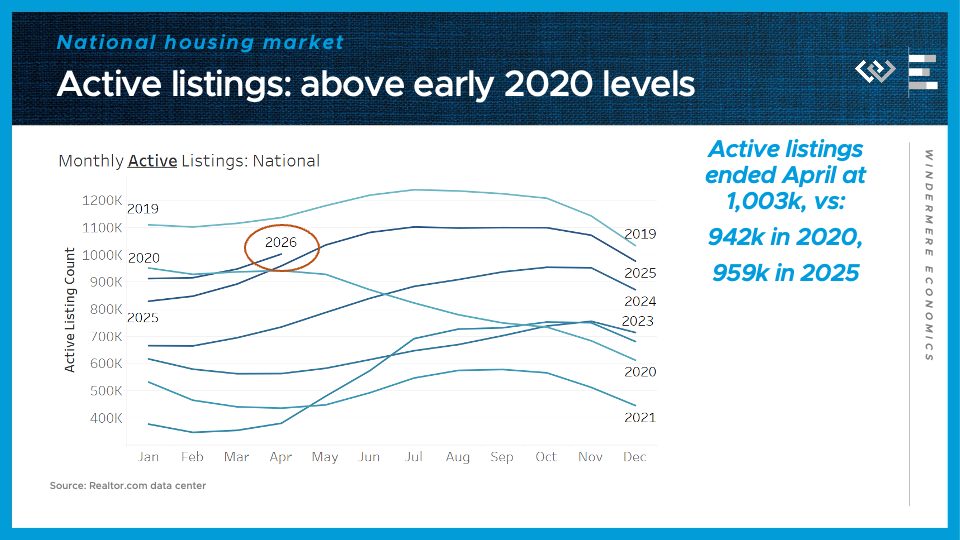

Speaking of the housing market, we saw just over a million active listings at the end of April—about 60 thousand more than this time in 2020, and 40 thousand more than this time last year.

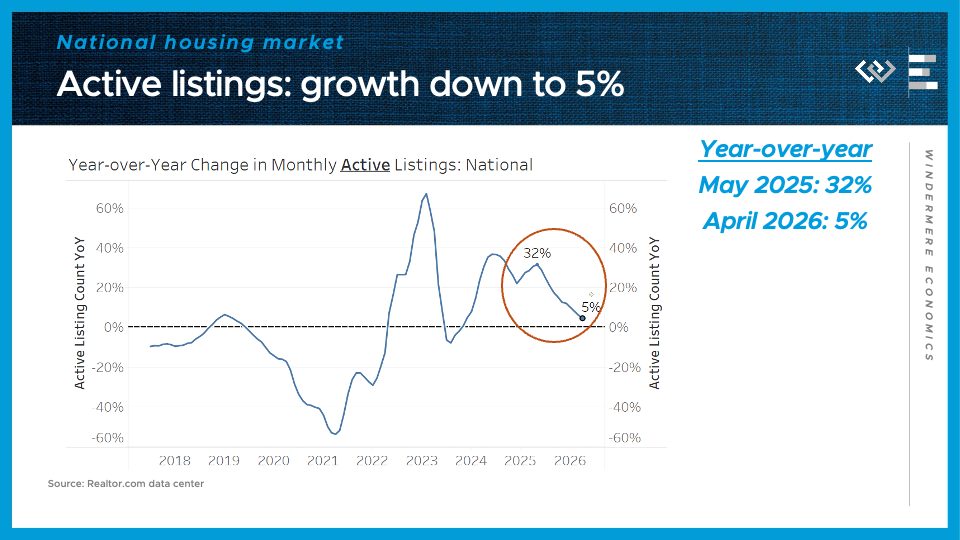

That year-over-year growth rate of just under 5% helps continue a trend of decelerating inventory growth, as the market looks more and more balanced this year – with neither a glut of home listings building up nor a frenzied shortage condition, at least on average across the country. Pending home sales were also basically flat from this time last year, but if mortgage rates stay above 6.5%, I expect the months of May and June will look weaker than the same time last year. Once again, that means the forecast depends on whether durable peace can take hold, and whether oil begins to flow again, in the Middle East.

For four decades, the Windermere Cup has brought together world-class rowing, Seattle tradition, and community celebration on the shores of the Montlake Cut. This year’s 40th annual Windermere Cup weekend carried that legacy forward in memorable fashion, with exciting international competition, a sold-out Party on the Cut, and the return of the Media Cup—all leading into one of Seattle’s most beloved spring traditions.

