Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Local Look Western Washington Housing Update 8/6/26

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the June 2026 data from the Northwest MLS.

We are now in the dog days of summer here in Seattle, and so far, the housing market hasn’t escaped the doldrums of a weak spring selling season.

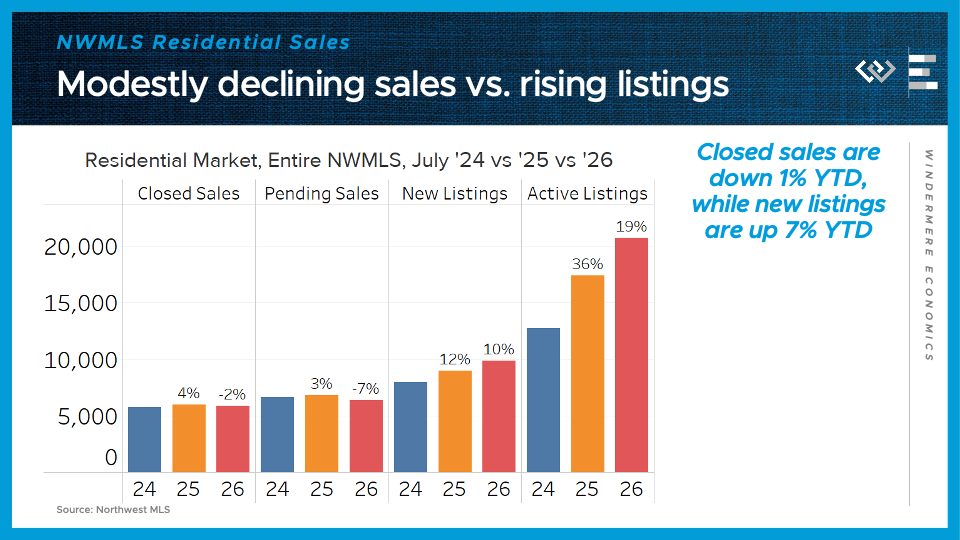

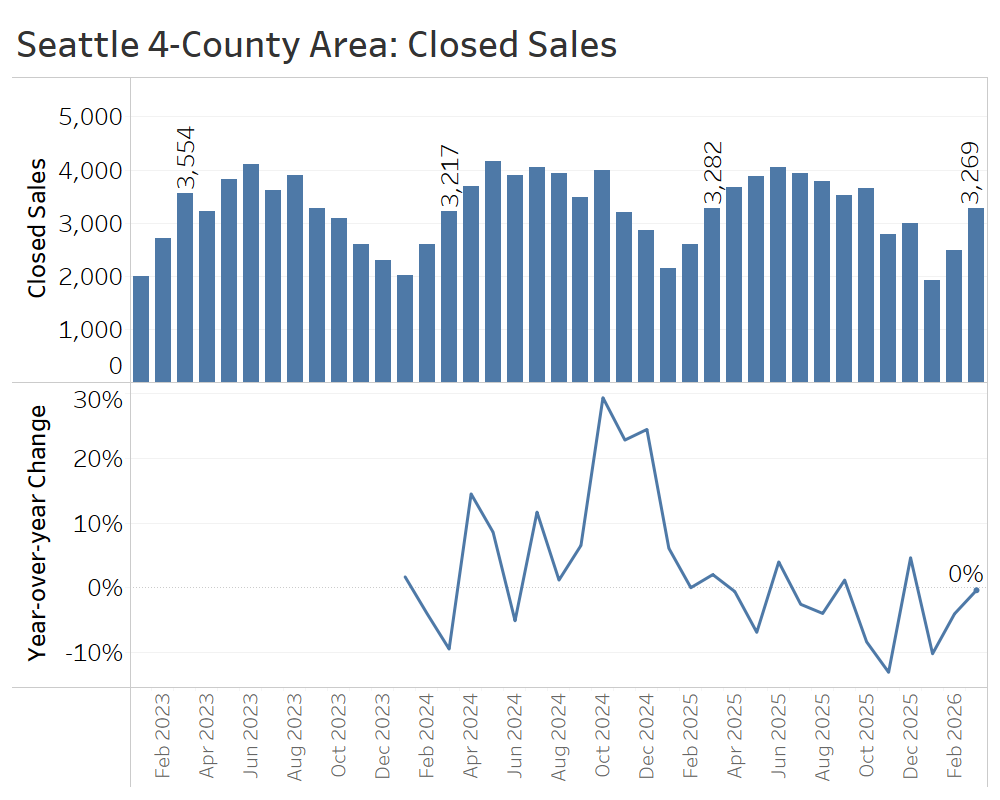

Across the entire Northwest MLS, there were 2% fewer closed sales in July of 2026 than in July of last year – the same drop we saw in April and May. Pending home sales dropped by 7% from last year, but that was partly explained by an extra Tuesday last July.

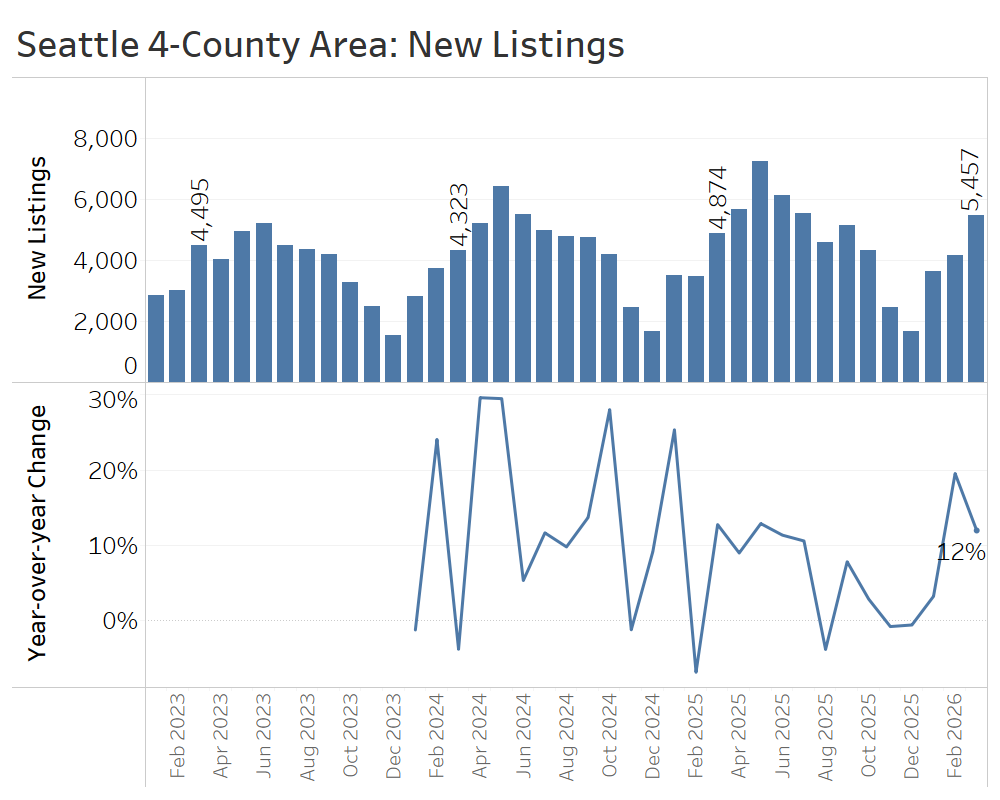

On the supply side, new listings actually climbed 10% from last July, and the month ended with nearly 21,000 active listings around the MLS, or 19% more than last July. Unfortunately, that’s a modest acceleration from a 17% pace of annual gains in May, which suggests further softening for prices ahead.

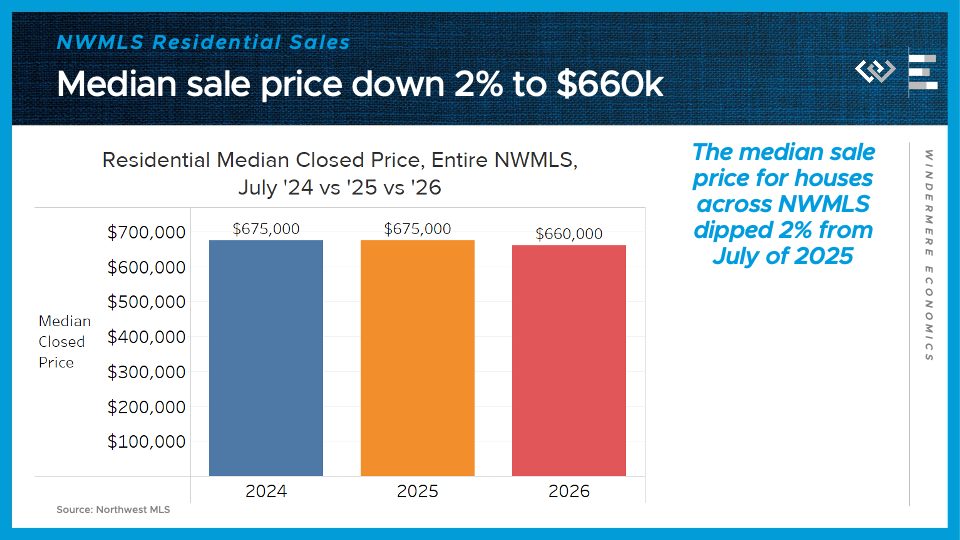

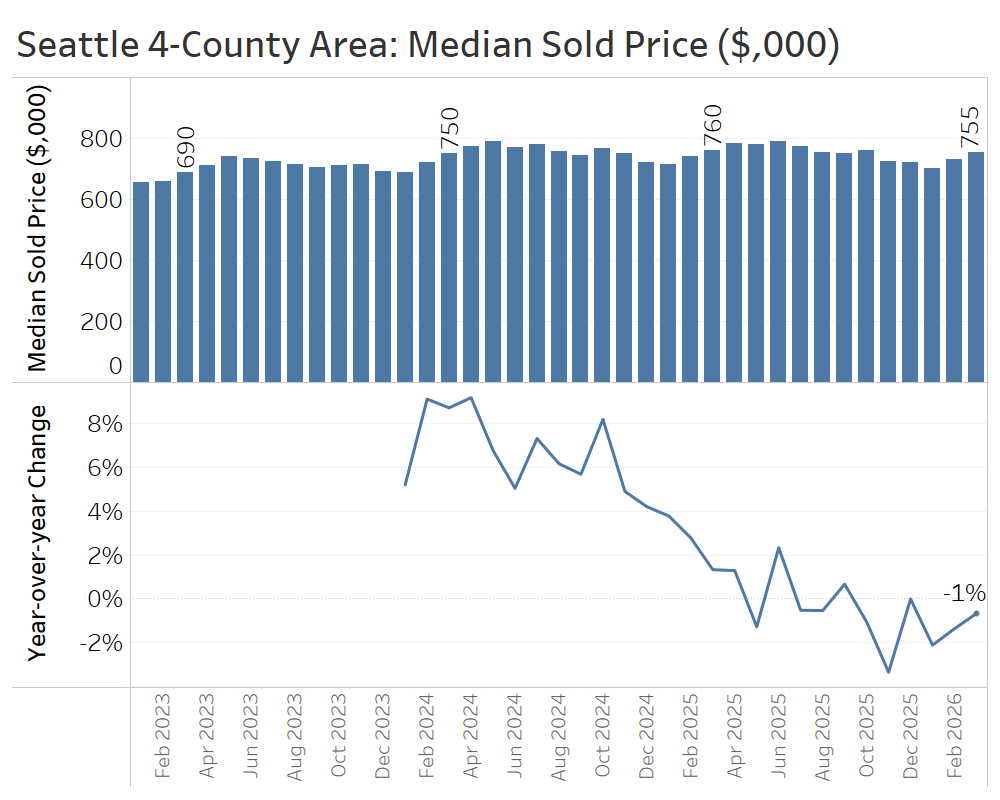

Speaking of which, the median sale price dipped versus last July by about 2%, to $660,000, after a couple of years at $675,000.

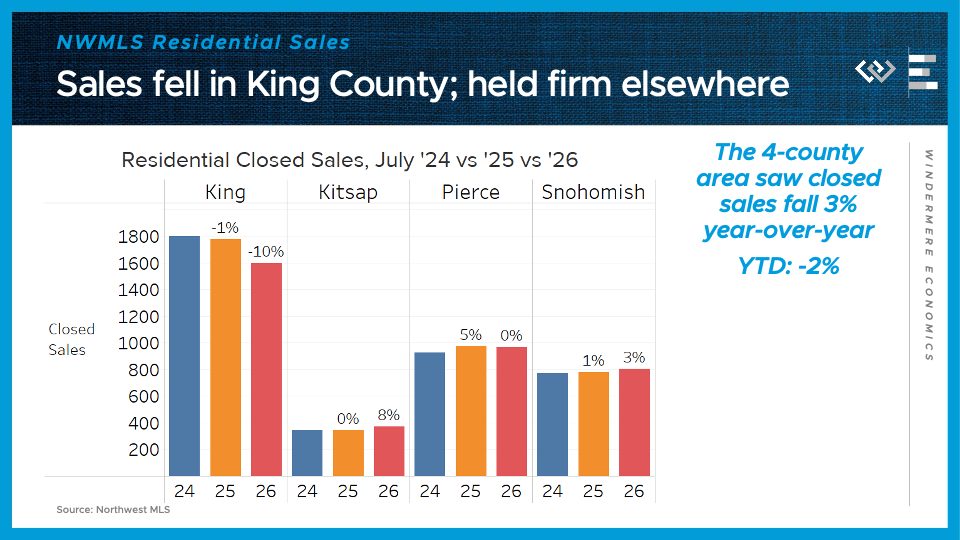

Now I’ll take a closer look at the four counties encompassing the greater Seattle area.

Closed sales declined by 3% from last July, and that was entirely driven by a 10% drop in King County. Meanwhile, Kitsap looked pretty strong, with 8% sales growth, while Snohomish County ticked up 3% and Pierce was flat from last year.

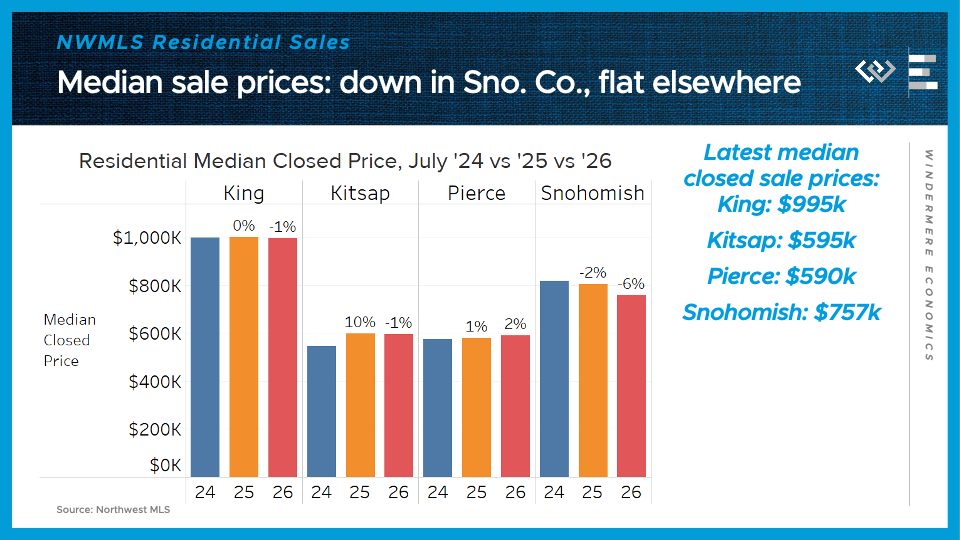

Median sale prices were mostly flat or down slightly, around the region – down the most, by 6%, in Snohomish County again to $757,000, and down just five thousand dollars in King County from $1 million in each of the last two Julys.

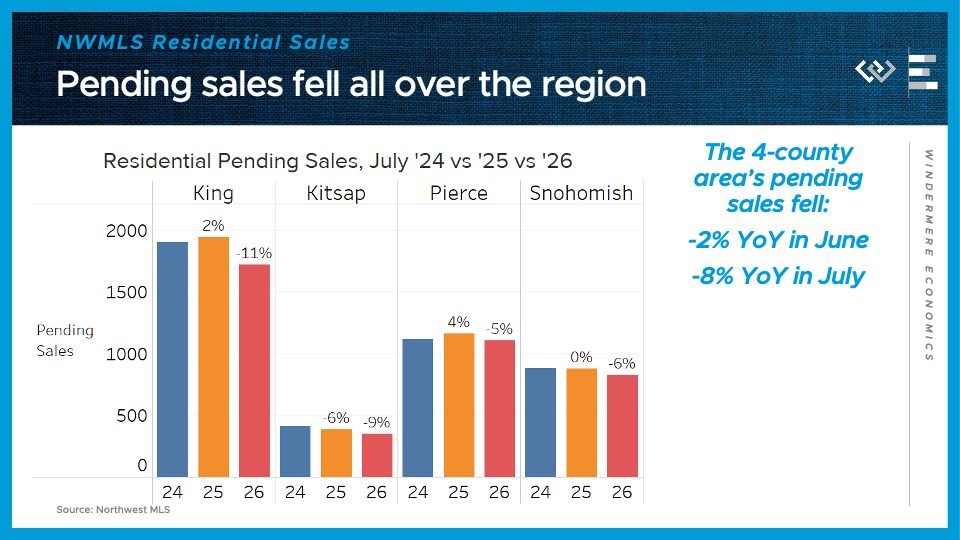

Looking ahead, pending sales fell all around the region, led by a drop of 11% in King County. That is partly attributable to calendar effects, as last July had one more Tuesday than this one, but July’s drop follows on the heels of a 2% drop in June, suggesting a generally weak sales environment all summer so far.

