In today’s evolving real estate landscape, one of the biggest changes buyers will encounter is the relatively new requirement to sign a Buyer Agency Agreement. While this added step may sound formal, it’s actually designed to make the home-buying process more transparent, secure, and ultimately more beneficial for everyone involved.

What is a Buyer-Agency Agreement?

At its core, a Buyer Agency Agreement is a written contract between you and your real estate agent. It outlines your working relationship, defining the agent’s responsibilities, the services they’ll provide, the duration of your partnership, and how their compensation will be handled. Think of it as the roadmap for your home-buying journey, ensuring everyone starts on the same page, with mutual understanding and trust.

Starting in mid-2024, the National Association of REALTORS® (NAR) began requiring agents to have a signed buyer agency agreement before showing homes to clients. This change stems from a nationwide settlement designed to bring greater transparency and accountability to real estate transactions by ensuring all agent-buyer relationships are clearly defined in writing. In some markets, this requirement isn’t new; states like Washington, Idaho, and Utah have long recognized the importance of formalizing this relationship. But for many buyers, this will be their first time signing such an agreement, and understanding its purpose can make all the difference.

So, why does it matter?

Transparency and Trust

This agreement ensures clarity around both compensation and representation. It spells out how your agent is paid—whether by the seller, by the buyer, or by both—so there are no surprises later. With these details defined upfront, you can move forward with confidence, knowing your agent’s focus is squarely on your best interests.

Defined Roles and Responsibilities

A Buyer Agency Agreement clearly outlines what your agent will do for you: from helping you navigate listings and compare neighborhoods to guiding you through offers, inspections, and closing. It also defines your responsibilities as a buyer, such as communicating openly and working exclusively with your chosen agent throughout the duration of the agreement. Together, these expectations create a smoother, more collaborative experience.

Protection and Professionalism

Buying a home is one of life’s biggest investments, and having a written agreement in place protects both you and your agent by setting clear parameters for your working relationship. It ensures your agent is committed to advocating for your needs, maintaining confidentiality, and acting in your best interest throughout the process.

While some may see the Buyer Agency Agreement as an extra step, it’s really a safeguard, one that reinforces the professionalism and dedication that define Windermere Real Estate agents. It turns a handshake of trust into a documented commitment, empowering buyers to make confident, informed decisions at every stage of the journey.

Connect with a Windermere agent today to learn more about how we can help you navigate your home search with confidence.

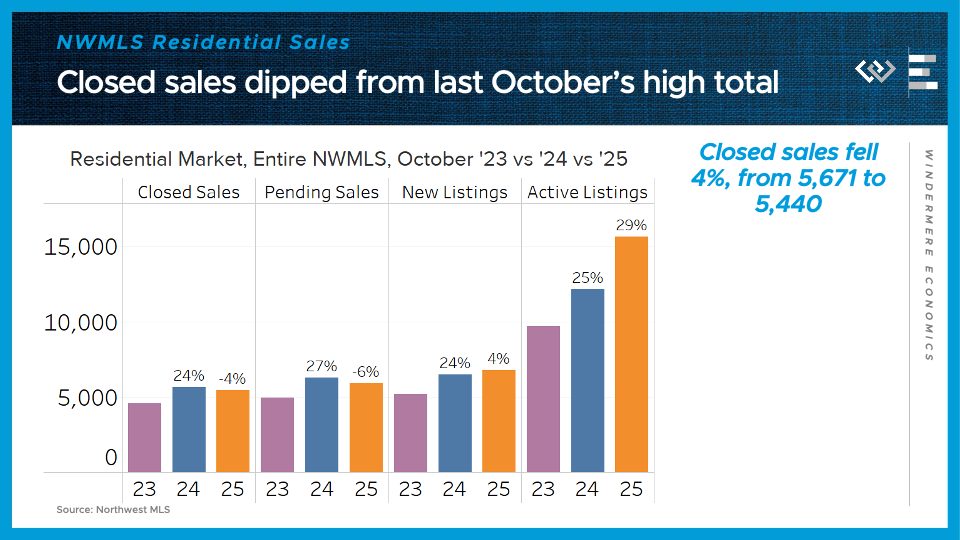

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the October 2025 data from the Northwest MLS.

This October, the Washington housing market began its usual seasonal shift into the cooler 4th quarter. Compared to last year, it looked particularly cool, because last October saw a sudden burst of buying activity in the wake of the Fed finally beginning to cut interest rates.

Across the Northwest MLS, closed home sales came in 4% below last October’s total. MLS. Pending sales, which give some signal about next month’s sales, were down 6% from the same time last year.

On the supply side, the flow of new listings remains roughly even with last year’s, or just 4% higher. Finally, the month ended with 29% more active listings than last October, continuing a slowdown in inventory growth but still leaving buyers with more options than they had last year or the year before.

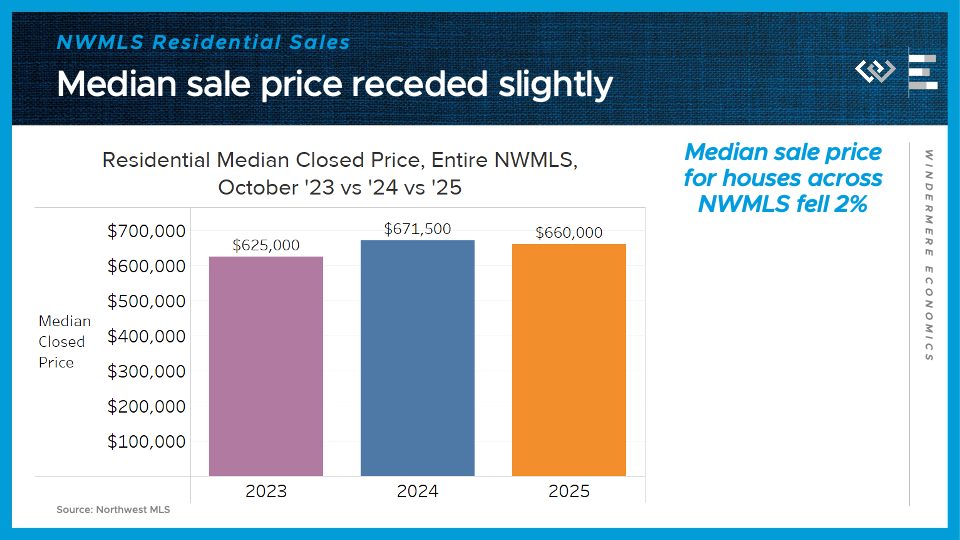

Those higher inventory levels are starting to put some downward pressure on prices, which dipped 2%, to a median of $660,000 for a residential home sale in October.

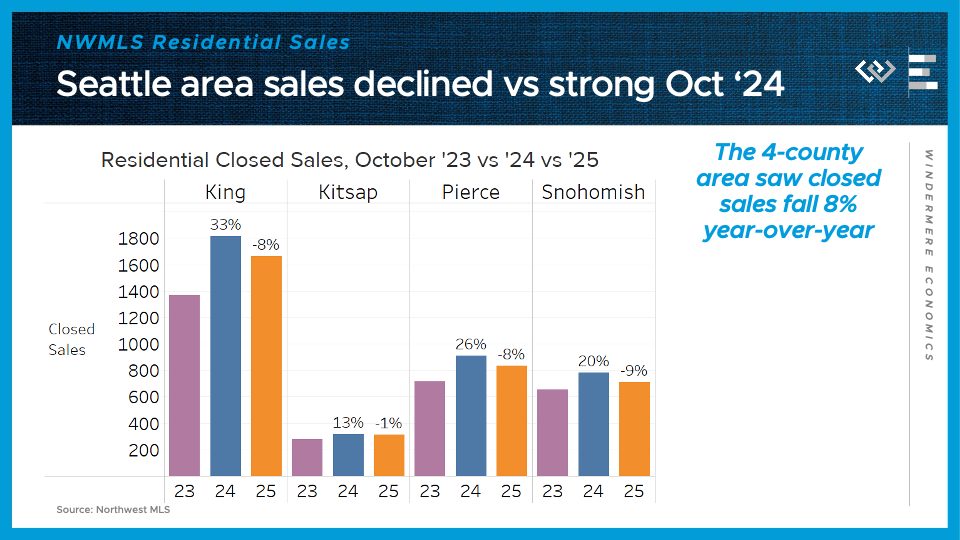

Now I’ll turn to a closer look at the four counties encompassing the greater Seattle area.

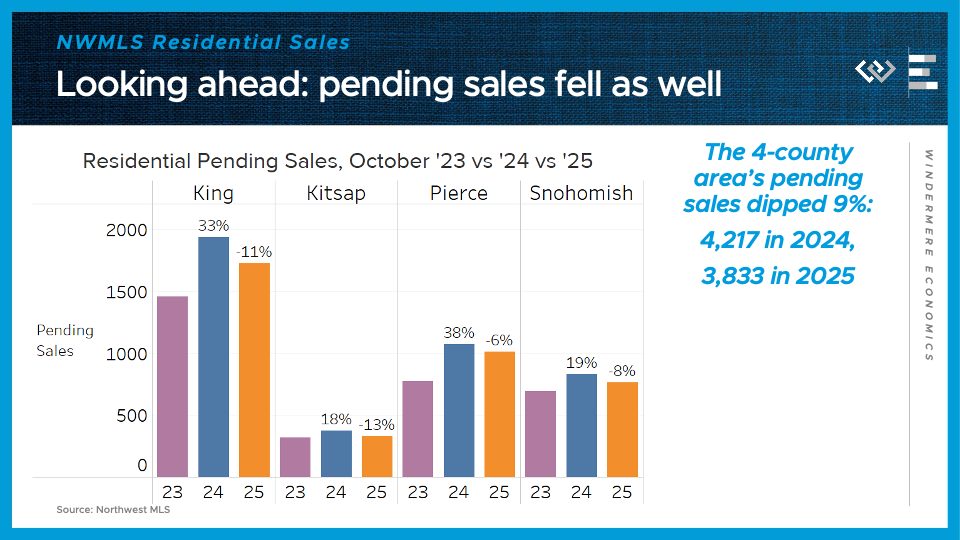

Closed sales stepped down by 8% from last October, although that month last year had unusually high sales, especially in King County, where 2024’s sales were a whopping 33% higher than in 2023.

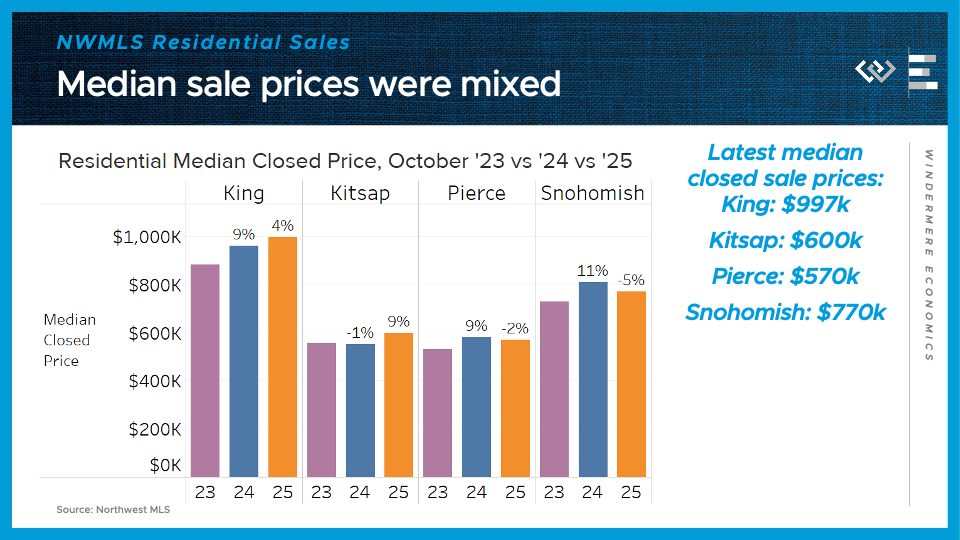

Median sale prices were split: 4% higher in King; 9% higher in Kitsap; but 2% lower in Pierce, and 5% lower in Snohomish County. That may represent a continued trend of demand retrenching toward the employment center of the region, around Seattle and Bellevue, as new return-to-office policies come into effect.

Looking ahead, pending sales fell 9% across the region, although again King County’s sales drop looks a bit like mean reversion after a standout 2024 number.

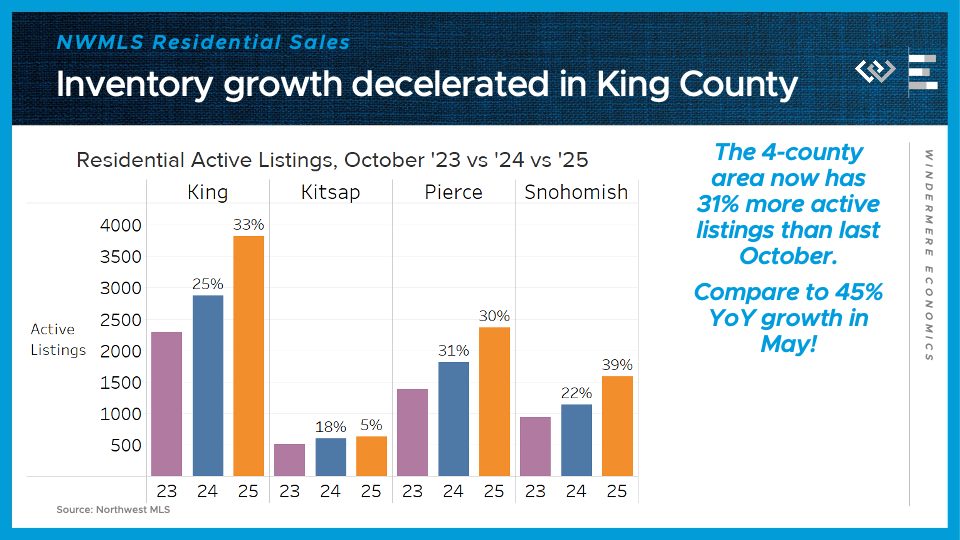

On the supply side, the 4-county greater Seattle area had 31% more active listings than at the end of October 2024. That continues the moderation of inventory growth we’ve seen since May, when this metric peaked at 45% year-over-year growth.

Looking ahead, we are entering one of the best times of the year for savvy buyers and their agents to find a bargain, and with much more inventory than even this time in the last two years. Whether they jump at the opportunity will be revealed in next month’s data!

For more than 20 years, the benefits of home staging have been well documented. Countless studies have shown that staging helps homes sell more quickly, and often for a higher price. According to the National Association of REALTORS®, 30 percent of agents reported that staging led to a 1 to 10 percent increase in the dollar value offered by buyers, and nearly half of sellers’ agents said staging helped reduce the time on market. Studies also indicate that buyers can generally decide if they’re interested within the first 30 seconds of seeing a home.

Staging is all about creating a welcoming, move-in-ready atmosphere. It helps buyers picture themselves in the space, highlights your home’s best features, and minimizes anything that might distract from its potential. From small styling updates to full furniture placement, staging can make a big difference in how your home is perceived and how it performs on the market.

If you’re planning to sell, here’s why staging is still one of the smartest strategies you can use and how to make the most of it.

A Strong First Impression Starts Online

In 2023, the National Association of REALTORS® Generational Trends Report revealed that 96 percent of buyers now rely on the internet to search for their next home. And in a market where most buyers begin their home search online, how your home looks and feels from the start has never been more important. Your online photos, videos, and virtual tours should make buyers want to see more. Staging helps make that possible by photographing better, helping rooms look more spacious and inviting, and encouraging buyers to take the next step.