What began in 1987 as a partnership between Windermere Real Estate, the University of Washington, and the Seattle Yacht Club has grown into one of the premier rowing events in the world and a defining part of Opening Day of Boating in Seattle. The original vision was to showcase the excellence of UW Rowing and the Montlake Cut by bringing the world’s best competition to Seattle. That first year featured crews from the Soviet Union in one of the few athletic competitions held between the Soviet Union and the United States in more than two decades.

40 years later, the Windermere Cup continues to honor that vision, bringing together elite athletes, passionate fans, longtime community partners, and generations of Seattle tradition.

Media Cup Returns for Its 13th Year

Windermere Cup week officially kicked off on Tuesday, April 28th, with the 13th annual Media Cup, where four of Seattle’s television stations took to the water to compete for bragging rights and to support nonprofits of their choice that are making a difference in our community.

Continuing another meaningful Media Cup tradition, the Windermere Foundation also presented a $5,000 donation to the George Pocock Rowing Foundation, an organization dedicated to helping young people access and experience the life-changing sport of rowing.

A Sold-Out Night at Party on the Cut

On Friday evening, the community gathered once again for the 8th annual Party on the Cut. The sold-out event has become a staple of Windermere Cup weekend, bringing together rowing fans, community members, and supporters of the Windermere Foundation for an unforgettable night on the shores of the Cut.

Guests enjoyed live music from Nite Wave, Seattle’s premier ‘80s new wave tribute band, along with Hysteria, the ultimate Def Leppard tribute band, along with local food trucks, drinks, and the return of the Twilight Sprints, where the women’s crews from Great Britain Rowing, Rowing Canada Avion, and the University of Washington gave spectators a preview of Saturday’s competition.

From the music to the food trucks, volunteers, vendors, and community partners who helped bring the evening to life, Party on the Cut once again delivered a memorable kickoff to Windemere Cup weekend. Support from partners like Gentle Giants Moving Company, the official moving partner of Windermere Cup, and Sentry Computing, the official bar partner for Party on the Cut, helped make the celebration possible.

As always, proceeds from Party on the Cut benefited the Windermere Foundation and its ongoing mission to support low-income and homeless families throughout the Western U.S.

Celebrating 40 Years of Partnership

Saturday morning brought thousands of spectators back to the Montlake Cut as Seattle’s Opening Day of Boating Season once again paired with one of the city’s most iconic sporting traditions.

The Windermere Cup would not exist without the longstanding partnership between Windermere, the University of Washington, and the Seattle Yacht Club. For more than 100 years, the Seattle Yacht Club has organized Seattle’s Opening Day celebration, while UW Rowing has built one of the most respected rowing programs in the world. Together, those partnerships have transformed the Montlake Cut into an internationally recognized racing venue and one of the most unique settings in the sport.

Adding to the celebration was the appearance of the historic Malibu boat, which served as the lead boat in the Opening Day Boat Parade as it celebrated its 100th anniversary. The Malibu has long been connected to both Seattle Yacht Club history and the legacy of Windermere founder John Jacobi, making its presence this year an especially meaningful tribute to the people, partnerships, and traditions that have shaped Windermere Cup over the past 40 years.

The women’s Windermere Cup race featured a strong international field, with the GB Rowing Team women’s crew taking first place, followed by UW Women’s Purple in second, Rowing Canada Aviron in third, and UW Women’s Gold in fourth.

The men’s race delivered one of the most exciting finishes in recent Windermere Cup history. Racing against the current Olympic gold medal-winning GB Rowing Team men’s crew, the University of Washington Rowing men secured a dramatic photo-finish victory in front of the home crowd. Northeastern rounded out the field in third place.

Official race results and final standings are available here.

Forty years after its founding, the Windermere Cup continues to represent far more than a rowing race. It remains a celebration of Seattle’s community spirit, international competition, waterfront traditions, and the partnerships that have made the event possible for generations.

Here’s to 40 years on the Cut, and to many more ahead!

