Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

ECONOMIC OVERVIEW

Washington State has seen very robust growth over the past 12 months with the addition of 102,600 new jobs, which is 224,000 more jobs than seen at the previous peak in 2008. With this robust growth, it is unsurprising to see the unemployment rate trend down to 5.8%—well below the long-term average of 6.4%. As pleasing as it is to see the unemployment rate drop, it is equally pleasing to see that the decrease comes in concert with growth in the civilian labor force, which continues to grow at a very solid pace. I continue to believe that there is no risk that we will see a statewide decline in the employment picture in 2016.

HOME SALES ACTIVITY

- There were 13,841 home sales during the first quarter of 2016, up by 3.8% from the same period in 2015. Sales activity continues to slow as a function of inventory constraints. Any spring “bounce” in listings has, thus far, failed to materialize.

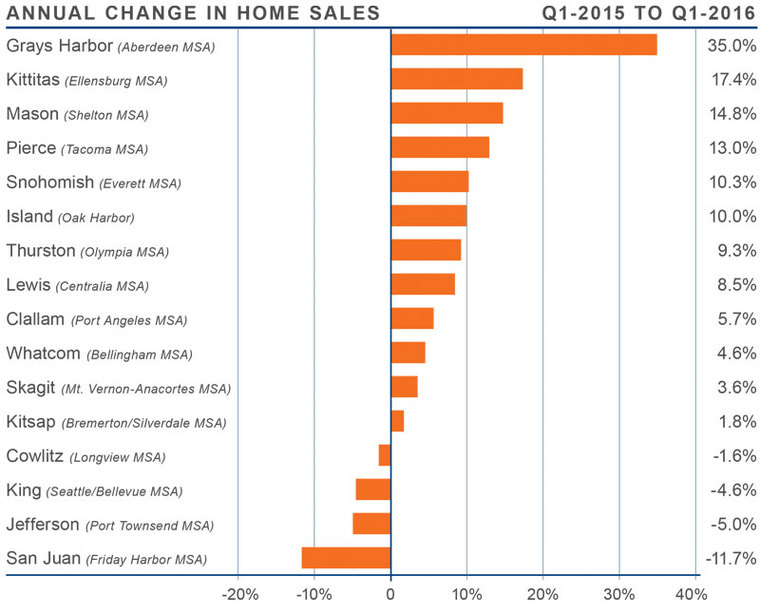

- The growth in sales was most pronounced in Grays Harbor County, which increased by 35% (but represented a real increase of just 63 units). Robust increases were also seen in Kittitas, Mason, Pierce, Snohomish and Island Counties. Sales declines were seen in San Juan, Jefferson, Cowlitz and King Counties.

- Overall listing activity was down by 30.1% compared to the first quarter of 2015, and this continues to put upward pressure on home prices (discussed below).

- Economic vitality in the region, combined with interest rates that continue to retest historic lows, is driving buyer demand that simply cannot be met. I hope that we will see more inventory come online as we move through the year, but believe that any reasonable growth in inventory will still be insufficient for the demand in the market.

HOME PRICES

- Given the demand factors mentioned above, I am not surprised that prices are up by an average of 10.1% year-over-year. This is up from the 9.3% average growth in prices that was reported in the fourth quarter 2015 report.

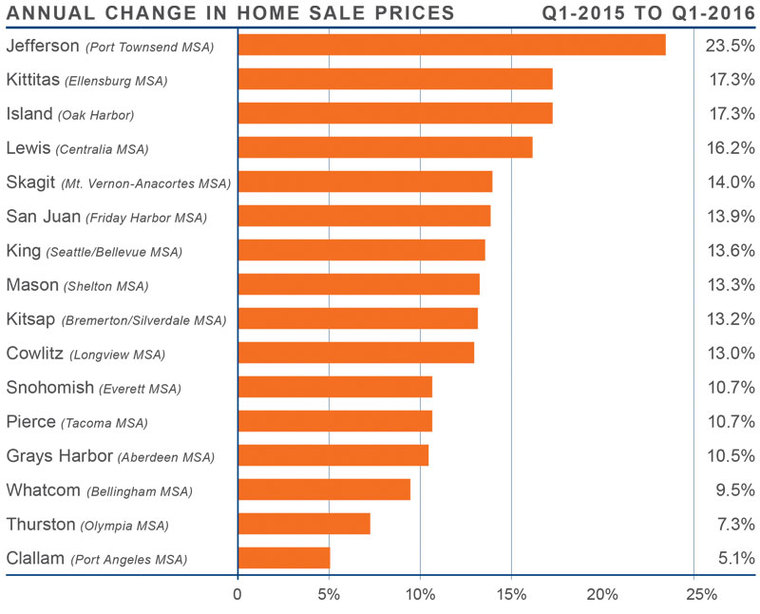

- When compared to the first quarter of 2015, price growth was most pronounced in Jefferson County, and all but three counties saw prices increase by double digits from the previous year.