Thanks to newer tools like virtual staging and AI design platforms, sellers have more options than ever to enhance their home’s online presence. These can be especially helpful for vacant homes or spaces that are difficult to define, giving buyers a sense of scale, purpose, and warmth before setting foot in the front door.

What Rooms Matter Most?

Not every room in your home needs to be staged, but some have more influence on buyers than others. 37 percent of buyer’s agents say that the living room is the most important room to stage, followed by the primary bedroom at 34 percent, and the kitchen at 23 percent. These are the spaces where people imagine themselves spending the most time, relaxing, hosting, and settling into daily life.

Staging can also be especially helpful in vacant rooms or uniquely shaped rooms. A few well-placed pieces of furniture can help define how the space might be used and create a natural flow from room to room. When these rooms feel welcoming and well put together, buyers are more likely to see the home as a fit for their lifestyle. A little extra effort in the right spaces can go a long way toward making that connection.

Clear, Clean, and Clutter-Free

To further inspire buyers to imagine the space as their own, make sure every room—including closets and the garage—is clean and clutter-free. You may even want to hire professionals to give your home a thorough deep clean.

Family photos, personal memorabilia, and collectibles should be removed from the home for your safety. Closets, shelves, and other storage areas should be mostly empty. Workbenches should be free of tools and projects. Clear the kitchen counters, store non-necessary cookware, and remove magnets from the refrigerator door.

The same goes for furniture. If removing a chair, a lamp, a table, or other furnishings will make a particular space look larger or more inviting, then do it.

You don’t want your home to appear cold, unloved, or unlived-in, but you do want to remove distractions and provide prospective buyers with a blank canvas of sorts. Plus, de-cluttering your home now will make it that much easier to pack when it comes time to move.

Neutralize and Brighten

Every home is a personal expression of its owner. But when you become a seller, you’ll want to look for ways to make your home appeal to your target market. Keep in mind, your target market is the group of people most likely to be interested in a home like yours, which your agent can help you determine.

A good strategy for staging your home is to “neutralize” the design of your interior. A truly neutral interior design allows people to easily imagine their own belongings in the space—and to envision how some simple changes would make it uniquely their own.

Paint over bold wall colors with something more neutral, like a light beige, warm gray, or soft brown. The old advice used to be, “paint everything white,” but often that creates too sterile an environment, while dark colors can make a room look small, even a bit dirty. Muted tones and soft colors work best. Likewise, consider removing wallpaper if it’s a bold or busy design.

Lighting is key. Replace heavy, dark curtains with neutral-colored sheer versions; this will soften the hard edges around windows while letting in lots of natural light. Turn on lamps, and if necessary, install lighting fixtures to brighten any dark spaces—especially the entry area.

A Smart Investment with Lasting Impact

Staging is a powerful advantage when selling your home, but that’s not the only reason to do it. Staging uncovers problems that need to be addressed, repairs that need to be made, and upgrades that should be undertaken. Staged properties are more inviting, and that inspires the kind of peace of mind that gets buyers to sign on the dotted line. In the age of social media, a well-staged home is a home that stands out, gets shared, and sticks in people’s minds.

What’s more, the investment in staging can bring a higher price. According to the National Association of REALTORS®, the average staging investment is between 1 percent and 3 percent of the home’s asking price, and typically generates a return of 8 to 10 percent.

In short, with less time on the market and higher selling prices, the small cost of staging your home is a wise investment.

Where to Start

If you’re concerned about the additional cost of staging, rest assured. Even a relatively small investment of time and money can reap big returns. There are even things you can do yourself for little to no cost. Contact your agent for advice on how to stage your home most effectively or for a recommendation on a professional stager. While the simple interior design techniques outlined above may seem more like common sense than marketing magic, you’d be surprised at how many homeowners routinely overlook them. And the results are clear: staging your house to make it more appealing to buyers is often all it takes to speed the sale and boost the sale price.

Thinking about selling your home? Connect with a Windermere agent to learn more about staging and how it can help you get the best possible results.

This is the latest in a series of videos with Windermere Principal Economist Jeff Tucker, where he delivers the key economic numbers to follow to keep you well-informed about what’s going on in the real estate market.

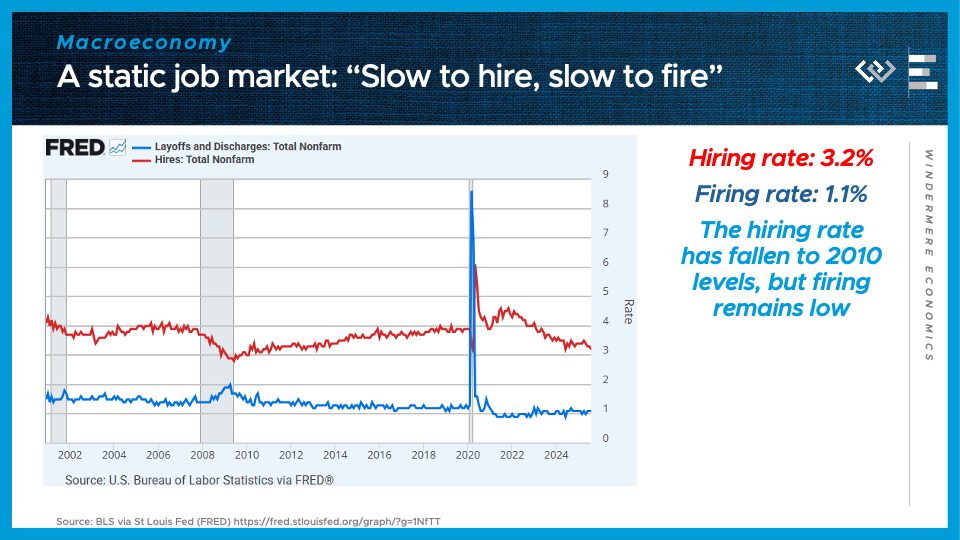

The government has shut down, and that means most government data publication has paused as well. The monthly CPI inflation report is delayed, and the monthly jobs report is suspended this month. So I’ll have to plan to revisit those when they resume, and in the meantime, I’ll start by checking in on the last publication out of the BLS before the shutdown: the Job Openings and Labor Turnover Survey, or JOLTS for short.

3.2%

That was the hiring rate in August, meaning the share of the workforce that just got hired. It’s around the lowest hiring rate since 2010, when the economy was just beginning to dust itself off and climb out of the Great Recession. It’s one half of a simple summary of the economy that labor economists have been using for a couple years now: “Slow to hire, slow to fire.”

1.1%

That’s the rate of layoffs and discharges, or, broadly, the firing rate, to fit the rhyming scheme. It is not particularly high right now, even if it’s up slightly from the essentially record-low firing rate below 1% we saw briefly in 2022.

Putting it together, what “Slow to hire, slow to fire” means is that employers are essentially hunkering down, hanging on to their workers but not interested in growing those payrolls quickly. For people with jobs, this means the economy feels essentially OK – not great, but OK. But for those without a job, it’s proving unusually hard to break back into the workforce, which makes this a terrible time to be unemployed, and is gradually inflicting stress on the credit system and consumer spending. These are early signs of an economic slowdown, but not yet any indication of a recession.

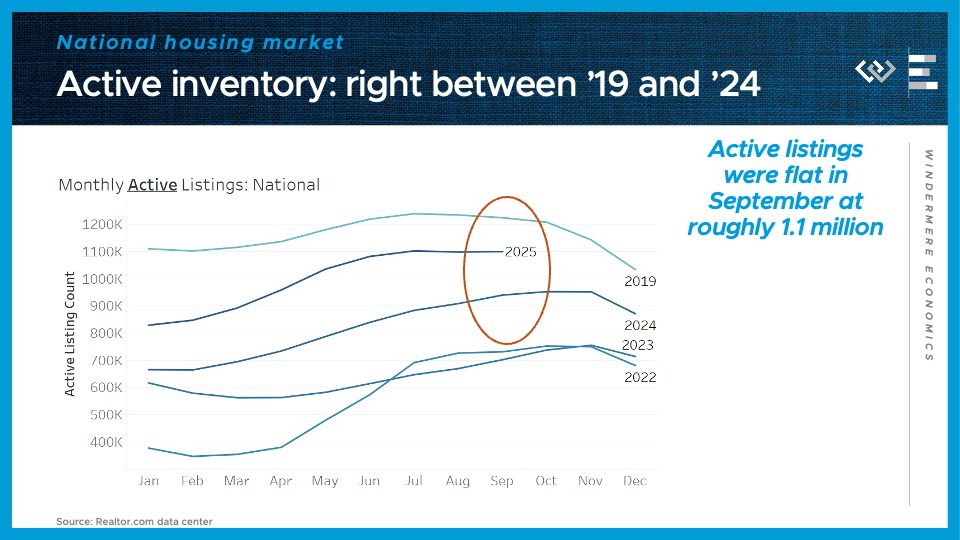

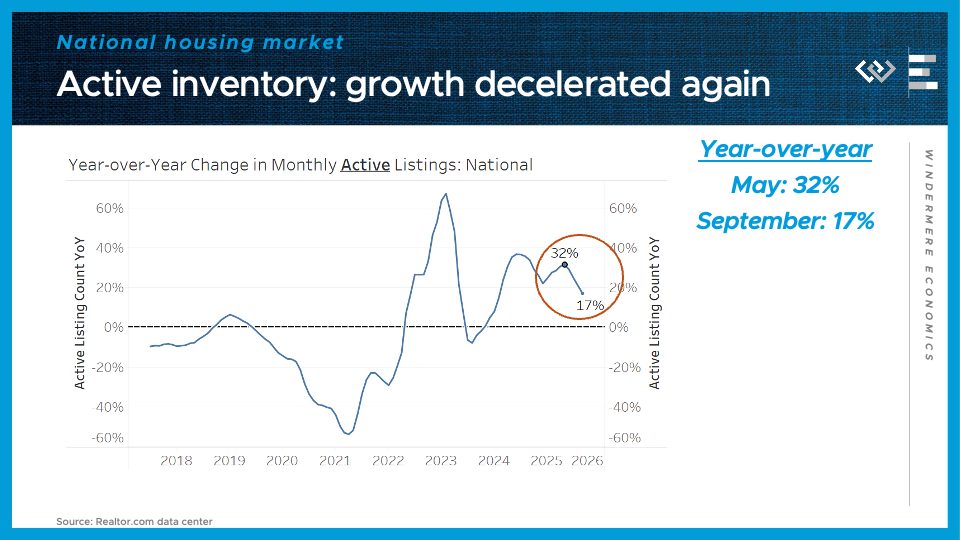

Turning to the housing market: we’ve got a familiar refrain this month. More inventory means buyers have gained more negotiating leverage, although September likely represented the high-water mark for the year, with about 1.1 million active listings for the 3rd month in a row. That’s 17% more than the same time last year.

Importantly, inventory growth has passed an inflection point: for the fourth month in a row, the pace of growth of inventory has fallen yet again. Growth has now been roughly cut in half, from the 32% annual growth seen in May. That means inventory is not on a runaway growth track toward a glut that would push prices down. Rather, the market is re-equilibrating, as some sellers steer clear of a buyers’ market, or de-list after not getting a satisfactory offer. For buyers, it means conditions have moved in their favor but they shouldn’t count on that trend intensifying much further.

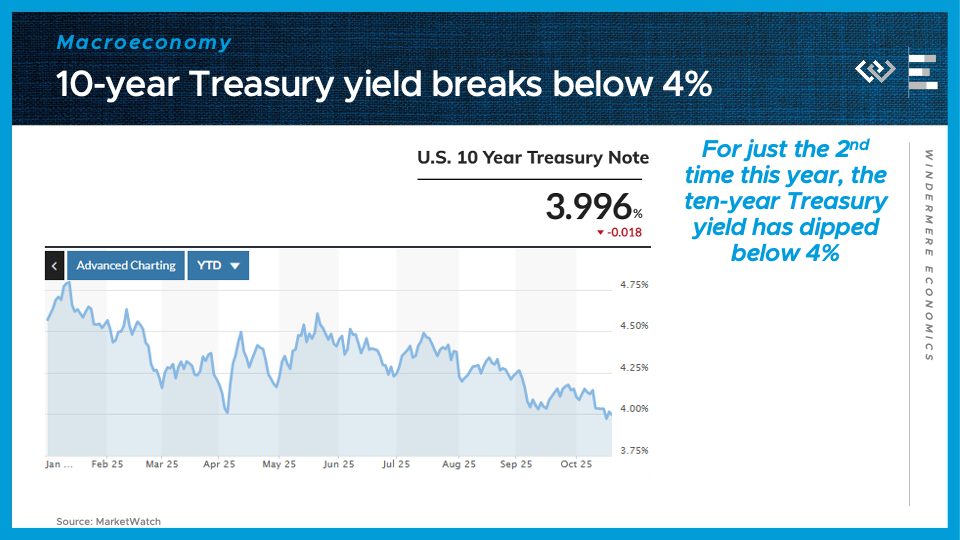

Another helpful factor for buyers, though, is that borrowing costs have continued to fall. The ten-year treasury yield, which is a major benchmark that mortgage rates tend to track, plus about 2 points, has now dipped below 4% for the first time this year. That reflects the combination of lower expected economic growth, and the resulting lower Fed Funds Rates expected over the next few years, as the Fed reacts to try to prevent a recession.

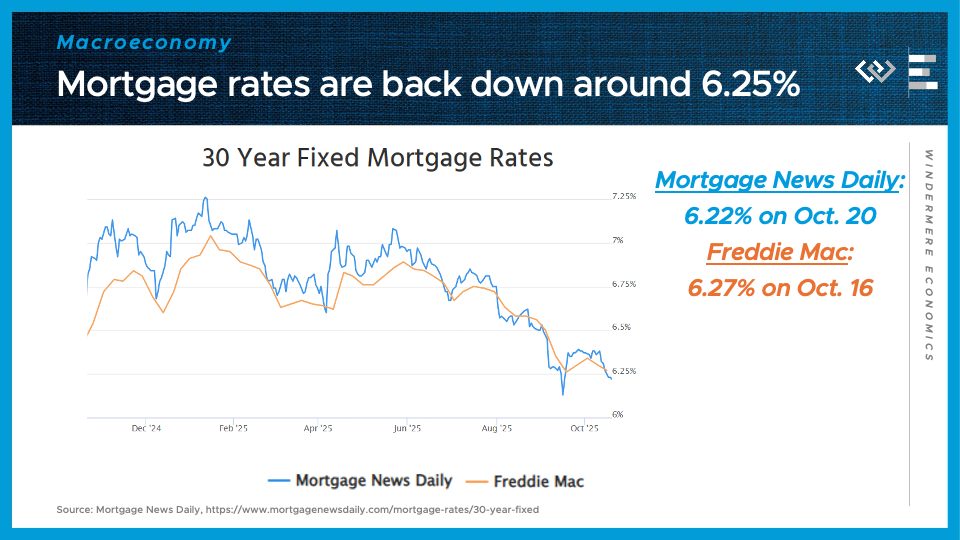

Hand in hand with those lower Treasury yields: Mortgage rates are moving back into their most favorable territory in 12 months, right around 6.25%. That represents significant savings compared to the rates of around 7% to start the year, and is partly driven by investor expectations of interest rate cuts to come. Because those expectations are already factored into the lower rates today, there’s no guarantee that mortgage rates will fall further even if and when the Fed continues cutting its overnight rate.

