Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Hawaii/Maui Real Estate Market Update

The following analysis of select Maui real estate markets is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

COVID-19 continues to significantly impact employment on Maui, causing the loss of 23,000 jobs between February and September. That said, although it really is no consolation, employment has risen by 900 jobs from the low in May. The mandatory 14-day self-quarantine proclamation introduced by Governor Inge has been replaced with a pre-travel testing option. Hopefully this will lead to increased tourism, which is the backbone of Maui’s economy. The unemployment rate on the island hit a very high 35.8% in April. This has dropped to the current rate of 24%, which is still high. I will temper enthusiasm about this improvement by saying that much of the decline was due to a significant reduction in the labor force. All of the Hawaiian Islands are suffering, but a bottom in employment has been reached. That said, I am not holding out any hope of significant job recovery until next year when a vaccine is freely available—and being used.

HOME SALES

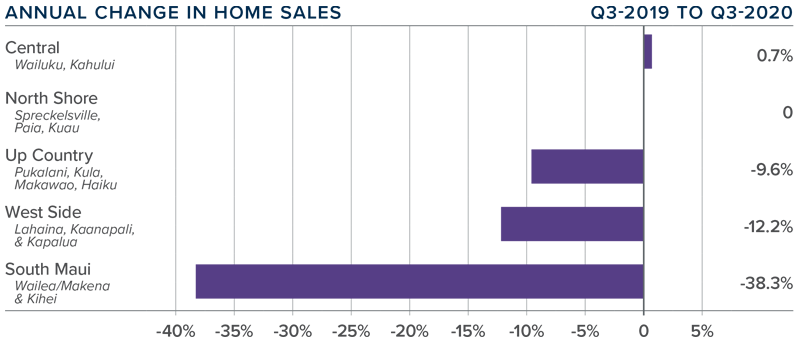

❱ In the third quarter of 2020, 487 homes sold, a drop of 19.8% compared to the same period a year ago, but 36.8% higher than in the second quarter of this year.

❱ Sales did rise in the Central area, but the increase only amounted to one additional sale. The largest drop in sales was again in South Maui, where 98 fewer transactions closed compared to a year ago.

❱ Listing activity rose 14.7% compared to the same quarter in 2019 and was 10% higher than in the second quarter. This increase in the choice of homes for sale appears to have helped increase sales from the second quarter.

❱ Pending home sales were 2.2% lower than a year ago but they were a significant 49.3% higher than in the second quarter of this year. This means closings in the final quarter will likely be positive.

HOME PRICES

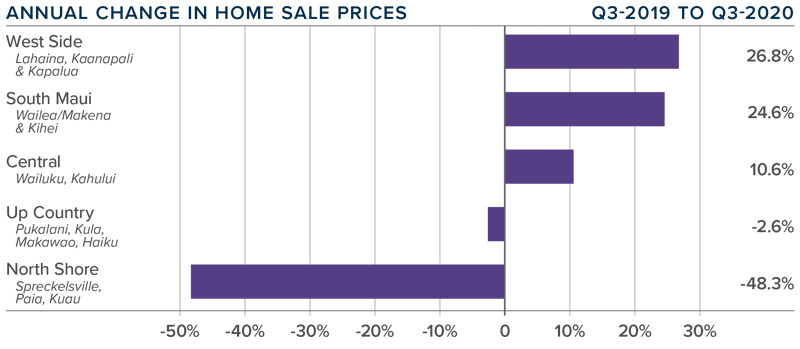

❱ As we saw in the second quarter, the average home price on the island rose 14.7% from last year to $1,030,000 and was 5.7% higher than in the second quarter of this year.

❱ Affordability is still a significant issue, but prices continue to appreciate. It is possible that buyers from the mainland are seeking out alternatives to traditional hotel or rental home vacations and are choosing to buy instead.

❱ Price growth was a mixed bag, with prices rising in three areas and dropping in two. The Westside and South Maui saw significant price growth, but the North Shore market experienced a major price drop. I am not particularly concerned about this as it is a very small area.

❱ The takeaway here is that price growth was very positive regardless of the economic issues that persist.

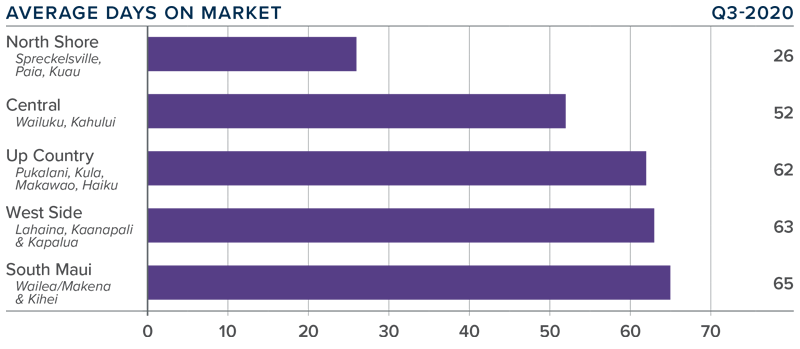

DAYS ON MARKET

❱ The average number of days it took to sell a home on Maui dropped 18 days compared to the third quarter of 2019.

❱ The amount of time it took to sell a home dropped in the Westside, North Shore, and Up Country but rose in all other areas.

❱ In the third quarter, it took an average of 54 days to sell a home, with North Shore homes selling at the fastest pace. It is taking the longest time to sell in South Maui.

❱ Market time not only dropped relative to a year ago, it also took 16 fewer days than in the second quarter. This is positive and shows there is demand from buyers.

