To successfully sell your home, you need to attract buyers. This is why open houses are an integral part of the selling process: they allow buyers to experience the property for themselves and envision what life will look like in their new home. To prepare for an open house, you’ll need to work closely with your agent. They can advise you on what buyers in your area are looking for to increase your chances of selling your home.

How to Prepare for an Open House

The earlier you can begin prepping your home for an open house, the better, since getting it in prime showing condition will take time. Start by decluttering and organizing room by room. To truly get your home sparkling clean, you can’t miss those hard-to-reach areas like the baseboards, under your furniture, and your appliances.

To best position your home to sell, consider hiring a professional stager. A well-staged home helps it appeal to the widest possible array of potential buyers, not only for in-person showings, but in online photos as well. Professional staging is equal parts science and art. Stagers are experts in depersonalizing a home while maintaining its stylistic qualities to give buyers the opportunity to imagine the space for their own use. It isn’t just about psychology, though. Staging is a high-ROI expenditure that can add real value to your home.

It may feel counterintuitive, but your absence can be your greatest asset in making your open houses successful. Buyers will often feel uneasy in the presence of the seller as they tour, which will limit their ability to envision their own lives in the home and get excited about the prospect of ownership. Accordingly, you may need to arrange for temporary accommodations during the times your home is being shown. It’s helpful to solidify these plans several weeks in advance to avoid an eleventh-hour scramble.

Put buyers in a feel-good mood with Windermere’s “Open House” playlist on Spotify. Click the image above to listen.

Working with Your Agent

Your agent will be your greatest asset in preparing for open houses. They are experts in understanding how to effectively market your home and how the local market conditions will impact their marketing plan. Once you know it’s time to sell, they’ll analyze data to accurately price the property and keep it competitive in the current market. They’ll also work with you to schedule open houses at the times when buyers are maximally available and actively searching for listings.

Your agent will also help you to stay safe while selling your home. The reality of open houses is that you’re opening your doors to an influx of unfamiliar faces, and it’s worth it to take a few safety precautions beforehand. Perform a thorough walkthrough of your home with your agent to make sure all valuable belongings, medications, family heirlooms, and other important items have been properly secured and/or removed. Once you’ve given your home a clean sweep, discuss your process for screening potential buyers.

For more resources on preparing to sell your home, our Home Selling Guide has everything you need: selling tips, moving checklists, our Home Worth Calculator, and info on how an agent can help.

Your home’s façade and front yard play a role in its curb appeal, but the backyard is for you and your household to enjoy. Spending time making improvements to your backyard will help to maximize your enjoyment of your property and can increase its value. These backyard design projects will help to beautify your yard while creating opportunities for new ways of spending time in it.

Consider butting up your built-in seating to your deck’s banister or railing and wrapping it around the perimeter. This will help make your deck more welcoming while saving space that would be taken up by chairs. For an even more efficient space-saving strategy, keep the space underneath your built-in seating open or install a drawer system to store your backyard and/or outdoor kitchen items and tools. If a deck rebuild isn’t in the cards, try simpler improvement projects like restraining it or adding outdoor lighting.

2. Build a Tool Shed

Every backyard requires maintenance, and you typically need tools to keep it in tip-top shape. A useful DIY project for your backyard is to build a tool shed to house your garden tools and landscaping equipment. This will give them a safe, dry storage space, which helps to extend their useful life and avoids having to make unnecessary replacements. When in doubt, add extra shelving space, as you very well may build out your tool collection over time. Once your shed is complete and all your tools are in their right place, install a secure locking system to protect your equipment.

Image Source: Getty Images – Image Credit: vgajic

3. Create an Outdoor Cooking Area

Outfitting your backyard for a robust outdoor kitchen with all the bells and whistles can be expensive. Fortunately, you can create an outdoor cooking area without having to break the bank. Depending on your local climate, it may be wise to cover this area with some sort of roof structure. If so, be sure to leave ample room between your cooking equipment and the height of the roof to allow flames and fumes to safely escape.

Different types of barbecues can satisfy your outdoor kitchen needs, depending on how much room you have to work with. Charcoal grills are ideal for smaller spaces, while built-in barbecues can provide a more comprehensive grilling setup if you have the allotted square footage.

4. Give Your Flower Beds a Makeover

Flower beds have quite an impact on the overall aesthetic of your backyard. If your flower beds are overgrown, start by pulling out the weeds. Use a garden trowel; this will help to dig up the roots and decreases the chance of recurring weeds. Remove all the weeds and debris, then rake the soil to prepare it for composting. While you rake, keep an eye out for rocks and gravel and remove them from the flower bed.

Now you’re ready to add a new layer of compost. This does wonders for the health of the soil and encourages new plant growth. Sprinkle in two to three inches of compost and work it into the soil with a shovel. You can also experiment with adding other nutrient-rich ingredients or plant materials that are conducive to soil in your climate, such as peat or manure.