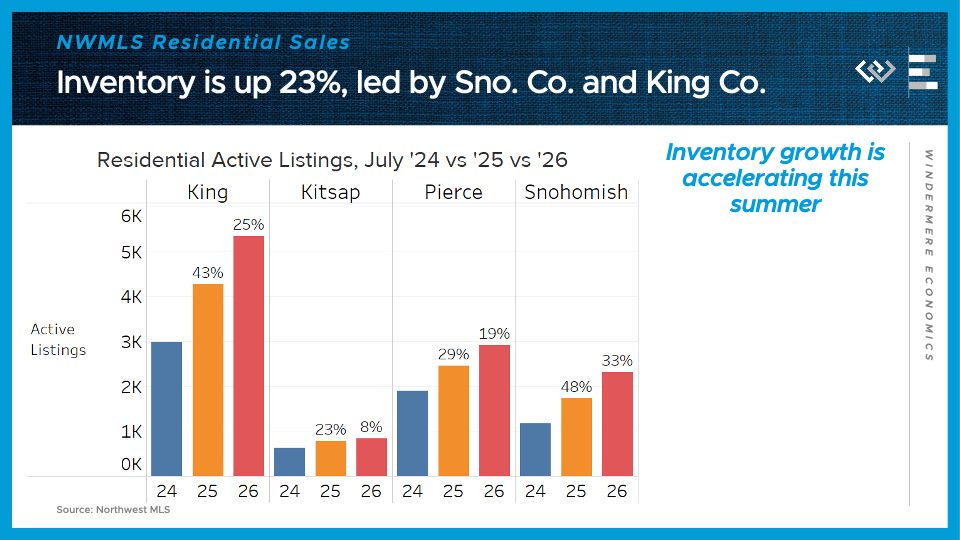

On the supply side, the 4-county greater Seattle area ended the month with 23% more active listings than last July, up from an 18% growth rate in May. That re-acceleration of inventory growth seems to stem from buyers not showing up in a big way so far this summer.

All in all, the data through midsummer are reinforcing the message of a swing toward a buyer’s market in Washington, and especially in King County and Greater Seattle. Homeowners looking to sell should be prepared for more competition from other listings, and be prepared to face buyers expecting a bargain. Conversely, home shoppers are likely to see a excellent conditions to buy a home here this fall, between a high-water mark for inventory and lower prices than the last couple of years.

2026 Second Quarter Regional Real Estate Report

This is a recurring series of blog posts taking a closer look at the U.S. economy and several major regional markets in Windermere’s nine-state footprint. Updates will be released on a quarterly basis.

Economic Overview

At the start of the second quarter, new geopolitical turmoil threatened to derail an expected rebound in housing market activity. The disruptions to energy markets and supply chains caused by the Iran war drove both inflation and interest rates up sharply. Mortgage rates averaged 6.41% over the entire quarter, erasing the welcome declines observed in the winter.

Source: Freddie Mac via FRED.

The war in Iran also reversed the past winter’s modest improvements in consumer sentiment, according to the University of Michigan’s Consumer Sentiment Survey.

Source: University of Michigan via FRED.

Remarkably (but less remarked upon), the labor market decisively improved in the first half of the year: employment levels reversed the stall seen in late 2025, posting solid gains throughout the spring, while job openings turned up in April and May. The stock market also posted strong year-to-date gains of nearly 10% by midyear, shaking off initial declines at the outbreak of the war.

In the final tally, the balance of macroeconomic tailwinds and headwinds did not send the housing market back into hibernation. The spring selling season saw time on market drop while sales climbed from the first quarter, following the seasonal trends that we see almost every year. Sales also increased year over year across most of the regions in this report, although they dipped slightly around the Seattle area. After two straight springs marked by geopolitical disruptions, there’s reason to hope that a quieter summer and fall leading into the midterm elections will provide the foundation for strong sales activity in the second half of 2026, especially if inflation cools and mortgage rates ease.

The following is a detailed overview of housing trends across six regional markets within Windermere’s footprint during the second quarter of 2026. They include:

- Greater Seattle Area

- Greater Portland Area

- Greater Sacramento Area

- Northwest Washington State

- Spokane, WA and Coeur d’Alene, ID markets

- Salt Lake County, UT

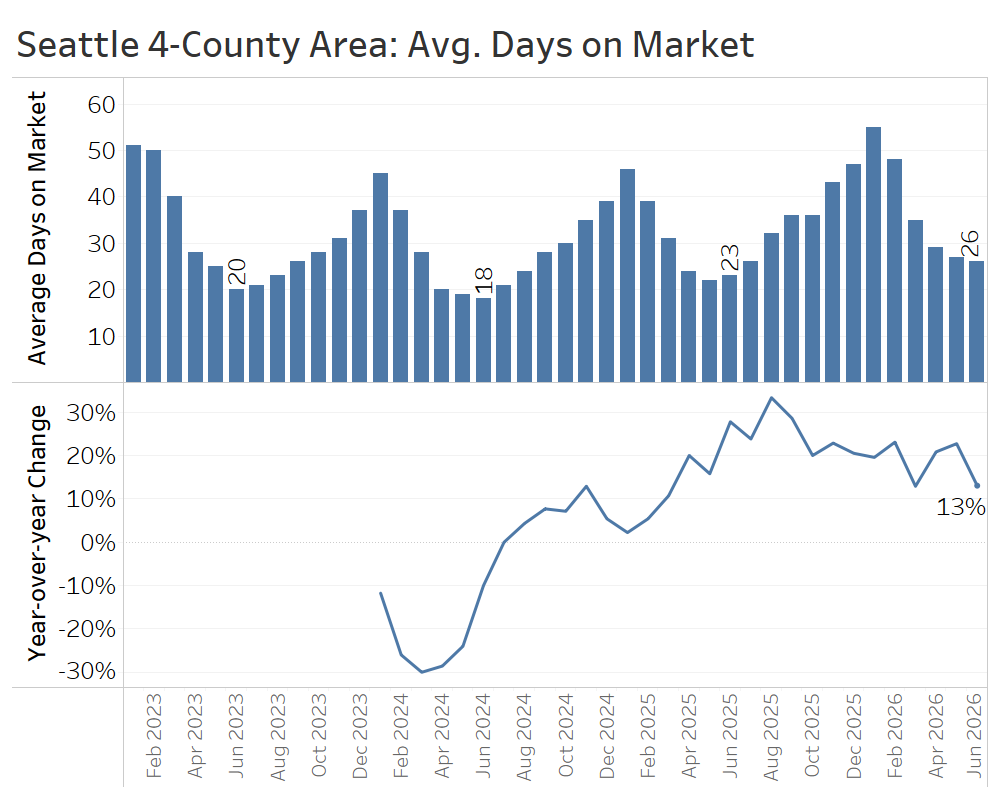

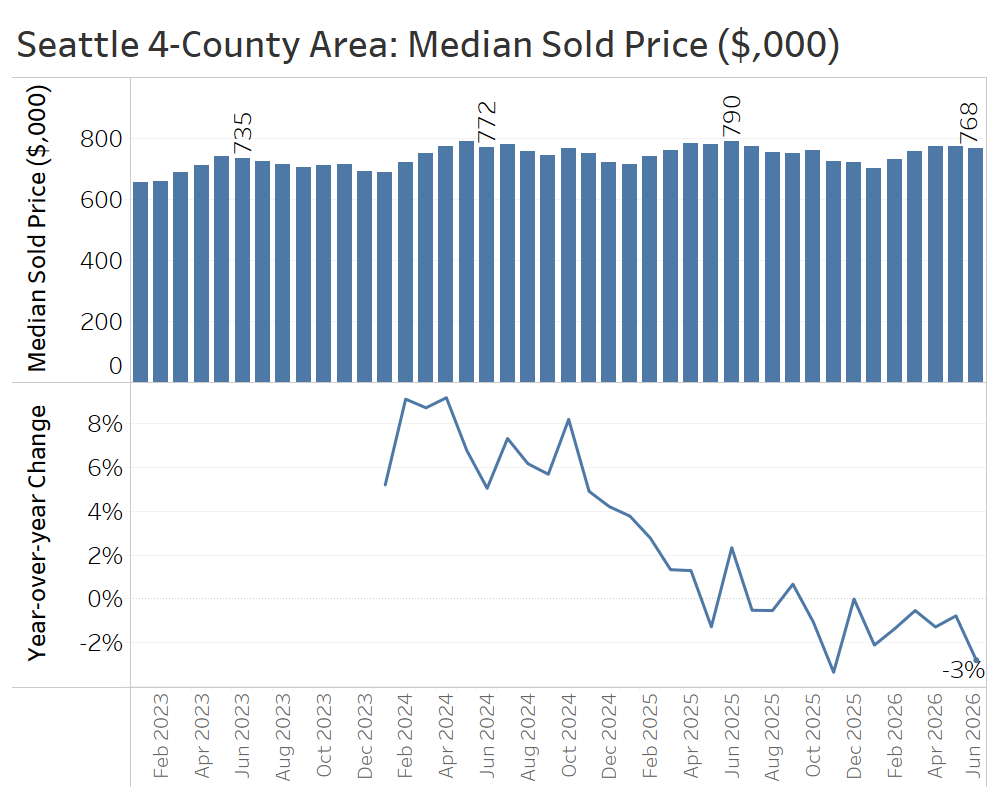

Greater Seattle Area (King, Snohomish, Pierce, and Kitsap Counties)

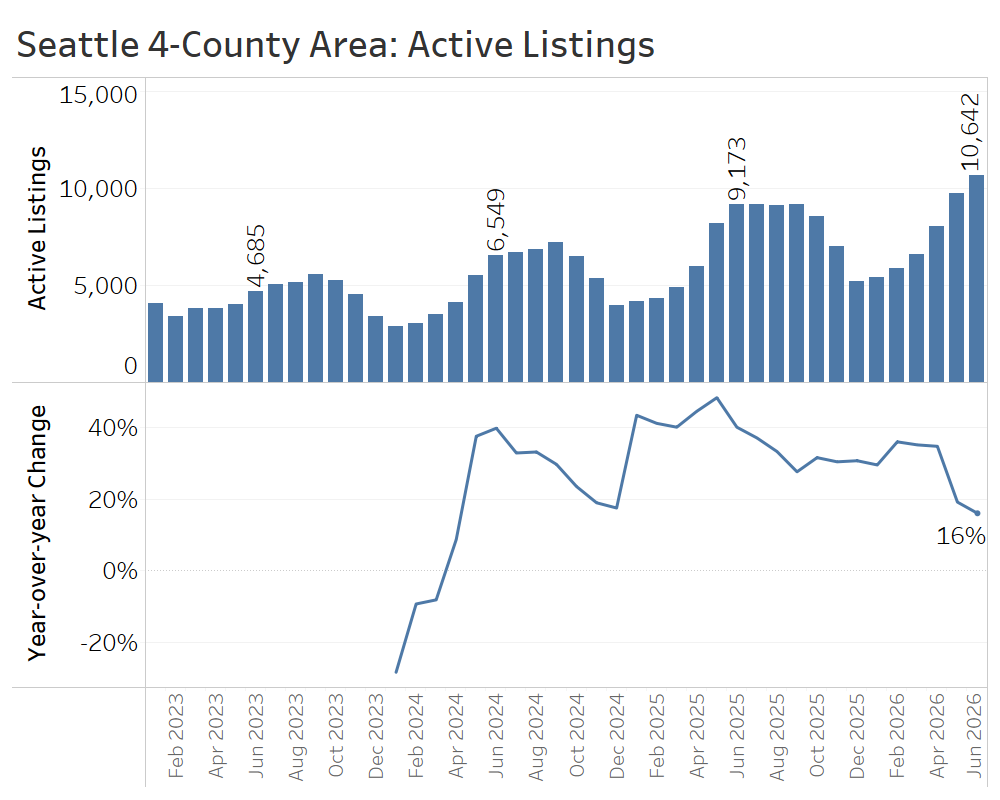

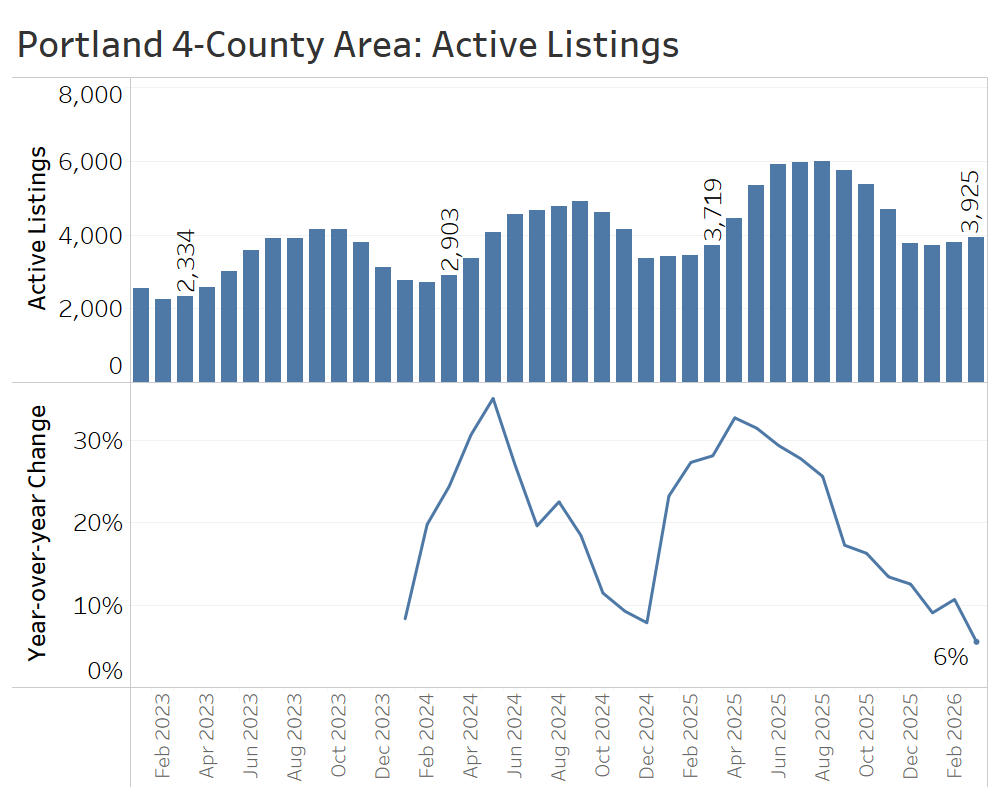

The Seattle-area housing market saw a more buyer-friendly spring selling season than expected. The spring increase in active listings outpaced year-ago levels, giving buyers more choices and putting pressure on sellers to consider accepting lower offers. The pace of inventory gains, however, slowed to just 16% year over year in June, which may mark an inflection point of slowing accumulation of active listings – a trend to watch in the third quarter.

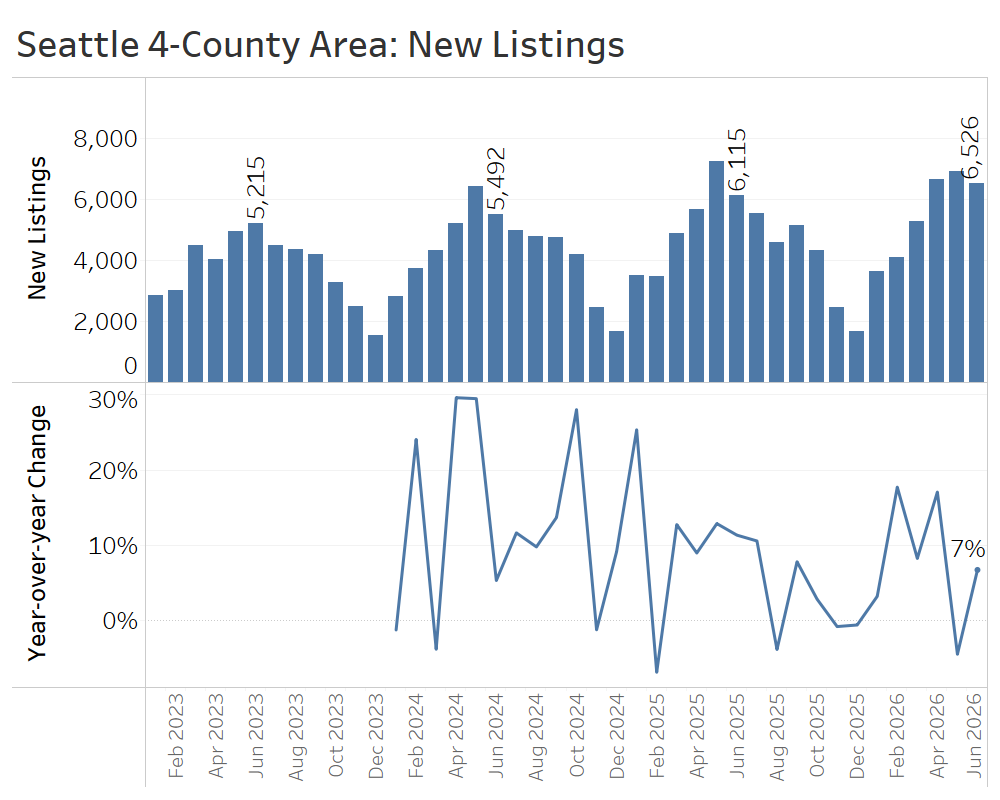

The growth in active listings was supported by a continued flow of new listings in the second quarter. Some sellers who had waited out the uncertainty of late 2025 returned to test the market during the spring, but buyer demand did not increase enough to absorb all the additional supply.