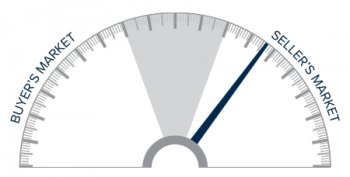

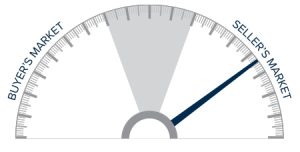

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

Unsurprisingly, the island is still reacting to the influences of COVID-19. Demand, although down from a year ago, was up relative to the second quarter, which is good. The pandemic will continue to influence the direction of the housing market and, as I suggested would be the case in the second quarter Gardner Report, there does appear to be some sort of return to a more normal market.

Price growth was significant, and sales rose in the quarter. As such, I am moving the needle back a little more in favor of sellers.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Big Island of Hawaii Real Estate Market Update

The following analysis of the Big Island real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

COVID-19 continues to significantly impact employment on the Big Island, causing the loss of 13,000 jobs between February and September. That said, although it really is no consolation, employment has risen by 900 jobs from the low in May. The mandatory 14-day self-quarantine proclamation introduced by Governor Inge has been replaced with a pre-travel testing option. Hopefully, this will lead to increased tourism, which is the backbone of the Big Island’s economy. The unemployment rate on the island hit a high of 23.4% in April. It has dropped to the current rate of 13.6%, which is still quite high. I would also note that the rate would have been higher had the island not seen a significant reduction in the labor force. All of the Hawaiian Islands are suffering, but a bottom in employment has been reached. That said, it will be a long slog to get back to the employment levels of early spring.

HOME SALES

❱ In the third quarter of 2020, 890 homes sold on the Big Island, an increase of 6.7% compared to the third quarter of 2019, and a significant 52.9% higher than in the second quarter of 2020.

❱ Sales were higher in six markets, were static on one, and fell in two. Kau, South Kona, and North Kohala all saw significant increases in sales and the markets where sales were lower only experienced small losses on an absolute basis.

❱ The growth in sales came even as inventory levels dropped 24.2% from a year ago. The average number of homes for sale in the quarter was also down 15.7% from the second quarter of 2020.

❱ Pending home sales jumped 49.3% from the second quarter, suggesting that closed sales will be positive in the final quarter of the year.

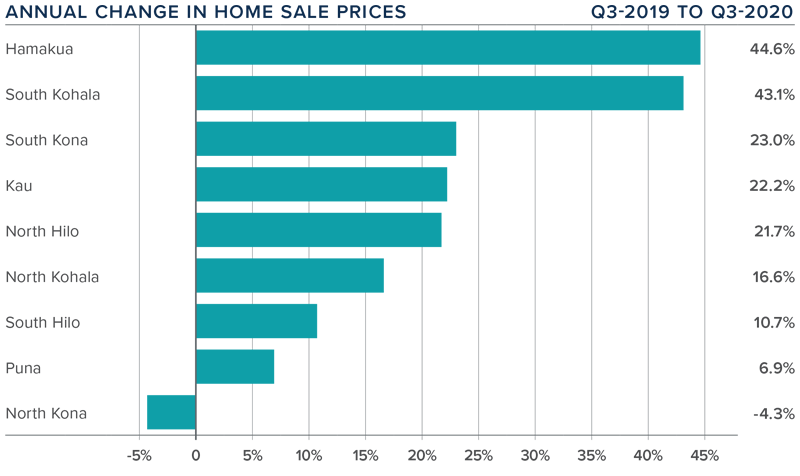

HOME PRICES

❱ The average home price on the island rose an impressive 8.1% year over year to $629,751. Prices were also 8.8% higher than in the second quarter of 2020.

❱ Affordability remains an issue, but there appears to be demand from locals as well as mainlanders. Buyers have dipped their toes back into the market. This is likely due to very competitive mortgage rates, as well as people seeking out alternatives to traditional hotel or rental home vacations and choosing to buy instead.

❱ Prices rose in every market other than North Kona. Appreciation was strongest in the Hamakua market area. In areas that saw market growth, all but one of them experienced double-digit increases.

❱ The market has improved, and I am hopeful this will continue with the easing of travel restrictions.

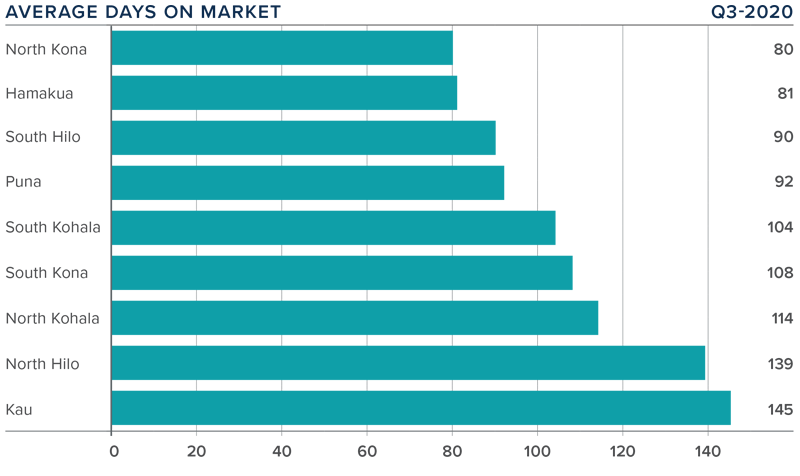

DAYS ON MARKET

❱ The average time it took to sell a home on the Big Island dropped eight days compared to the third quarter of 2019.