5. Build Your Ultimate Patio

For many homeowners, building a patio exists at the crossroads between a DIY project and one that requires a professional’s expertise. Whichever route you choose, executing a patio installation can take your backyard to the next level. Choosing your patio material is the first step. Concrete, flagstone, brick, terra-cotta, and pea gravel are all common patio materials that have their respective advantages and disadvantages. If having a patio that’s built to last is your top priority, then brick, flagstone, or concrete may be the way to go. These materials also complement a variety of house styles, as well. If you’re looking to create a more relaxed environment in your backyard, then pea gravel or clay may be more your style. These materials recall aspects of the beach and seaside living.

For more information on how you can take your yard to the next level, read our blog post on seven ideas for creating a beautiful yard:

Contingencies help to spell out the specifics of a real estate transaction by dictating what must happen so the contract becomes legally binding. If certain conditions aren’t met, the applicable contingency gives the buyer and the seller the right to back out of the contract per their agreed-upon terms. When selling your home, a buyer may make their offer with contingencies attached. Here are some common contingencies you might see in a buyer’s offer and what they mean for you.

Common Real Estate Contingencies

Home Inspection Contingency

A home inspection contingency allows the buyer to have the home professionally inspected within a certain window of time. If the buyer finds outstanding repairs that need to be made, they can negotiate them into their offer. If the seller chooses not to make the repairs outlined in the buyer’s home inspection report, the buyer can cancel the contract.

As a seller, it’s important to be transparent in listing any issues with the home. This is why many sellers find a pre-listing inspection to be beneficial: it provides transparency about the home’s condition ahead of time and can help to streamline the buying process, which can be especially helpful when selling in competitive markets.

Financing Contingency

Also known as a “mortgage contingency,” a financing contingency gives the buyer a specified period of time to secure adequate financing to purchase the home. Even if a buyer is pre-approved for their mortgage, they may not be able to obtain the right loan for the home. If they are unable to finance the purchase, the buyer can back out of the contract and recover their earnest money, and the seller can re-list the home.

The seller won’t be on the hook if the buyer fails to cancel the contract. Even if the buyer is not able to secure financing by the agreed-upon date, they are still responsible for purchasing the home if they do not terminate the contract.

Image Source: Getty Images – Image Credit: fizkes

Appraisal Contingency

An appraisal contingency states that the home must appraise for, at minimum, the sales price. It protects the buyer in that it allows them to walk away from the deal if the property’s appraised value is lower than the sales price, and typically guarantees that their earnest money will be returned. This can be an issue in certain markets where demand is driving prices up to numbers that appraisals don’t reflect. Depending on the agreement you make with the buyer, you may be able to lower the price of your home to the appraised amount and sell it at that price. When selling your home, remember that there is a difference between appraised value and market value. An appraiser’s value of a property is based on several factors using comparative market analyses, whereas market value is what buyers are willing to pay for a home.

Home Sale Contingency

If a contract includes a home sale contingency, it means that the buyer is tying their purchase of a home to the sale of their existing one. Though it is common for homeowners to buy and sell a house at the same time, attaching a home sale contingency to an offer does create some added variability in a real estate transaction that sellers should be aware of before accepting such an offer. This contingency allows buyers to sell their current home and use the proceeds to finance the purchase of their new one. Although you will have the right to cancel the contract if your buyer’s home is not sold within a specified time, you’re still waiting on them for the deal to go through, which means you could potentially miss out on other offers while you wait.

Title Contingency

Before the sale of a home goes final, a search will be performed to ensure that any liens or judgements made against the property have been resolved. A title contingency allows a buyer to raise any issues they may have with the title status of the property and stipulates that the seller must clear these issues up before the transfer of title can be complete. If an unpaid lien or unpaid taxes turn up in the home’s title search, this contingency also allows the buyer to back out of the deal and look for another home. A majority of sellers will pull a pre-title report to provide transparency for a smooth transaction.

These are just some of the contingencies you may encounter in a buyer’s offer. Work closely with your agent to understand the terms of these contingencies and how they impact the sale of your home as you go about finding the right buyer. For more information on the process of selling your home, connect with an experienced, local Windermere agent today.

The right lighting can give your home the quality and mood you’re looking to achieve. Knowing about the different temperatures of light, lighting types, and how to blend lighting elements will help you narrow down your choices and find the best fixtures for your home.

How to Find the Right Lighting for Your Home

Before taking a trip to the hardware or lighting store, it’s worth your time to understand the different types of lighting and how they complement each other to fill the large surface areas of your home while spotlighting the nooks and crannies. Ambient lighting, accent lighting, and task lighting are the three basic lighting types that cover the spectrum of illuminating a home.

Ambient Lighting

Ambient light is what fills a room. Also known as “general light,” this is the primary light source for the spaces in your home. When selecting your ambient lights, know that your choice in color will play a significant role in the atmosphere of that room, since this type of lighting is so widely distributed.