That is all for this month; I hope we’ll have more BLS data next month, and thanks as always for watching!

This is the first in a recurring series of blog posts taking a closer look at the U.S. economy and several major regional markets in Windermere’s nine-state footprint. Updates will be released on a quarterly basis.

Economic Overview

After a slow spring, the U.S. housing market cooled further this summer, with price gains leveling off and sales holding steady. Existing home sales have hovered around an annualized pace of 4 million through August—nearly identical to last year’s unusually low 4.06 million. Mortgage rates dropped in the third quarter, falling from an average of 6.82% in May and June to 6.35% in September. The combination of rising inventory, softer pricing, and lower mortgage rates is making this fall a good time to buy a home.

A key driver behind falling mortgage rates is the cooling U.S. economy, following a sharp slowdown in job growth over the summer. After revisions, nonfarm payrolls show little to no growth from April through August, and the next jobs reports are on hold due to the government shutdown. While slower growth poses challenges, it often brings the silver lining of lower interest rates—and this cycle appears to be following that pattern.

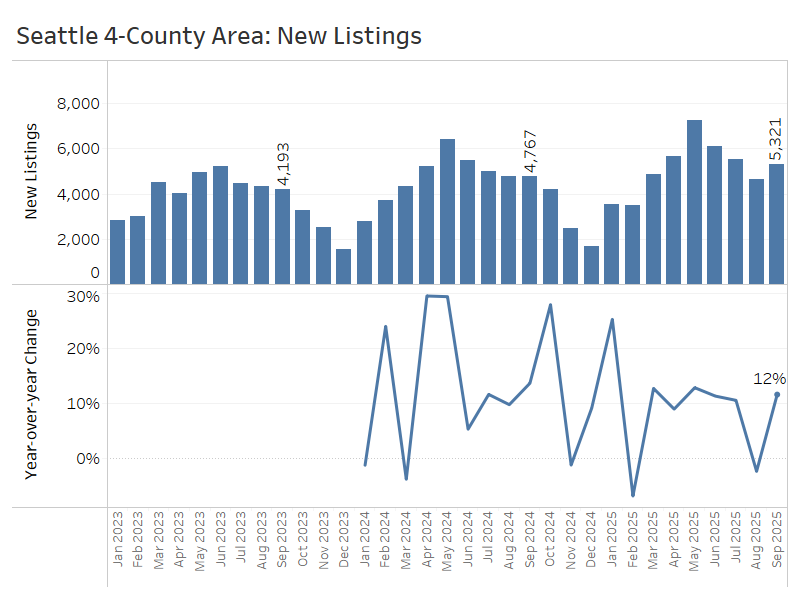

Greater Seattle Area (King, Snohomish, Pierce, and Kitsap Counties)

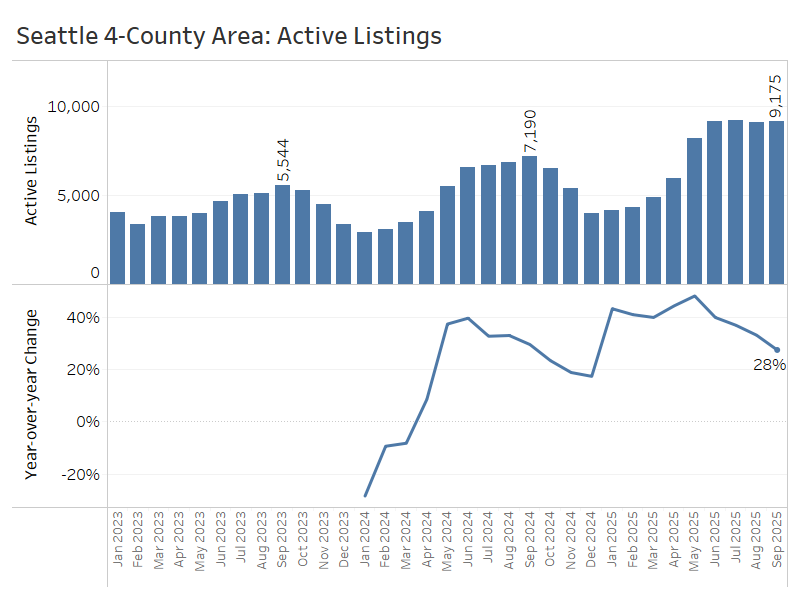

High inventory in the greater Seattle area has swung the balance of negotiating power in buyers’ favor across the region this year. As of the end of September, buyers could choose from nearly 9,200 active listings—8% more than the same time in 2024. Still, inventory growth has slowed throughout Q3, from a peak of 48% year-over-year growth back in May. Slower inventory growth means we are not headed for a glut of listings, which is good news for sellers.

Inventory growth reflects several consecutive months of rising new listingsoutpacing closedsales, which gradually replenishesthesupply of homes for sale. In September, the greater Seattle area had just over 5,300 new listings—about 12% more than last September. The entirety of Q3 reported 15,500 new listings, a 7% increase from Q3 2024.

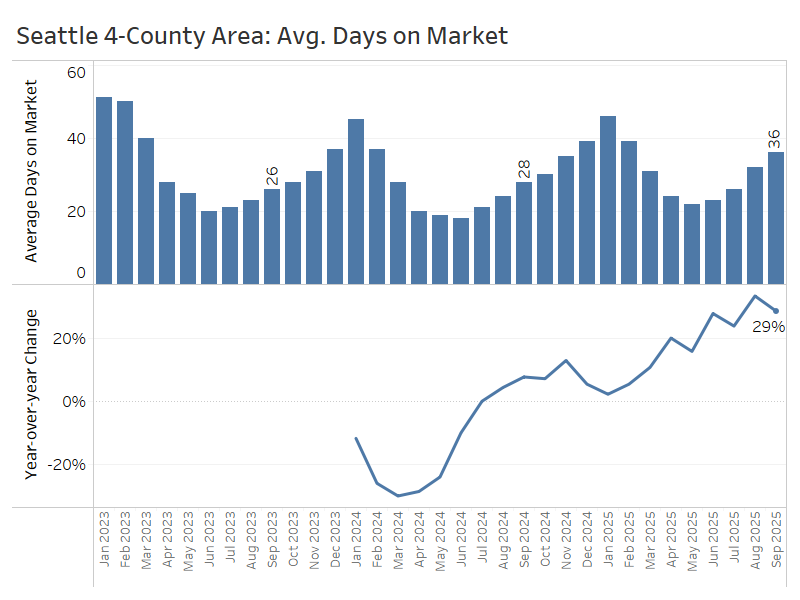

Not only do buyers have more options compared to a year ago, but they are also seeing listings linger on the market longer : an average of 36 days on market in September, up from 28 dayslast year. Days on market were substantially longer than last year’s levels in each month of Q3.

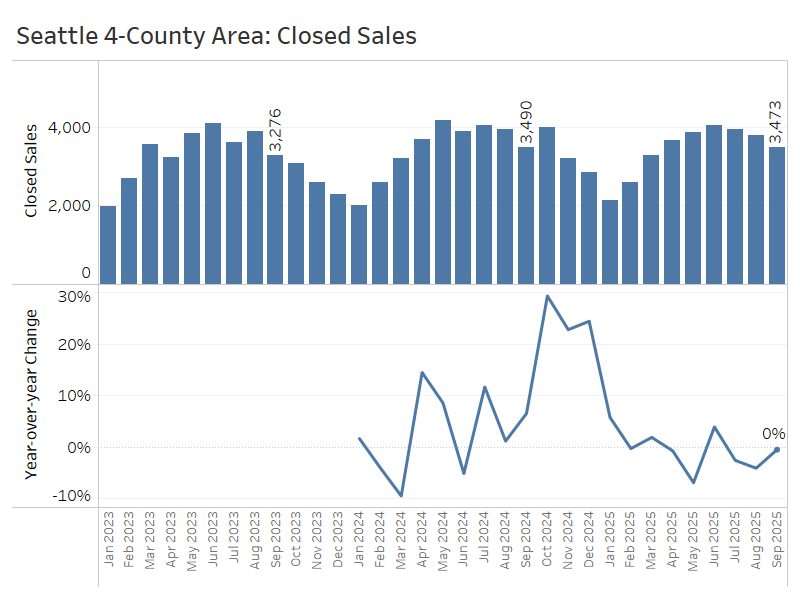

Unfortunately, the growth of inventory and new listings has not done much to generatehome sales.Closed sales in September totaled just under 3,500—virtually unchanged from the same period last year—following year-over-year declines of 3% in July and 4% in August.

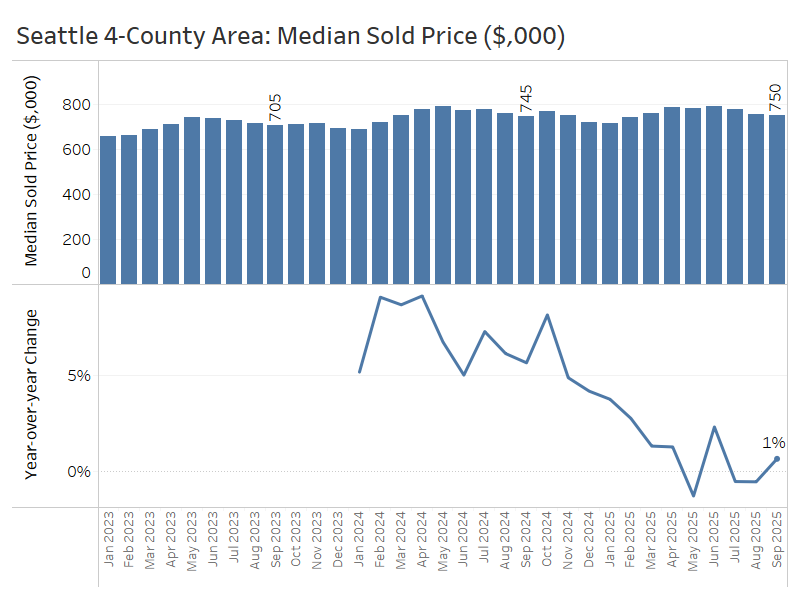

Home prices remain flat alongside sales. September’s median price of $750,000 was up less than 1% from a year ago, after slight declines in July and August.High mortgage rates and affordability challenges are capping price growth, while rising inventory will likely put downward pressure on prices going forward. The wildcard is seller behavior—whether they’ll cut prices to sell or hold firm and wait.

The greater Seattle region is still grappling with elevated inventory, but it has clearly passed an inflection point: inventory growth decelerated over the third quarter, preventing conditions from swinging much further in buyers’ favor. As it stands, they’ll still have ample options and negotiating leverage this fall and winter.

Greater Portland Area (Multnomah, Washington, Clackamas, and Clark Counties)

Broadly speaking, the greater Portland area housing market has entered the same holding pattern as many other Western U.S. cities: flat sales and prices; rising inventory and days on market; more negotiating power and options for buyers.

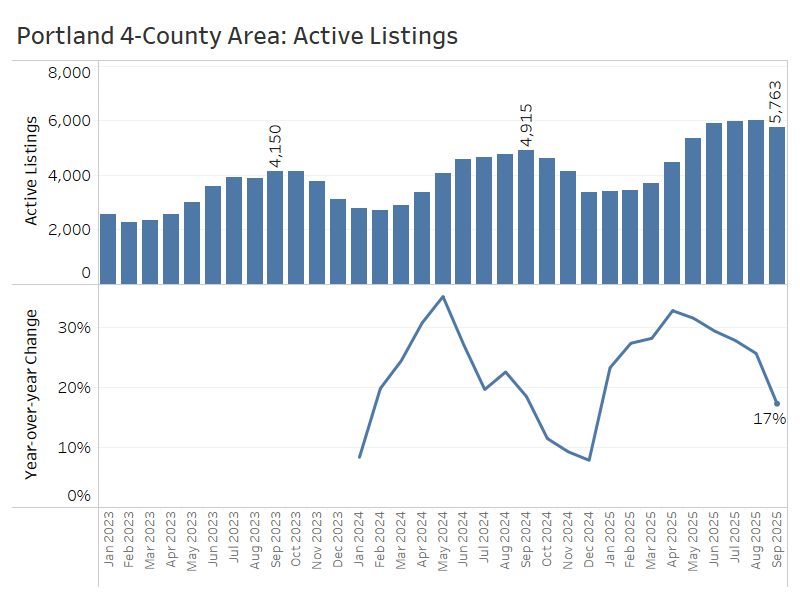

Active listings in the Portland area now stand close to 5,800, or about 17% more than this time last year. But the pace of inventory growth has decreased sharply since hitting 33% in April.

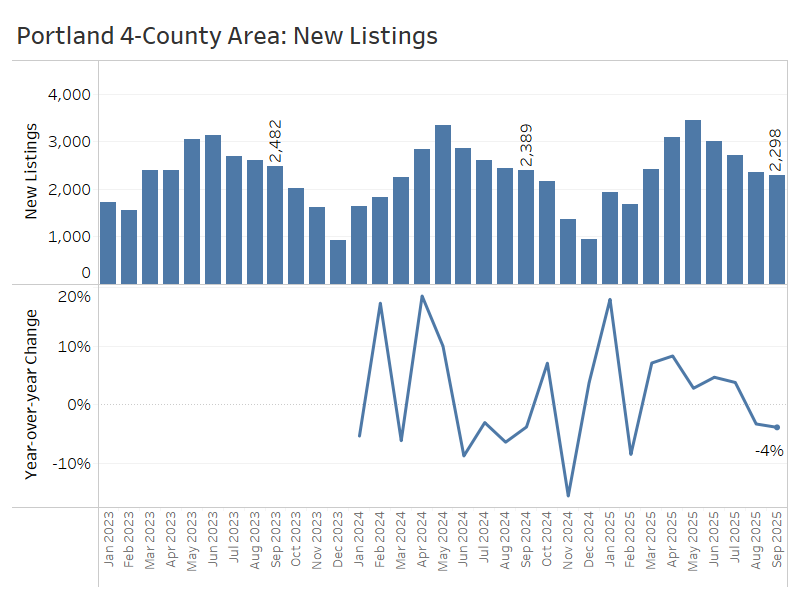

The slowdown in inventory growth can partly be attributed to a lower flow of new listings. The four–county Portland area saw year-over-year declines in new listings in both August and September, as some homeowners balked at listing in a slower market.

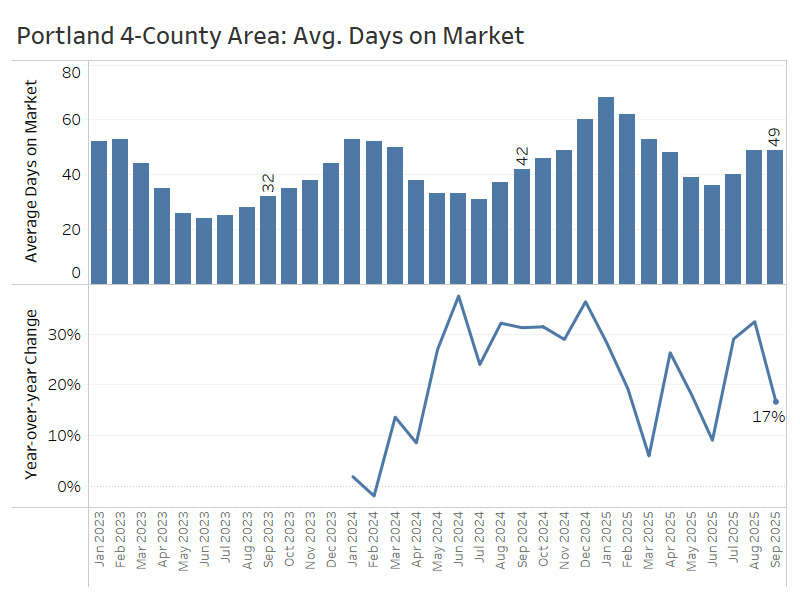

The average home sold after 49 days on the market—about a week longer than last September. This slower pace helps explain the higher inventory levels observed this year.