❱ The amount of time it took to sell a home dropped in North Hilo, North Kohala, and Kau, but rose in all other markets.

❱ In the third quarter, it took an average of 106 days to sell a home. Homes sold fastest in North Kona and slowest in Kau.

❱ It took 14 fewer days to sell a home in the third quarter than in the second quarter of this year.

CONCLUSIONS

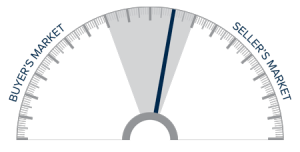

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

Unsurprisingly, the island is still impacted by the influence of COVID-19. Demand has improved and I remain hopeful that lowered travel restrictions will allow Island sales to continue to improve.

Increased demand and a low supply of homes for sale has allowed prices to rise at a very decent pace. As such, I am moving the needle back a little more in favor of home sellers.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

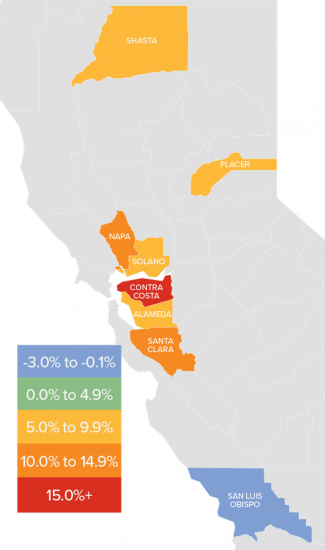

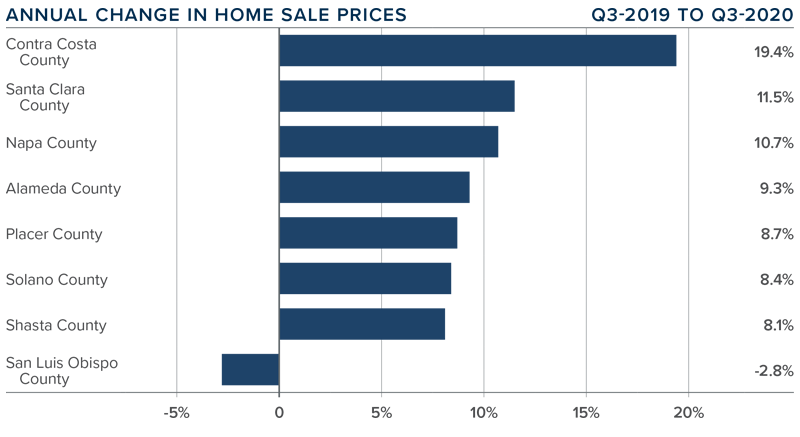

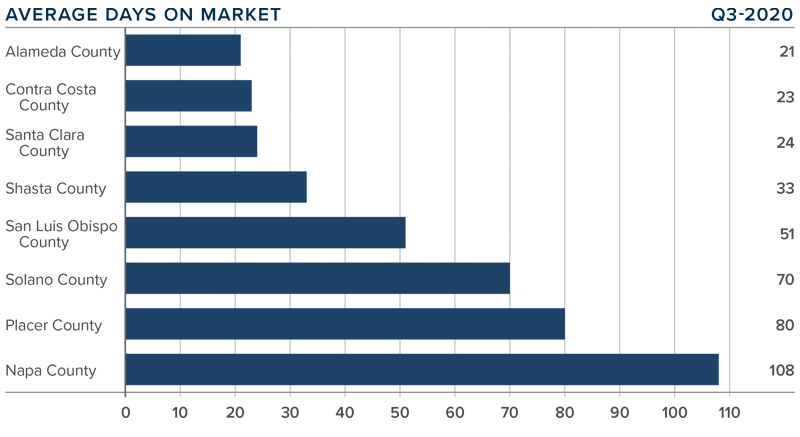

Northern California Real Estate Market Update

The following analysis of the Northern California real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

We are certainly seeing some “green shoots” in the regional economy, but employment levels across the Northern Californian counties contained in this report remain well below where they were before COVID-19 hit. The region shed more than 432,000 jobs between February and May, but it appears as if we have turned the corner: preliminary data for September shows the region has recovered over 162,000 of those lost jobs. Even though jobs are returning, close to a quarter of a million people are still looking for work. It is, therefore, unsurprising to see the unemployment rate remain elevated at 8.3%, up from 3% in February. By county, the lowest jobless rate was in Santa Clara County (7%) and highest in Solano County (9.7%). The economy is recovering, and it appears as if new COVID-19 cases in the state are leveling out. However, some counties in Northern California appear to be doing better than others. Additionally, the state’s wildfires—although mostly contained—are still likely to act as headwinds to a complete economic recovery.

HOME SALES

❱ In the third quarter of 2020, 14,800 homes sold, an increase of 14% compared to the third quarter of 2019. I was pleased to see a significant recovery from the second quarter of this year

as well, as sales rose a notable 62.2%.

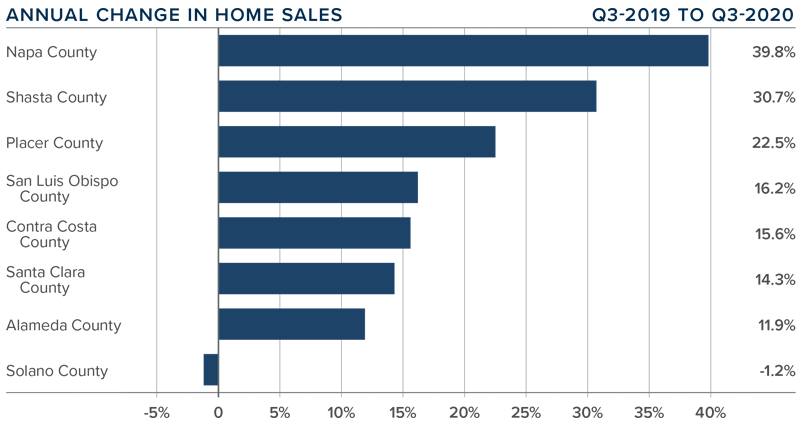

❱ Year-over-year sales were positive in all counties other than Solano, although the drop there was very modest. The largest increase in sales was in Napa County, which was a little surprising given its exposure to the Hennessy Fire.