Accent Lighting

Accent lighting has a smaller footprint than ambient lighting. It is meant to direct focus and attention to a specific spot. By pulling the eye toward this spot lit area, it allows you to highlight décor and design pieces, such as picture frames and artwork, houseplants, or small sculptures.

Task Lighting

It’s all in the name when it comes to task lighting. This form of lighting exists to help you perform tasks. Whether it’s cooking, working on arts and crafts, tinkering away at a desk, or tending to your indoor garden, having task lighting in place will ensure that you’re able to see while you work. Feel free to experiment with closeup light sources when installing task lighting to provide the maximum attention to detail while you work. Task lighting fixtures can be as simple as a floor lamp or desk lamp.

Image Source: Getty Images – Image Credit: TG23

Different Temperatures of Light

There are three basic light temperatures: warm, cool, and neutral. Warm light creates a cozy, comfortable feeling, and functions best in rooms where you plan to kick back and relax, such as the bedroom or the living room. Cold light encourages attention to detail, and therefore works well in places like the kitchen and bathroom. Neutral light sits between warm and cold light but functions like cold light in that it can help you focus on the task at hand in the rooms where it’s used. Places like the garage, home office, or bonus/utility rooms are all fitting homes for neutral light.

After you’ve researched the different types of lighting and decided which temperatures fit best throughout your home, it’s time to pick your fixtures.

Chandeliers

Chandeliers have been around for centuries and they are still popular today. Due to their formal nature, they can set the stage for dining rooms and foyers alike with traditional style. Chandeliers typically give off lots of light, making them perfect for filling larger spaces.

Surface Lights

Surface lights sit flush against the wall where they are installed. These lights are typically used in smaller areas such as hallways.

Pendant Lights

Pendant lights are commonly found in the kitchen or the dining room. Suspended from the ceiling, pendant lights come in a variety of styles, but often appear as a linear series of lights that run the length of a table or slab underneath them.

Recessed Lights

Recessed lights sits inside the wall and provide a level distribution of illumination. These lights are a popular choice for vaulted ceilings, where you’ll usually see them spaced evenly apart to fill the room with ambient light.

For more information and resources on putting together the home you envision, read our blog post on how to upgrade your dining room:

This video is the latest in our Monday with Matthew series with Windermere Chief Economist Matthew Gardner. Each month, he analyzes the most up-to-date U.S. housing data to keep you well-informed about what’s going on in the real estate market.

The Impact of Rising Mortgage Rates

Hello there. I’m Windermere Real Estate’s Chief Economist Matthew Gardner. Welcome to the latest episode of Monday with Matthew.

Over the past several weeks I’ve gotten a lot of messages from you wanting me to discuss the spike in mortgage rates that followed comments by the Federal Reserve, but also asking me if there will be any impacts to the housing market following Russia’s invasion of the Ukraine. This is clearly a hot topic right now, so today we are going to take a look at how these events have impacted mortgage rates, but also look at how this may have changed my mortgage rate outlook for 2022. So, let’s get to it.

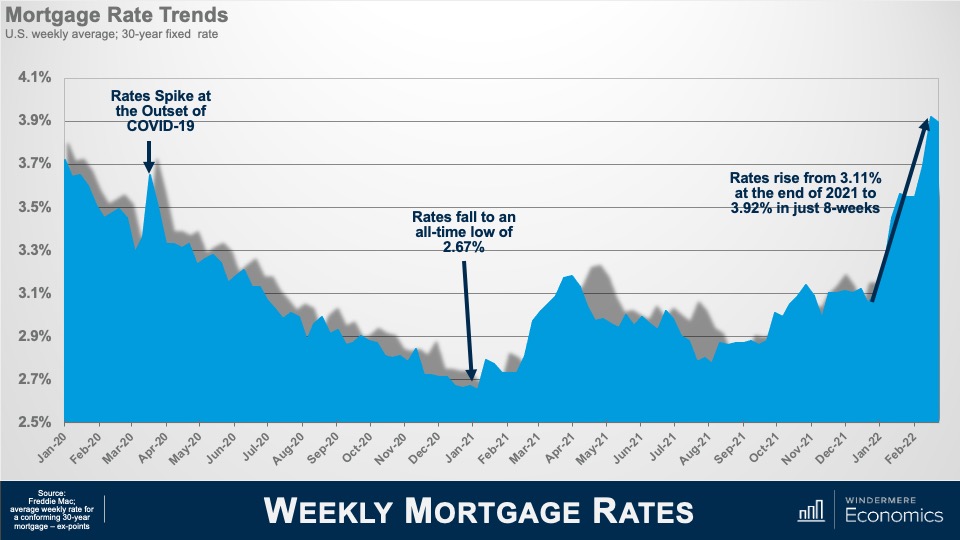

Weekly Mortgage Rates

Here is a chart that shows how rates have moved over the past two years or so using Freddie Mac’s average weekly rate for a conforming 30-year mortgage. You’ll see that rates were falling in early 2020, but when COVID-19 was announced as a pandemic they spiked, but almost immediately the Fed announced their support for the economy by implementing a broad array of actions to keep credit flowing and limit the economic damage that the pandemic would likely create. And part of that support included large purchases of U.S. government and mortgage-backed securities. With the Fed as a major buyer of mortgage securities, rates dropped ending 2020 at a level never seen in the more than 50 years that the 30-year mortgage has been with us.