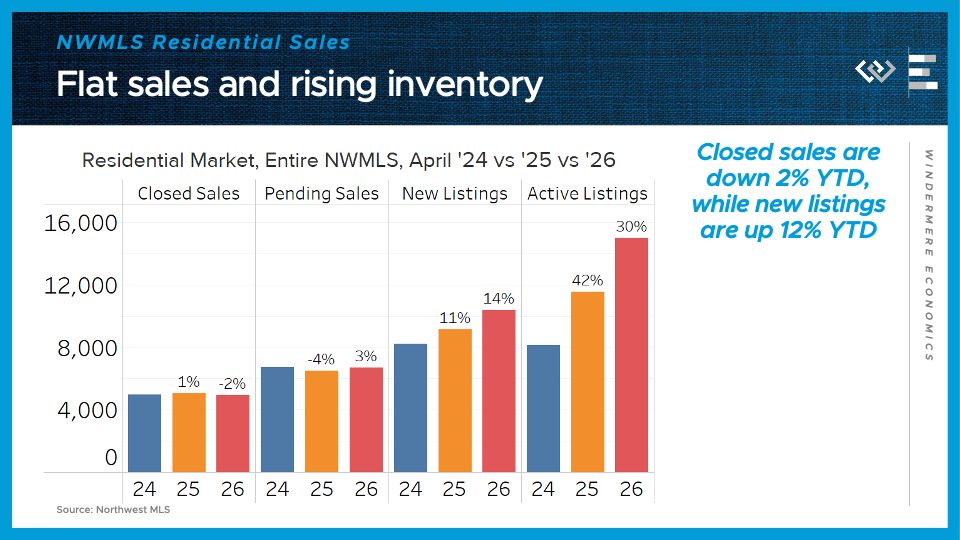

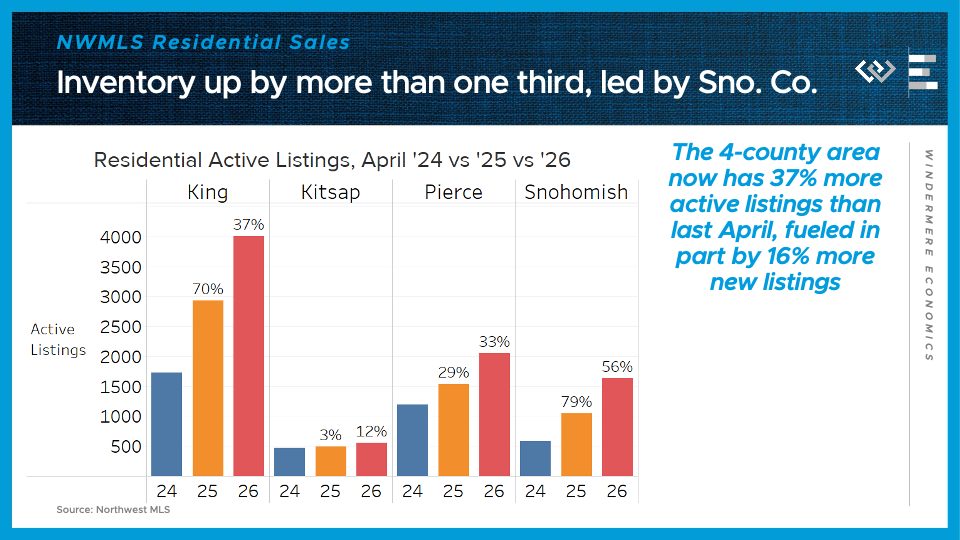

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the April 2026 data from the Northwest MLS.

We are now in the heart of the spring selling season, and it is shaping up to be a little quieter than last year’s spring.

Across the Northwest MLS, there were 2% fewer closed sales in April 2026 than in April of last year. Pending home sales, by contrast, climbed by 3% from last year.

On the supply side, the flow of new listings was up an impressive 14% from last April’s pace, or 12% cumulatively, year-to-date. Finally, the month ended with just over 15,000 active listings around the MLS, or 30% more than last April. That continues the local trend of rising inventory, reflecting more sellers than buyers coming to the market this year.

The median sale price ticked down from last April, by just $5,000, or less than 1%.