❱ Listing activity was down 32.1% compared to the third quarter of 2019, and came in 12.5% lower than in the second quarter of this year.

❱ It was also encouraging to see pending home sales in the quarter rising significantly (42.7%) compared to the second quarter, which tells me that closings in the final quarter of the year will be positive.

HOME PRICES

❱The average home price in the Northern Californian counties contained in this report rose 12.7% year-over-year to $1,029,000.

❱The average home price in the Northern Californian counties contained in this report rose 12.7% year-over-year to $1,029,000.

❱ The most affordable counties in terms of average sale prices were Placer and Solano. Price growth in these markets was very solid, but we also saw significant price increases in the more expensive counties.

❱ Average prices rose in all but one of the counties contained in this report. There was a small drop in San Luis Obispo County, reversing the impressive increase that this county saw last quarter.

❱ Home price growth is a function of supply and demand. Supply levels, which increased in the second quarter, have pulled back and it appears as if solid demand has pushed prices significantly higher.

DAYS ON MARKET

❱ The average time it took to sell a home in the Northern Californian counties covered by this report rose four days compared to the third quarter of 2019.

❱ The amount of time it took to sell a home dropped in six counties but rose in Napa (34 days) and Solano (25 days).

❱ In the third quarter, it took an average of 51 days to sell a home, with homes selling fastest in Alameda County and slowest in Napa County.

❱ The greatest drop in market time was in Contra Costa County, where it took seven fewer days to sell a home than in the third quarter of 2019.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

I was pleased to see jobs returning in reasonable numbers, and buyers—likely buoyed by very attractive mortgage rates—returning to the market. That said, listing activity was underwhelming, and this is likely part of the reason for the significant price growth.

If COVID-19 cases slow further and the forest fires are extinguished, I see no reason why the market cannot continue to improve. Because of these factors, I am moving the needle a little more in favor of home sellers.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Nevada Real Estate Market Update

The following analysis of the greater Las Vegas real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

COVID-19’s massive impact on jobs has started to taper, but the market is still a long way from a full recovery. Las Vegas shed almost 247,000 jobs in only two months, but more than 118,000 of them have returned. Naturally, the Leisure & Hospitality sector was significantly impacted, but I am pleased to report that well over half of those 136,000 lost jobs have now returned. With major declines in employment, it was not surprising to see the unemployment rate rise from 3.9% in February to 34% in April. Given the return of a significant number of jobs, the rate in September came down to 15.5%. The market still has a long way to go to get back to where it was pre-COVID, but the improvement is palpable. Although it is certainly too early to say we are out of the woods, the direction the economy is heading is positive. That said, COVID-19 infection rates in Nevada started increasing in June and that may slow the economic recovery if the direction is not reversed.

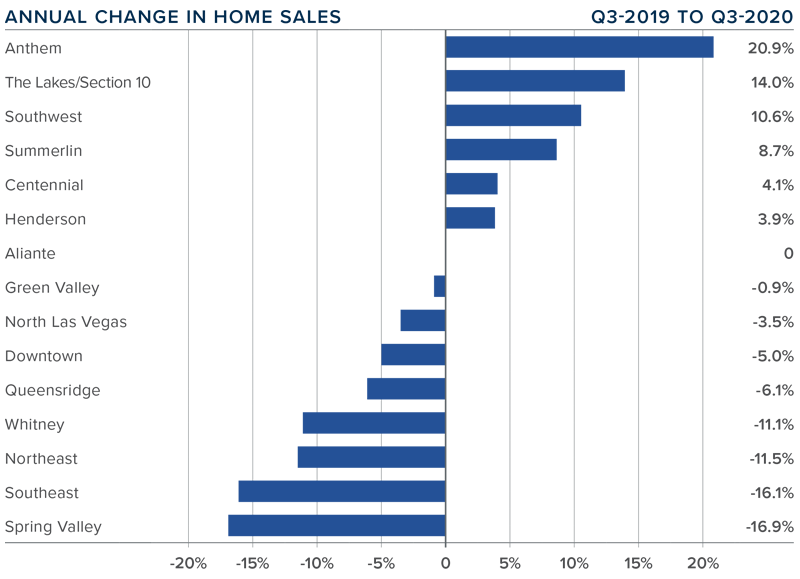

HOME SALES

❱ A total of 9,515 homes sold in the third quarter of 2020. This was an increase of only 0.9% compared to the same period a year ago, but a significant 56% higher than in the second quarter of 2020.

❱ Pending sales jumped 33.6% over the second quarter, suggesting that faith in the market is returning, which bodes well for closings in the fourth quarter.

❱ Sales rose in six markets, were static in one, and dropped in eight. The Anthem area saw significant growth, but this increase was offset by lower sales activity in the Spring Valley and Southeast Las Vegas markets.

❱ Listing activity was down 11.9% from the second quarter of the year and down 31.9% compared to a year ago. This is not encouraging. Listings will likely remain relatively muted until a vaccine is available, and the Las Vegas economy gets back to as close to normal as is achievable.