In early 2021, rates started to rise again as the country became more confident that the pandemic was coming under control, but all that changed with the rise the Delta variant of COVID-19 which pushed rates lower through mid-summer. As we again started to believe that COVID was under control and a booster shot became available, you’ll see rates resumed their upward trend in August.

What has everyone worried today is this spike that really took off at the end of last year. A jump of almost a full percentage point in just eight short weeks understandably has a lot of agents, buyers, and sellers, concerned about what impacts this might have on what has been a remarkably buoyant housing market. Now, rates rising so quickly was unusual, but not unprecedented. If you really wanted to be scared, I’d regale you with stories from 1980 when mortgage rates jumped by over 3.5% in less than eight weeks.

Anyway, before we really dig into this topic, some of you may be thinking to yourselves that my numbers have to be wrong because they differ from the rates you have been looking at. This is due to the fact that the Freddie Mac survey methodology is different from other rate surveys but, even though their rates may not match the ones you’ve been seeing from other data providers, the trend is still consistent.

So, let’s chat for a bit about what caused the spike in rates. You know, it’s always good to have a villain in any story and the primary but certainly not sole culprit responsible for the jump in rates is—you guessed it—the Federal Reserve.

As I mentioned earlier, the Fed was the biggest buyer of pools of home loans (otherwise known as mortgage-backed securities) as we moved through the pandemic, but last December they announced an end to what had been an era of easy money by winding down these purchases in order to lay the groundwork for shrinking their 2.7 trillion—yes I said “trillion”—dollar stockpile of MBS paper they had built up. This decision to move from “quantitative easing” to “quantitative tightening” so rapidly had an almost immediate impact on mortgage rates simply because the market was going to lose its biggest buyer of mortgage bonds.

Immediately on the heels of their announcement, bond sellers raised the interest rate on their bond offerings to try and find buyers other than the Fed, so lenders raised the rates on mortgages housed within these bond offerings. Finally, mortgage brokers moved quickly to raise the rates that they were quoting to the public. The result of all this was that rates leapt. Although we know that the primary party responsible for rates rising was the Fed, there were other players too, and here I am talking about inflation—and as you are no doubt aware—it too started to spike at the beginning of this year and now stands at a level not seen since 1982. And if you’re wondering why inflation is important. Well, high inflation is a disincentive to bond buyers because if the rate of return, or interest on mortgage bonds, is lower than inflation, investors lose interest pretty quickly.

So, we can blame the Fed, we can blame inflation, but what about Russia? Well, their invasion of the Ukraine on February 24 has certainly influenced mortgage rates, but maybe not in the way you might expect. In general, when there’s any sort of global or national geopolitical event, investors tend to gravitate to safety, and this invariably means a shift out of equities and into bonds.

So you would be correct is thinking that at face value Russia was actually responsible for the tiny drop in rates we saw following the invasion, and also the more significant drop we saw last week when the market saw the biggest two-day drop in rates in over a decade. But before you start to think that rates are headed back to where they were a year ago, I’ve got some bad news for you. That is almost guaranteed not to happen.

Given what we know today, the terrible conflict in Eastern Europe is highly unlikely to push rates back down to where they were at the start of this year, but they will—at least for now—act as a headwind to rates continuing to head higher at the pace we have seen over recent weeks. That will continue until the conflict is hopefully peaceably concluded. And although the Ukraine situation is unlikely to have any significant impact up or down on mortgage rates, there are some indirect impacts which could negatively hit the housing market. Now I’m talking about oil.

Russia is the third largest energy producer in the world and an already tight global oil supply could get even tighter following newly announced financial sanctions on Russia. A barrel of oil has jumped by almost $20 to $109 a barrel since the start of the occupation and, if the occupation is sustained, and Russia is faced with even greater sanctions, I wouldn’t be surprised to see the price of gas rise by between 20 and 40 cents a gallon. And it’s this, in concert with already high inflation, which will directly hit consumers wallets and this itself could certainly impact mortgage borrowing. So we can blame the Fed, we can blame inflation and we can blame Russia for the jump in rates, but are the rates you are seeing today really something to lose sleep over? I actually don’t think so. At least not yet.