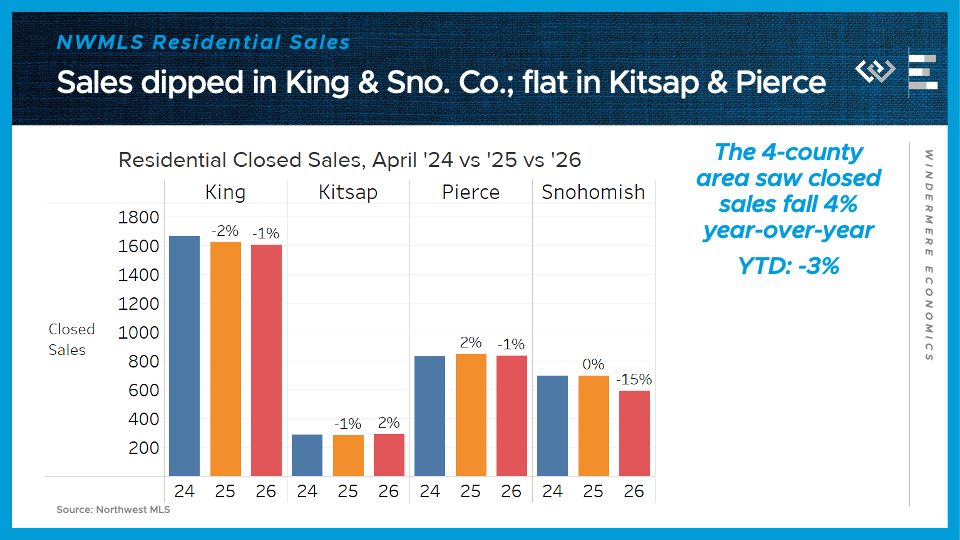

Now for a closer look at the four counties encompassing the greater Seattle area.

Closed sales declined by 4%, or 130 homes, from last April around the region. Snohomish County alone saw closed sales drop by 104 homes, or 15%, while King, Pierce and Kitsap Counties saw sales within a couple percentage points of last April’s totals.

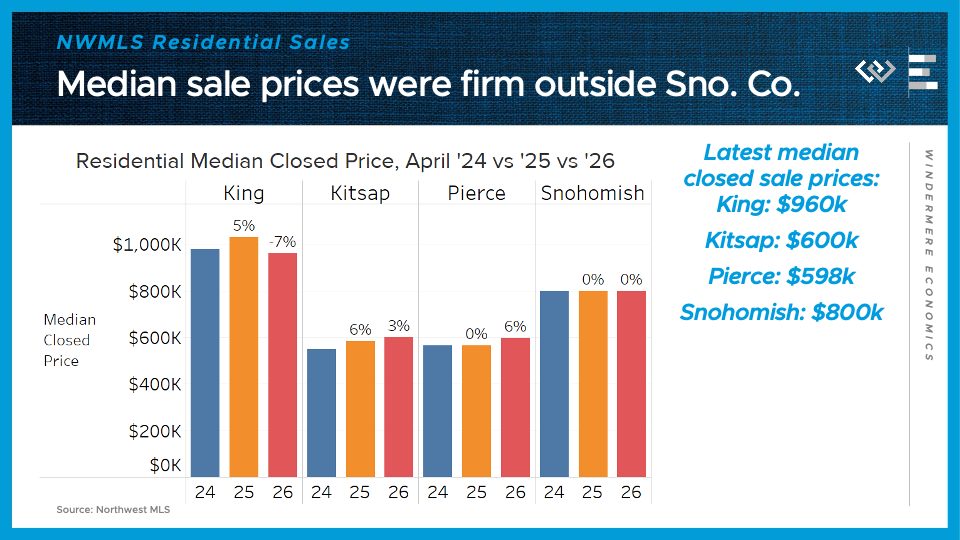

Median sale prices, though, dipped the most here in King County, where they fell 7% short of last April’s $1,030,000 mark. Prices were flat in Snohomish, near $800,000; and up modestly to about $600,000 in both Pierce and Kitsap Counties.