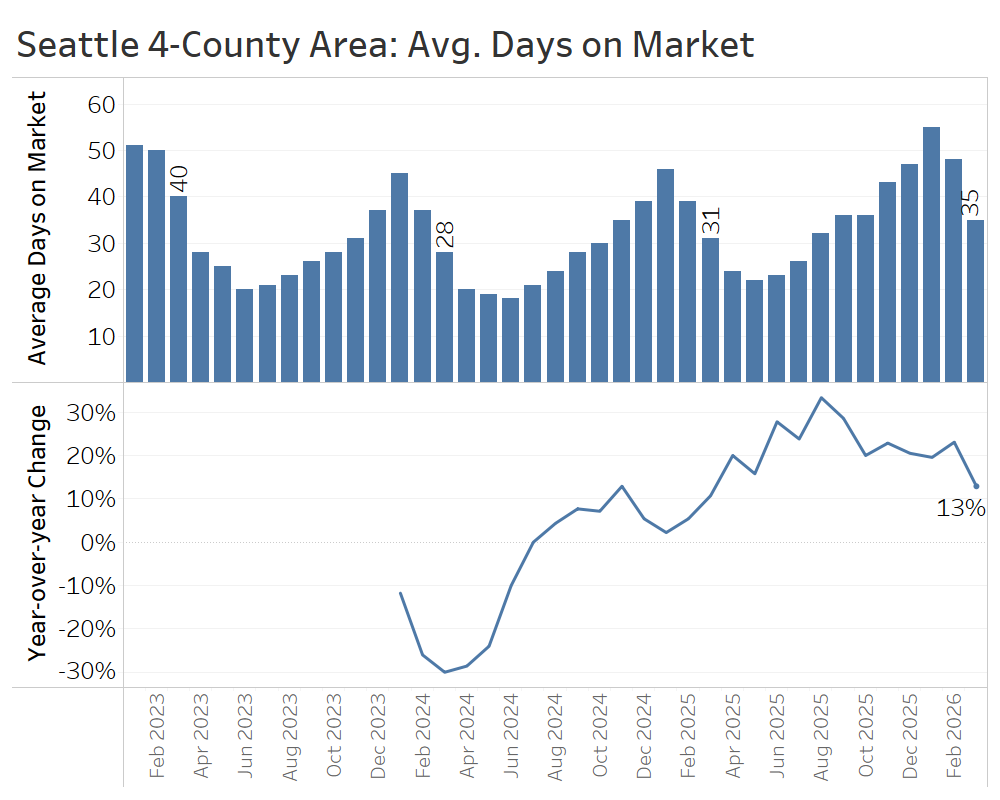

Time on market dropped from winter levels, as is typical during the spring, but homes still took longer to sell than they did last year or in the prior two years at this time.

Closed sales lagged behind year-ago levels in April and May, before registering a 1% year-over-year gain in June. It’s too early to tell, but this could mark the beginning of an inflection point if buyers are starting to clue into the favorable inventory and pricing conditions.

Softer demand continued to show up in pricing. Median sale prices were generally flat to slightly below year-ago levels, as elevated inventory put downward pressure on prices.

Overall, the second quarter brought more choice for Seattle-area buyers and more competition for sellers. Well-priced homes continued to move, but most sellers needed more realistic list prices, paired with the best possible presentation, in order to sell quickly.

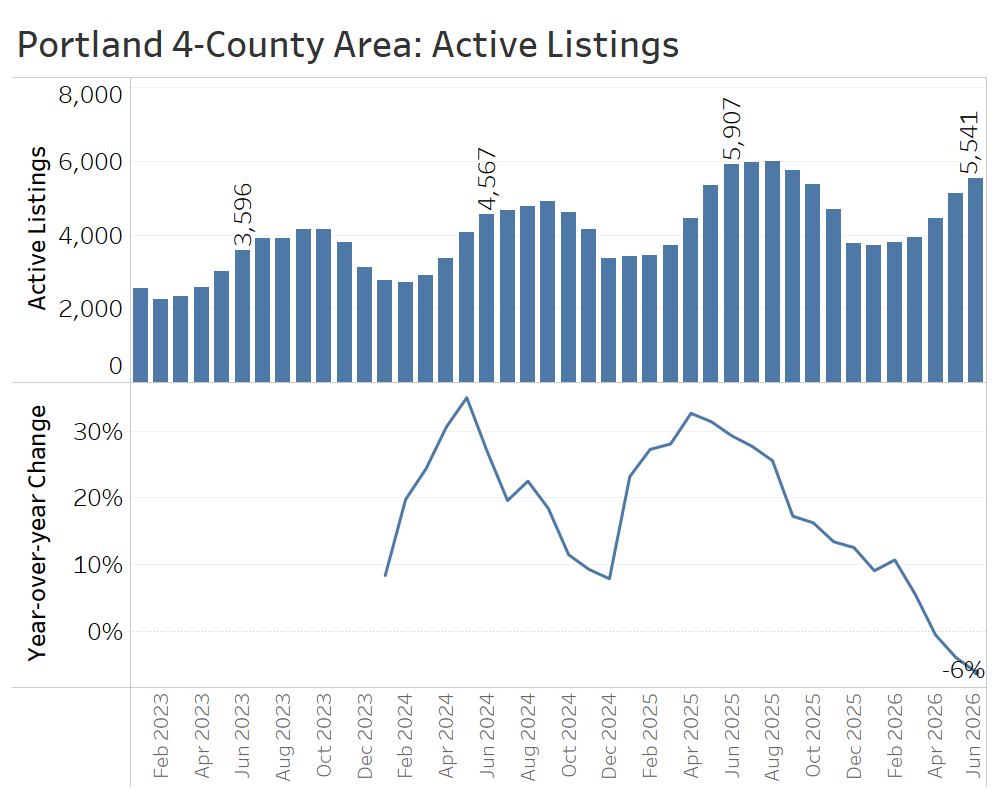

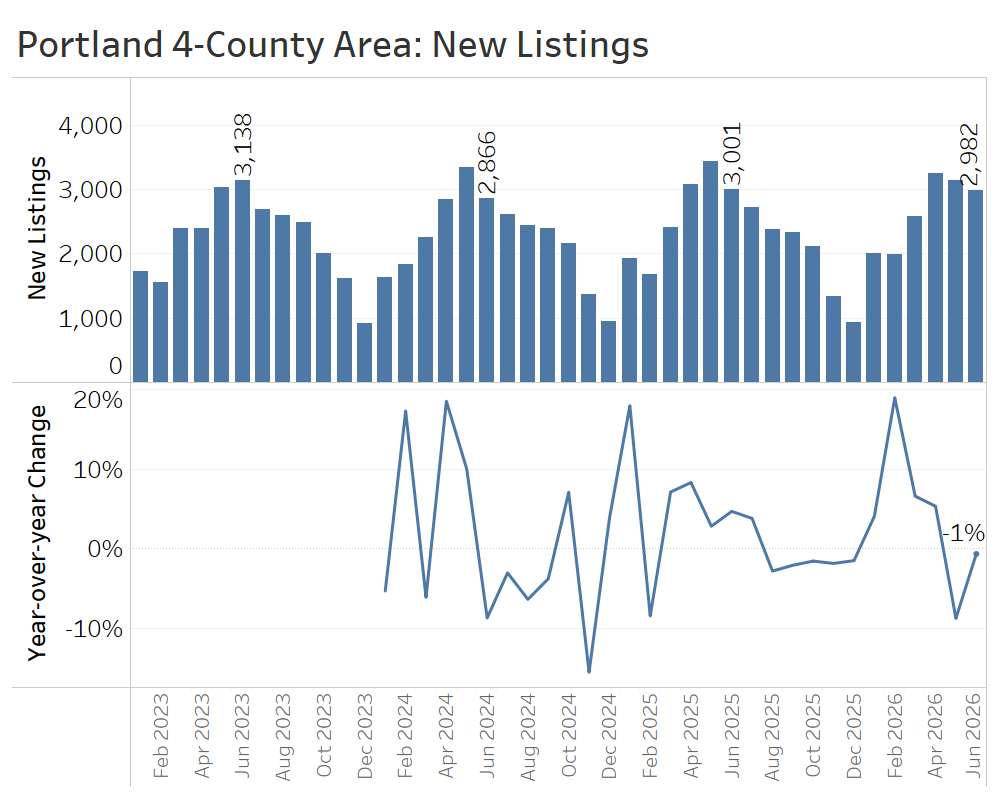

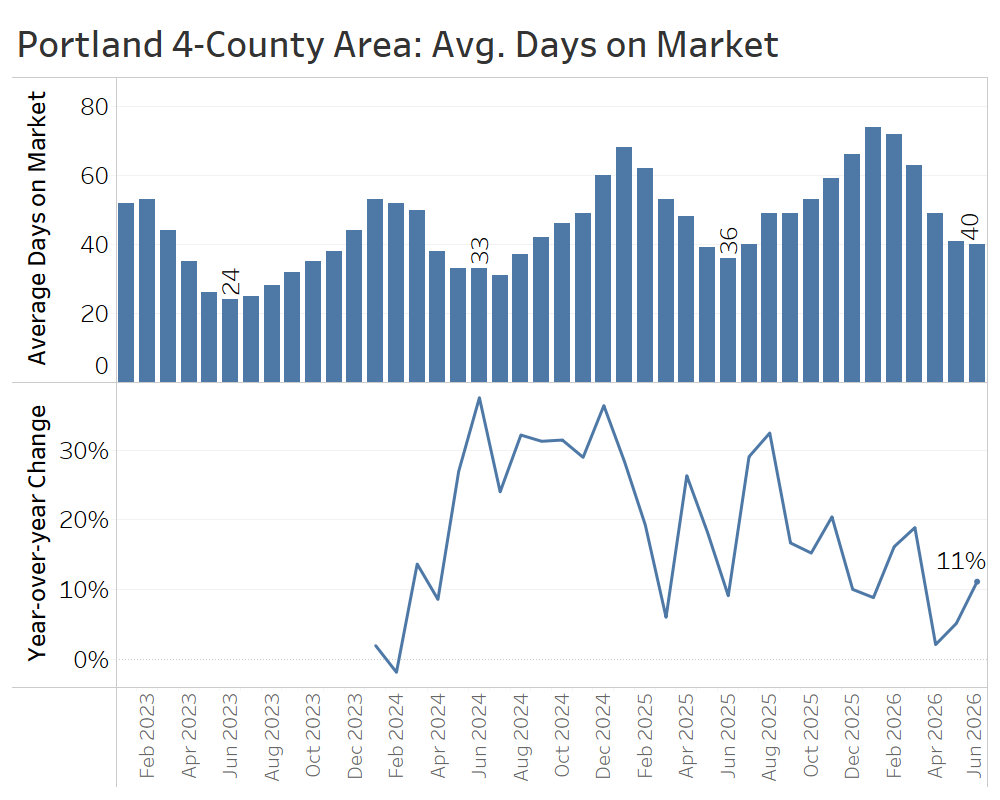

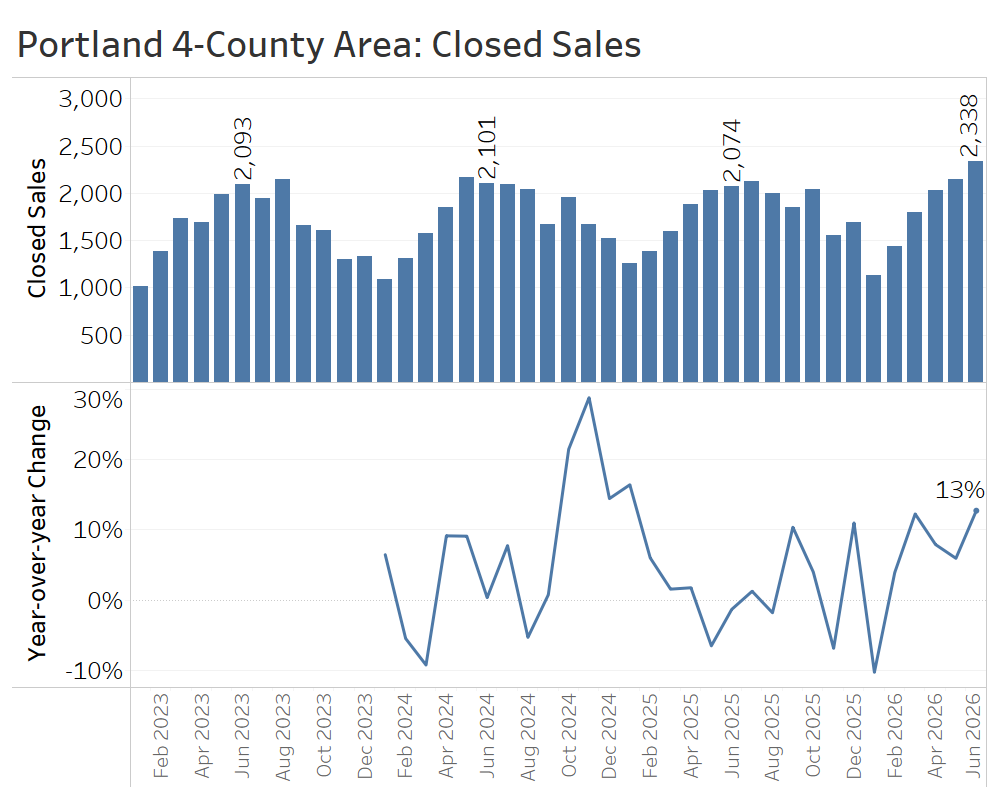

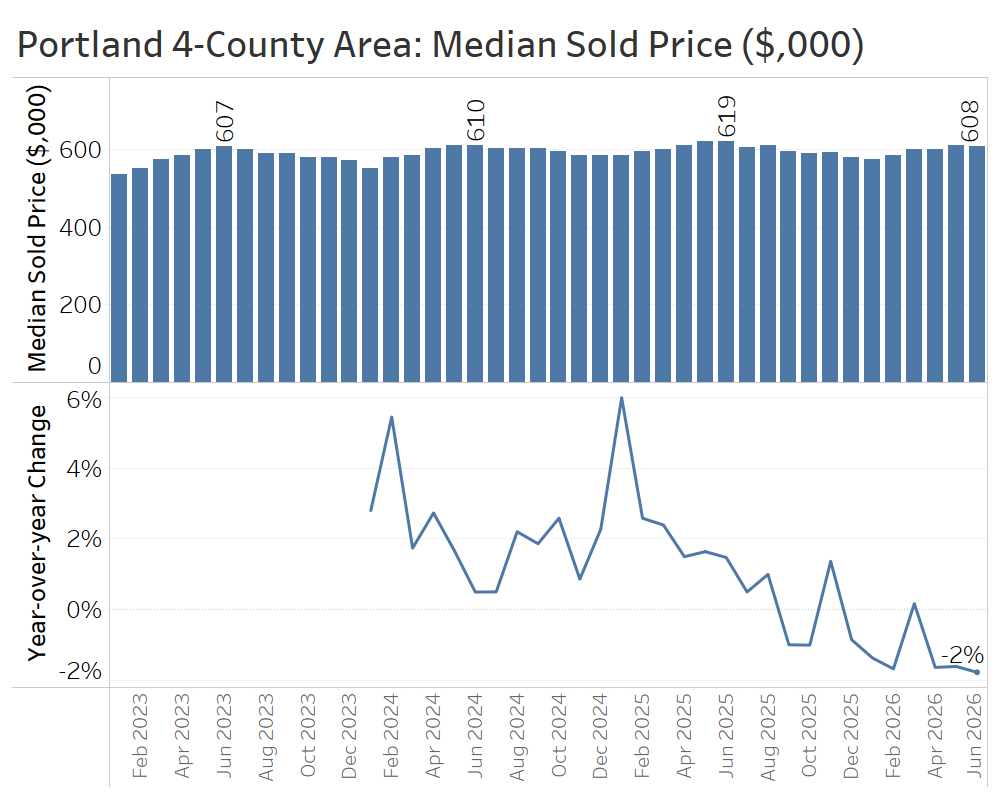

Greater Portland Area (Multnomah, Washington, Clackamas, and Clark Counties)

The greater Portland area began to swing from a buyer’s market back into balance, as inventory actually fell year over year, and sales began to climb.

Active listings fell below year-ago levels in April, and by the end of June were 6% lower than at the midpoint of 2025.

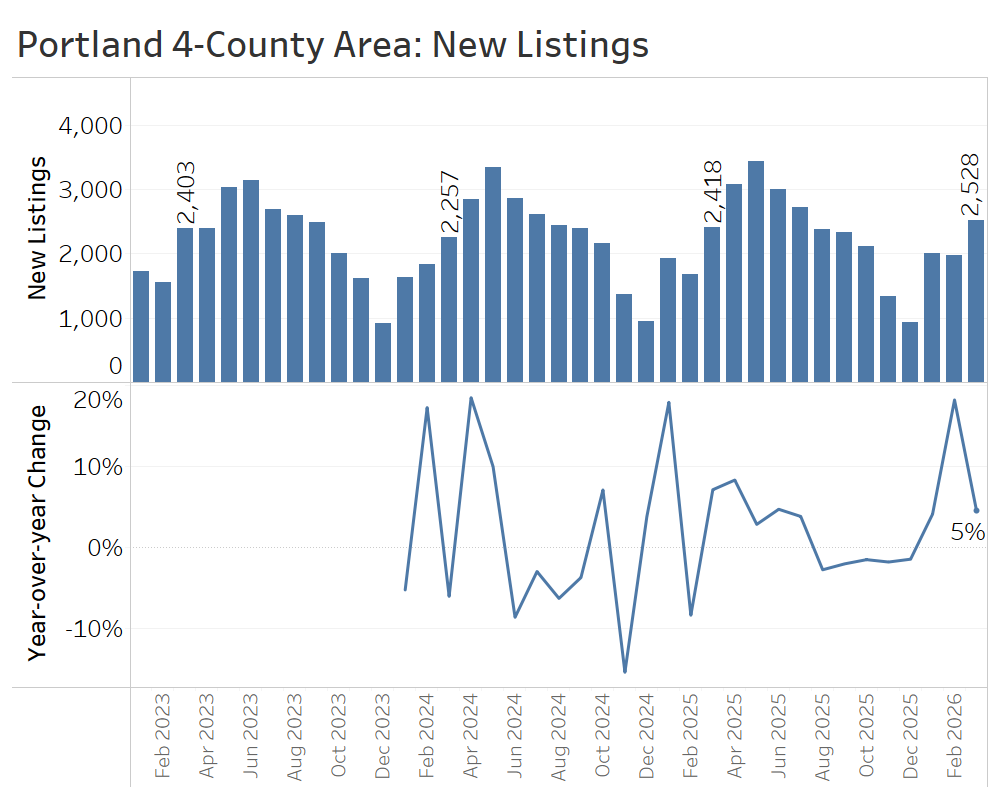

The flow of new listings contracted slightly, with 2% fewer new listings in the second quarter than in the same quarter of 2025. That modest inflow helped set the stage for the decline in active listings by midyear.

