Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the February 2026 data from the Northwest MLS.

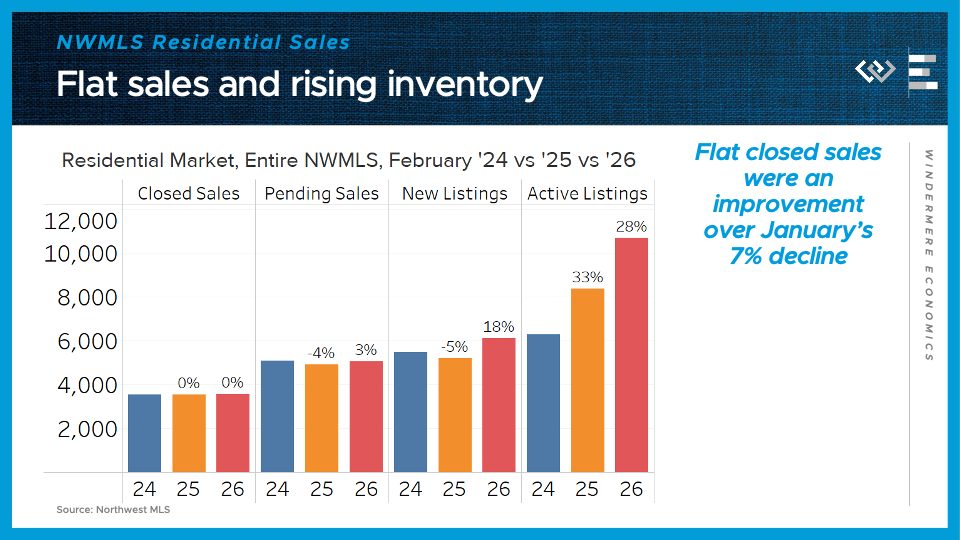

We are now on the cusp of the busy spring selling season, and the data so far in 2026 point to a market that’s relatively balanced for buyers … for this time of year.

Across the Northwest MLS, there were almost exactly the same number of closed home sales as in February 2025, or the prior February for that matter. And pending home sales ticked up by 3%.

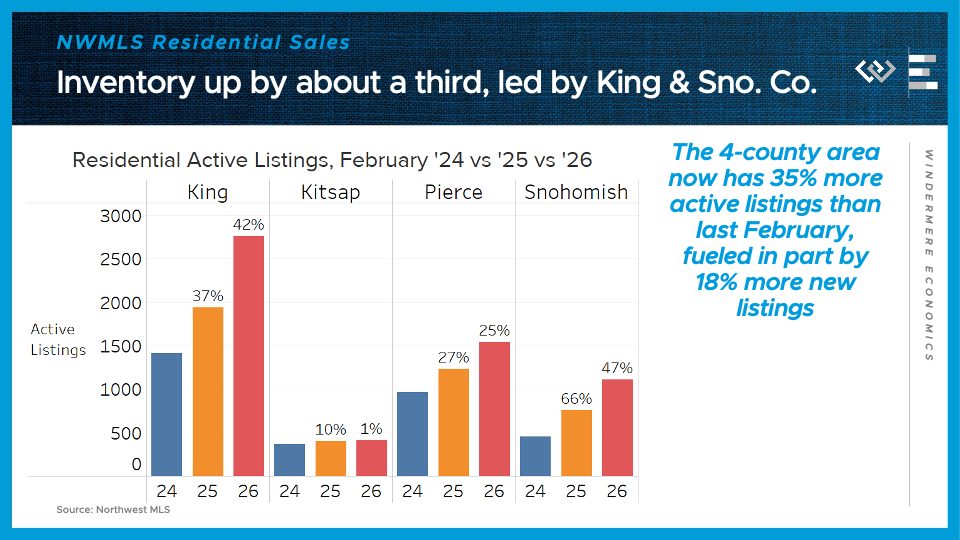

On the supply side, the flow of new listings was up a whopping 18% from last February’s pace. Finally, the month ended with 28% more active listings than last February. That’s a major uptick in inventory, and even the pace of that growth has now accelerated.