- Interestingly, there were eight counties that actually saw a drop in average sale prices between the last quarter of 2015 and the first quarter of 2016. I believe this was caused by seasonal factors, but will keep an eye on it.

- Very straightforward supply and demand factors are pushing prices higher. While this certainly favors sellers, I believe that there are some buyers who are starting to suffer from “buyers’ fatigue”. Rampant growth in inventory would sort this out but it is unlikely to occur this year.

DAYS ON MARKET

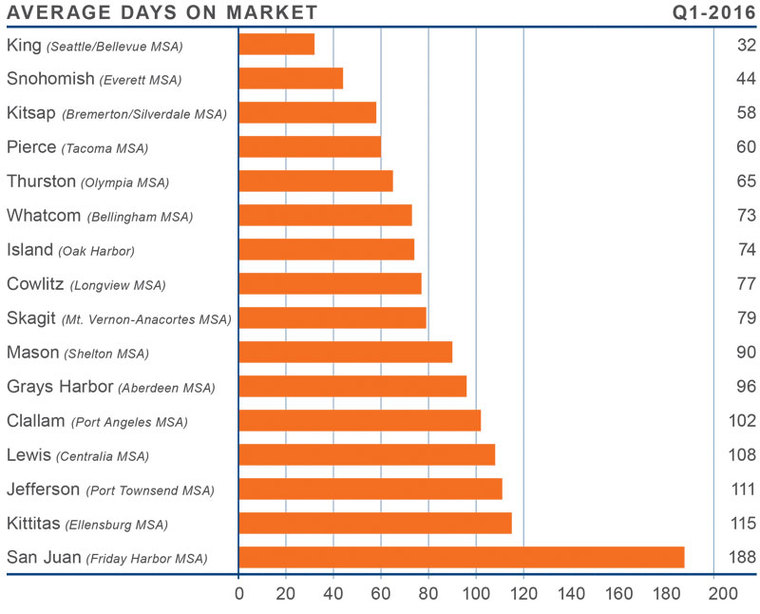

- The average number of days it took to sell a home dropped by sixteen days when compared to the first quarter of 2015.

- As was seen in the Q4 2015 report, there were just two markets where the length of time it took to sell a home did rise, but again the increases were minimal. Skagit County saw an increase of three days while San Juan County rose by nine days.

- It took an average of 86 days to sell a home in the first quarter of this year—up from the 78 days it took to sell a home in the last quarter but this is simply due to seasonality.

- Sales activity remains most brisk in the Central Puget Sound counties. Given their proximity to the major job centers, this is not a surprise.

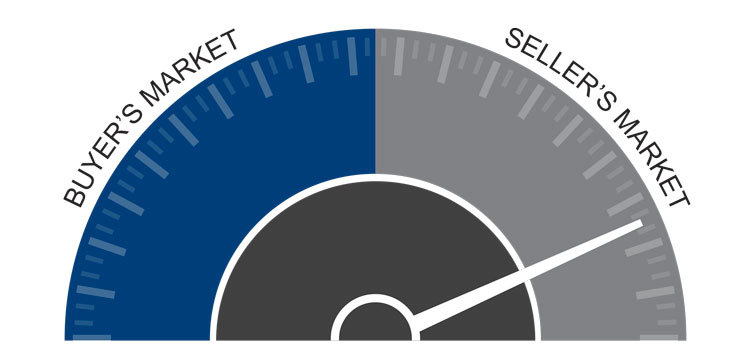

CONCLUSIONS

This speedometer reflects the state of the region’s housing market using housing inventory, price gains, sales velocities, interest rates, and larger economics factors. For the first quarter of 2016, I have moved the needle slightly more in favor of sellers. Inventory constraints persist and this is now starting to affect sales activity, with growth in pending as well as closed sales starting to trend down. However, price growth remains well above average and interest rates are still close to historic lows.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

")