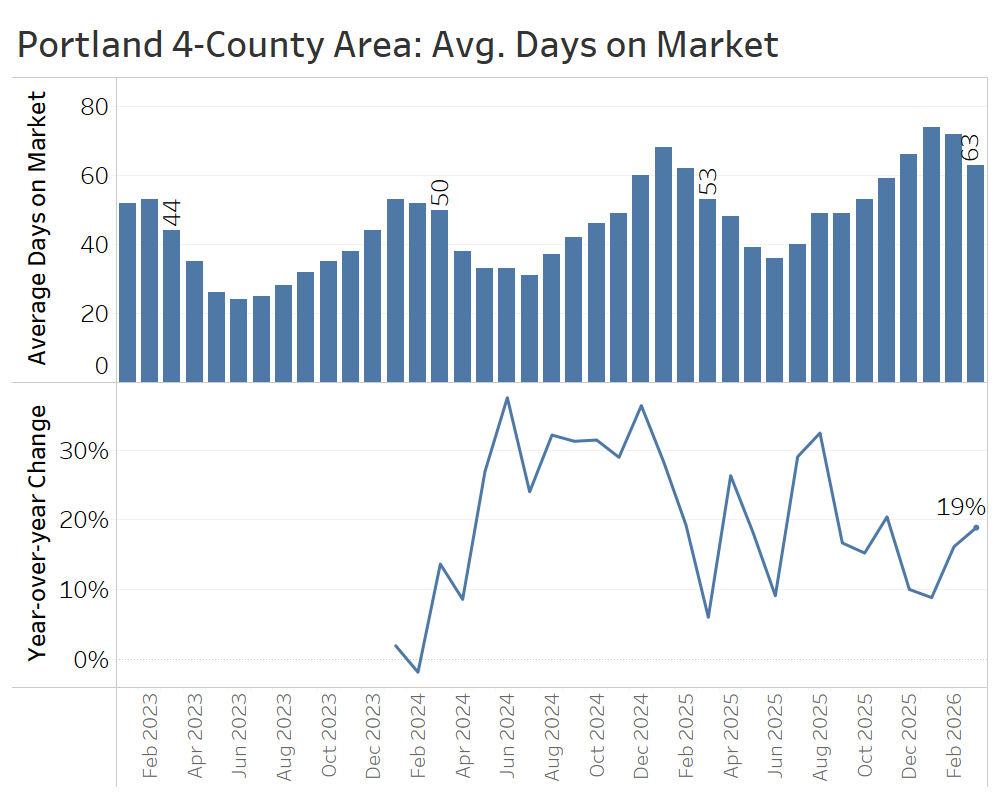

Homes sold faster than they did during the winter months, but the June data still point to a slower market than a year ago, with buyers taking more time and sellers facing greater price competition.

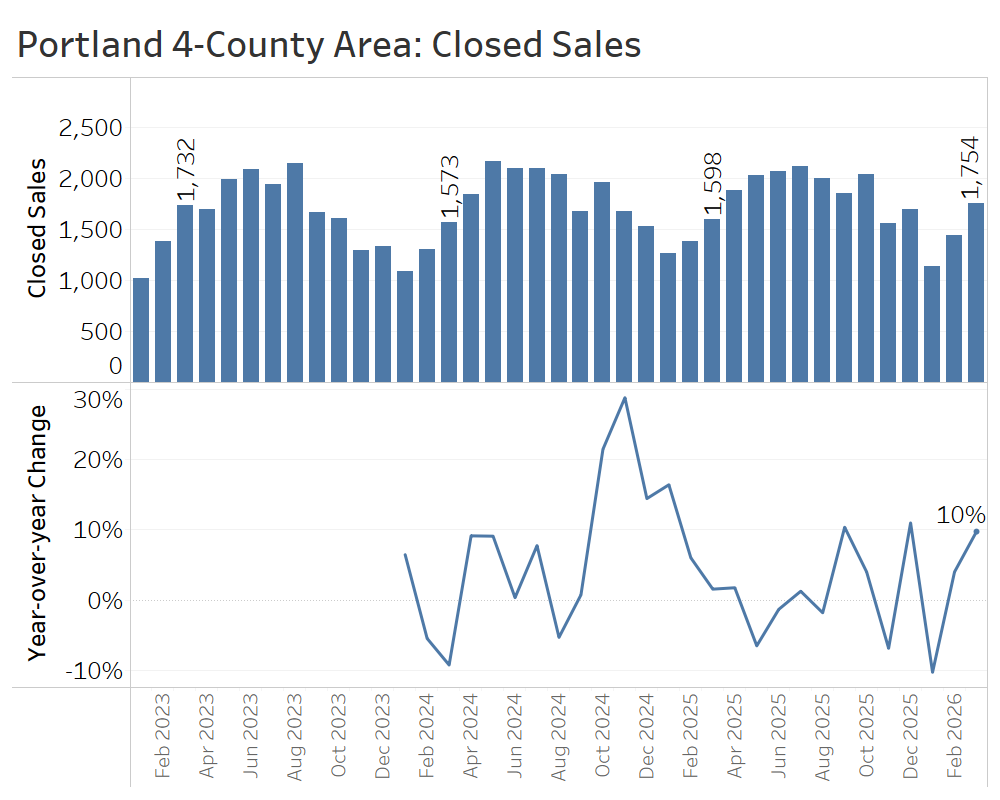

Sales activity climbed at an impressive pace, with 9% year-over-year growth for the quarter as a whole, including a 13% increase in June as compared to last year.

Median sale prices slightly lagged behind year-ago levels, with declines of about 2% year over year throughout the second quarter. That reflects the still-ample supply of listings to choose from, which kept the demand rebound from reigniting price growth…for now.

Portland’s second-quarter market looked balanced, with stable, still-reasonable pricing, stronger sales activity than we’ve seen in quite some time, and enough inventory to keep sellers from regaining clear leverage.