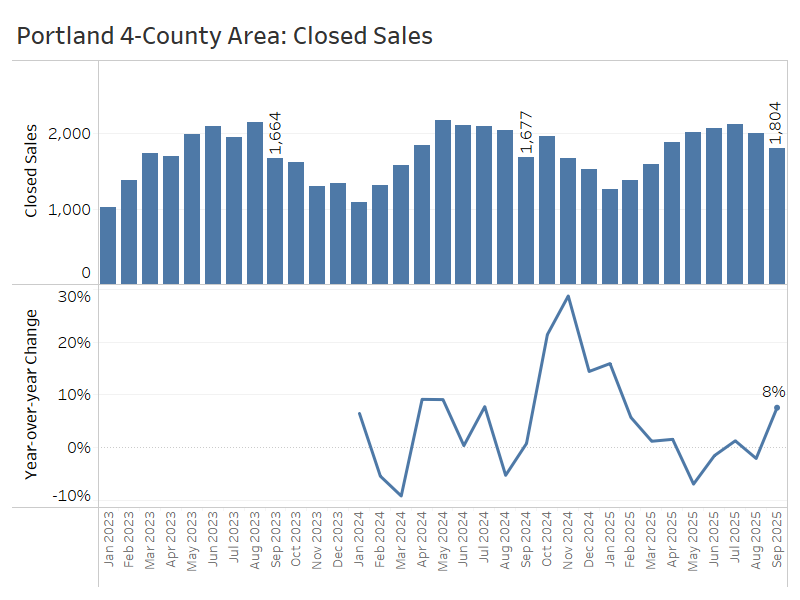

Closed sales of single-family homes climbed 8% yearoveryear in September, following relatively flatactivity in July and August. Sales volume momentum dropped sharply in May of this year, after impressive growth in late 2024.

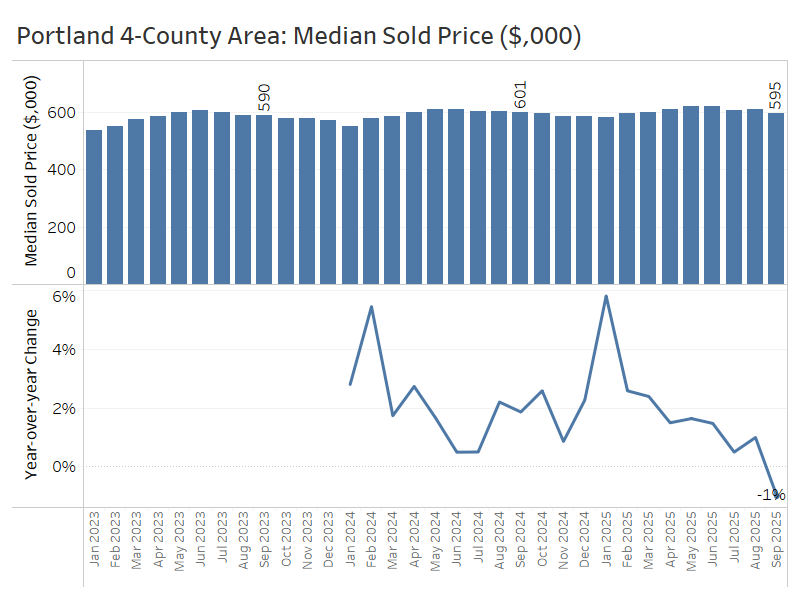

Alongside rebounding sales activity in September, the median home price edged slightly below year-ago levels—slippingfrom just over $600,000 to about $595,000. This trend of flat or modestly negative price growth is giving household incomessome time to catch up with the higher mortgage costs we’ve seen this year.

All in all, the greater Portland area seems to be working through the early stages of a market cooldown. The buildup of inventory is beginning to put downward pressure on home prices, whichappears to be discouraging some would-be sellers while also creating opportunities for buyers.

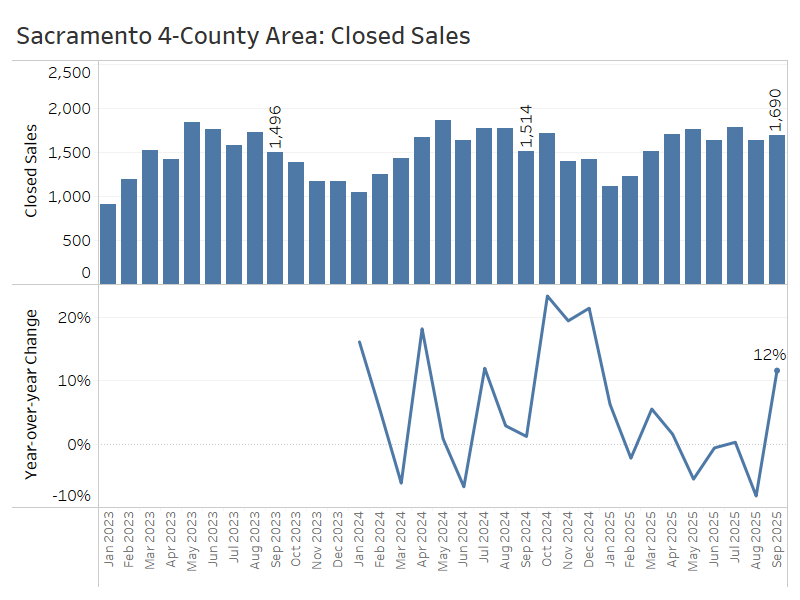

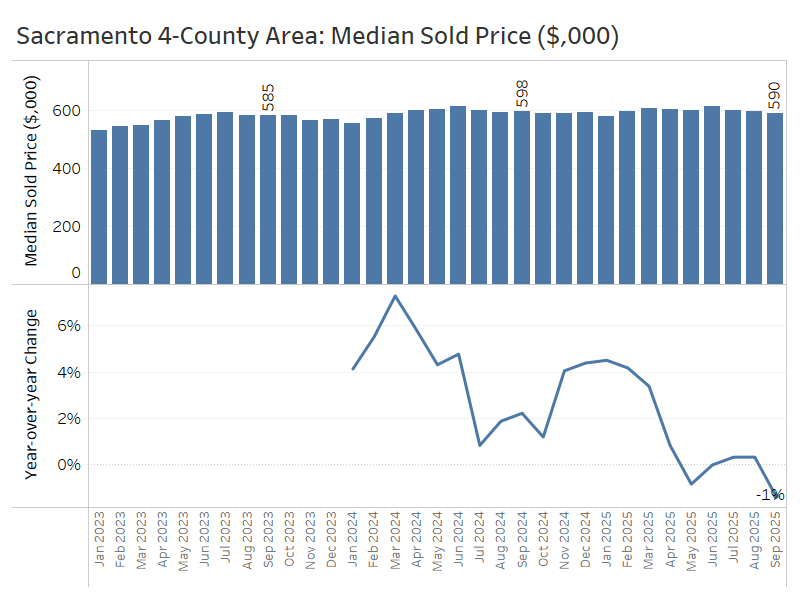

Greater Sacramento Area (Sacramento, Yolo, El Dorado, and Placer Counties)

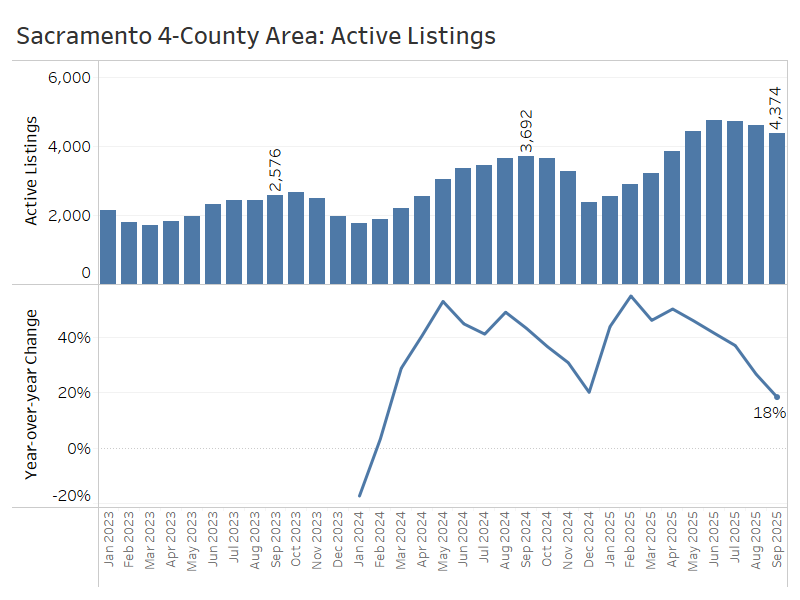

The greater Sacramento area has followed a similar trajectory to Portland, with market conditions gradually shifting in favor of buyers. Inventory has climbed, prices have cooled, and sales activity has remained relatively flat. That said, the pace of inventory growth has recently slowed, and home sales perked up in September, hinting at a possible shift in momentum.

At the end of September, there were nearly 4,400 active listings—an increase of 18% compared to the same time last year. However, the pace of inventory growth has slowed considerably since earlier in the year when year-over-year gains peaked at 55% in February.

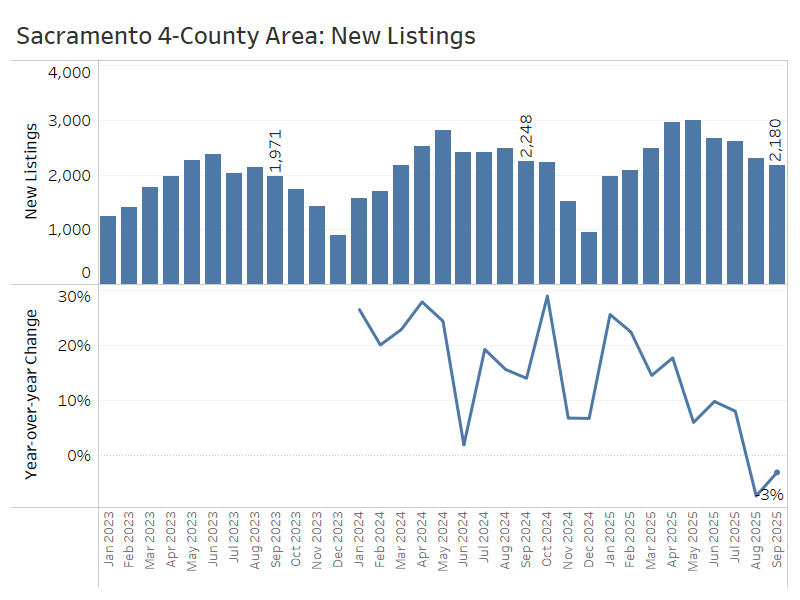

The flow of new listings has fallen below its year-ago pace for two months running now, with about 3% fewer new listings in September than last year.

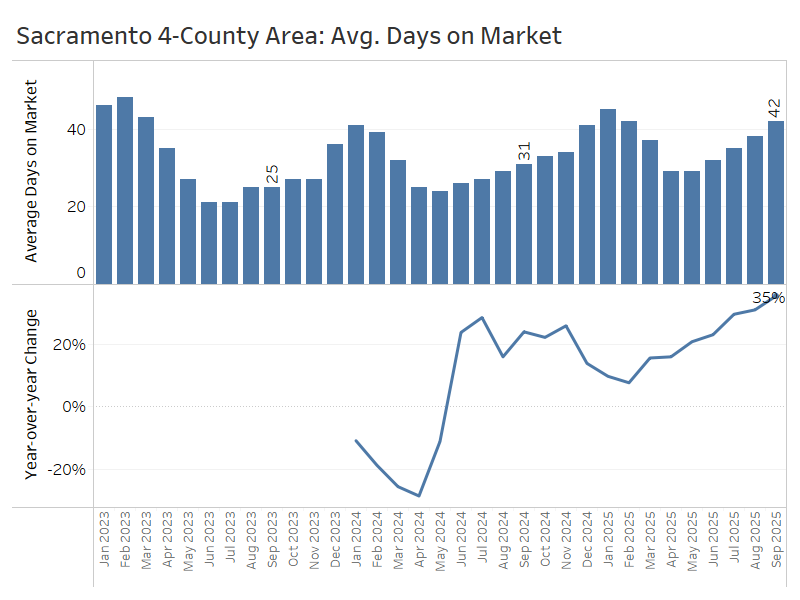

Average days on market rose by about 11 days compared to last year, reaching 42 days in September—a noticeable shift in how long homes are taking to sell.

After a period of solid sales growth in Q4 of 2024, the Sacramento region returned to low or negative growth through much of 2025. However, September saw a 12% year-over-year increase in sales, which might reflect a rebound from a weak August or aboost in buyers attracted to lower mortgage rates in the third quarter.

Median sale prices dipped 1%, from about $598,000 last September to $590,000 this year, after staying steady at almost exactly year-ago levels in July and August.

Third-quarter trends in the greater Sacramento area point to a market where rising inventory is finally putting modest downward pressure on prices, even as falling mortgage rates begin to draw some buyers back. That combination could result in an upturn in sales alongside flat price growth.