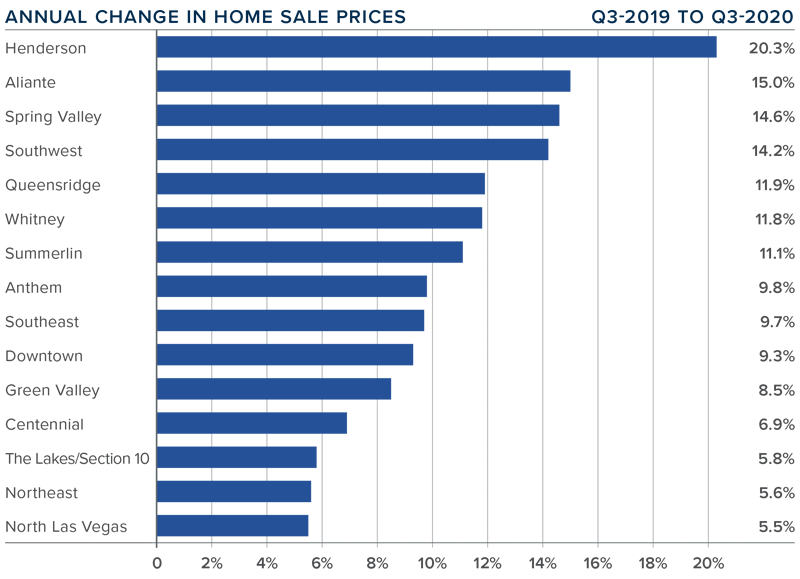

HOME PRICES

❱ As sales jumped and inventory remained tight, prices took off. The average sale price rose 13.1% year over year to $363,793. Prices were up 7.7% compared to the second quarter this year.

❱ Annual home price growth is still solid. It is clear that buyers are competing for homes, and favorable interest rates are allowing prices to rise at well-above-average rates.

❱ Prices rose in every sub-market compared to the same quarter last year, with significant gains in Henderson. Also of note is that prices rose by double-digits in seven areas.

❱ Buyers are out there, irrespective of an economy that is still on the mend. Belief in the benefits of homeownership is apparent, and this is certainly benefiting home sellers.

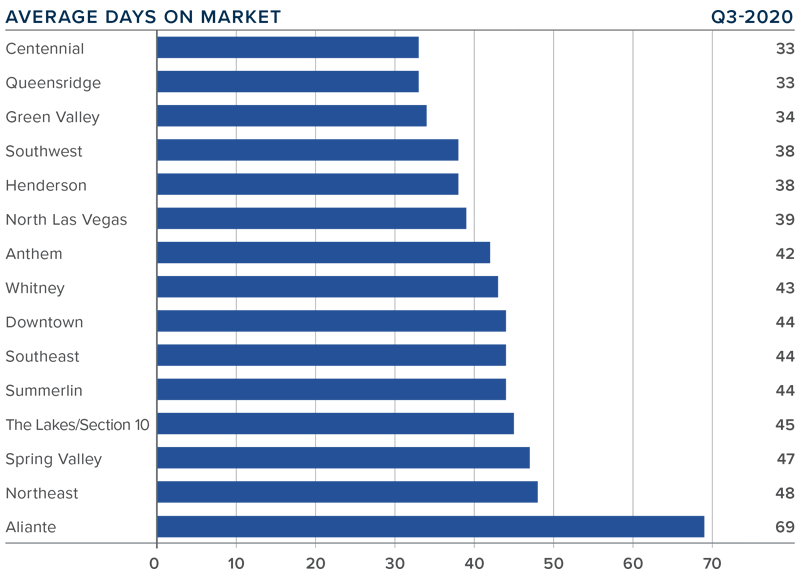

DAYS ON MARKET

❱ The average time it took to sell a home in the region dropped one day compared to the third quarter of 2019.

❱ Regionally, it took an average of 43 days to sell a home in the third quarter of 2020. It took 5 more days to sell a home than during the second quarter of this year.

❱ Days on market dropped in nine sub-markets, remained static in two, and rose in four compared to a year ago.

❱ The greatest decline in market time was in the Queens Ridge neighborhood. The greatest increase in market time was in Aliante, where homes took an average of 17 more days to sell than they did a year ago.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

The market continues to recover from the impact of COVID-19. Demand has improved, as suggested by the number of pending sales in this quarter, and buyers have become more active. If new infection rates start dropping and the economy continues to improve, the market will recover. Buyers are out there, and supply remains tight. As such, I am moving the needle a little more in favor of home sellers.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Park City Real Estate Market Update

The following analysis of select neighborhoods in the Park City real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

Though Utah is still feeling a significant economic hit, the jobs losses in March and April have certainly turned around. The pandemic caused the loss of more than 144,000 jobs in the state, but the most recent figures show that Utah has now recovered 95,900 of them. Although that still leaves a shortfall of 48,700 jobs, the numbers are promising.

The unemployment rate, which peaked at 10.4% in April, has dropped and now stands at a very respectable 4.1%.

If a headwind exists, it’s that new COVID-19 infection rates started to rise pretty aggressively again in September, and this has the potential to significantly slow Utah’s economic recovery.