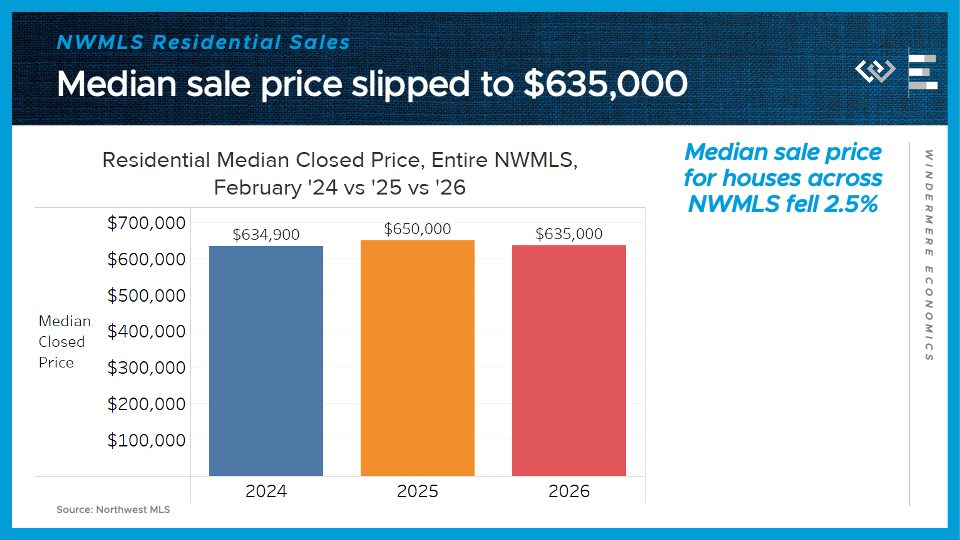

More negotiating leverage for buyers translated into lower home prices in February: down 2 and a half percent from last year, or basically back to 2024’s level.

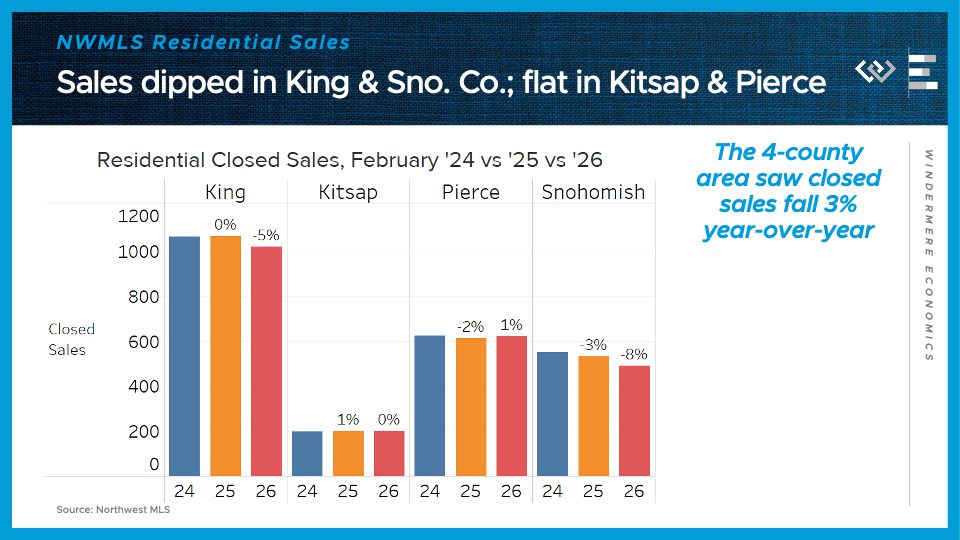

Now for a closer look at the four counties encompassing the greater Seattle area.

Closed sales dropped by 3% from last February around the region, which looked like a modest dip compared to January’s 9% decline. Once again Snohomish County had the biggest decline, followed by King County, while Kitsap and Pierce Counties’ sales volumes have held steady.