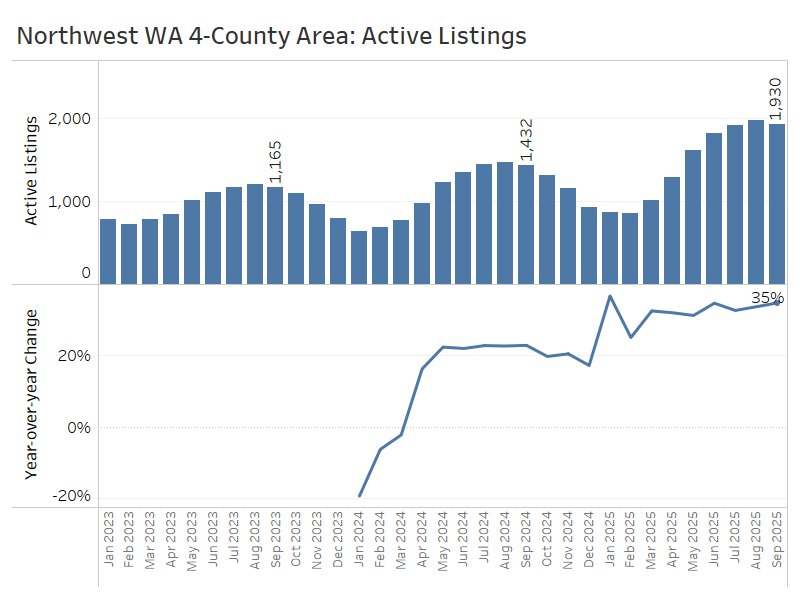

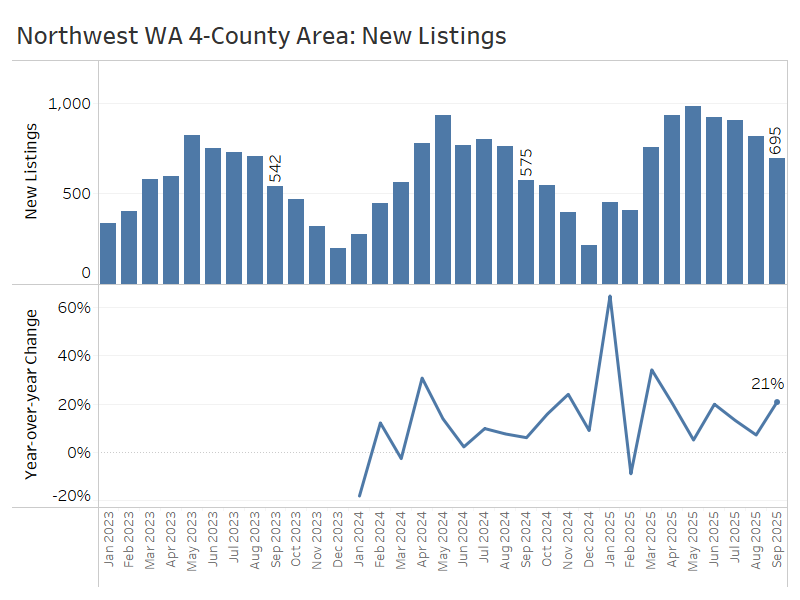

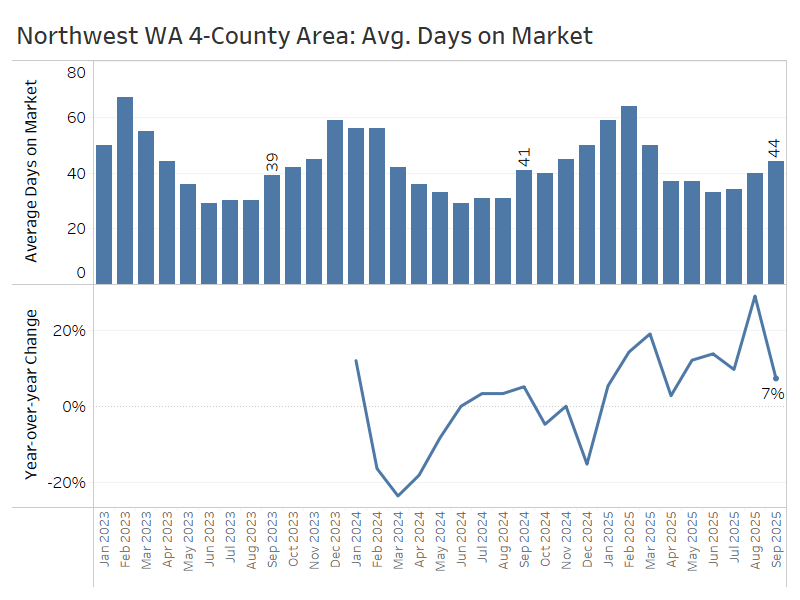

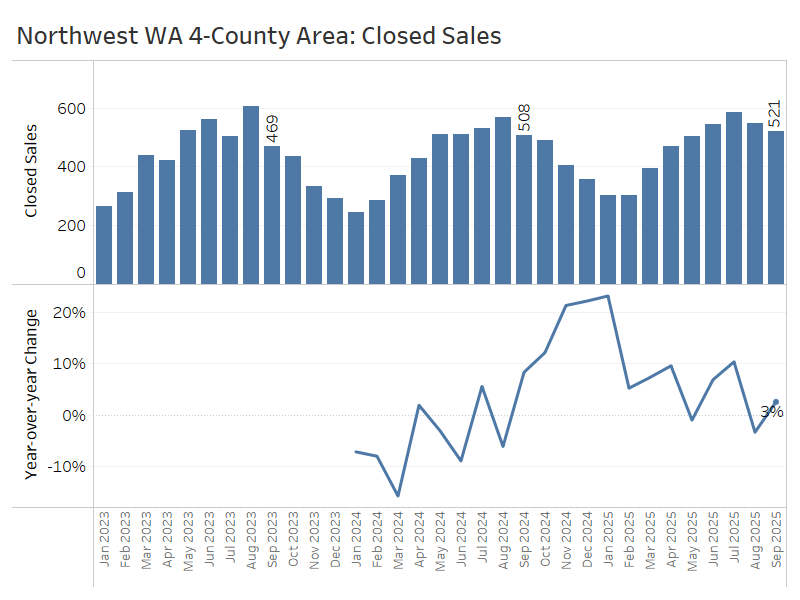

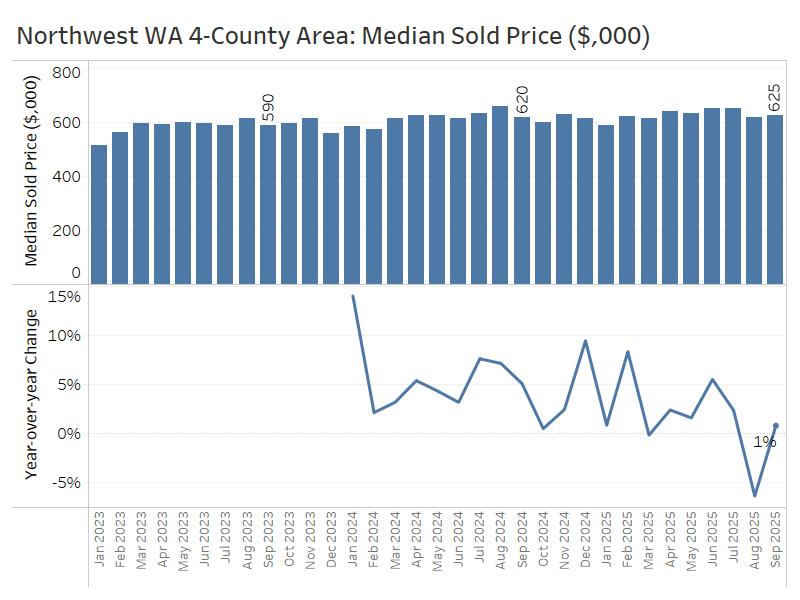

Northwest Washington – Skagit, Whatcom, San Juan, and Island Counties

North of the greater Seattle area, the market conditions in the four northernmost counties of the Puget Sound region are experiencing a major shift in buyers’ favor.

At the end of September, there were 1,900 active listings, up 35% from a year ago. There’s no evidence of a slowdown in inventory growth here, like that of the Seattle area this quarter.

The flow of new listings has experienced healthy growth throughout most of 2025, resulting in a 21% increase compared to September of last year.

Time on market has climbed modestly but steadily all year, now up to 44 days on average in September, up from 41 days last year.

Closed sales were up 3% year over yearin September, after a 3% dip in August and 10% growth in July.

Compared to the same time last year, median home prices rose 2% in July, dipped 6% in August, and then increased 1% in September to$625,000.

Looking ahead, priceswill likely cool as buyers take advantage of increased inventory and gain more negotiating power.

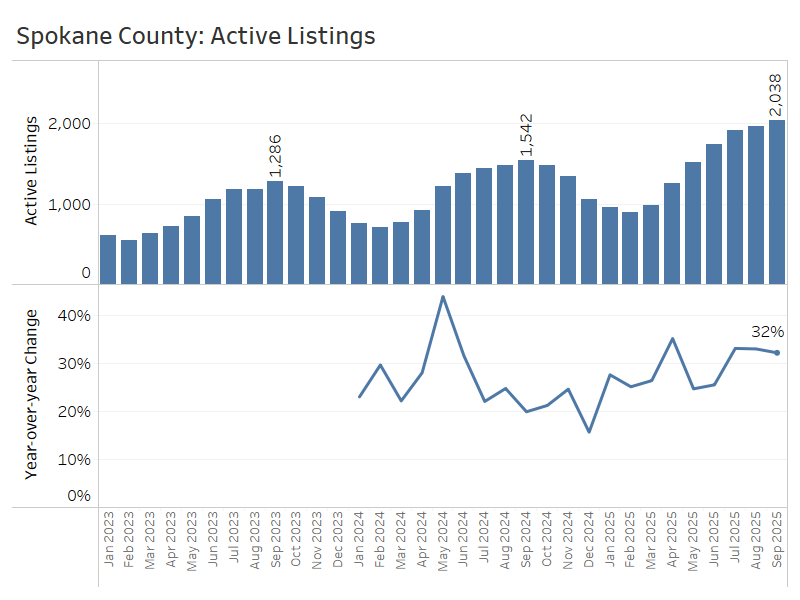

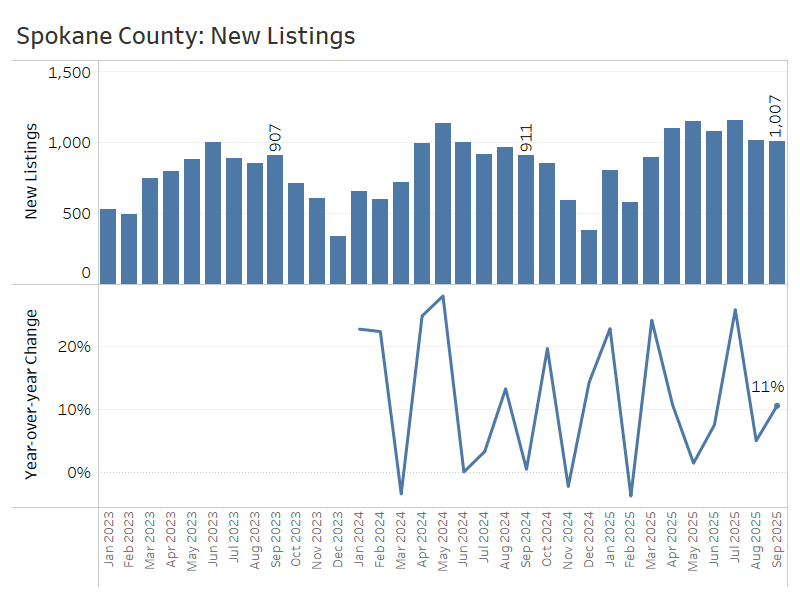

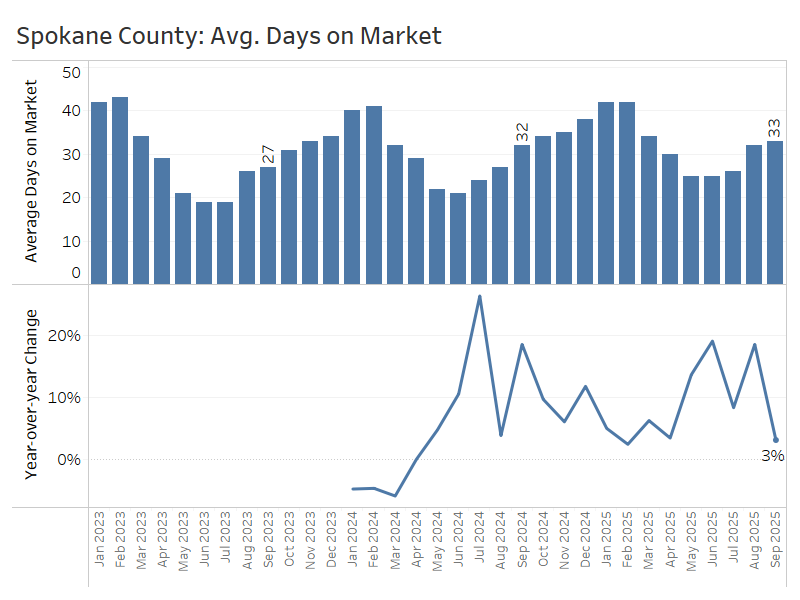

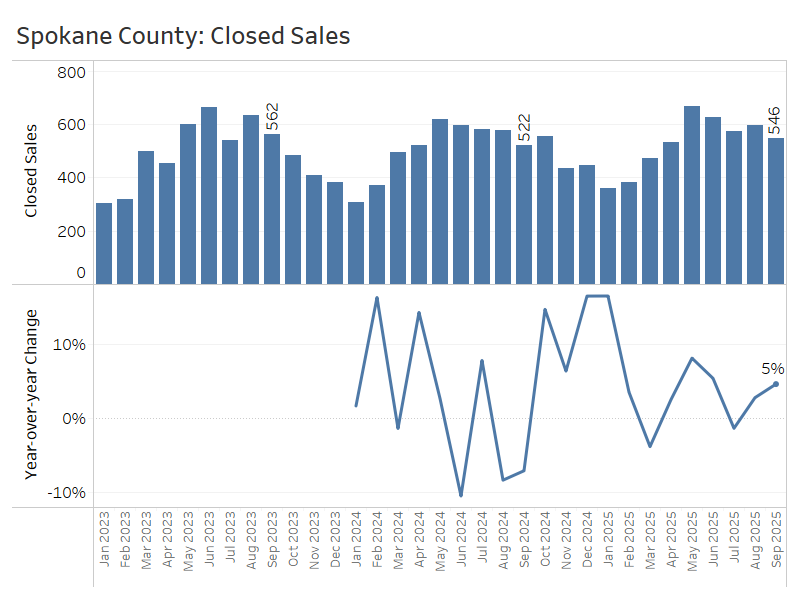

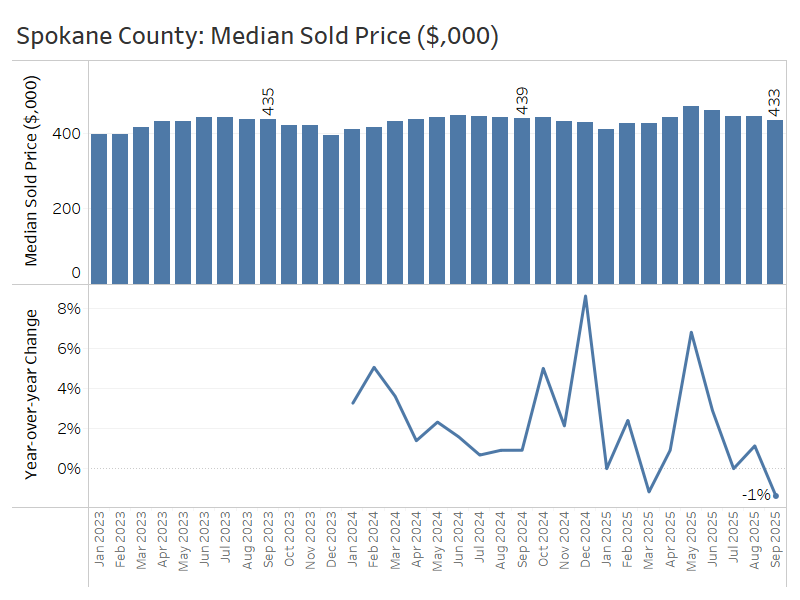

Spokane County, Washington

Spokane County, which anchors Eastern Washington, is experiencing many of the same market trends as Western Washington: higher inventory, softer buyer demand, and flat home prices.

At the end of September, there were just over 2,000 active listings, up 32% from a year ago and significantly higher than two years ago, when there were fewer than 1,300 listings. The pace of inventory growth has only slightly slowed from the 33% year-over-year increases we saw in July and August.

New listings climbed 11% from last September, after increasing 26% in July and 5% in August.

Unlike some of the other markets in this report, Spokane has seen only modest increases in the number of days it takes to sell a home, averaging 33 days this September, up from 32during the same time last year.

Closed sales in September were up 5% year over year, following a 3% increase in August and relatively flat sales in July.

Compared to last year, median sale prices in September dipped by about 1%, from $439,000 to $433,000. Prices were relatively flat yearoveryear in July and August.