Even with mortgage rates where they are today, I look at them and think to myself that they are still exceptionally low by historic standards and that there really is no need for panic. But let me explain my thinking to you. To do this, we will take a look at the impact of rising mortgage rates, not as it relates to buyers’ ability to finance a home purchase, but on how it impacts their monthly payments.

Hypothetical Home Purchase

For this example, we’ll use the peak sale price for a single-family home in America, which was just over $370,000 back in June of last year. And to finance this purchase, a buyer was lucky enough to lock in the lowest mortgage rate for that month at 2.96%. Assuming that they put 20% down, and are paying the U.S. average homeowners insurance premium and average property taxes a buyer closing on that home in June of last year would have a monthly payment of $1,682.

Now, what if a buyer had bought the exact same house but in February of this year? Well, the average rate for the third week of February was 4.06%—a big jump from last June—and higher mortgage rates would have increased their payment to $1,864. What does this all mean? Well, a jump of over a full percentage point means that the monthly payment is more, but only a relatively modest $182. So, even though rates have risen by almost a full percentage point, the increase in payments was, I think you’ll agree, relatively nominal.

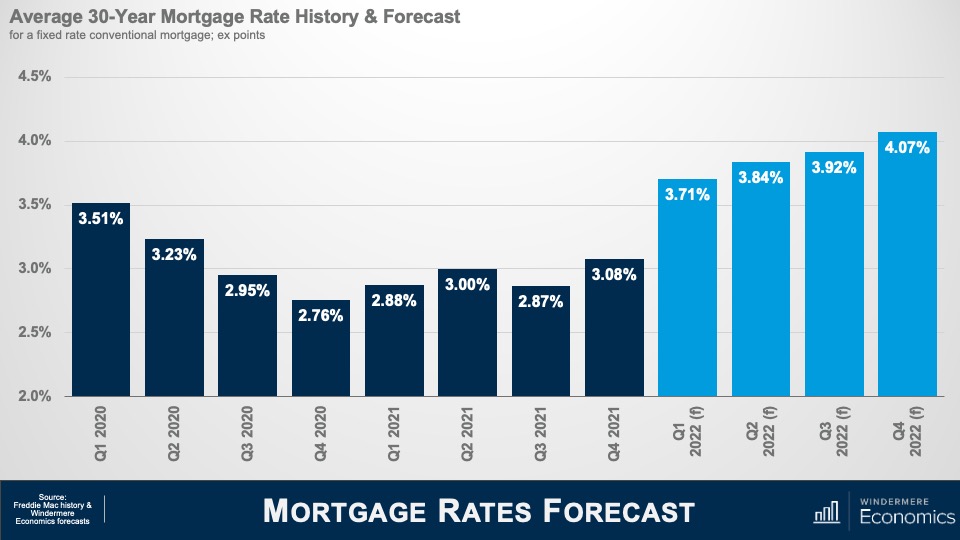

But what if rates had risen to 5%? Well, that would be a very different picture with payments increasing by a far more significant $348. Of course, this is a very simplistic way of looking at it as I have not included any other debt payments that a buyer may have, but I hope that it does demonstrate that, even though mortgage rates are certainly significantly higher than they were last summer, because we started from such a low basis, monthly payments have seen a relatively modest increase. The bottom line is that rates were never going to hold at the record lows we have seen, and we need to just accept the fact that they will continue trending higher as we move through the year but are yet at a level that suggests impending doom for the housing arena. So, where do I think that rates will be by the end of this year? Well, here is my very latest forecast for the rest of this year.

Mortgage Rates Forecast

Given all we know in respect to the Fed and the current situation in Ukraine, my model suggests a significant jump in the first quarter, but then the pace of increase slows significantly and we will end this year at a rate that is almost half a percentage point above the forecast I offered at the start of the year.