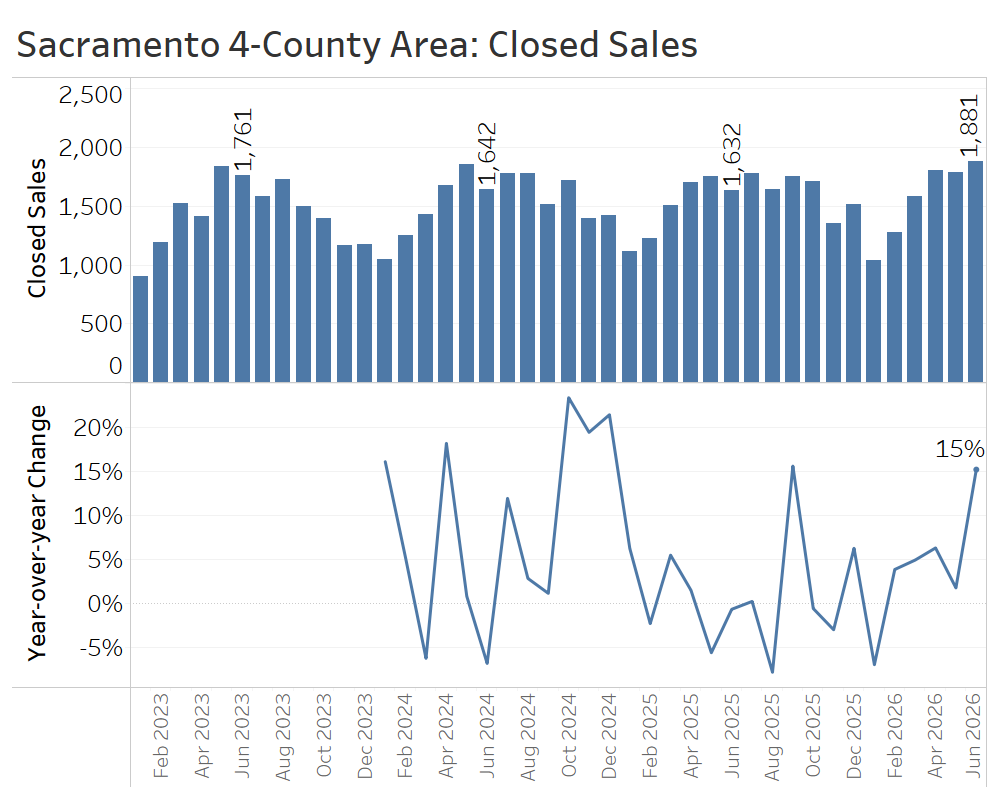

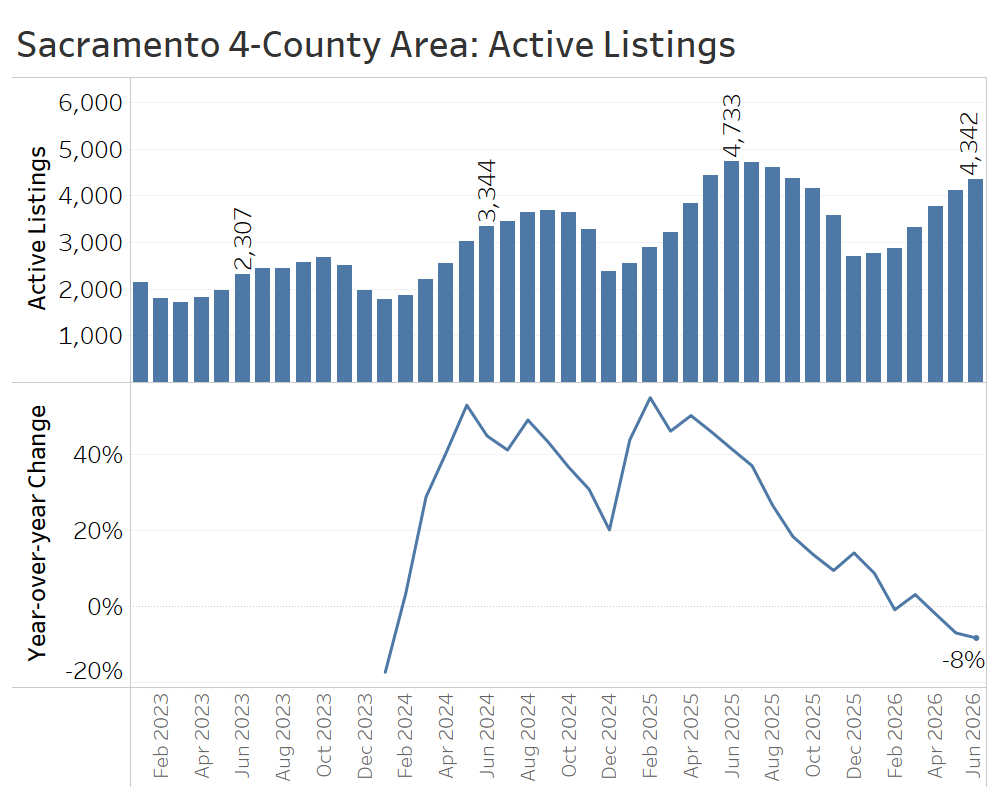

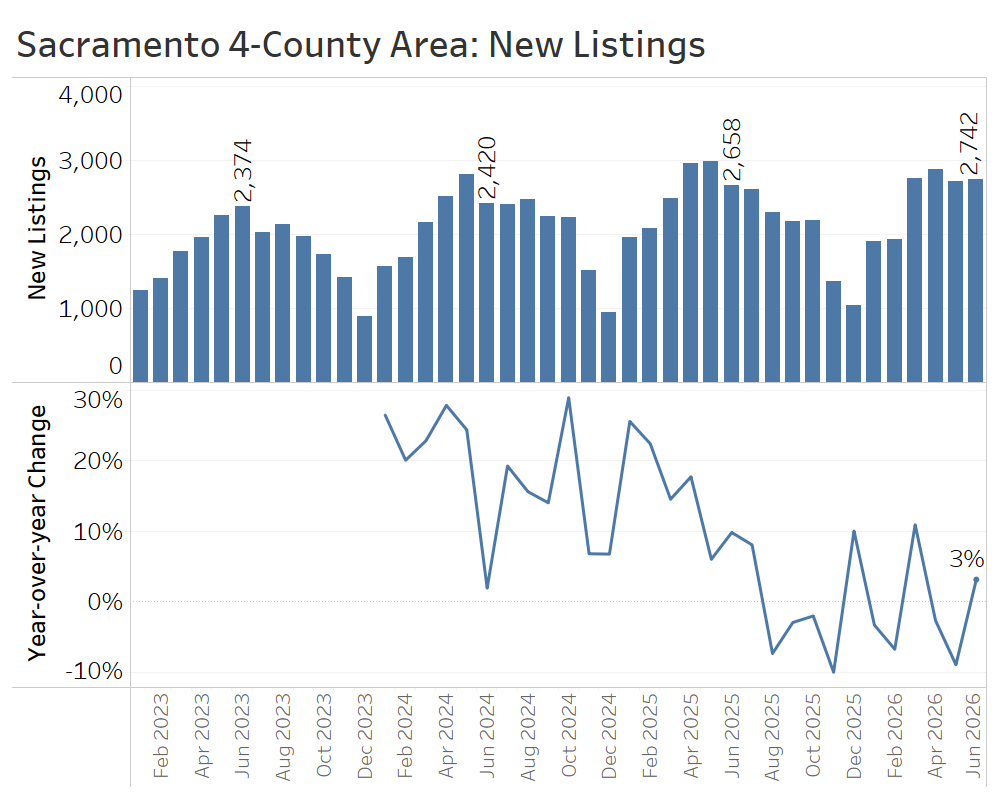

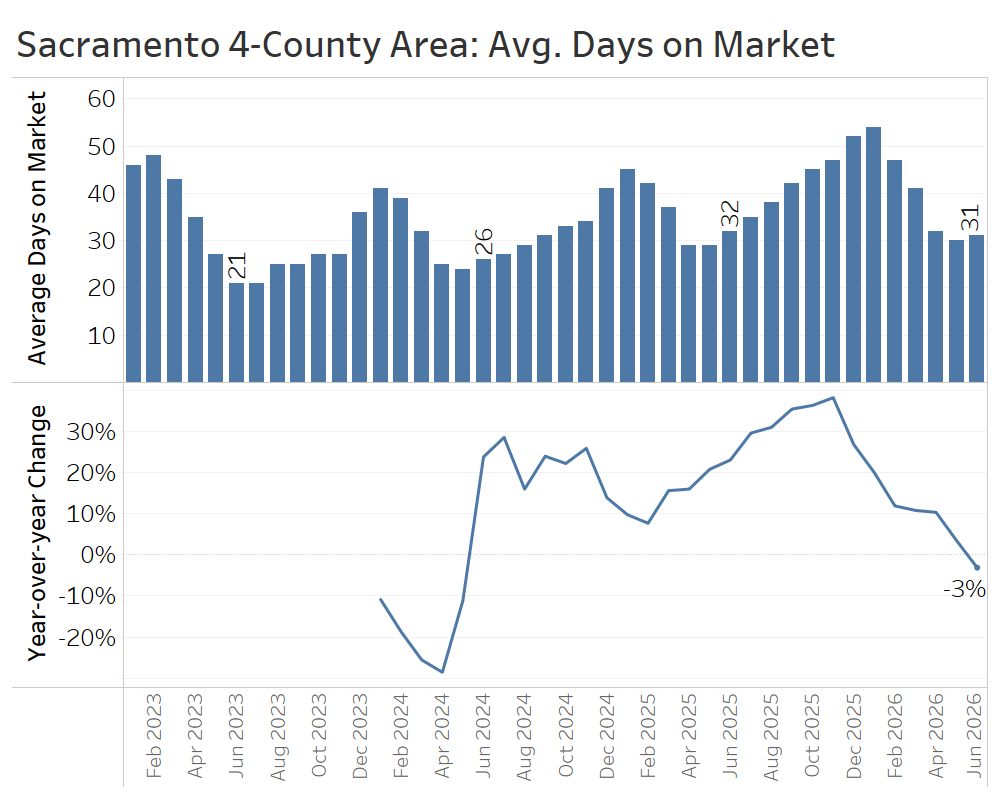

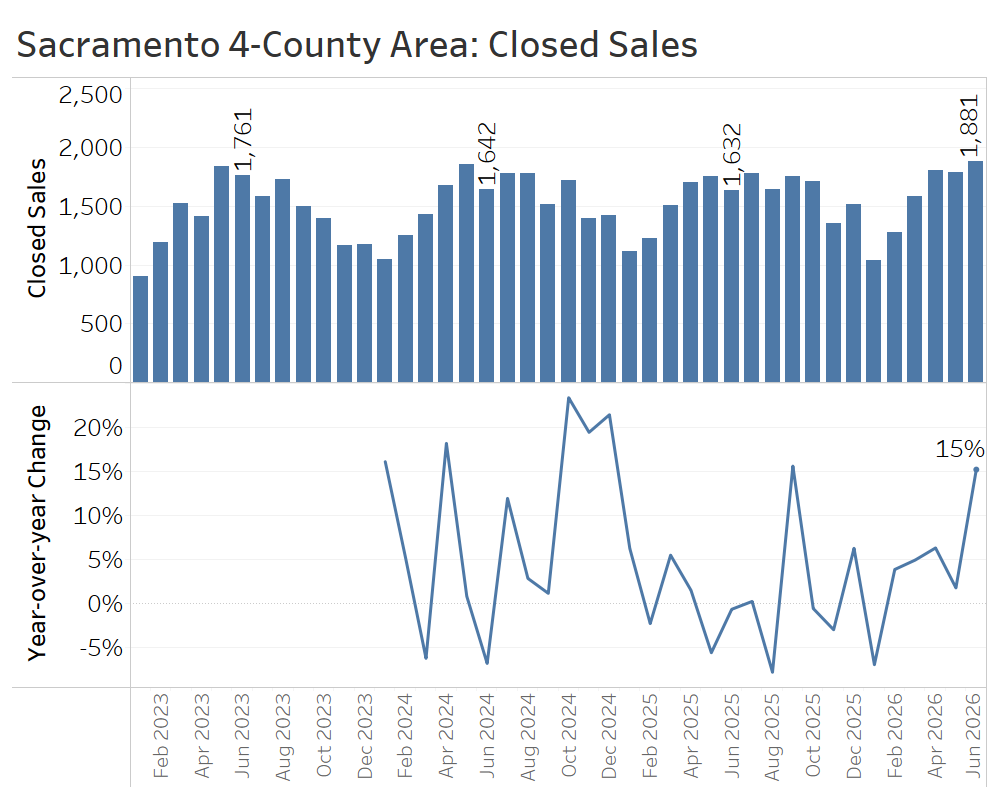

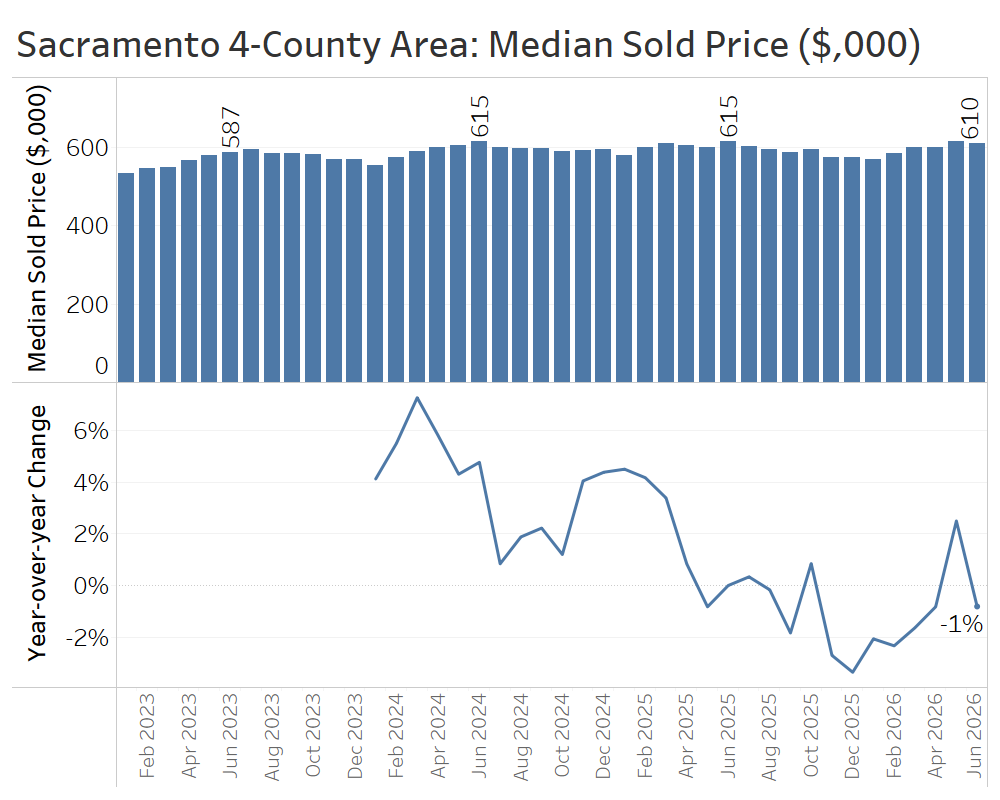

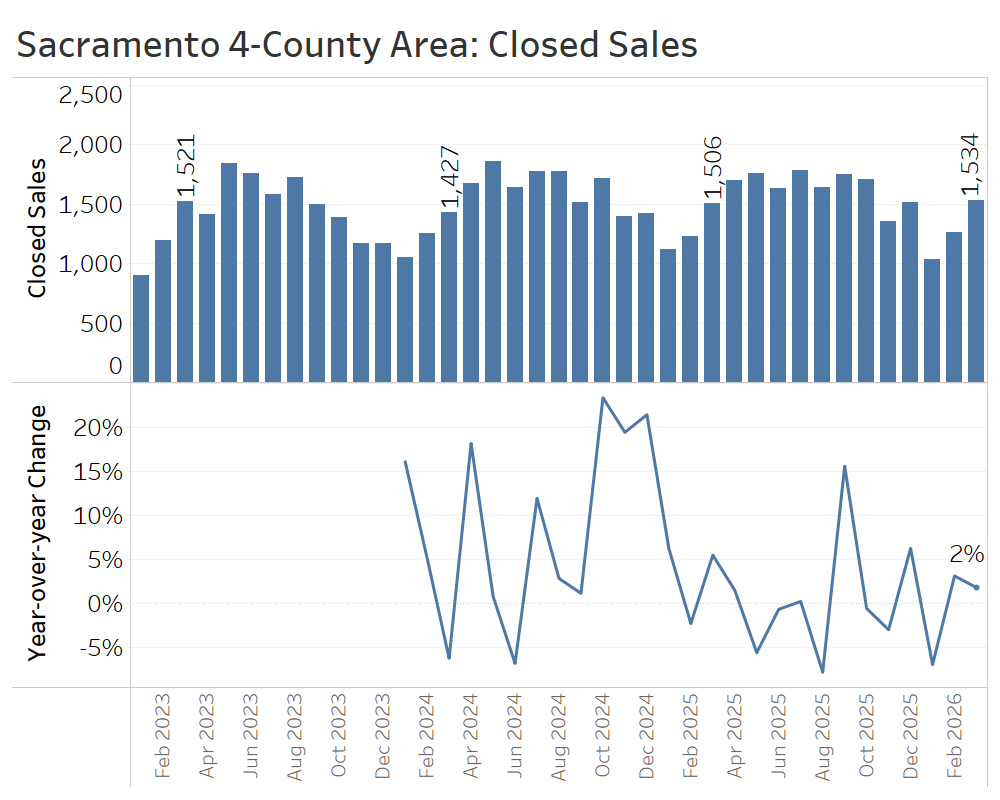

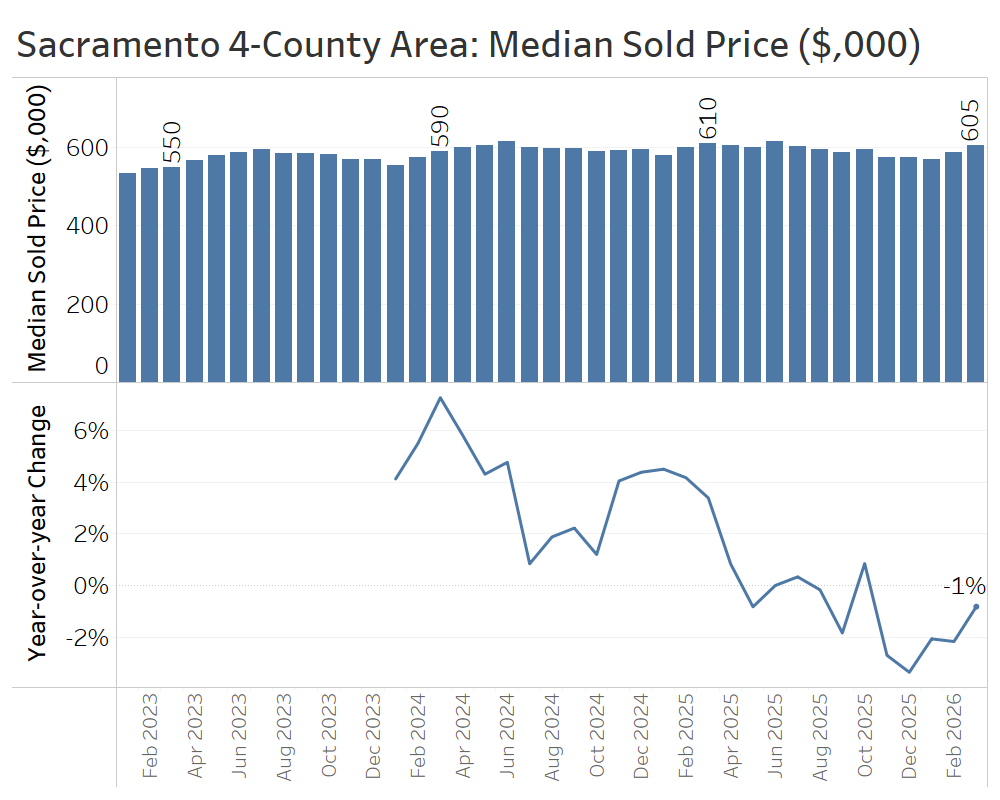

Greater Sacramento Area (Sacramento, Yolo, El Dorado, and Placer Counties)

The greater Sacramento area continued to show signs of swinging back toward balanced activity in the second quarter after shifting toward buyers during 2025.

By June, active listings were 8% below last year’s level, which had set a new cycle high of more than 4,700 homes for sale. This continued a trend of decelerating inventory growth, which moved past zero into modest inventory decline.

New listings remained volatile month to month, but the second quarter as a whole had 3% fewer new listings hit the market than in the second quarter of 2025. That has certainly contributed to the inventory slowdown noted above.

Average days on market fell below year-ago levels in June, marking the first year-over-year decline in time on market since 2024. That represents another major milestone in the shift away from a buyer’s market.

Closed sales climbed over the second quarter, particularly with June’s impressive year-over-year gain of 15%. Altogether, the quarter had 8% more closed sales than the same quarter last year, marking a major pickup in sales activity.

Median sale prices recovered from seasonal winter lows but remained close to year-ago levels: slightly higher in May but slightly lower, year over year, in April and June.

All in all, Sacramento’s second-quarter data suggest that last year’s inventory growth is keeping a lid on pricing, but strong sales growth and a modest drop in time on market indicate that demand is now outpacing supply.

