Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This is the latest in a series of videos with Windermere Principal Economist Jeff Tucker, where he delivers the key economic numbers to follow to keep you well-informed about what’s going on in the real estate market.

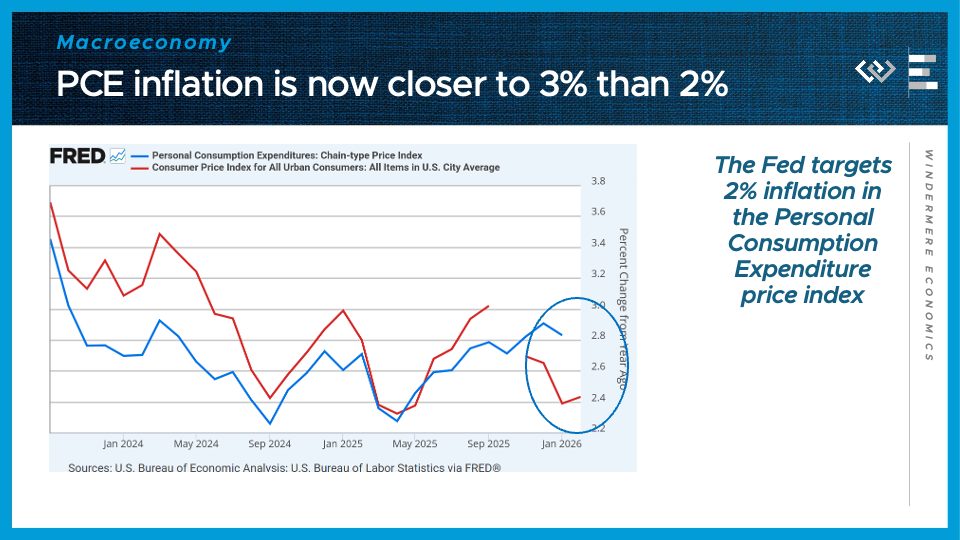

The first news this week is that the Federal Reserve did not cut interest rates at their meeting on March 18. Moreover, at the press conference following their meeting, Jerome Powell said they would not resume cutting interest rates this year until they saw some progress on inflation coming down further. For some insight into WHY that happened, our first number to know this week is 3%: that is where the Fed’s preferred inflation index has been heading in recent months. The Personal Consumption Expenditures price index normally runs a little cooler than the more well-known CPI inflation rate, and so the recent data showing the PCE inflation rate climbing toward 3% is giving the Fed even more of a reason to stop cutting rates than the benign CPI data this winter might have suggested.

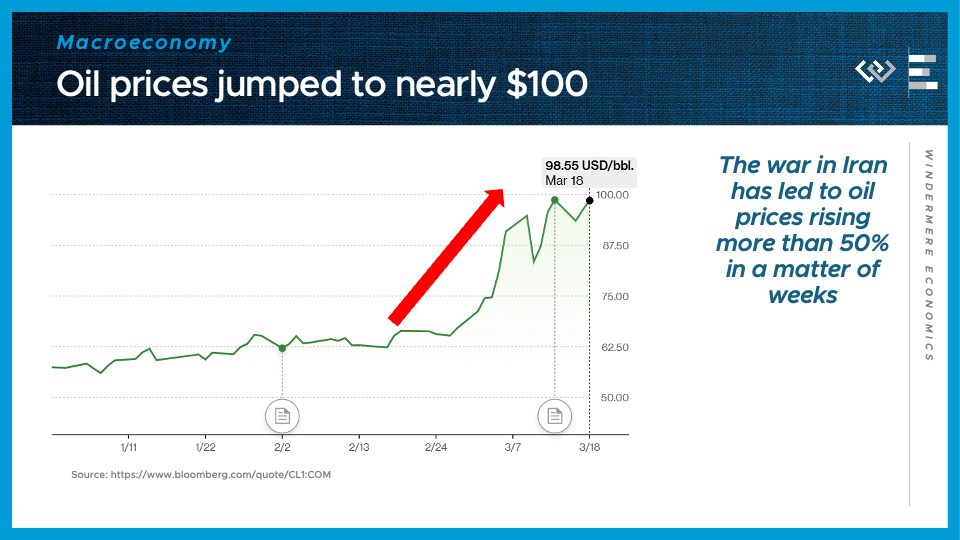

Our second number to know: about $100. That is the ballpark for what a barrel of oil is now costing on major world benchmarks, up more than 50% from prices under $60 just a few short months ago. The culprit, of course, is the war on Iran and the resulting cutoff of most oil normally shipped from the Persian Gulf. This is a volatile, unpredictable situation where the news may change at any time, but for now, the impact is clear: higher costs for almost everything in the economy, as the higher cost of energy ripples out through the economy. That is a major source of concern about inflation this year, which Jerome Powell cited ON TOP OF lingering tariff inflation, as a reason to wait and see before cutting rates any further.