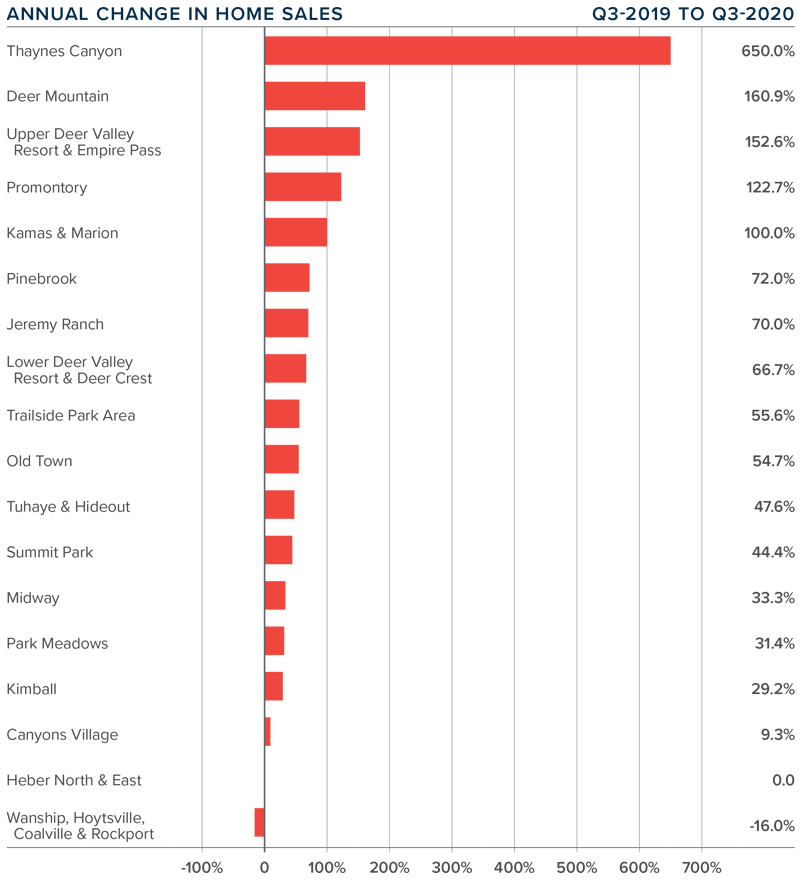

HOME SALES

❱ In the third quarter of 2020, 349 homes sold in the Park City area, an increase of a very solid 46% compared to the third quarter of 2019. Sales were also up by a remarkable 166.4% compared to the second quarter of this year.

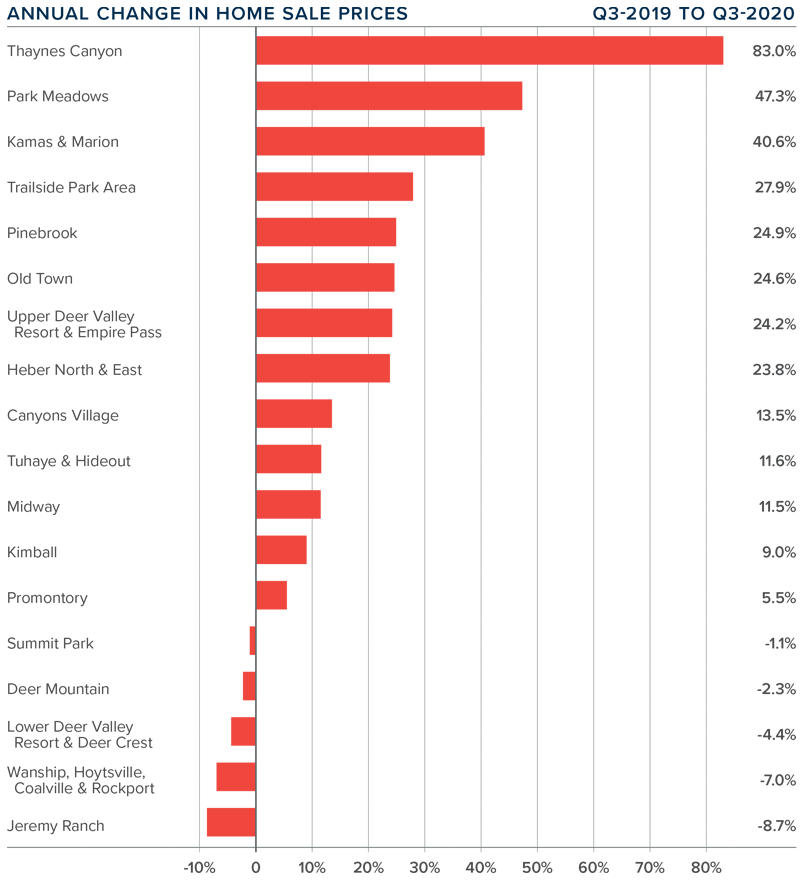

❱ Sales were down 16% in Wanship/Hoytsville/Coalville/Rockport, and static in Heber North & East from the quarter before. Sales rose in all other areas. Thaynes Canyon saw a remarkable 650% increase, though that equated to only 15 sales in the quarter.

❱ The growth in sales relative to the second quarter came as inventory levels dropped almost 10%. The growth in sales was a far cry from the significant decline we saw in the second quarter of the year. The market is clearly back!

❱ Pending home sales were 80.7% higher than a year ago, and up 228% compared to the second quarter of this year. Closings in the fourth quarter will be impressive.

HOME PRICES

❱ The average home price in the Park City neighborhoods contained in this report rose 28.3% year over year to $1.469 million. Prices were 26.7% higher than in the second quarter of 2020.

❱ The most affordable neighborhoods in terms of average home prices were again in the Kimball, Heber North & East, and Wanship/Hoytsville/Coalville/Rockport neighborhoods. The most expensive areas were Thaynes Canyon and the Upper Deer Valley Resort, where average home prices exceeded $3 million.