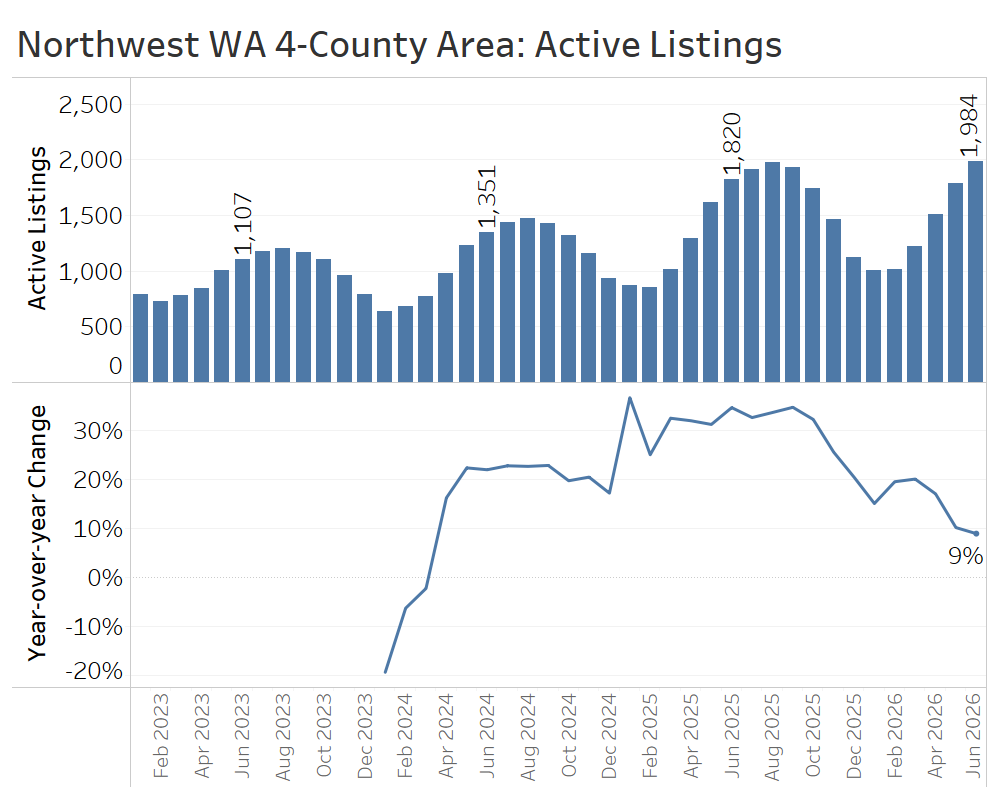

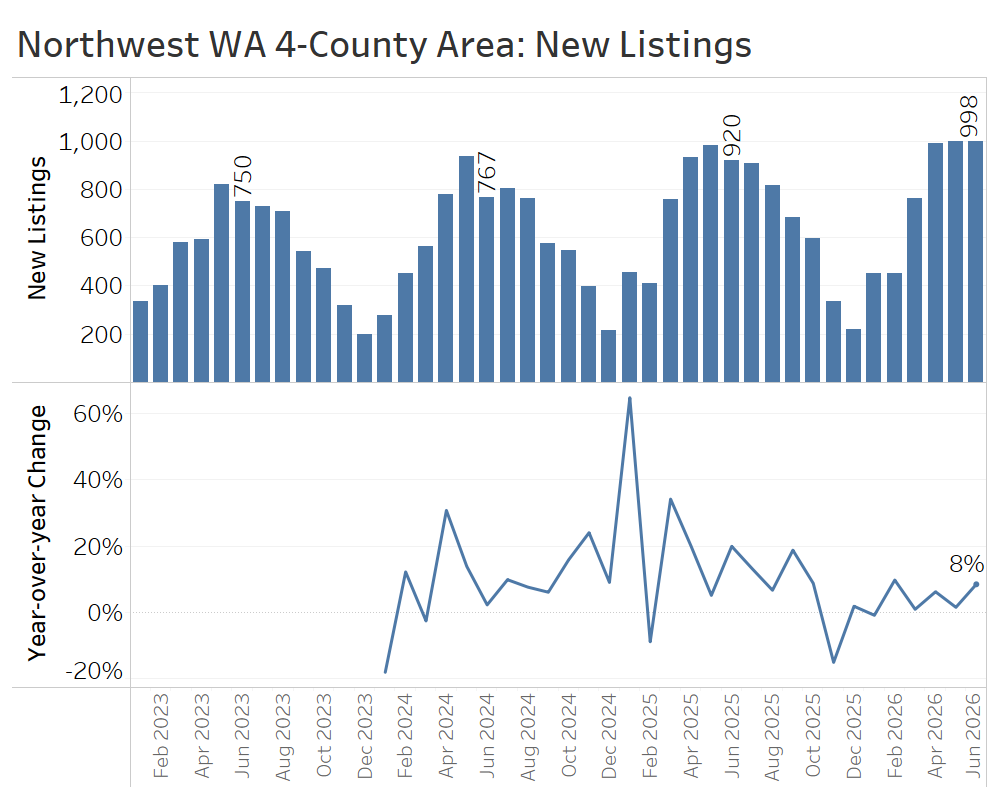

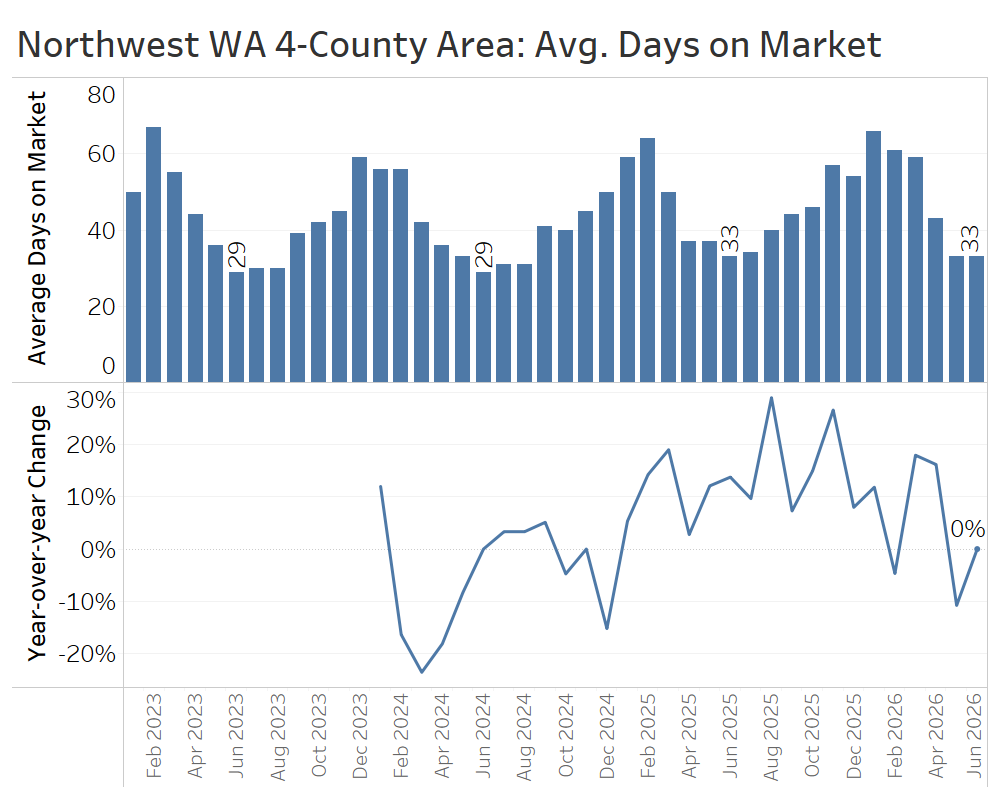

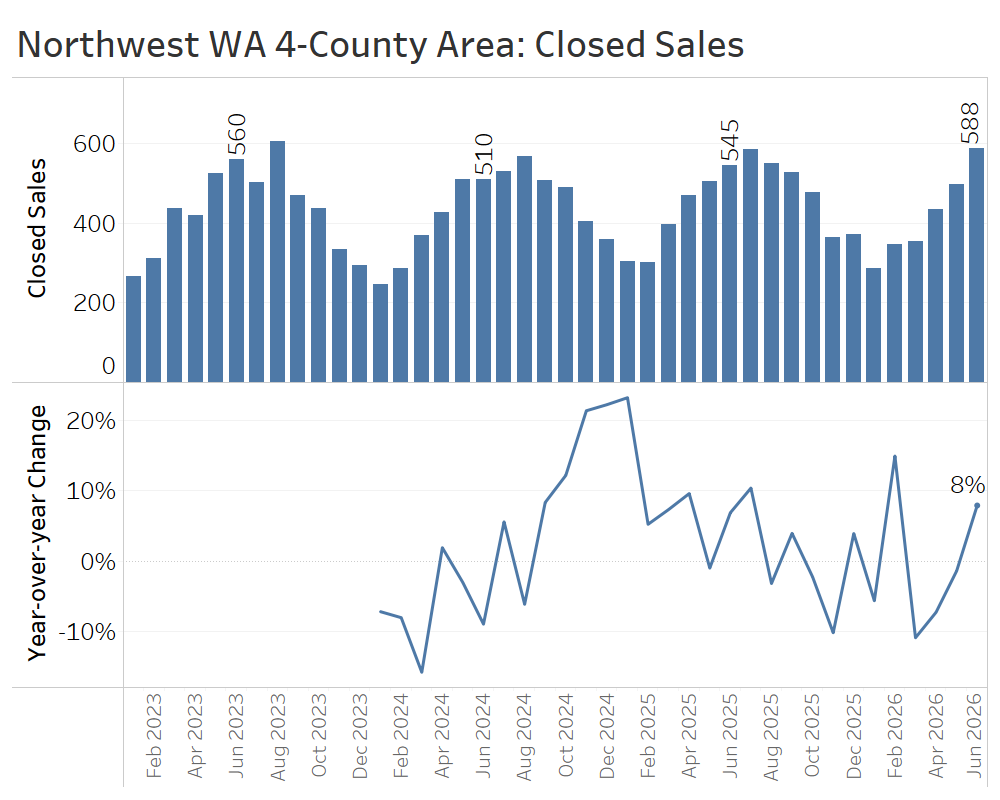

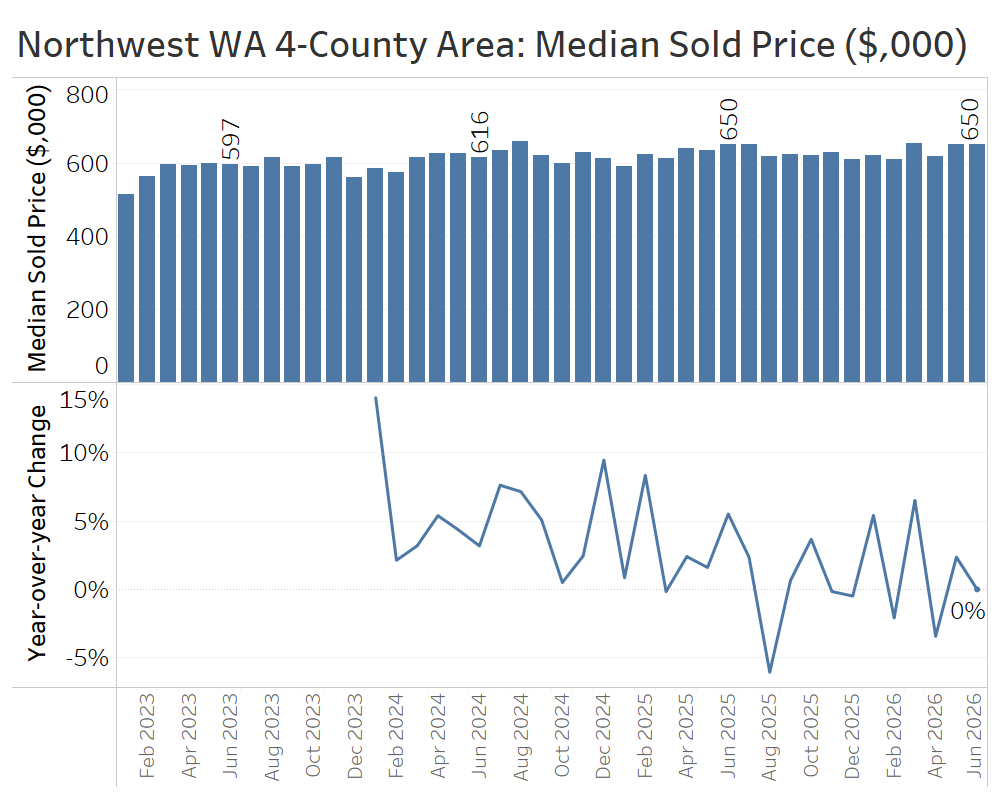

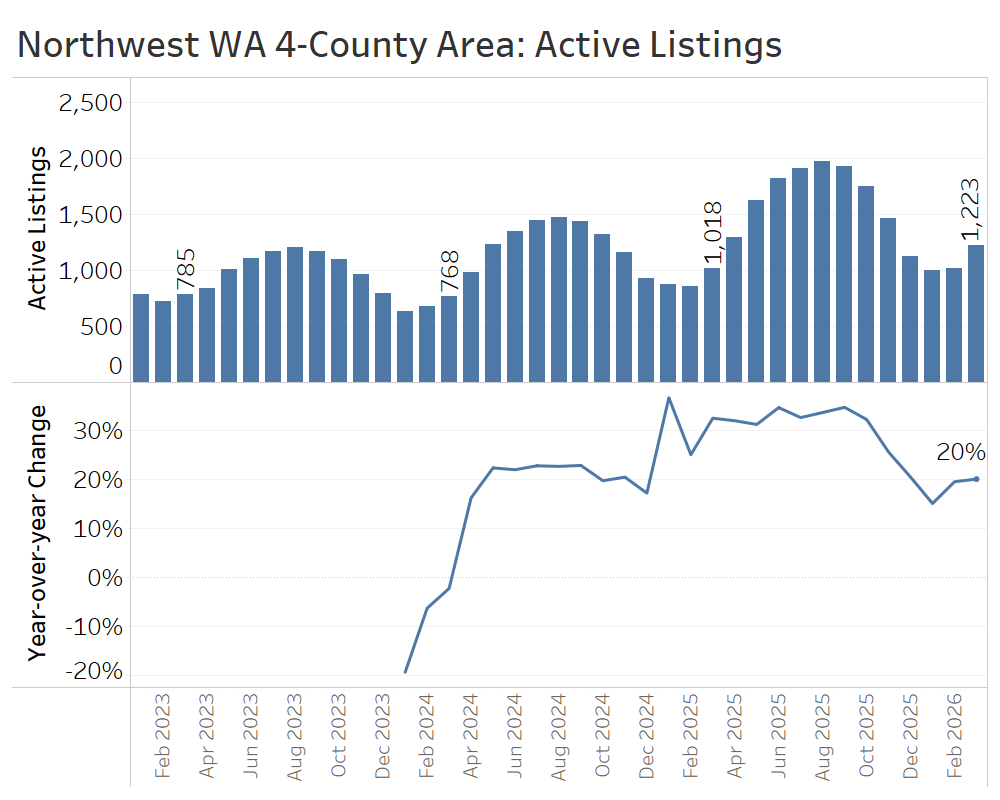

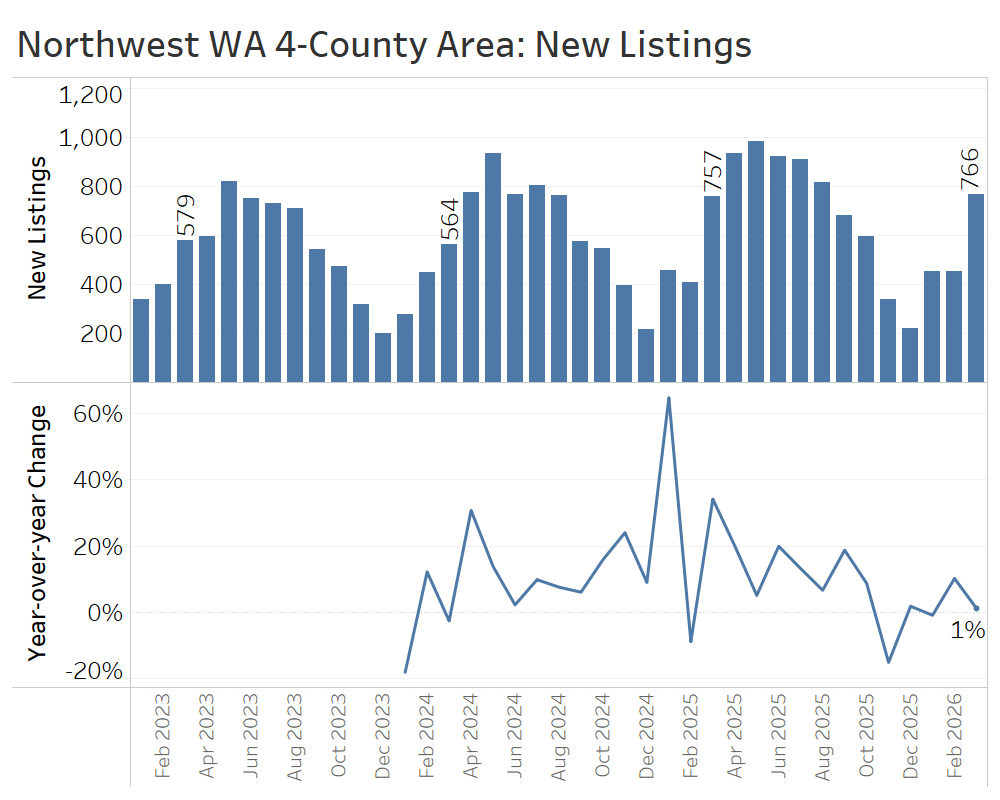

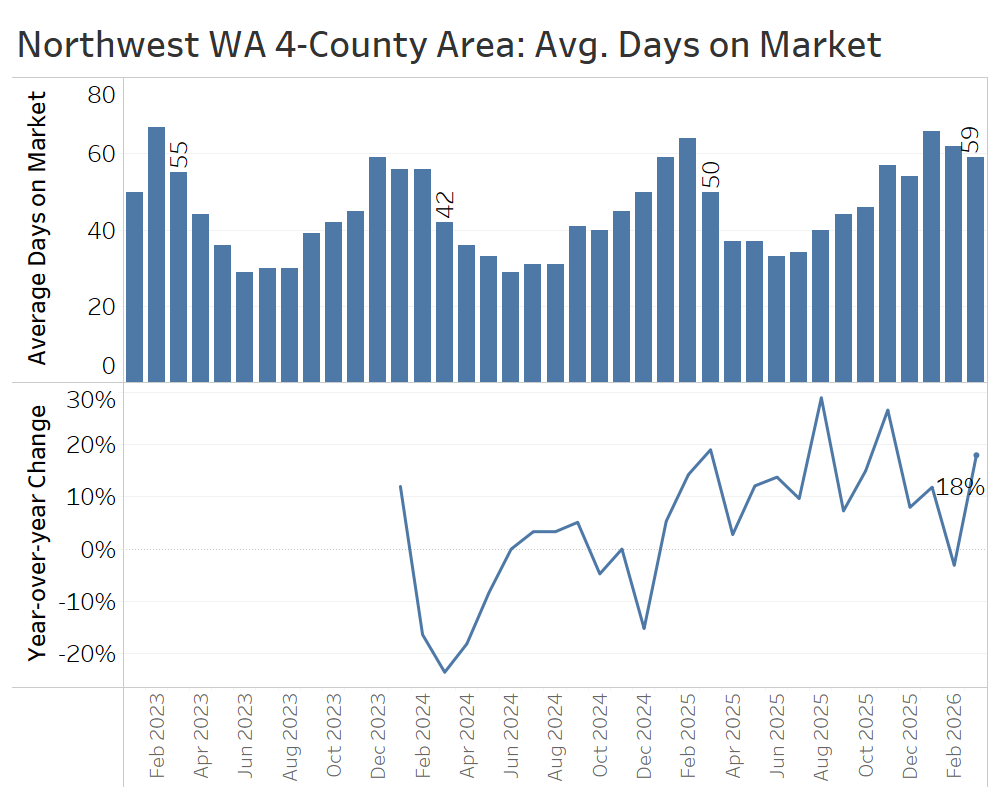

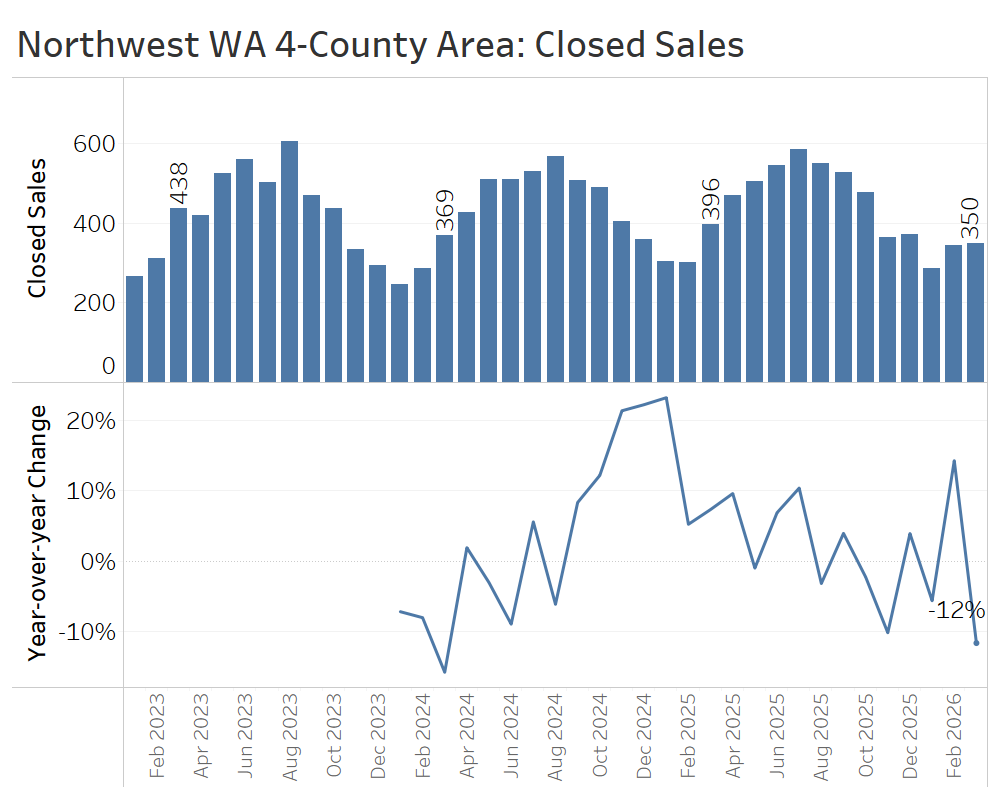

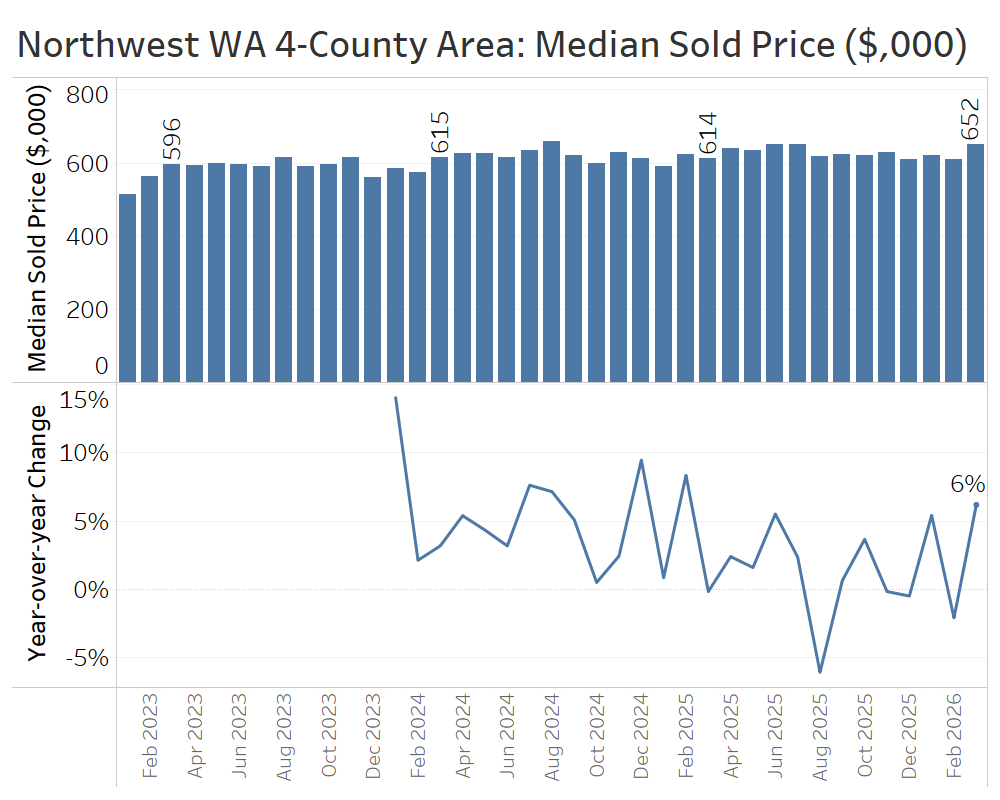

Northwest Washington (Skagit, Whatcom, San Juan, and Island Counties)

Market conditions in the four northernmost counties of Western Washington continued to tilt toward buyers through the second quarter.

Active listings in June remained meaningfully higher than a year earlier, although the year-over-year growth rate decelerated to just 9% in June.

The flow of new listings kept growing, with 5% more new listings over the quarter than the same time last year.

Days on market dipped below year-ago levels in May and matched them in June, suggesting some stabilization in the balance between supply and demand. Third quarter’s data will give a clearer answer as to whether this truly marks an inflection point of the market returning to balance.

Closed home sales almost exactly matched last year’s second-quarter total, although sales volume grew sharply over the course of the quarter, culminating in strong 8% growth in June. This could signal a sales rebound in the third quarter, as buyers begin to take note of the favorable market conditions.

Median sale prices were mostly flat, holding onto 2025’s modest pricing gains over the previous two years.

Overall, the second-quarter data show that the Northwest Washington housing market remains tilted in buyers’ favor, but with some early indications that it may be starting to swing back toward balanced conditions.