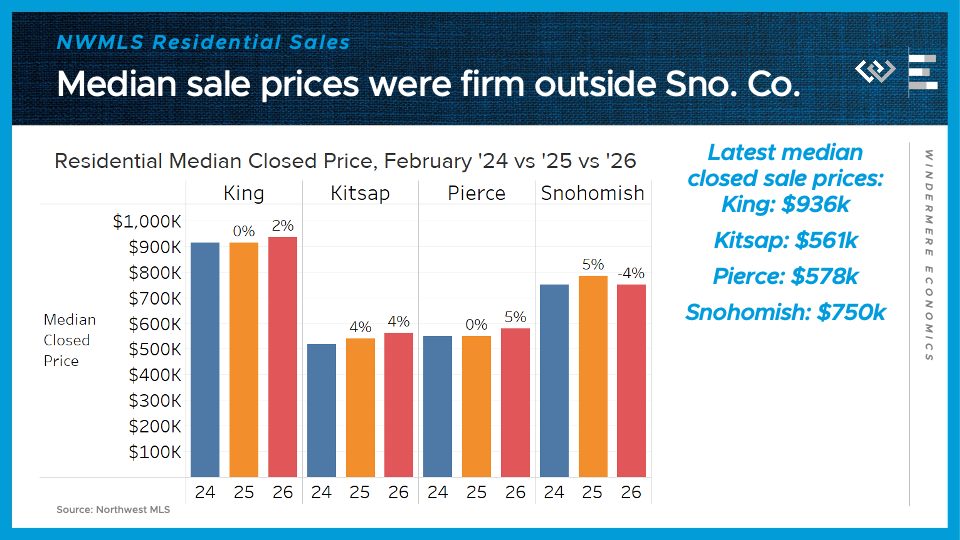

Median sale prices were mostly firm around the region, combing 2% in King, 4% in Kitsap, and 5% in Pierce County. Snohomish County, though, saw prices step back down to 2024 levels.

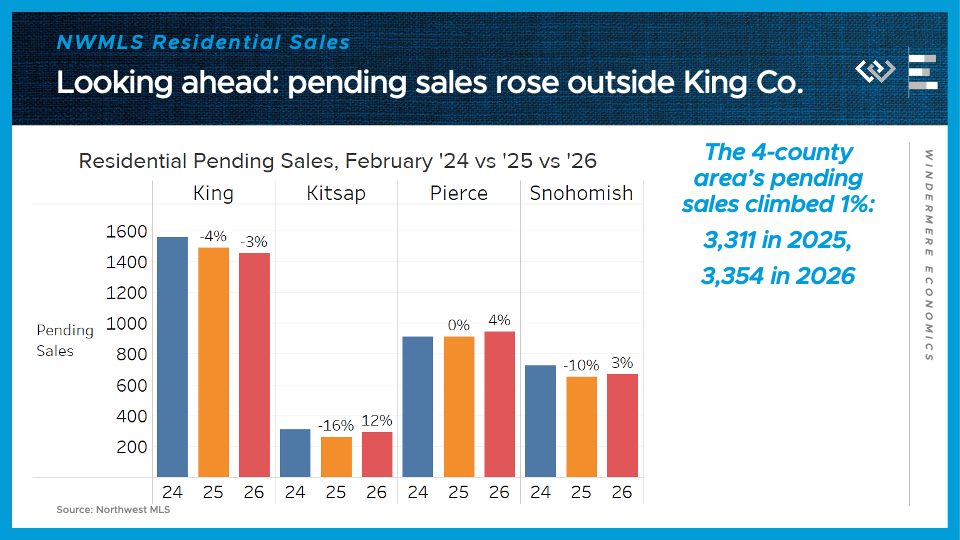

Looking ahead, pending sales climbed 1% across the region in February, buoyed by a big bounce back in Kitsap, and modest growth in Pierce and Snohomish Counties. Only King County saw a modest dip in pending home sales.

On the supply side, the 4-county greater Seattle area ended the month with 35% more active listings than last February, led by 47% growth in Snohomish County and 42% growth in King County. I think in those two core, higher-cost counties, buyers will see an unusually favorable spring buying season, thanks in part to a boost in listings from homeowners who de-listed last year and are now returning to the market.

Looking ahead to March and April, I think the big question is whether buyers feel emboldened by higher inventory and lower mortgage rates, or spooked by geopolitical turmoil and rising gas prices. As it stands, they will have more homes on the market to choose from than any spring in recent memory.

")