❱ Even with aggregate prices up significantly, they did not increase in all neighborhoods. Prices dropped in five neighborhoods, but I am not particularly concerned, as small areas can experience wild swings in prices depending on the homes that sold. Annual prices dropped in seven markets, with the most significant decline in the Canyons Village area.

❱ The Park City market is relatively small but contains some very expensive real estate. I mentioned in last quarter’s Gardner Report that it would be interesting to see if COVID-19-related impacts were going to persist or not. It appears as if they haven’t.

DAYS ON MARKET

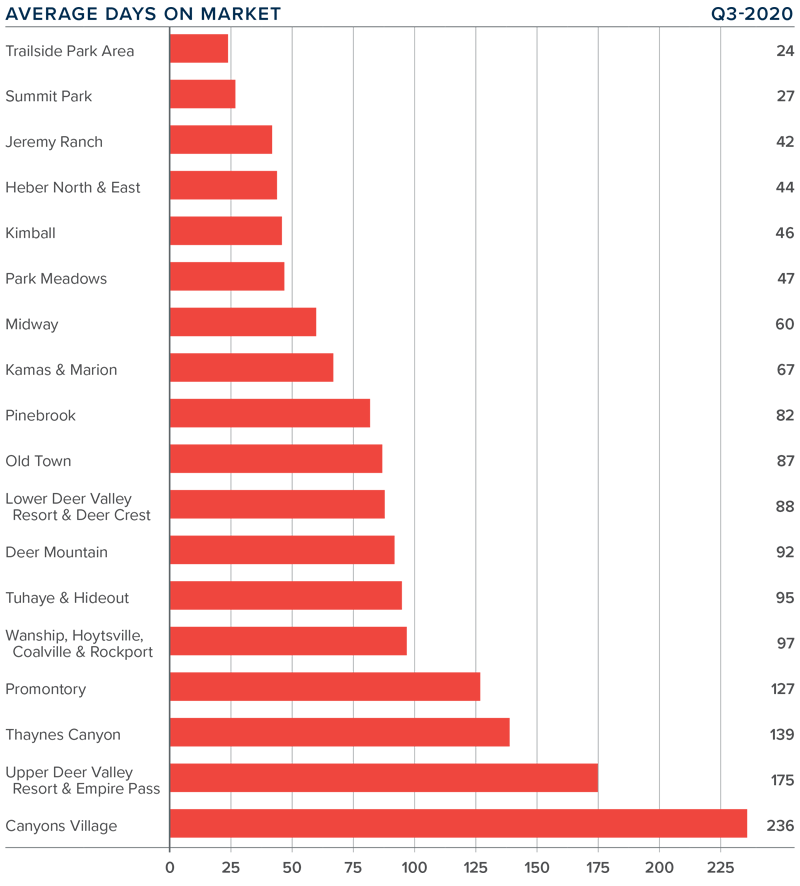

❱ The average time it took to sell a home in the Park City area dropped 25 days compared to the third quarter of 2019, and was down 13 days compared to the second quarter of this year.

❱ The amount of time it took to sell a home dropped in all but three neighborhoods relative to the third quarter of 2019: Wanship/Hoytsville/Coalville/Rockport, Deer Mountain, and Tuhaye/Hideout.

❱ In the third quarter, it took an average of 88 days to sell a home. Homes sold fastest in the Trailside Park and Summit Park areas and slowest in the Canyons Village neighborhood.

❱ The greatest drop in market time was in the Kamas & Marion neighborhood, where it took 94 fewer days to

sell a home than during the same period a year ago.

CONCLUSIONS

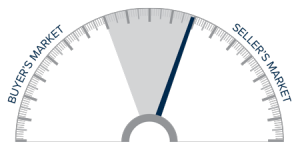

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

Buyers are trying to take advantage of historically low mortgage rates, and many are offering cash in order to put themselves in a more competitive position than other would-be buyers. Assuming the state gets new infection rates back under control, I believe sellers still have the upper hand.

I am therefore moving the needle a little more in their favor.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Utah Real Estate Market Update

The following analysis of select counties of the Utah real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

Though Utah is still feeling a significant economic hit, the jobs losses in March and April have certainly turned around. The pandemic caused the loss of more than 144,000 jobs in the state, but the most recent figures show that Utah has now recovered 95,900 of them. Although that still leaves a shortfall of 48,700 jobs, the numbers are promising. The unemployment rate, which peaked at 10.4% in April, has dropped and now stands at a very respectable 4.1%. If a headwind exists, it’s that new COVID-19 infection rates started to rise pretty aggressively again in September, and this has the potential to significantly slow Utah’s economic recovery.

HOME SALES

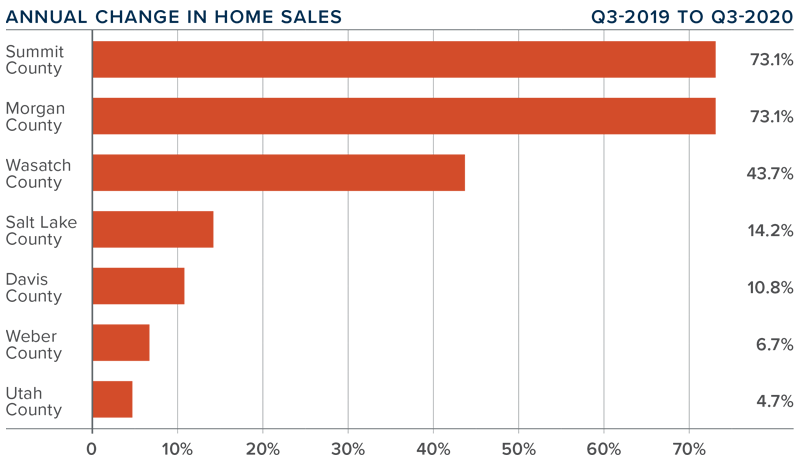

❱ In the third quarter of 2020, 11,623 homes sold, an increase of 11.3% compared to the same period in 2019. Sales were 24.7% higher than in the second quarter—on the back of a significant increase over the first quarter.