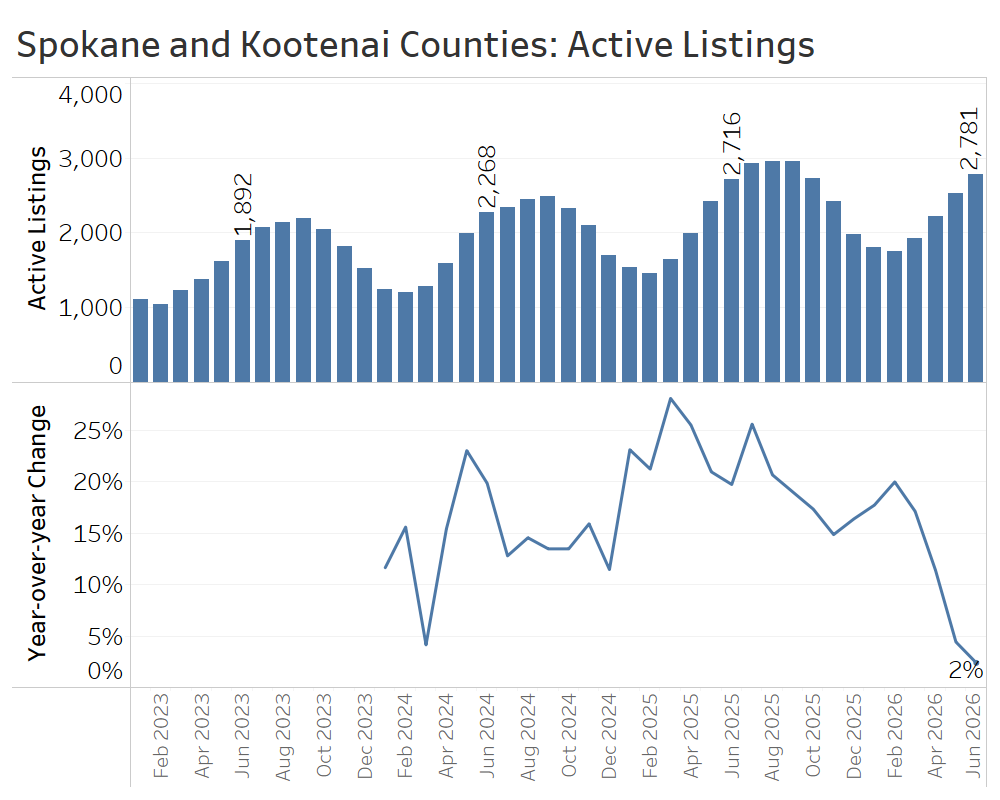

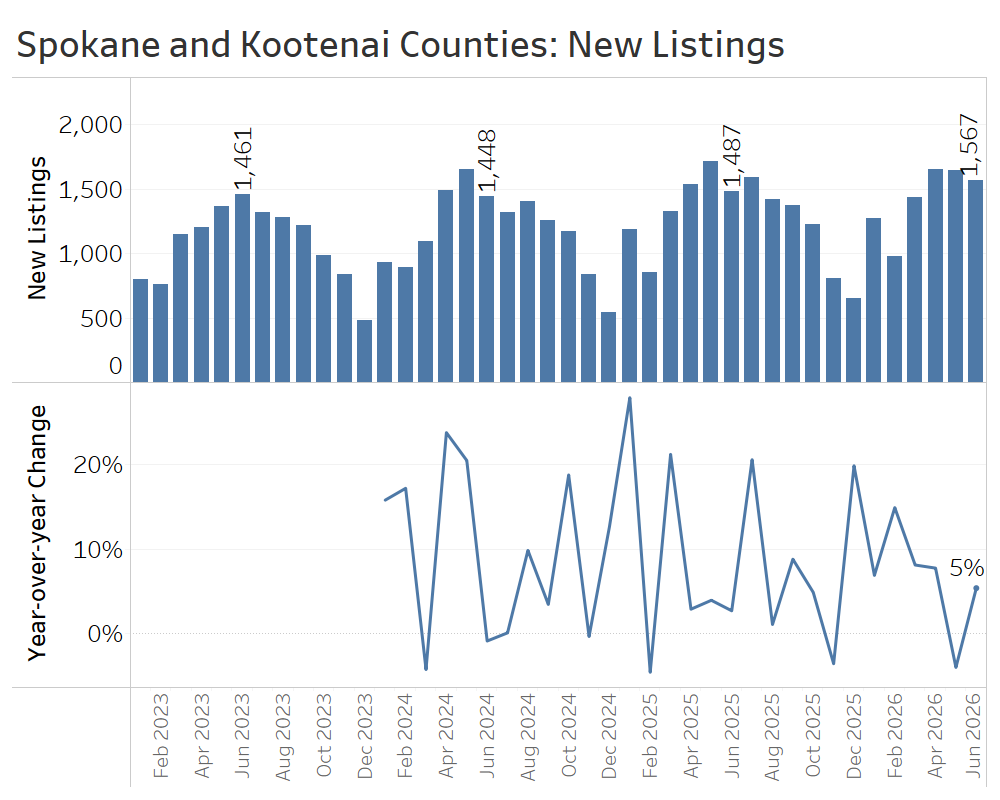

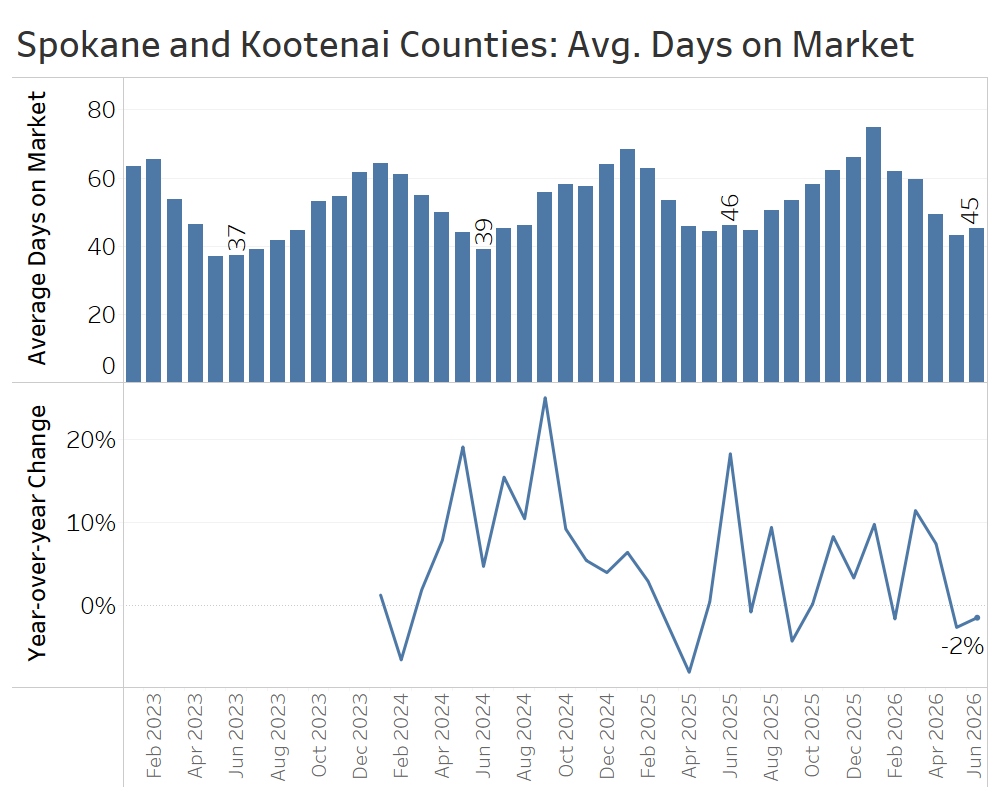

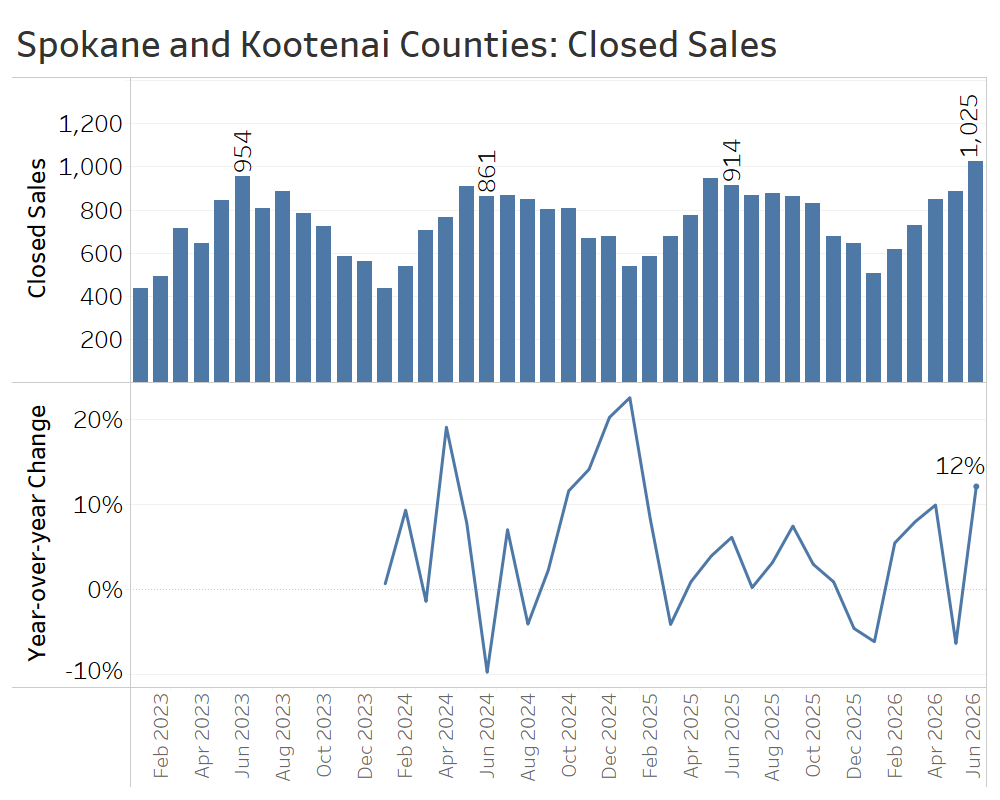

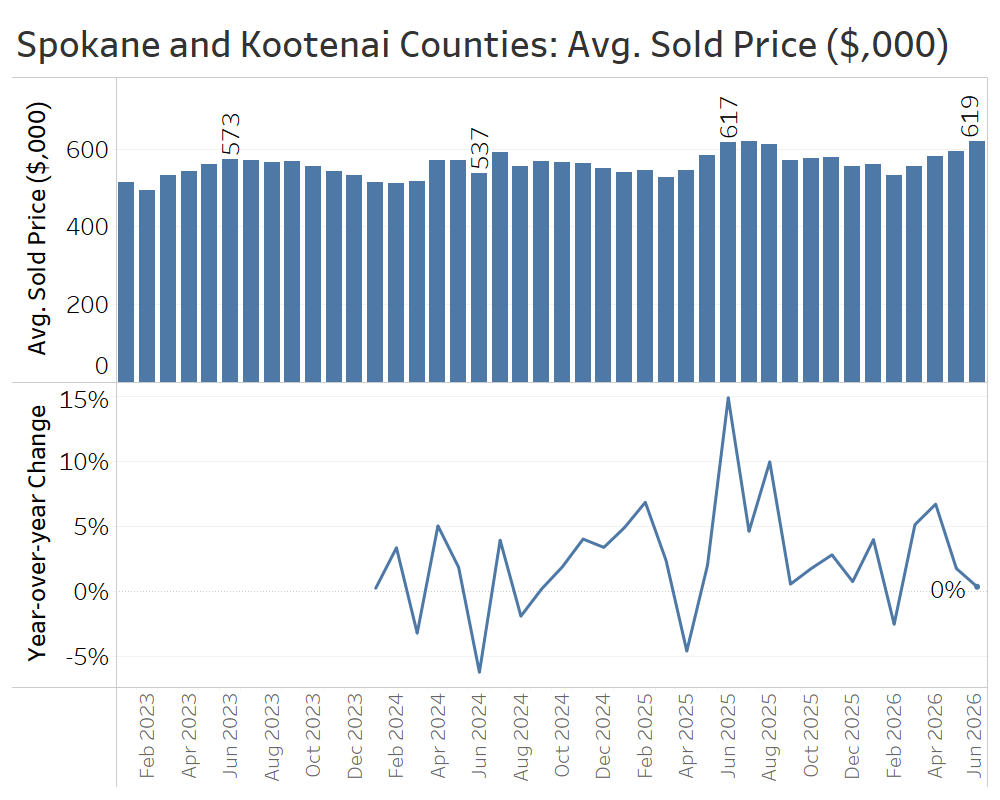

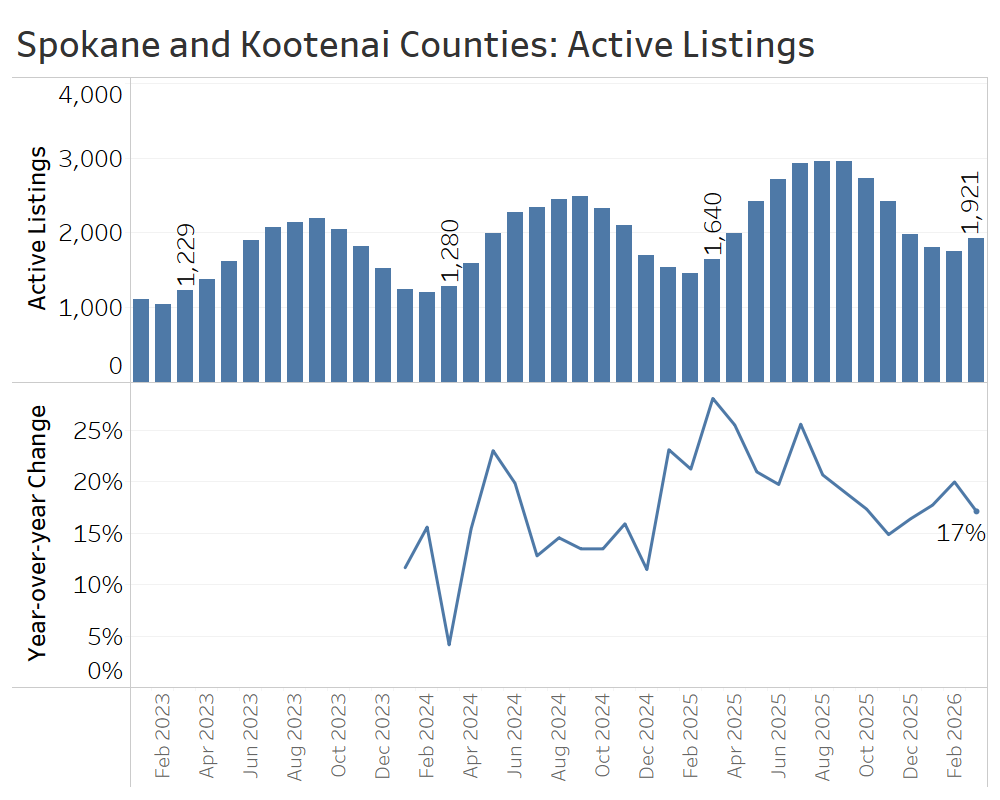

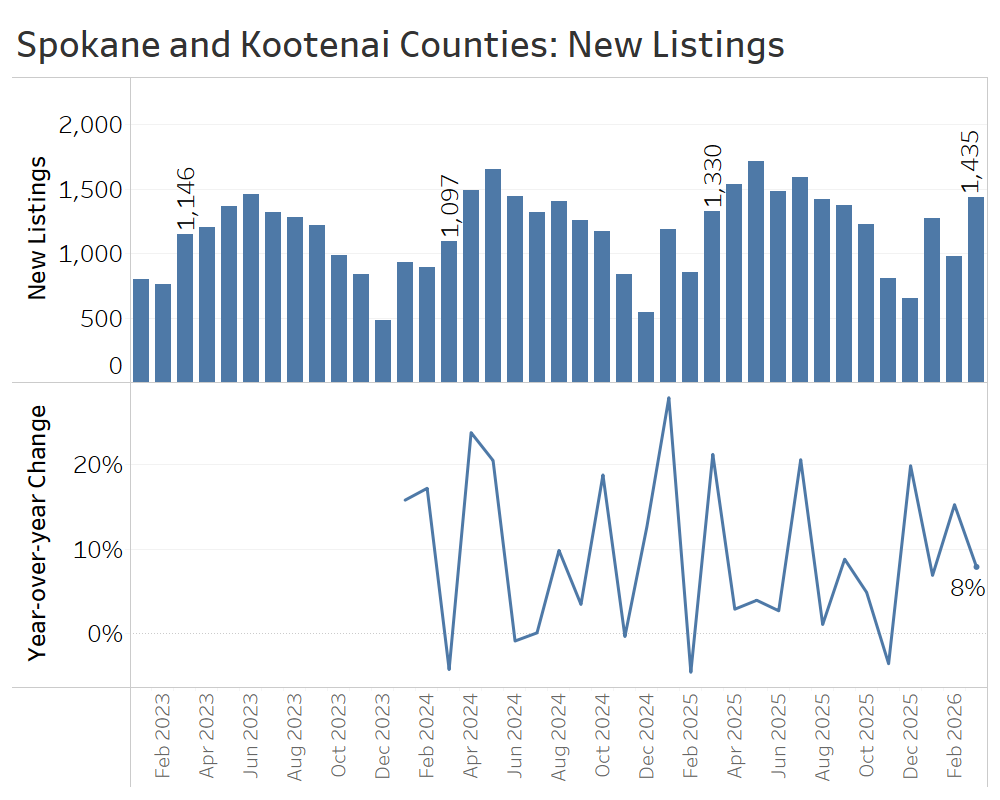

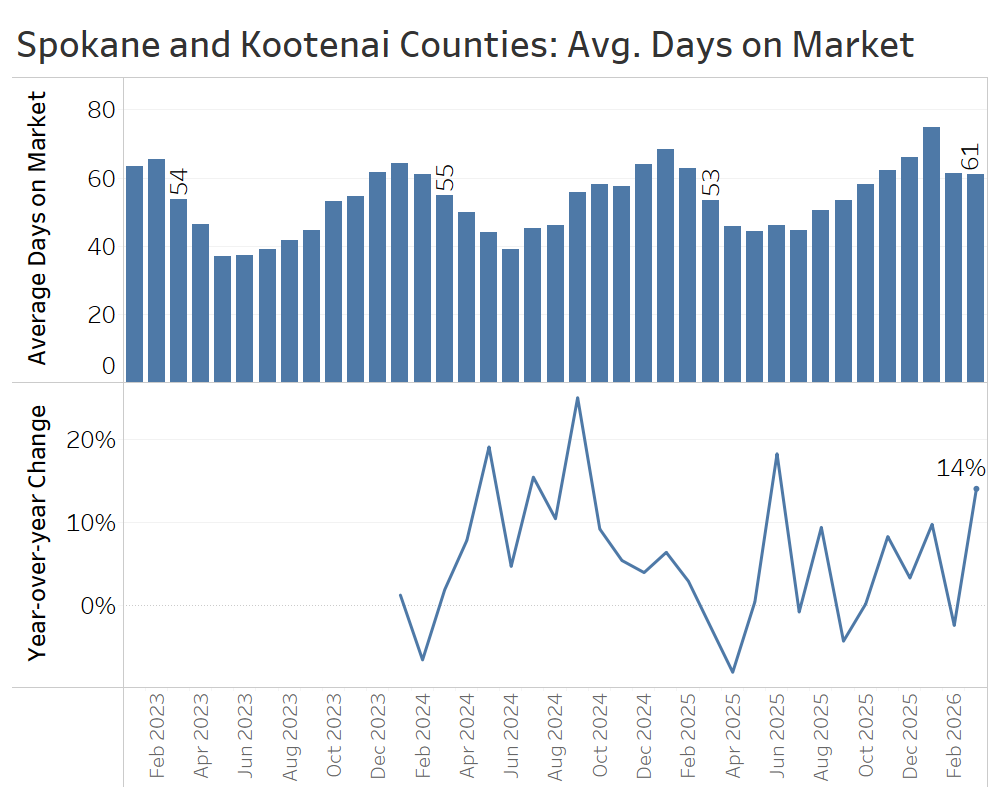

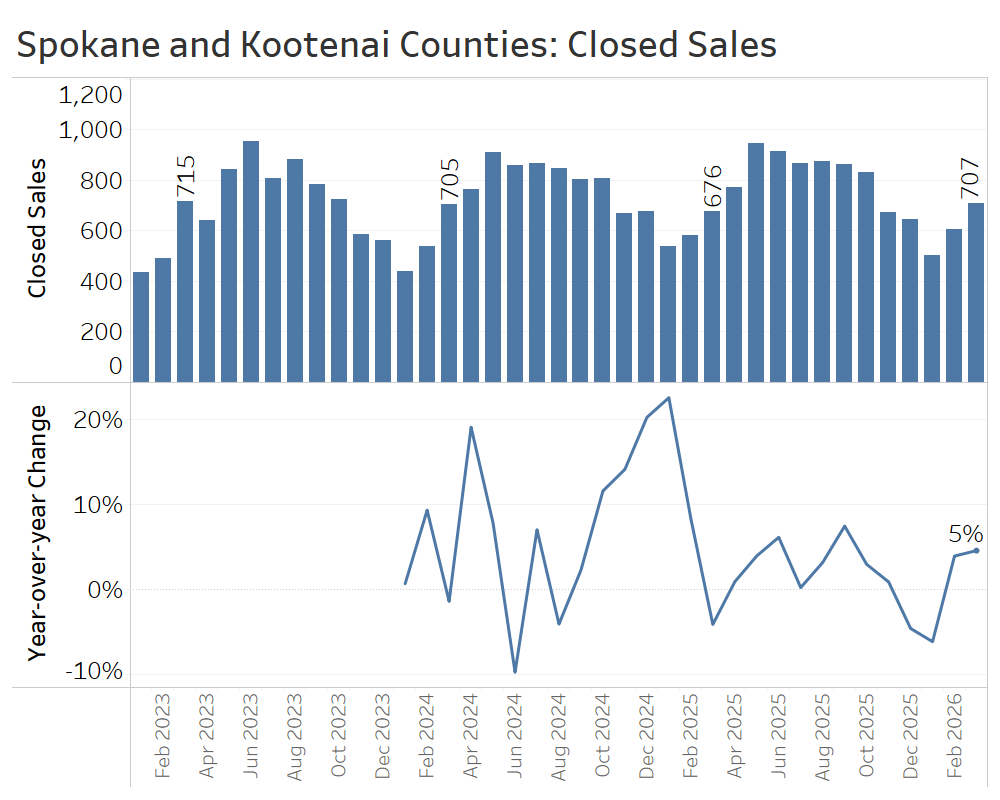

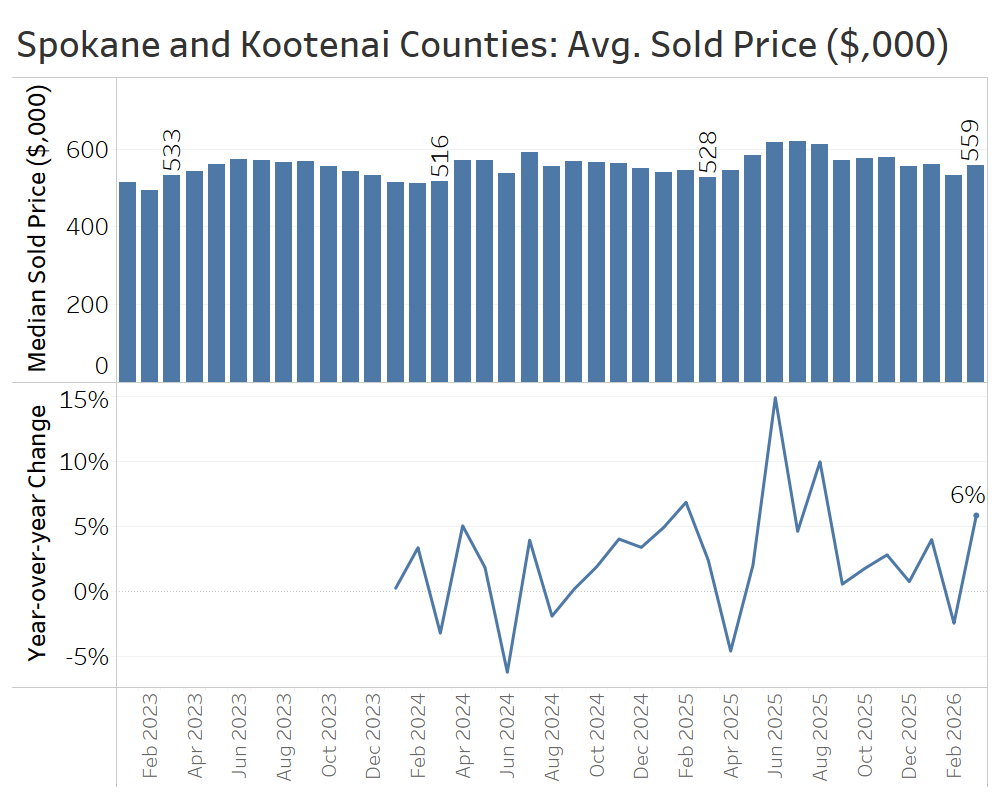

Spokane, WA and Coeur d’Alene, ID Area (Spokane and Kootenai Counties)

The greater Spokane-Coeur d’Alene region, spanning the Washington-Idaho border, looked like a balanced-to-seller-friendly market in the second quarter, as inventory growth cooled and sales activity hummed higher.

Active listings in June were just barely (2%) higher than year-ago levels, after years of double-digit growth that continued through the first quarter of 2026.

New listings were slightly higher than year-ago totals, with 3% more listings for the quarter as a whole, helping to replenish supply despite healthy sales activity.

Days on market dipped below year-ago levels in May and June, a major milestone that suggests a shift away from buyer-friendly conditions and reflecting renewed buyer demand.