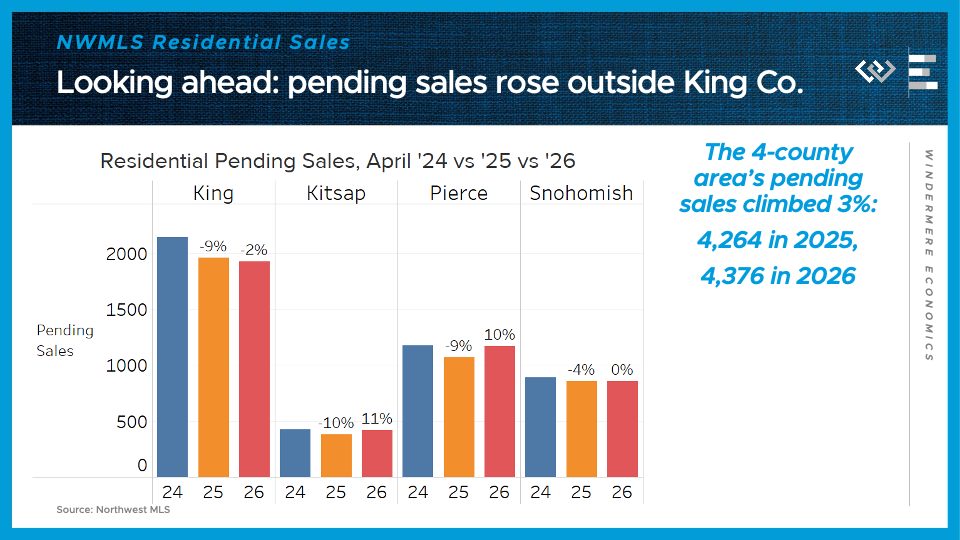

Looking ahead, pending sales actually climbed 3% across the region in April, led by strong growth in Pierce and Kitsap Counties, while only King County saw a modest dip in pending home sales.

On the supply side, the 4-county greater Seattle area ended the month with 37% more active listings than last April, led by 56% growth in Snohomish County and 37% growth in King County.

Spring remains the best time of year to sell a house, but this spring also looks like an unusually good time to buy a house, thanks to unusually many listings, which are taking a little longer to sell on average, and in some areas selling for a little less than similar houses last year. Well-presented, appropriately-priced homes are still seeing a lot of competition, but plenty of other homes are lingering a little longer on the market, selling at or below list price. It seems that the negative effects of the war in Iran are discouraging some buyers, who may be taking a “wait-and-see” approach, which leaves the market a little more balanced for the many buyers who are still forging ahead this spring. If economic and geopolitical news improves, there’s still plenty of time to see a busy second half of the spring selling season.

Many of us spend a significant amount of time at home, and as spring arrives with longer days and fresh air, it’s often the moment when small things start to stand out. A little dust here, some clutter there—it all adds up. Spring cleaning is an opportunity to reset your space in a way that supports both your home and your overall well-being.

Whether you’re preparing to list your home, settling into a new one, or simply refreshing your space, a thoughtful approach to cleaning can make a noticeable difference. Here are some tips to guide you through your spring cleaning this year.

First clean, then disinfect

General cleaning removes dirt and buildup, while disinfecting targets bacteria and germs. Both play an important role in maintaining a healthy home, especially in high-use areas.

Focus on high-touch surfaces like doorknobs, countertops, light switches, and faucets. Devices like phones, laptops, and tablets should also be included, as they’re among the most frequently handled items in your home.

When possible, opt for cleaners with plant or mineral-based ingredients. Many homeowners today are choosing low-toxicity options that are effective without introducing harsh chemicals into their living space.

Work top to bottom

Working from ceiling to floor helps prevent re-cleaning the same areas and keeps dust moving in one direction.

Ceiling and upper surfaces

Spring is peak allergy season, so dusting is especially important. Pay attention to ceiling fans, vents, light fixtures, and corners where cobwebs collect. Curtains, blinds, and even the tops of cabinets often go overlooked but can hold a surprising amount of dust.

Walls and windows

A quick wipe-down of walls—especially in kitchens and high-traffic areas—can instantly freshen a space. Clean windows inside and out to maximize natural light. It’s one of the simplest ways to make your home feel brighter and more open.

Floors

Different flooring materials require different care. Vacuum or sweep first, then follow with the appropriate method, whether that’s mopping sealed wood floors or dry mopping laminate and vinyl. Taking the extra step to use the right technique will help preserve your flooring over time.

Don’t forget your appliances

Appliances are some of the hardest-working features in your home, but they’re often overlooked during routine cleaning.

Refrigerator and freezer

Toss expired items, wipe down shelves, and vacuum coils if accessible

Dishwasher

Run an empty cycle with a cleaning solution to remove buildup and odors

Oven and microwave

Deep clean interiors to eliminate grease and food residue

Washer and dryer

Clean the washing machine drum and thoroughly clear the dryer vent and lint trap.

Keeping appliances clean not only improves performance but can also extend their lifespan.

Declutter with intention

Decluttering can feel overwhelming but breaking it into smaller steps makes it more manageable. Approach your home room by room and set realistic goals for each space. As you go, sort items into clear categories like keep, donate, and store, which helps streamline decision-making and keeps things moving. Group donation items together so they can be dropped off in one trip, rather than lingering in your space. For anything you plan to store, consider accessibility: items you use more frequently, like tools or seasonal essentials, should be easy to reach.

If you have pets, spring cleaning comes with a few extra considerations, but the effort goes a long way in keeping both your home and your pet happy and healthy.