❱ Total sales activity rose in all counties covered by this report, with significant gains in the small counties of Summit and Morgan.

❱ In less positive news, the number of homes for sale in the quarter was 56.4% lower than during the same period a year ago and down 38.6% from the second quarter of this year.

❱ Pending sales in the third quarter were up 1.9% compared to the second quarter, suggesting that closings in the final quarter of 2020 will be positive. As I have stated in past reports, sales are only limited by the number of homes on the market.

HOME PRICES

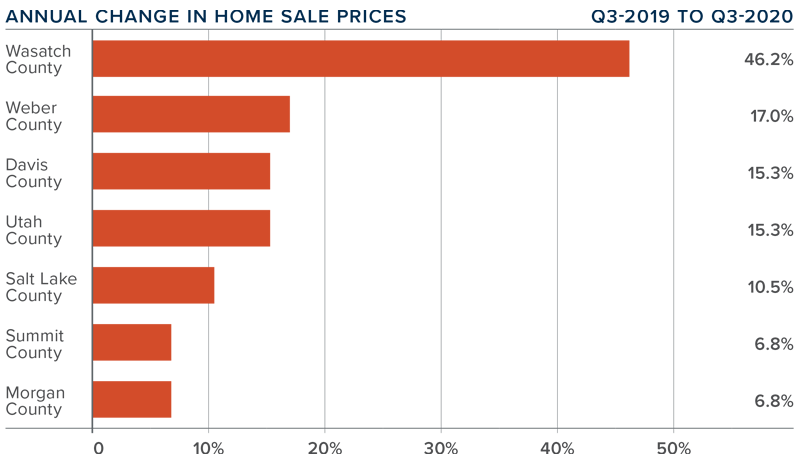

❱ The average home price in the region continued to rise in the third quarter, with a year-over-year increase of an impressive 15% to $432,640. Home prices were also 5.9% higher than in the second quarter of 2020.

❱ The average home price in the region continued to rise in the third quarter, with a year-over-year increase of an impressive 15% to $432,640. Home prices were also 5.9% higher than in the second quarter of 2020.

❱ Outside of Wasatch County, every county covered by this report saw solid price appreciation compared to the same period

a year ago.

❱ Price growth was strongest in Wasatch County, where prices rose a remarkable 46.2%. This is clearly an anomaly, and I expect to see price growth pull back in the fourth quarter.

❱ Home prices are appreciating at significant rates, demonstrating faith in the concept of home ownership, but also showing that buyers are taking advantage of historically low mortgage rates.

DAYS ON MARKET

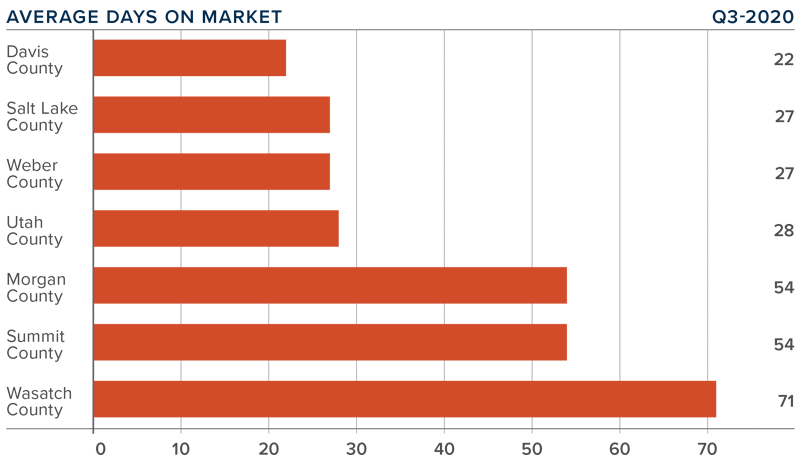

❱ The average number of days it took to sell a home in the counties covered by this report rose one day compared to the third quarter of 2019.

❱ Homes again sold fastest in Davis and Salt Lake counties. The longest time it took to sell a home was in Wasatch County. It took less time to sell a home in all counties other than Morgan, Wasatch, and Summit.

❱ During the third quarter, it took an average of 40 days to sell a home in the region, down 7 days from the second quarter of this year.

❱ Market time was essentially static compared to a year ago, but significantly lower than in the spring of 2020. This is likely due to the lack of inventory, making the housing market more competitive.

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

We know we have demand in the region, and that limited supply is heating up the housing market as demonstrated by reduced market time and significant price appreciation.

Listing activity is unlikely to improve as we round out the year, and buyers keen on taking advantage of historically low mortgage rates will be competing for the limited number of available homes. As such, I am moving the needle a little more in favor of home sellers.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national

level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

Montana Real Estate Market Update

The following analysis of select Montana real estate markets is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

Idaho Real Estate Market Update

The following analysis of select counties of the Idaho real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

Central Washington Real Estate Market Update

The following analysis of the Central Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

Eastern Washington Real Estate Market Update

The following analysis of the Eastern Washington real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

")