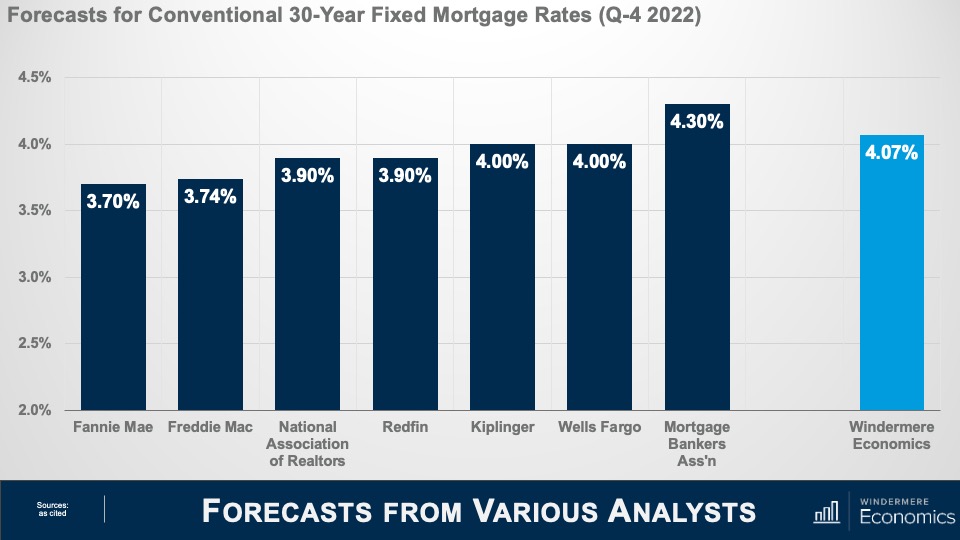

Forecasts From Various Analysts

Of course, this is the opinion of just one economist, so I thought it would be useful for you to see what others are thinking. And amazingly enough, most of us—at least for now—are still in a pretty tight range regarding our expectations for the average rate in the 4th quarter of 2022 with Fannie Mae at the low end of the spectrum and the Mortgage Bankers Association at the high end.

I honestly believe that, all things being equal, the impact of higher mortgage rates is unlikely to significantly impact the U.S. market this year and, even with rates rising, the market will remain tight in terms of supply and will continue to favor home sellers. That said, once we break above 4.5%, I would expect to see the increased cost of financing having a greater impact on not just on demand but on price growth, too.

And if you are wondering why I am so sure about this, it’s simply because we saw the exact same situation in 2018 when rates rose to 4.9% and we saw a palpable pull back in sales; which dropped from an annual rate of 5.4 million to 5 million units and the pace of price growth dropped from 5.9% to 3.3%. Now, I don’t see rates getting close to 5% for quite some time and therefore still expect demand to remain robust—off the all-time highs we have seen—but still solid given demographically-driven demand as well as increasing demand from buyers trying to find a new home before rates much further.

Of course, the impact of rates rising will not be felt equally across all markets. Many areas, and especially in coastal States, have seen home values skyrocket to levels that are well above the national average. Although incomes are generally higher in these markets, buyers in more expensive areas will feel more pain from higher financing costs.

And there you have it. I hope that today’s chat has not only given you some additional tools to use in your day-to-day business but has also given you enough information to hopefully ease some of the worry that many of you are feeling right now. As always, if you have any questions or comments about this particular topic, please do reach out to me but, in the meantime, stay safe out there and I look forward to visiting with you all again next month.

Known for its signature chic comfort, the farmhouse style is a popular method of interior design for homeowners looking to blend elements of modern and traditional design. With a rustic charm at its heart that recalls images of the countryside and wide-open landscapes, the farmhouse style steadily picked up steam in the 2010s and continues to grow in the 2020s. The following information is a guide to understanding the characteristics that make up the farmhouse style and how you can translate them into your home.

What is farmhouse style?

The farmhouse style predominantly uses a white/grey/beige color palette which provides a foundation for complementing elements and brighter colors. Against this clean backdrop, rustic materials can really shine. Exposed wood beams of timber or reclaimed wood, shiplap, and wrought iron are materials typically used help to round out the aesthetic, creating that rural-with-a-touch-of-modern feeling that the farmhouse style is known for. These combinations create a sense of openness and simplicity in the spaces where they’re used. In the kitchen, the farmhouse style feels clean and inviting; in the living room, it beckons members of the household and guests alike to sit back and relax; and in the dining room, it creates the perfect setting for enjoying a meal together.

When it comes to furniture, there are specific choices you can make that will help reinforce your personal farmhouse style. Functionality is a core principle of farmhouse design, exemplified by its use of reclaimed and found materials. When looking at furniture, tune your radar to pieces that are simple and functional rather than ornate and complex. Farmhouse’s warmth contrasts the colder feel of minimalism, so when thinking about texture, know that you’re not bound to selecting only the cleanest possible lines—feel free to experiment! With natural elements like stone and wood already providing a varied blend of textures, you can afford to be bold in your choice of throw pillows, blankets, carpeting, and furniture set pieces.

The farmhouse style will give you license to decorate with antiques and vintage materials. Items like armoires, wooden iceboxes, and vanities will find a fitting home among your complementary decorative items. With a prevalence of wood, choose grain patterns and wood tones that complement each other well without clashing. Clutter can get in the way of the coziness that the farmhouse style naturally evokes, so it’s important to keep your main living areas well maintained to truly let your home’s interior design flourish.

With the farmhouse style, it all comes back to comfort. If you’re looking to make the spaces in your home more comfortable, either fully adopting or borrowing from the farmhouse style may be just the ticket. For more helpful tips on home design, read our blog post on how to upgrade your bedroom:

The process of buying a home is made up of several stages. After preliminary stages like getting pre-approved, searching for homes, and finding a buyer’s agent, various contracts and buyer-seller agreements will enter the fold as the purchase of a home is finalized. Escrow is a pivotal point in the buying process that will ultimately lead to you, the buyer, receiving the keys to your new home. Here is your guide to understanding escrow and how it works.