Altogether, the more balanced market conditions in Spokane this summer began to yield more sales activity alongside flat to slightly lower prices—a healthy combination for the market right now.

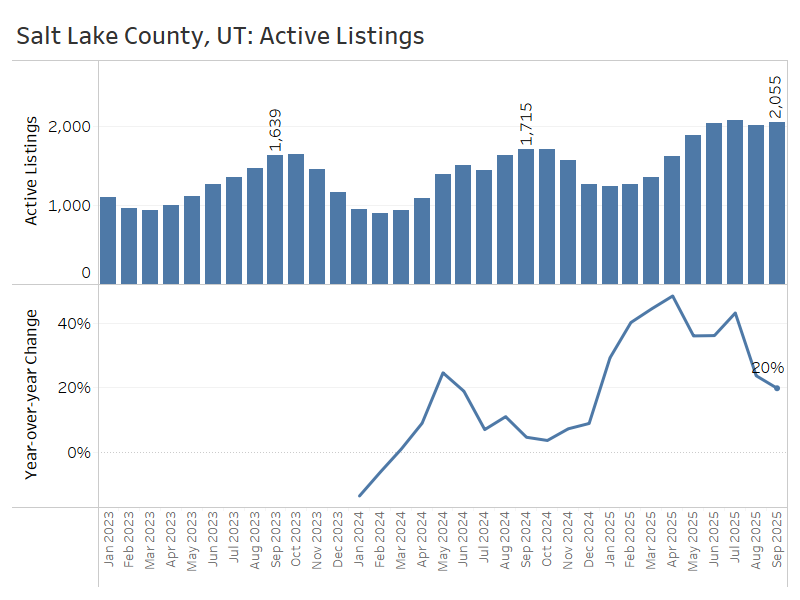

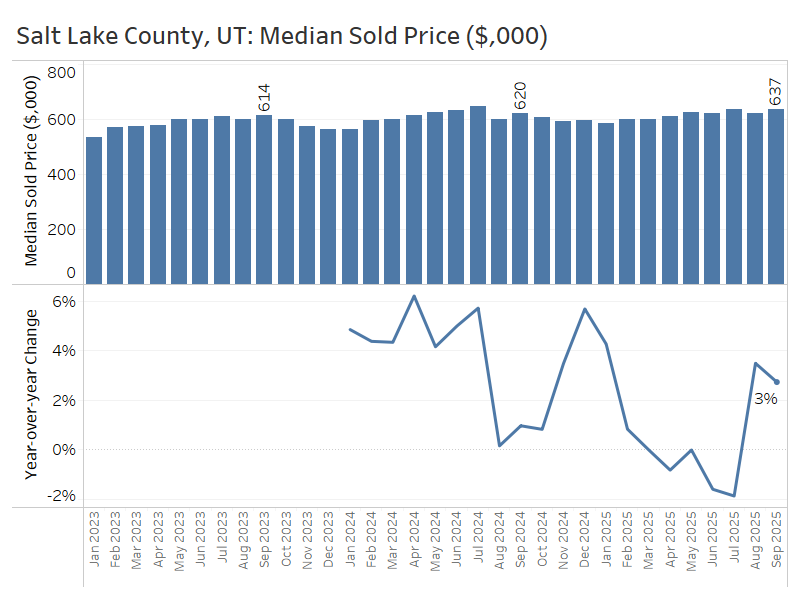

Salt Lake County, Utah

Earlier this year, Salt Lake County experienced an even sharper swing in buyers’ favor than the other markets in this report: higher inventory growth leading to modest price declines. Increasing sales growth in the third quarter shows that buyers have begun to take advantage of these conditions.

Active listings at the end of September stood at over 2,000 homes, up 20% from a year ago—a major slowdown from 43% inventory growth in July.

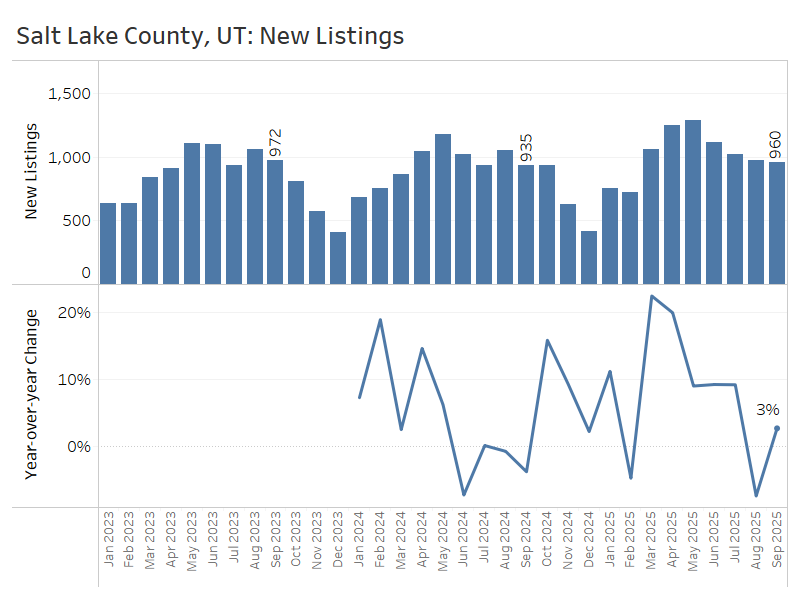

Salt Lake County saw substantial year-over-year growth in new listings earlier this spring, exceeding 20% in March and April, but only 3% growth in September. Selling enthusiasm seems to have faded this summer after the buildup of inventory in late spring.

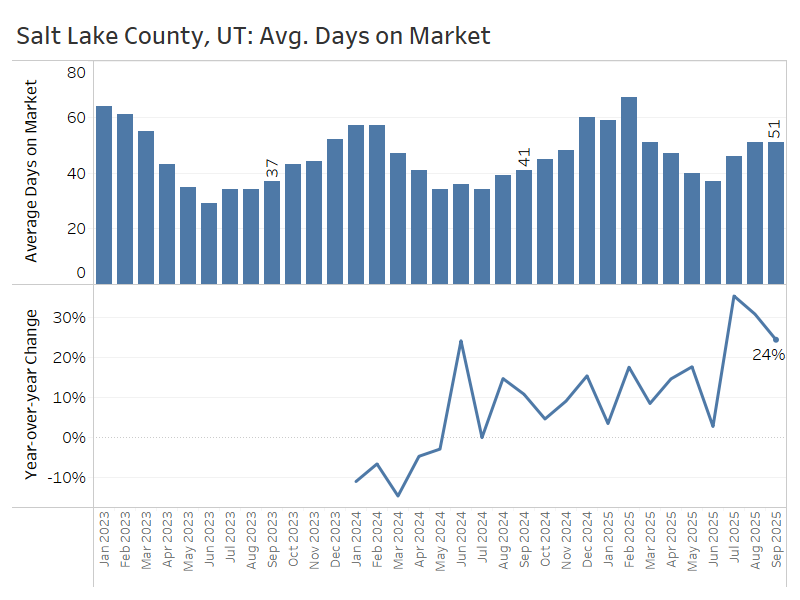

The average number of days it took to sell a home in Salt Lake County was up substantially throughout the third quarter, ending at 51 days in September compared to 41 days the previous year.

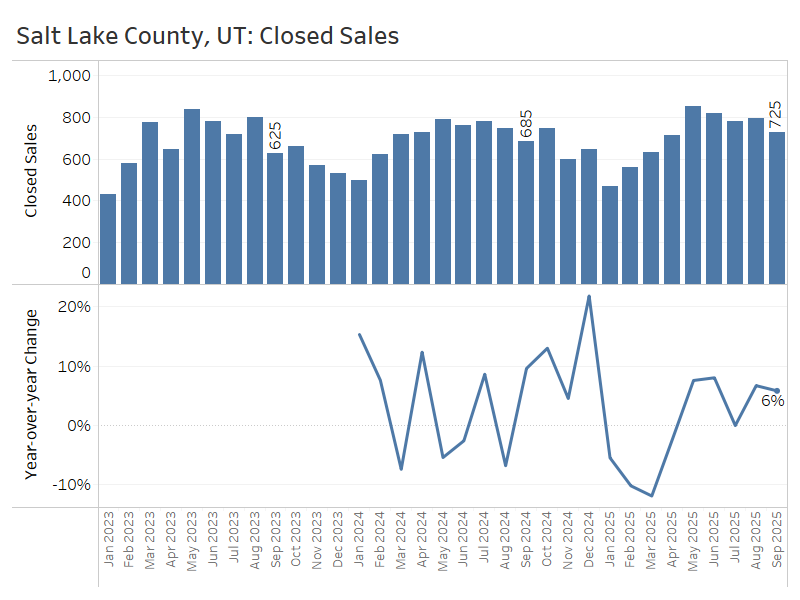

Closed sales climbed 6% from a year ago in September, after a 7% increase in August. This is a promising early sign that buyers are responding to improved inventory and mortgage rate conditions.

In September, the median sale price rose 3% yearoveryear—from $620,000 to $637,000. This uptick, along with August’s gain, broke a streak of modest price declines seen earlier in the summer.

All in all, Salt Lake County has begun to show a bit more balance after swinging in buyers’ favor earlier this year: inventory gains slowed down, and rebounding demand showed up in both rising sale counts and prices.

Conclusion:

All of the markets covered in this report have shifted into balanced or buyer-friendly territory, so it’s a good time to plan accordingly.

A consistent theme across the regions is the rise in inventory, paired with flat home sales and relatively flat prices compared to a year ago. This environment offers prospective buyers several advantages: more homes to choose from, greater leverage to negotiate, and less pressure to rush into a decision or compete in bidding wars.

For sellers, it’s important to be aware that the market has changed. Unlike the last several years, buyers now have more options, and home prices have leveled off. Success in today’s market depends on setting a realistic list price and presenting the home in its best possible light. With the right strategy, many homes are still selling quickly—and even above asking price—in every market highlighted in this report.

Sources: TrendGraphix analysis of NWMLS, RMLS, Spokane MLS, MetroList MLS, and Wasatch Front MLS data.

As Principal Economist for Windermere Real Estate, Jeff Tucker is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Jeff has over 10 years of experience as an economist at companies such as Zillow, Amazon, and AirDNA.

When it’s time to sell your home, one of the biggest questions is how to make it as appealing as possible to today’s buyers. While market conditions, location, and timing all play a role, the updates you choose before listing can make a meaningful difference in both your selling price and how quickly your home goes under contract. The key is knowing where to invest your time and money. Not every project pays off, but some smart upgrades can give your home a competitive edge, help it stand out in online listings, and create the kind of first impression that gets buyers excited.

Here are some of the most impactful ways to invest in your home before putting it on the market.

Fresh Paint and a Neutral Palette

Few improvements have a more substantial return on investment than paint. A fresh coat instantly refreshes a space, making it feel clean, updated, and well-maintained. Neutral tones for interiors, such as soft grays, light beige, and crisp whites, appeal to the broadest audience and allows buyers to envision their own style in the home. It’s crucial not to overlook trim, doors, and even ceilings, as these small details help create a polished, move-in-ready feel. And if your front door could use a pop of personality, consider a bold, welcoming color that complements the rest of the exterior.

Curb Appeal That Counts

Buyers often form an impression before they even step inside. Landscaping, exterior lighting, and simple maintenance go a long way toward making your home inviting. Think trimmed hedges, fresh mulch, pressure-washed walkways, and a tidy lawn. It’s also smart to ensure outdoor areas are safe, from repairing uneven paths to addressing any obvious hazards.

Adding planters with seasonal flowers, updating house numbers, or swapping out an old mailbox can elevate your home’s appearance without requiring a significant investment. For buyers scrolling through listings, that curbside charm can be a deciding factor that gets them to schedule a showing.

Kitchen and Bathroom Touch-Ups

Kitchens and bathrooms continue to be high priorities for buyers, but you don’t need to take on a full remodel to make an impact. Small upgrades like replacing outdated cabinet hardware, installing new light fixtures, or swapping in modern faucets can transform the look of these spaces.

In the kitchen, consider updating your backsplash with a clean, timeless tile or refreshing worn countertops with a durable surface. In bathrooms, regrouting tile, caulking any cracks, replacing mirrors, or updating vanities are simple ways to modernize without overspending.

Flooring Matters

Floors are often one of the first things buyers notice when touring a home. If your carpets are worn or stained, professional cleaning or even replacement can make a big difference. Hardwood floors are especially appealing and refinishing them is often more cost-effective than replacing them.

For areas where replacement makes the most sense, consider durable and stylish options like engineered wood or luxury vinyl plank. Consistent flooring throughout the main living areas can also help a home feel more spacious and cohesive.

Energy-Efficient Features

Today’s buyers are increasingly focused on efficiency and sustainability. Investments like LED lighting, programmable thermostats, and updated appliances not only lower utility bills but also signal to buyers that the home is modern and thoughtfully maintained.

If your budget allows, new windows or improved insulation can add value while appealing to environmentally conscious buyers. Highlighting these upgrades in your listing helps showcase both comfort and cost savings.

Decluttering and Staging

Sometimes the most impactful upgrade isn’t about new finishes, it’s about presentation. Decluttering each room, minimizing personal items, and rearranging furniture to optimize space can dramatically change how buyers perceive your home. And the best part? It’s completely free.

Professional staging takes this one step further, creating a warm and welcoming atmosphere that helps buyers envision living in the space. Even small touches, like fresh flowers, cozy throws, and well-placed artwork, can make your home feel more stylish, comfortable, and truly move-in ready.

Making Smart Choices

The goal of any pre-sale investment is to spend strategically, choosing projects that increase appeal without overextending your budget.

At Windermere, our agents are experts at helping sellers decide which upgrades matter most. From recommending paint colors to connecting you with trusted contractors, we’re here to make sure you get the best return on your investment. Through our Windermere Ready program, we can even front the cost of improvements like painting, landscaping, cleaning, and staging so your home shines its brightest when it hits the market. With concierge-level service and no payments due until closing, it’s a simple way to maximize your home’s value and sell faster.

Connect with an experienced Windermere agent today to learn more about how we can help you prepare your home for the market with confidence:

This is the latest in a series of videos with Windermere Principal Economist Jeff Tucker, where he delivers the key economic numbers to follow to keep you well-informed about what’s going on in the real estate market.

The Fed has finally started cutting. The two big questions are: Why? And now what?