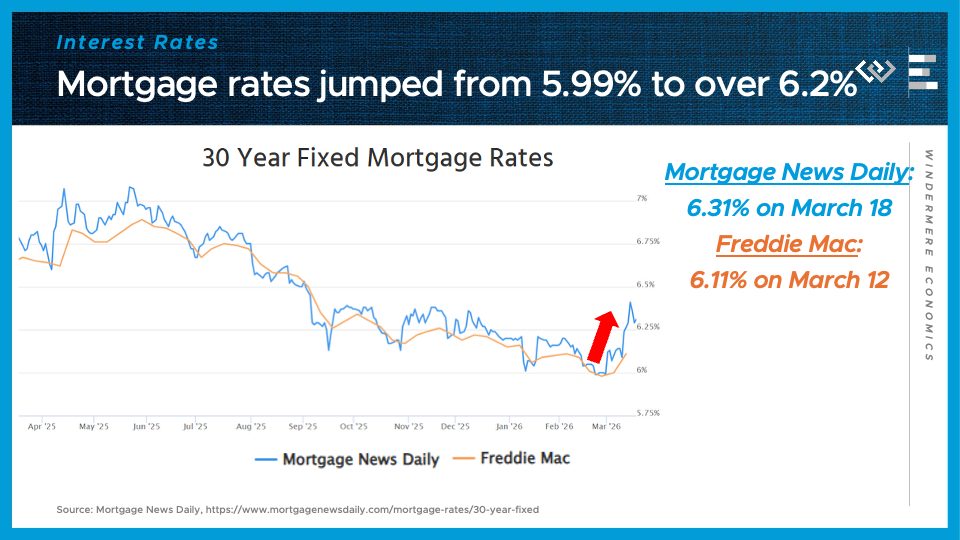

So our third number to know: mortgage rates back closer to 6 and a quarter percent, or higher. At the end of February we hit a major milestone: 30-year mortgage rates dipped below 6% for the first time in 41 months. But all the bad news I just shared about persistent inflation, especially driven by the new oil crisis, has sent mortgage rates soaring back up by a quarter point or more. That will throw a damper on home buying demand this spring, on top of the negative effects from higher gas prices and lower consumer confidence.

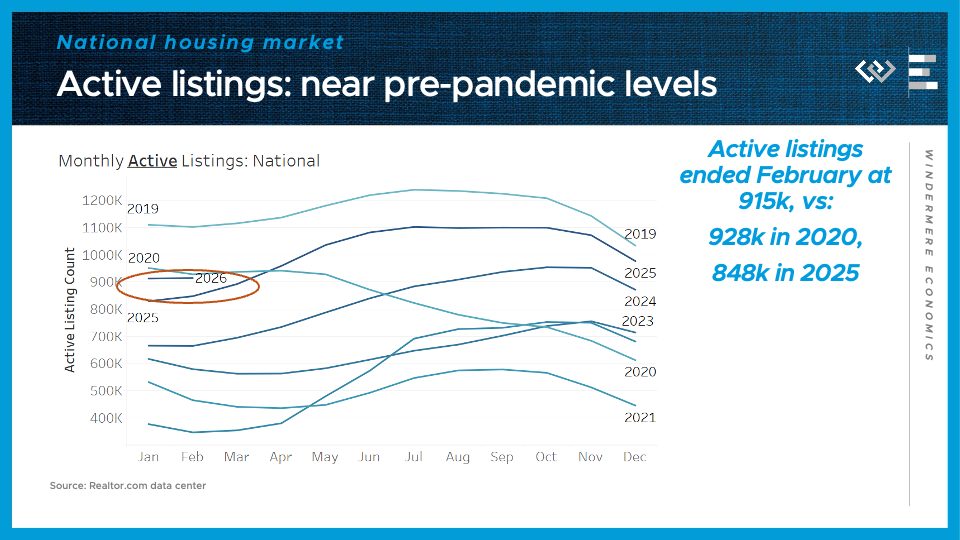

Speaking of the housing market, we saw 928 thousand active listings at the end of February, barely below where inventory stood at this time 6 years ago on the eve of the pandemic, and about 8% more than last year.

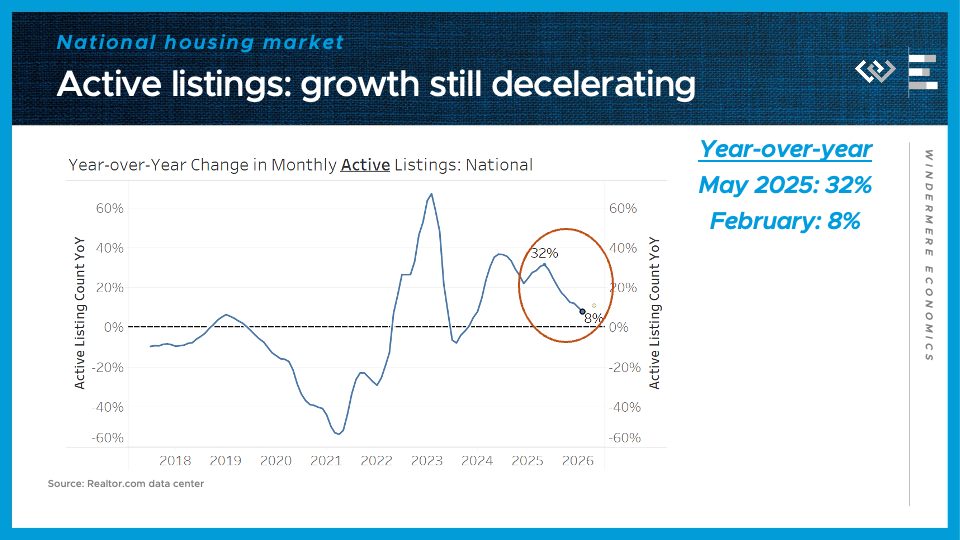

That marks yet another month where inventory is up year-over-year, but at a decelerating rate, ever since last May. Putting it all together, that means buyers will have more options in this spring buying season than in any recent year, but they should not expect a glut. The spring selling season always sees fierce competition for competitively-priced listings in desirable locations, so buyers should be prepared to move decisively if they see their dream homes, while sellers should do whatever they can to make their homes stand out amid the tide of other listings.

")