A Guide to Understanding Escrow

What is escrow?

Escrow is a vehicle for temporarily holding the funds in a real estate transaction and making sure they distribute properly when the deal goes through. The funds and documents are held by a third party “in escrow” until the terms of the agreement have been filled. Escrow accounts protect the buyer’s “good faith deposit” (also known as “earnest money”) to ensure it goes to the seller as outlined in the real estate contract. These funds show that the buyer is serious about staying true to their offer and does, in fact, intend to pay the seller.

The seller accepting your offer is your cue to begin the escrow process. Your first step is to open an escrow account. Then, you’ll go about securing a mortgage and obtaining insurance for the home. When the deal goes through, the funds in escrow will go towards your down payment and closing costs. Sometimes, the escrow funds are held in the account after the sale of the home has been finalized. This is known as an “escrow holdback.” This situation can often arise if a buyer discovers an issue with the home in their final walkthrough that wasn’t present during an earlier inspection. If the home is in a worse condition than what shows in the contract, then the good faith deposit will go back to the buyer, and they are released from the contract.

Before you make an offer, get a better idea of which homes you can afford by using our Home Monthly Payment Calculator. With current rates based on national averages and customizable mortgage terms, you can experiment with different values to get an estimate of your monthly payment for any listing price.

Once all the I’s have been dotted and the t’s have been crossed, an escrow officer will issue a deed with you listed as the new property owner. Then, you’ll order a wire transfer for the funds to be allocated. Once closing is complete, the third party holding the escrow funds will distribute them per the terms of the agreement. This distribution of funds makes up a part of the total closing costs for buyers, which include, among others, real estate agent commissions, title and insurance fees, and any HOA dues that may apply.

Escrow evolves after the purchase of a home. Once you’ve bought your new house, your lender will open a mortgage escrow account, through which you’ll pay for your property taxes and homeowners insurance. Held by your lender, the money in this account is added to your monthly mortgage payment.

To not get overwhelmed during the escrow process, it’s important to read your documents carefully and ask questions to make sure you understand them. When it comes time to close on the home, read through everything carefully to make sure you haven’t missed anything before the deal goes final. For more information on the required financing throughout the home buying process, connect with an experienced, local Windermere agent.

Windermere Vice President of DEI, Samantha Enos, recently announced our partnership with non-profit Community Development Financial Institution HomeSight on a new loan product to increase purchasing power and help bridge the affordability gap facing Black/African American homebuyers.

The Sam Smith “Hi Neighbor” Homeownership Fund

“The Sam Smith ‘Hi Neighbor’ Homeownership Fund is designed to help low-to-moderate-income home buyers who have historically been underserved by traditional lenders,” said Enos, adding, “Through donations from the Windermere Foundation, U.S. Bank, and JP Morgan Chase, the Sam Smith fund is helping to reduce barriers to homeownership by funding loan products for Black/African American first-time home buyers in Washington State.”

Named after Washington State Legislator Sam Smith, who championed the passing of the state’s Open Housing Law barring discrimination based on race and religion in 1967, our hope is that, together with HomeSight, we can be part of a solution that helps increase Black/African Americans homeownership in the state of Washington.

According to a report by National Association of REALTORS®, Black/African American home buyers are more than twice as likely to be rejected for mortgage loans than white home buyers. Nationwide, only 43% of Black/African Americans can afford to buy a home versus 63% for Whites. In Seattle, the Black/African American homeownership rate is 25.8% compared to 50.9% of White homeowners. While in King County, the median income for Black households is $48,075, about half the median income of White households at $94,533.

Carl Smith, son of Legislator Sam Smith, said “It’s an honor and a pleasure to have the Sam Smith name used to pursue equity in home purchases,” said Mr. Smith, adding, “My grandfather instilled in my father that the way to have freedom is to have land and for people in that era, it was freedom.”

Since launching in November 2021, Windermere has contributed $80,237 to the fund through donations from our agents, offices, and company leadership, including a personal donation of $50,000 from the Jacobi family to help seed the fund. Windermere Co-President, OB Jacobi, said that the goal is for Windermere to raise $250,000 annually. Darryl Smith, Executive Director of HomeSight, adds that the fund has already helped three families realize their dream of homeownership and there are currently four additional families in the process of looking for homes.

HomeSight identifies borrowers that qualify for the Sam Smith fund and grants up to $12,000 to use towards their home purchase costs. The loans can be layered on top of the buyer’s existing mortgage loans or work in conjunction with other HomeSight purchase assistance programs. Sam Smith deferred loans are repayable in thirty years, when the homeowner refinances, or when they sell. Once the loans are paid off, HomeSight resolves the funds, ensuring availability to future borrowers.

For more information on our commitment to diversity, equity, and inclusion, visit windermere.com/dei.