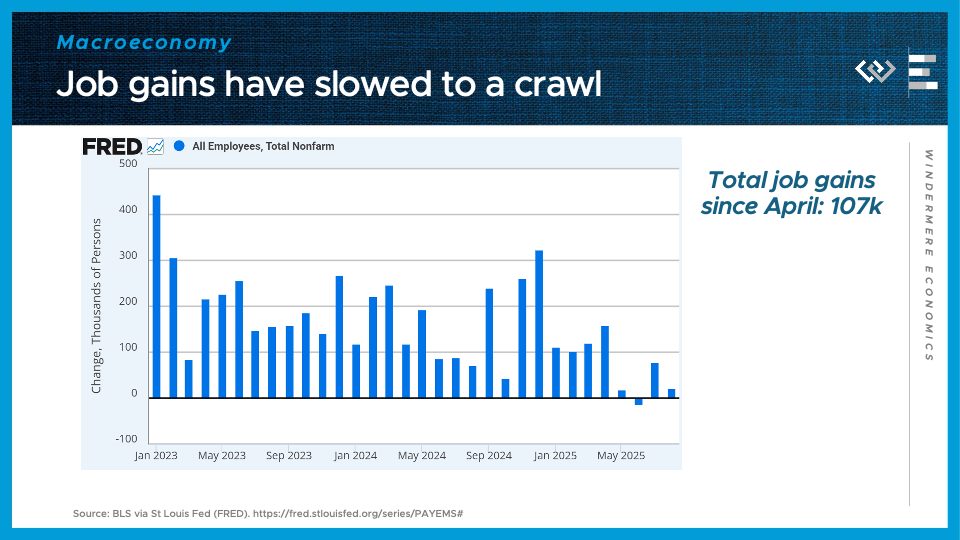

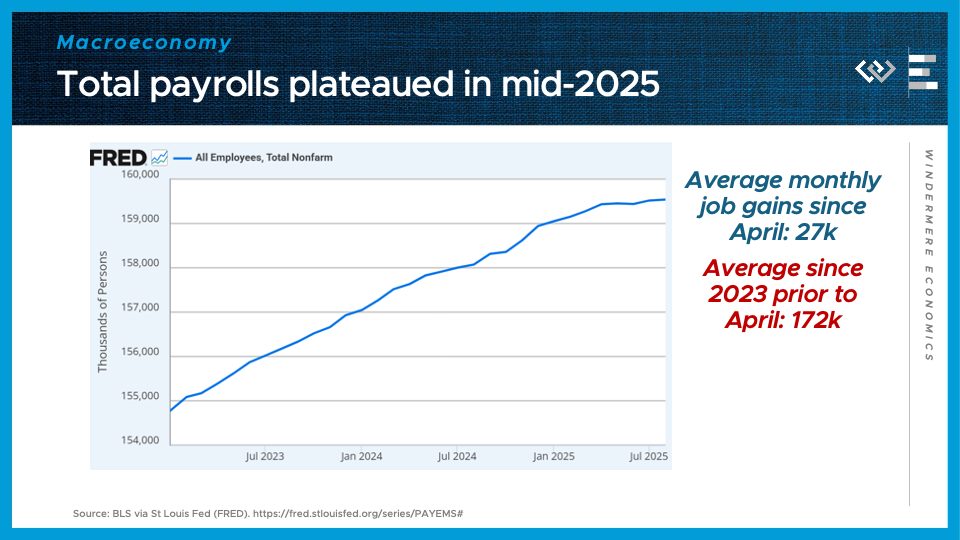

I’ll start with the why: the labor market has started showing signs of distress. The August jobs report delivered more bad news, continuing a streak of weak job growth since April.

The overall growth of nonfarm payrolls – the number of employed workers in the country – clearly passed a turning point this spring, as growth as slowed to a crawl.

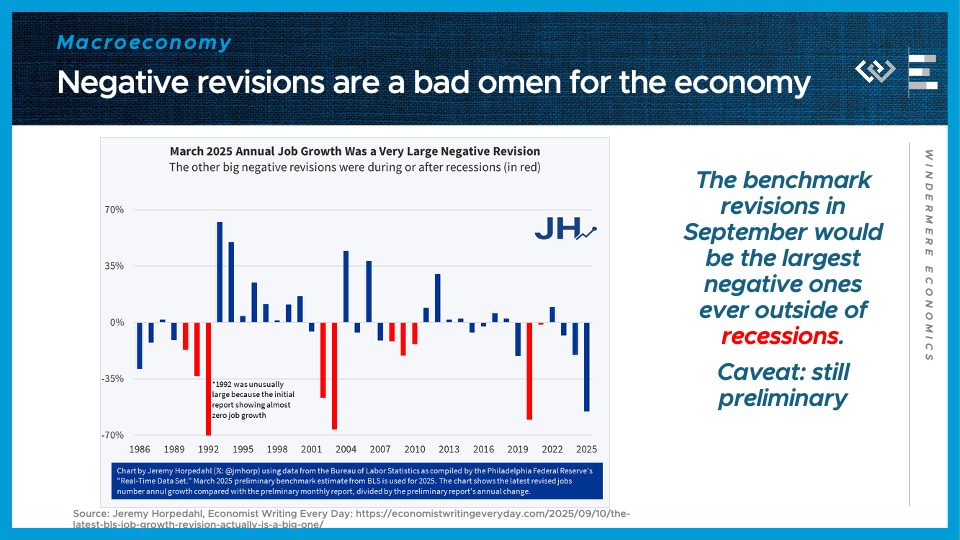

Moreover, the Quarterly Census of Employment and Wages just revised away more than HALF of the job growth previously estimated to have happened in the year ending March 2025, wiping out over 900,000 jobs originally thought to have been added in those 12 months.

Historically, as this chart by Jeremy Horpedahl highlights, big negative benchmark revisions, like the preliminary one released this month, have occurred during recessions. And big negative monthly revisions, like last month’s have been more common just before recessions.

That doesn’t mean a recession is around the corner, but it helps explain why the Fed is changing their posture to try to stop a recession before it gets going.

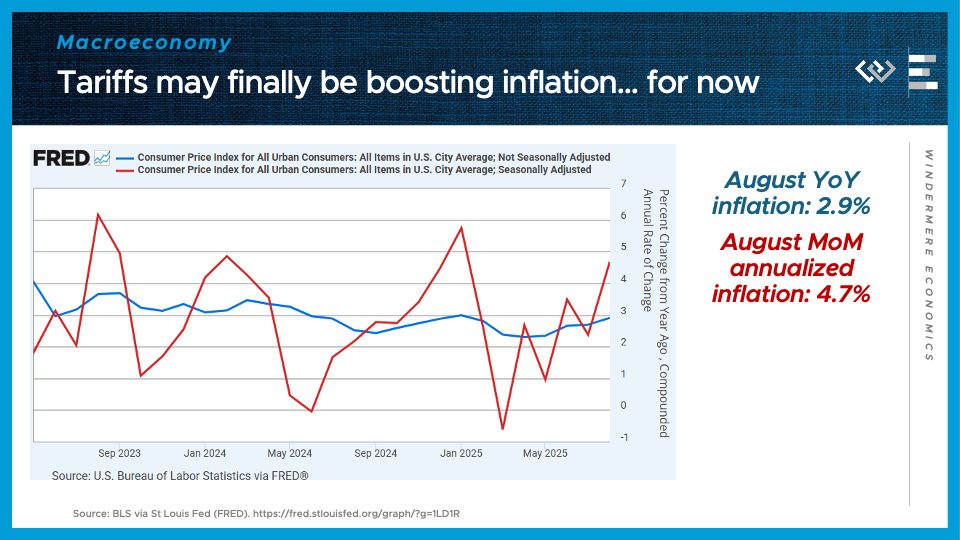

One challenge they’re facing, though, is that they have paused their fight against inflation before it was quite finished: annual inflation stopped falling this spring, and has now re-accelerated to nearly 3%; the more volatile monthly inflation rate is running at 4.7% annualized. Part of the reason the Fed is now willing to cut may be that they view some of this inflation as a transitory, one-time bump from tariffs, that they are willing to look through; but I think the biggest reason is just that the warning sirens in the labor market became too loud to ignore.

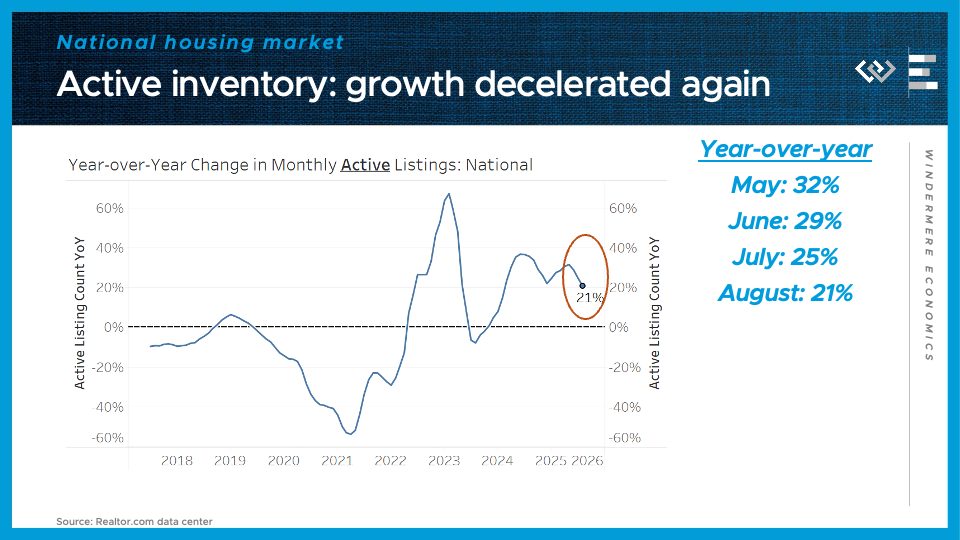

Turning to the housing market: the balance of power has swung in buyers’ favor this year, thanks to higher inventory, but it’s now clear that inventory growth passed an inflection point: for the third month in a row, the pace of growth of inventory has come down again. Now it’s down to just 21% growth from August of last year.

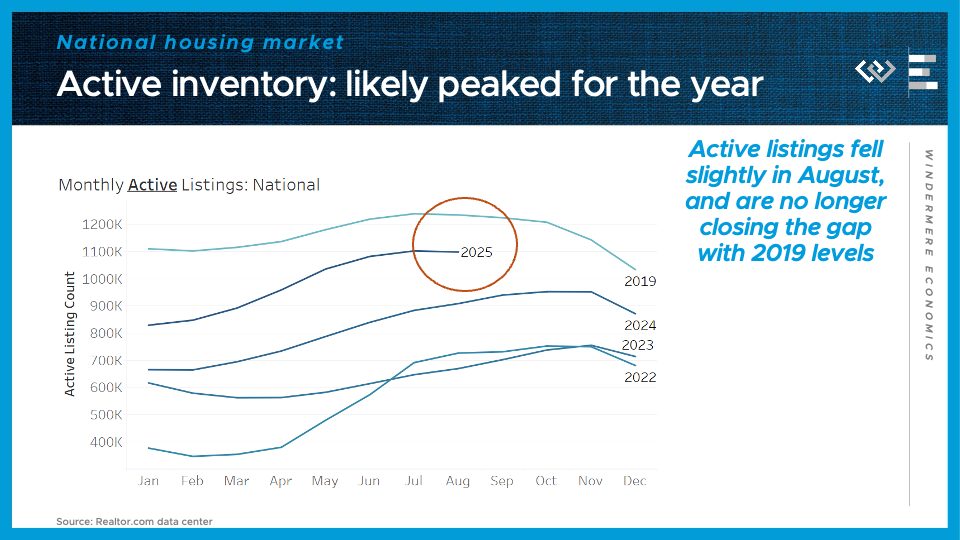

At the end of August, there were just under 1.1 million active listings on the market – down slightly from July, while each of the last 3 years saw inventory grow in August. This means buyers are still favored in many markets, but they can’t count on that pendulum to keep swinging further in their favor.

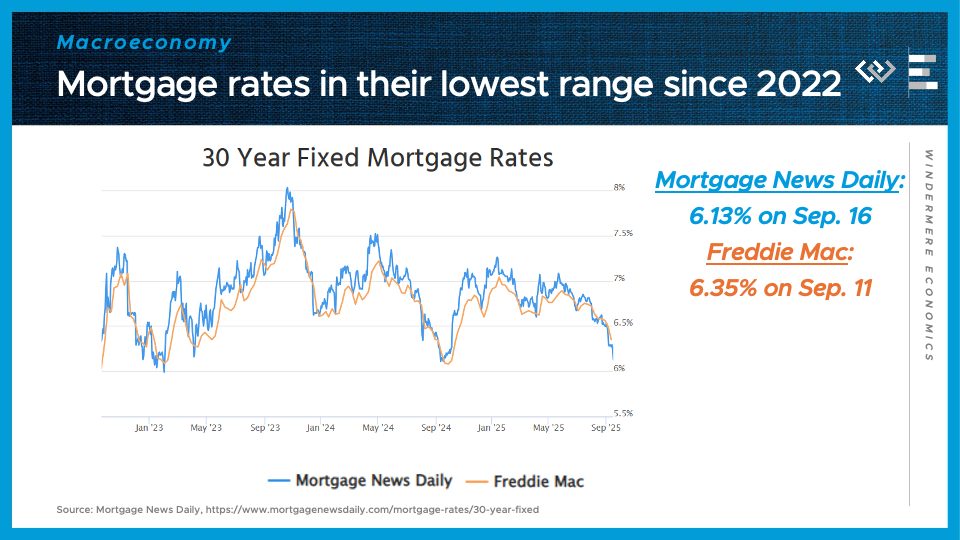

Especially because of the huge news for everyone in the housing market: mortgage rates have fallen to the neighborhood of 6 and an 8th percent, roughly their lowest level since 2022. Investors were anticipating this rate cut by the Fed, and if anything, the fact that the Fed was willing to press ahead with cutting rates, in spite of firmer inflation data, demonstrates their commitment to focus on helping the labor market with easier monetary policy, while setting aside inflation fighting to another day. Maybe more than anything, that change of posture by the Fed is helping to bring mortgage rates low enough that well-qualified borrowers are starting to see a 5-handle without paying any points. There’s no guarantee that the low rates will last – just look at what happened last October, so I’d advise everyone to strike while the iron’s hot. If rates do fall further this winter, well, you can always refi then.

Technology is transforming nearly every industry, and real estate is no exception. New tools and innovations are reshaping the way we search for, buy, and sell homes. Among these advances, artificial intelligence (AI) has quickly become one of the most talked-about technologies, being used for everything from writing and research to customer service. Naturally, this raises the question of whether it could ever replace jobs that rely on human connection and expertise, like real estate.

In the sections ahead, we’ll break down what AI can and can’t do in real estate, and how agents can use it to their advantage rather than view it as competition.

What is AI?

Artificial intelligence (AI) is technology that allows machines to simulate human intelligence. In recent years, AI has grown at lightning speed and has become part of daily life, often in ways people don’t even notice. Generative AI tools like ChatGPT, Copilot, Gemini, etc., are the ones most people hear about because they can answer questions, draft text, or create images. At the same time, other forms of AI are working quietly behind the scenes on websites, apps, and services we use daily, from recommendation engines to fraud detection.

Together, these tools are changing how we interact with technology, making it faster and more efficient. But when it comes to buying or selling a home, no algorithm can replace the insight, guidance, and personal care of a trusted real estate agent.

How AI is Shaping Real Estate

AI is already influencing how buyers and sellers approach the market. From predictive pricing tools and market analysis platforms to more intelligent home search engines, AI can process large amounts of data and provide insights more quickly than any individual could manage on their own. For agents, it can automate repetitive tasks like drafting emails or creating basic listing descriptions, while chatbots help answer simple client questions around the clock. Some platforms even use AI to match buyers with properties based on preferences or past behaviors. These tools save time and make processes more productive, but they’re only part of the real estate experience.

Why Real Estate Needs a Human Touch

Buying or selling a home is never just about the transaction—it’s often one of the biggest financial and emotional decisions of a person’s life. And while AI may provide quick data or market insights, it can’t sit down with an individual and understand their specific needs, calm their nerves during a stressful moment, or celebrate when the keys are finally handed over.

A real estate agent listens, adapts, and advocates for their clients in ways that no algorithm can replicate, bringing empathy, intuition, and lived experience into the equation rather than just facts and figures. They know the neighborhoods, the schools, and the subtle details that make a house a home. They can recognize when a client needs reassurance, when to negotiate a little harder, and when to suggest a creative solution to keep a deal moving forward. These instincts and skill sets are built on years of human connection, which is what makes the difference between simply completing a deal and guiding someone through a life-changing experience or helping them reach their real estate goals.