Start by washing pet bedding, blankets, and soft toys to remove built-up hair and odors. Take time to vacuum furniture and hard-to-reach areas where pet hair tends to collect, and wipe down baseboards, doors, and walls at pet height, where marks can easily go unnoticed. It’s also a good opportunity to deep clean litter boxes, crates, and feeding areas to keep everything as fresh and sanitary as possible.

Regular cleaning like this helps reduce allergens, odors, and everyday wear, keeping your home feeling clean and comfortable for both you and your guests.

Go for multipurpose solutions

Minimalism and multifunctional design continue to shape how people live in their homes, and even small adjustments can make your space feel more efficient and easier to maintain. Look for ways to incorporate furniture and layouts that serve more than one purpose, whether it’s a storage bed or ottoman that helps reduce clutter, a flexible dining area that can double as a workspace, or built-in shelving that maximizes both form and function.

A well-organized home is easier to clean, easier to live in, and often more appealing to future buyers.

Make it a habit, not a one-time task

Spring cleaning doesn’t have to happen all at once. Spacing tasks over a few days or even a few weeks can make the process more manageable and sustainable. And once you’ve done the deep clean, maintaining it becomes much easier.

Whether you’re refreshing for yourself or preparing for your next move, small improvements make a lasting impact. If you’re thinking about buying or selling this season, connect with a Windermere agent to make the most of your home.

In the Pacific Northwest, architecture is as much about the environment as it is about the home itself. With long stretches of gray skies, evergreen landscapes, and a strong connection to the outdoors, homes in the region are designed to feel both grounded and expansive.

Northwest Contemporary architecture, sometimes called Pacific Northwest style or Northwest Modern, reflects that balance. It’s a design approach shaped by climate, landscape, and a lifestyle that values comfort, simplicity, and a seamless connection to nature. Influenced heavily by the region’s natural surroundings, this style prioritizes livability, light, and a design that feels in tune with its environment.

Designed for the Pacific Northwest way of living

The Pacific Northwest is known for its natural beauty, but much of the area is also known for its long, rainy seasons. Because of this, homes are designed to enhance the experience of being indoors without losing that connection to the outside, while also being well-suited to handle the region’s climate, including frequent rain and moisture.

Northwest Contemporary homes often feel open and airy, with open floor plans that let light flow freely throughout the space. Large windows are a defining feature, bringing in natural light even on overcast days and framing views of trees, water, and surrounding landscapes. Rather than separating indoors from outdoors, these homes are designed to blur the line between the two. This approach creates spaces that feel calm, comfortable, and connected to their surroundings year-round.

A focus on natural materials and simplicity

At the core of Northwest Contemporary design is a commitment to natural materials and understated finishes. Wood, stone, and glass are used not just for aesthetics, but to reflect the textures and tones of the surrounding environment.

You’ll often see an emphasis on regionally sourced materials alongside wood beams, stone fireplaces, and clean-lined cabinetry that highlight craftsmanship without feeling overly ornate. The overall look leans minimalist, but not cold. Instead, it feels warm, intentional, and grounded.

There is also a growing focus on sustainability within this style, with many homes incorporating energy-efficient design, durable materials, and thoughtful siting to work with the landscape rather than against it.

This simplicity allows the home itself to complement the landscape rather than compete with it, resulting in a timeless aesthetic that doesn’t rely on trends.

Influences that shape the style

Northwest Contemporary architecture is influenced by a mix of design movements, most notably modern architecture and the international design principles popularized by architects like Frank Lloyd Wright. His emphasis on harmony between structure and environment is clearly reflected in homes throughout the region.

There are also strong ties to Japanese design, particularly in the use of clean lines, natural materials, and a focus on balance and tranquility. In many homes, you’ll also find elements inspired by Indigenous art and culture, adding depth and regional identity to the overall design. Together, these influences create a style that feels both modern and deeply rooted in place.

A style that continues to evolve

Like the region itself, Northwest Contemporary architecture is not defined by strict rules. It continues to evolve with new materials, technologies, and interpretations of modern living.

Some homes lean more modern, with sharper lines and more minimalist finishes, while others incorporate elements of related styles, such as Pacific Lodge or Japanese Modern. No matter the variation, the foundation remains the same: a connection to nature, thoughtful use of materials, and spaces designed for how people truly live.

If you’re drawn to Northwest Contemporary design or are considering buying or selling a home, a Windermere agent can help you better understand the architectural styles that define your local market.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

")

{kind=link}