The Spanish style of home design and the architecture from which it originates goes by many names but is commonly known as “Spanish Eclectic” or “Spanish Revival.” This distinct style has a long history that has helped to shape the residential aesthetic of certain parts of the United States, predominantly the Southwest. By digging into the history and design elements of this unique look, we can understand a bit more about why these homes are so special.

Spanish Eclectic

The Spanish Eclectic aesthetic is an amalgam of Native American, Mexican, and Spanish missionary styles. The first appearances of this housing style on American soil trace back to the days of the earliest Spanish settlers as they began to build out their dwellings. These homes were built with the materials that have become defined by their appearance: adobe, stucco, and clay. In this way, Spanish Eclectic shares some similarities with the Mediterranean style of architecture. Over time, this style saw periods of revival, during which construction of these homes experienced an uptick. Throughout these revival periods, additional features were added to the homes to accommodate the needs of modern living at the time.

The Spanish Eclectic style has several distinct characteristics in both its interior and exterior design. The thick stucco walls provide the backdrop for their unique look, but also help to keep the home cool during hot days and insulated at night. These homes typically have low-pitched terracotta roofs, exposed wooden support beams, and arched entryways and corridors, reflecting the features of their missionary origins.

Additional design details include wrought iron, colorful tile, and small windows. Though they may not be present in every Spanish Eclectic home due to limited space, courtyards are a common feature of this house style. You’ll often see a courtyard in the center of the home for a plaza-like arrangement, on the side of the home, or in the back.

For more information on the different home styles, read our blog post on cottage homes:

Financing terms are the nuts and bolts of a successful home purchase. Once you’ve decided you’re ready to buy a house, it’s a matter of making the numbers work. So, which home loan is the right one for you? Knowing the different types of mortgage loans available to you will allow you to pinpoint the one that best fits your needs and is financially viable.

The Different Types of Home Loans for Buyers

Conventional Loans

Conventional loans are the most popular type of home loan issued to borrowers. Offered by private lenders, they are not backed by the government. Conventional mortgages divide into two subsets: conforming loans; which adhere to Federal Housing Financing Agency (FHFA) guidelines, and non-conforming loans; which do not. Due to the added risk taken on by the lender, non-conforming loans typically have higher rates. A jumbo loan is an example of a non-conforming loan, due to its loan amounts being higher than the amount limits laid out in the underwriting guidelines. The two most common conventional loans are 30-year and 15-year fixed-rate mortgages.

15-Year and 30-Year Fixed-Rate Mortgages

The terms of your loan will drastically impact all aspects of your mortgage. With a 30-year mortgage, you’ll have lower monthly payments and a higher interest rate than you’d have with a 15-year mortgage, meaning you’ll pay more in interest over the life of the loan. With a 15-year mortgage, you’ll pay less interest, but you’ll have a higher monthly payment. Compared to a 30-year mortgage, a 15-year mortgage can save you money over the life of the loan, simply because you’re in debt for half the time; however, the higher monthly payments may be unaffordable for some.

Whereas conventional loans are not backed by a federal entity, there are several unconventional loans that are backed by the U.S. government. These unconventional loans can often provide a path to homeownership for borrowers who don’t have the credentials to qualify for a conventional loan.

FHA and USDA mortgages are two common types of government-backed loans. Instead of having to make a 20% down payment on a conventional loan to avoid private mortgage insurance (PMI), an FHA loan allows buyers to qualify for a mortgage with a down payment as little as 3.5%. USDA loans enable buyers to purchase a home with reduced interest rates. VA loans offer several benefits for active service personnel and veterans looking to buy a home, including not having to purchase mortgage insurance.

Home Monthly Payment Calculator

To get an idea of what you can afford, use our free Home Monthly Payment Calculator by clicking the button below. With current rates based on national averages and customizable mortgage terms, you can experiment with different values to get an estimate of your monthly payment for any listing price. By using the Home Monthly Payment Calculator, you can make a well-informed estimation of whether it’s the right time to buy.

Fixed-Rate vs. Adjustable-Rate Mortgages

Fixed-rate mortgages allow you to lock in a specified interest rate for the life of the loan. With an unchanging monthly mortgage payment, a fixed-rate mortgage makes financial planning easier. Adjustable-rate mortgages’ interest rates will go up and down based on market conditions. Many ARMs will start with a fixed-interest rate period followed by a variable interest rate until the loan amount is paid off. Keep in mind that a sudden change in your financial situation could make your monthly ARM payments unaffordable, which could result in a loan default.

Other Home Loans

There are other more niche financing options available for prospective home buyers. For example, a construction loan can be useful if you’re planning on building a home. Balloon mortgages and sub-prime mortgages can make homeownership feasible for those who aren’t financially prepared for the typical repayment structure of a mortgage. These loans, however, come with greater risks. Talk to a mortgage broker to understand the terms of these agreements before making a final decision.

For more information on financing your next home purchase, connect with an experienced, local Windermere agent:

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

")