The Future: Agents + AI, Not Agents vs. AI

Rather than replacing real estate agents, AI has the potential to make their work even more impactful. Tools like virtual tours, AI-powered staging, and digital imaging can help buyers visualize a property in new ways, while automation can create marketing materials, streamline scheduling, and analyze market trends at an increased speed. These efficiencies free up time and energy for agents to focus on what matters most: listening to clients, building trust, and guiding them through one of life’s most significant decisions.

When used thoughtfully, AI shouldn’t be viewed as a competition, but as a business companion. By blending cutting-edge technology with the irreplaceable human touch, real estate agents can continue to grow their business, deliver better service, and strengthen the personal relationships that remain at the heart of every successful transaction.

At Windermere, our agents use every tool available, but it’s their expertise and personal care that truly set them apart. Connect with an experienced Windermere agent today:

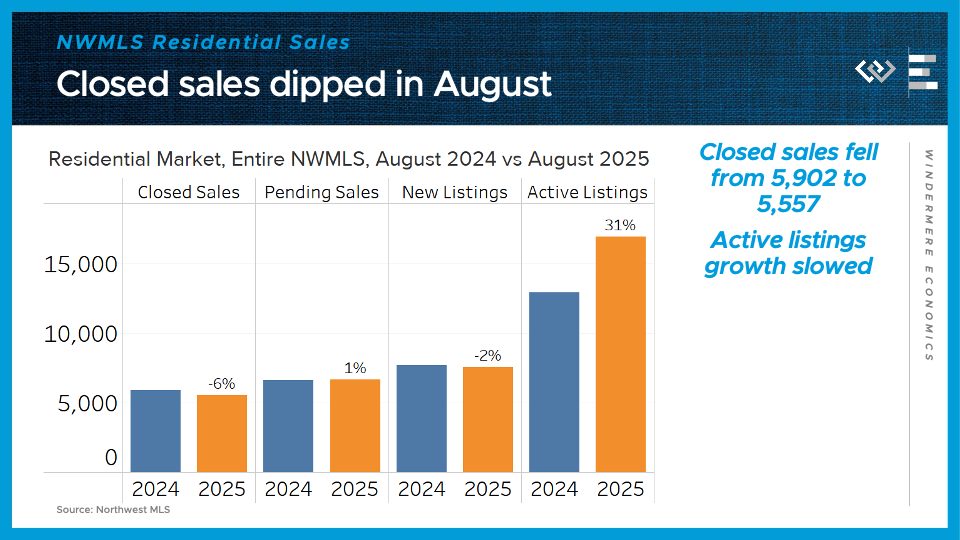

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the August 2025 data from the Northwest MLS.

This summer, the local market has decisively swung in buyers’ favor, as home sellers around Washington have had to contend with both softening demand, and more abundant competing listings. That’s good news for home buyers, but we are seeing fewer of them than we saw last year.

In August, closed sales of residential homes came in 6% below last year’s August total, across the Northwest MLS. Pending sales, which give some signal about next month’s sales, were roughly flat – up just 1% form last year.

On the supply side, we’ve passed an inflection point, where sellers are starting to back away from the market. There were 2% fewer new listings than last August – the first year-over-year decline in new listings since February. The month ended with 31% more active listings than last August, marking a slowdown from the inventory growth of about 36% the last two months. This pullback in supply should put a floor under any potential price decreases that the market shift could bring.

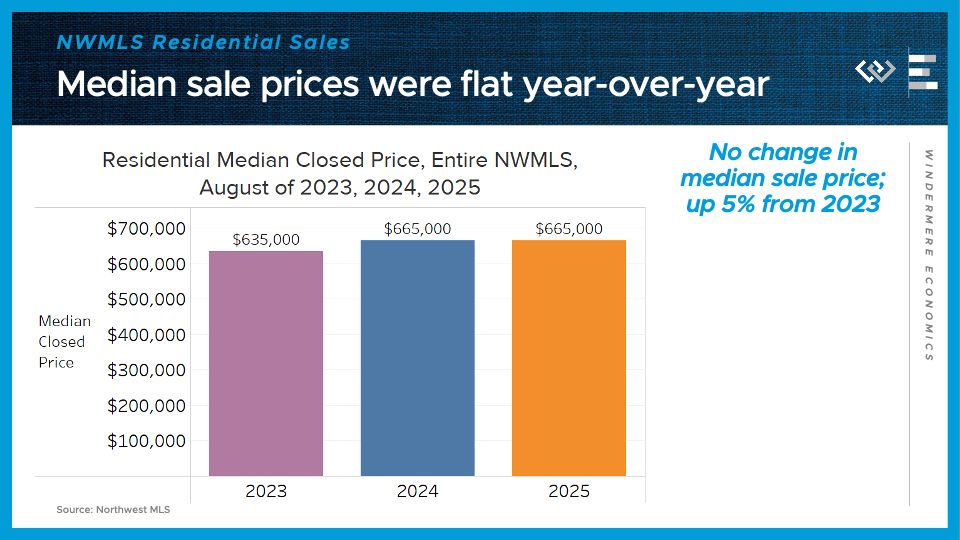

Speaking of which: the steadiest number across the Northwest MLS has been median sale price, which was exactly the same as last August: $665,000. That’s two months in a row of flat annual price changes, but it remains about 5% higher than in 2023.

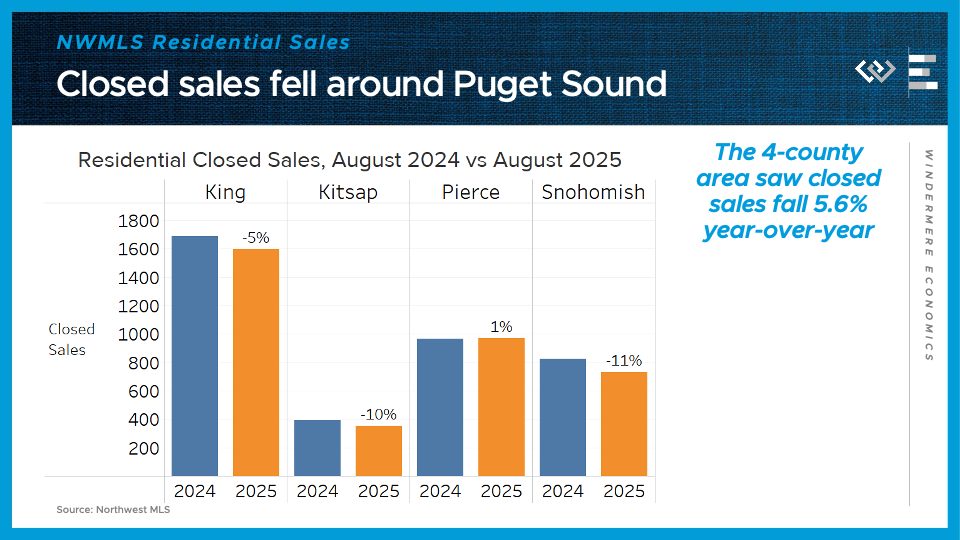

Now I’ll take a closer look at the four counties encompassing the greater Seattle area.

Closed sales dipped by almost 6% from last year. Only Pierce County saw a gain, albeit tiny, from last August.

Median sale prices actually crept upward from last year in all 4 counties: 4% higher in King; 7% higher in Kitsap, 1% higher in Pierce, and 1% higher in Snohomish County.

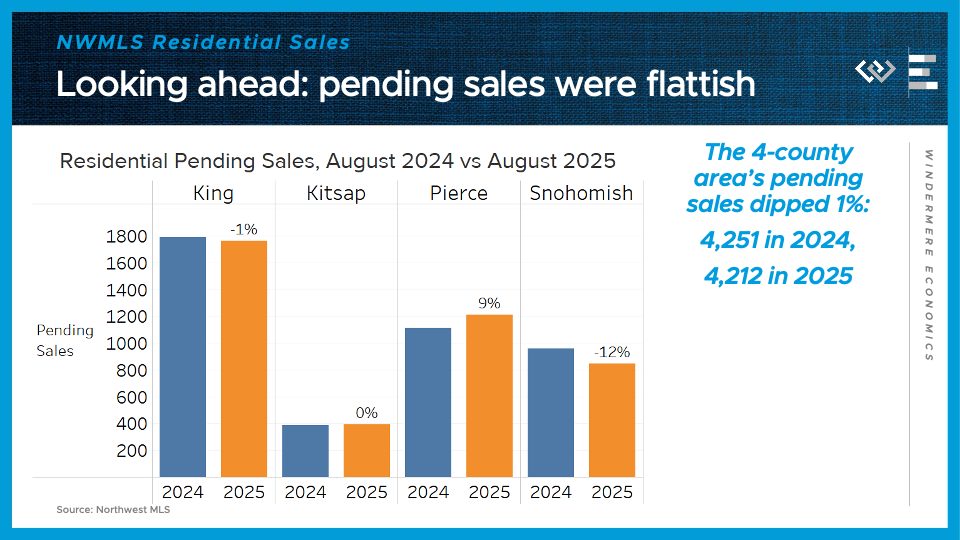

Looking ahead, pending sales dipped 1% across the region, although Pierce County was again the standout for sales, with 9% more pending sales than last year.

On the supply side, the 4-county greater Seattle area had 32% more active listings than at the end of August 2024. That continues the moderation of inventory growth we’ve seen since May, when this metric peaked at 45% year-over-year growth. King County especially has rebalanced, down from 50% growth to just 32% active listings growth.

Looking ahead, the key question is whether buyers begin to come off the sidelines in response to these more favorable conditions: they’ve got lots of inventory to choose from, listings that have lingered on the market, and mortgage rates that have dipped from about 7% to closer to 6.5% this summer. For people in a position to buy, this fall is looking like a sweet spot.

For Americans already struggling with the highest mortgage rates in a generation, new legislation out of Washington promises little relief. The “One Big Beautiful Bill Act” (OBBBA) will add trillions to the national debt over the next decades, further cementing an era of expensive borrowing.

The basic laws of supply and demand suggest this surge in government debt issuance will push interest rates even higher for everyone, straining the already-frozen housing market and increasing costs for all types of credit.

The one silver lining, though, is that the sooner lenders accept our “higher for longer” new world of interest rates, the sooner they can stop worrying so much about prepayment risk, which may shrink the spread they charge above 10-year Treasury yields. Below, we’ll explore how national debt impacts real estate.

As Uncle Sam borrows ever more, everyone’s interest rates will rise

The One Big Beautiful Bill Act, enacted this summer, puts the pedal to the metal for debt accumulation over the next decade in the U.S. The Committee for a Responsible Federal Budget estimates that it will add a cumulative $5.5 trillion to the debt by 2034, under the realistic assumption that its provisions written to expire will instead be extended, as has become normal in federal budgeting.

Even taking the expirations at face value, though, the bill raises deficits by a cumulative $4.1 trillion, an extraordinary choice in the midst of an economic expansion and coming on the heels of the worst bout of inflation in decades.

The issuance of trillions of dollars of additional debt in the next several years is expected to drive up interest rates. The Budget Lab at Yale has estimated that the bill will raise 10-year Treasury yields by about half a point in the next several years and by more than 1.4 points in the very long run.

This is driven in part by their modeling assumption that the Federal Reserve will succeed at keeping inflation close to 2 percent, which will require higher interest rates in the long run. They also expect a higher term premium on long-term debt, like 10-year Treasuries.

Altogether, this paints a picture of government borrowing crowding out private borrowing — as the Treasury issues more debt to finance its deficits, yields must rise to compensate investors. Other debt in the economy, such as mortgages, must yield more as well, in order to compete with Treasury bonds for lenders.

High interest rates have already frozen the housing market

While the U.S. economy continues to grow, the U.S. housing market has been stuck in neutral for over three years. Ever since mortgage interest rates rebounded from all-time lows below 3 percent for 30-year loans in 2020 and 2021, to generational highs above 7 percent in 2023, existing-home sales have been stuck in the neighborhood of 4 million annual sales.

It’s no surprise that fewer homes are changing hands than during the 2021 low-interest-rate boom, but 4 million is much fewer than even prevailed during the 2010s. In fact, 2024’s total of 4.06 million existing-home sales was the lowest total since the 1990s. The housing market is caught in a perfect storm, keeping homeowners frozen in place, thanks to the one-two punch of high price-to-income ratios and high mortgage rates.

While the OBBBA includes some sweeteners for certain homeowners, like the expansion of the state and local tax deduction cap to $40,000, the main long-term effect it promises for housing is just higher interest rates.

One near-term trend likely to help mortgage borrowers: a thinner spread

Bigger deficits, bigger debt, higher interest rates — the long-term fiscal outlook is getting darker. But there’s one silver lining that has begun to shine around the edge of these gathering clouds. The mortgage-Treasuries spread has begun to narrow again, resuming its progress back down toward pre-pandemic levels. The spread, here, refers to how much higher 30-year mortgage rates are averaging than 10-year Treasury yields.

In the 21st century, up to the pandemic, mortgage rates rarely exceeded 10-year Treasury yields by more than 2 percentage points, except during the global financial crisis. When mortgage rates soared back up in 2022, part of their climb was due to the widening spread. The two major reasons for widening spreads are a greater prepayment or refi risk on mortgages and interest rate volatility.

The latter has gradually faded this summer after spiking amidst tariff uncertainty in April. But the prepayment risk component is the bigger factor. For lenders and the investors who buy mortgage-backed securities, mortgages issued at high interest rates are uniquely risky because borrowers are expected to refinance them once mortgage rates fall back down.

The lack of a prepayment penalty for borrowers makes U.S. mortgages uniquely favorable to homebuyers here. If rates rise, they win by virtue of having locked in a lower rate; if rates fall, they can always refinance. Investors and lenders, by the same token, view refinancing as a unique downside to holding mortgages. They want a reliable coupon stream from mortgage holders’ monthly payments.

Seeing their loans wiped out by refinancing, replaced by cash in a new lower-interest-rate world, is a risk for which they must be compensated to make the loan in the first place.

That extra compensation for prepayment risk helped explain why mortgage rates soared even more than 10-year Treasury yields in 2022 and 2023. Now, though, as the reality sets in that we are living in a world where interest rates are “higher for longer,” lenders have gradually brought mortgage rates down relative to Treasuries, from about a 2.9-point spread in 2023 to 2.4 in recent months, or about one-third of the way back to normal.

The sooner investors conclude that refinancing prepayment risks aren’t so high, the sooner the spread can come down. The potential bankshot silver lining of the OBBBA? By putting a nail in the coffin of hopes for low interest rates, it may help further shrink the spread, so that higher 10-year Treasury yields don’t have to mean higher mortgage rates one-for-one.

Ultimately, the nation’s fiscal path points toward a new normal of higher borrowing costs for all. The “One Big Beautiful Bill Act” serves as an accelerant, solidifying a “higher for longer” interest rate environment that will impact everything from car loans to corporate debt. For the beleaguered housing market, this presents a bittersweet trade-off.

The bad news is that the foundational interest rate, the 10-year Treasury yield, is set to climb. The paradoxical good news is that by killing the hope of a return to ultra-low rates, the OBBBA may continue to shrink the risk premium lenders charge on mortgages. This narrowing spread won’t turn 7 percent mortgages back into 3 percent loans, but it might help us work our way back down closer to 6 percent.

Jeff Tucker is the Principal Economist at Windermere Real Estate in Seattle, WA. This blog was originally published on Inman News on 8/26/25.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

")