Closed sales for the quarter were up 5% year over year, building on gains from the previous year and marking a major pickup in sales activity after a sluggish winter in the region. June’s total of more than 1,000 single-family homes sold was particularly impressive, coming in 12% above last June’s total and indicating strong sales momentum heading into summer.

Average sale prices were up in April and May but roughly flat year-over-year in June, showing that the ample inventory built up over the spring could help to blunt the risk of price appreciation as demand grows, at least for now.

Altogether, the greater Spokane-Coeur d’Alene area looked balanced through the second quarter, with modest gains in sales and prices but enough inventory growth to keep the market from overheating.

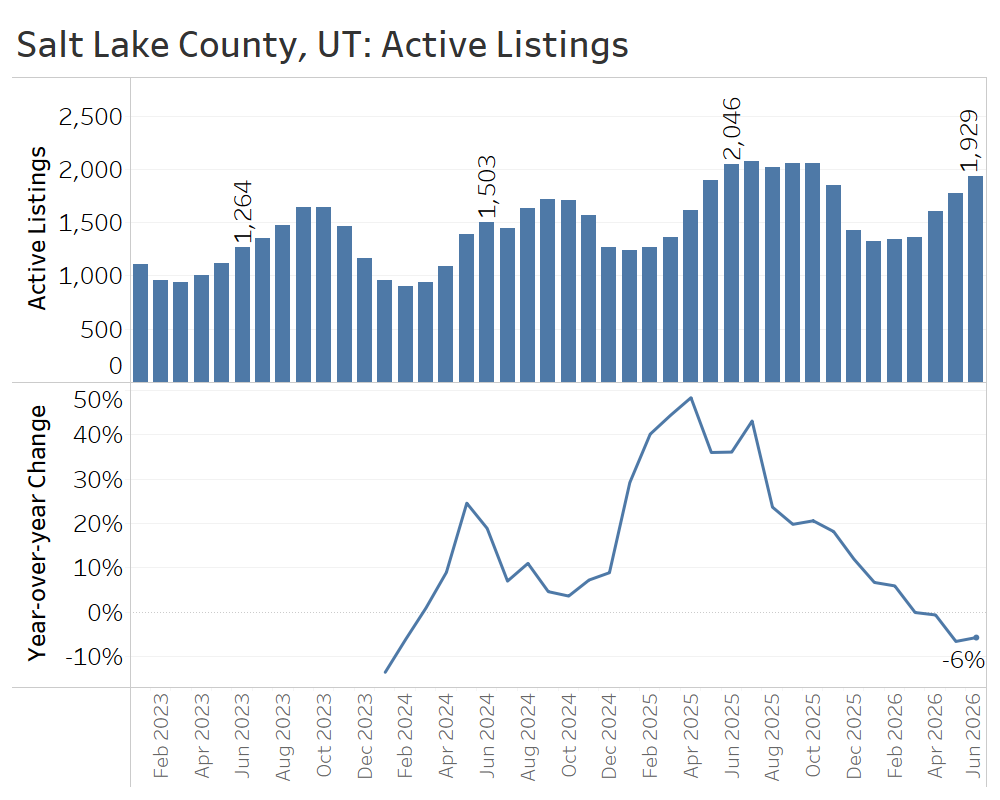

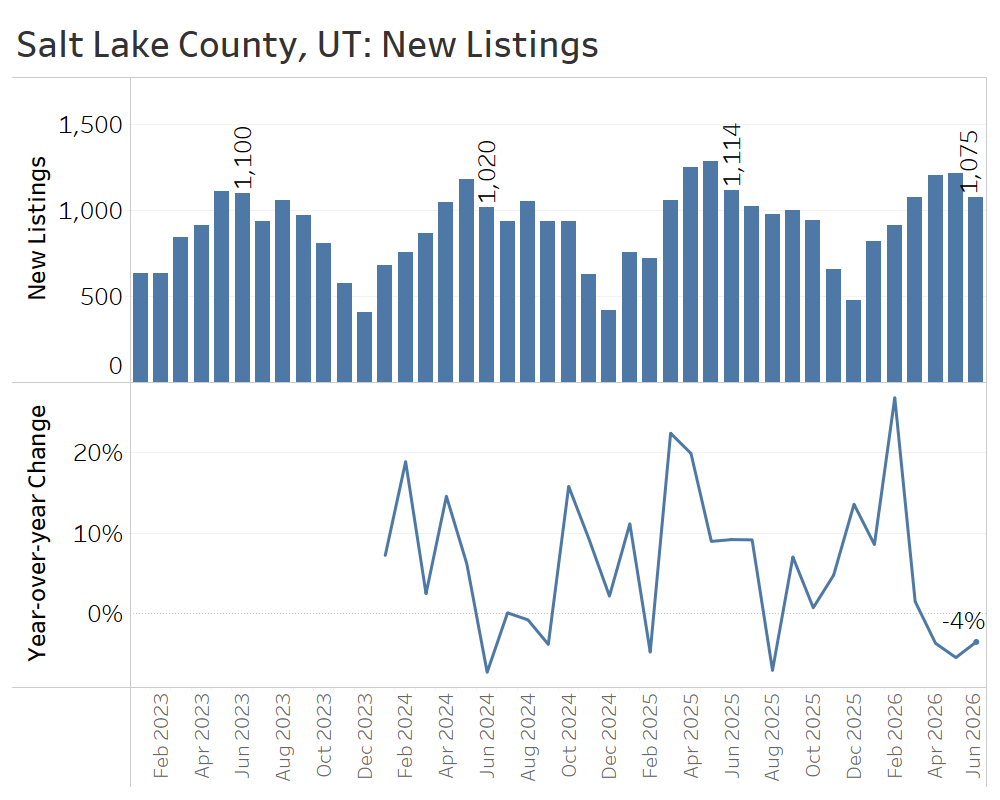

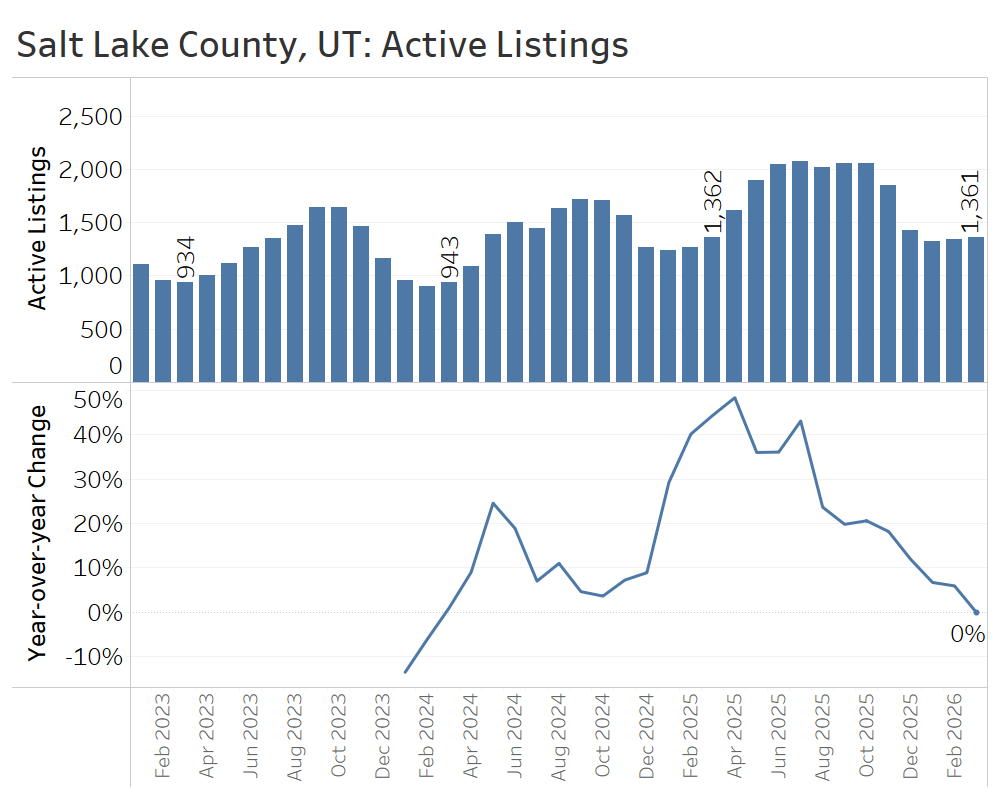

Salt Lake County, Utah

In the second quarter of 2026, the Salt Lake County market continued to show stronger sales activity than many of its peer markets, and inventory began to decline modestly.

Active listings ended the month of June 6% below year-ago levels, decisively closing the door on the prior two years of inventory buildup.

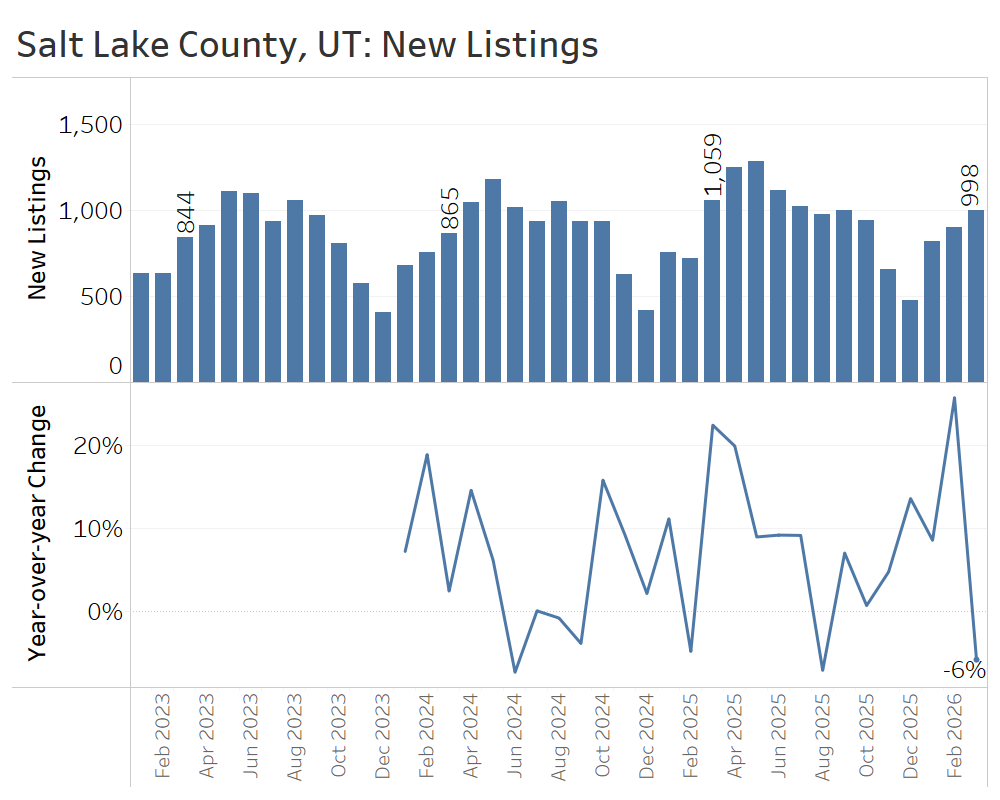

The reversal of inventory growth could be explained in part by the sudden dropoff of new listings. All told, the flow of new listings hitting the market declined by 4% from the same quarter last year.

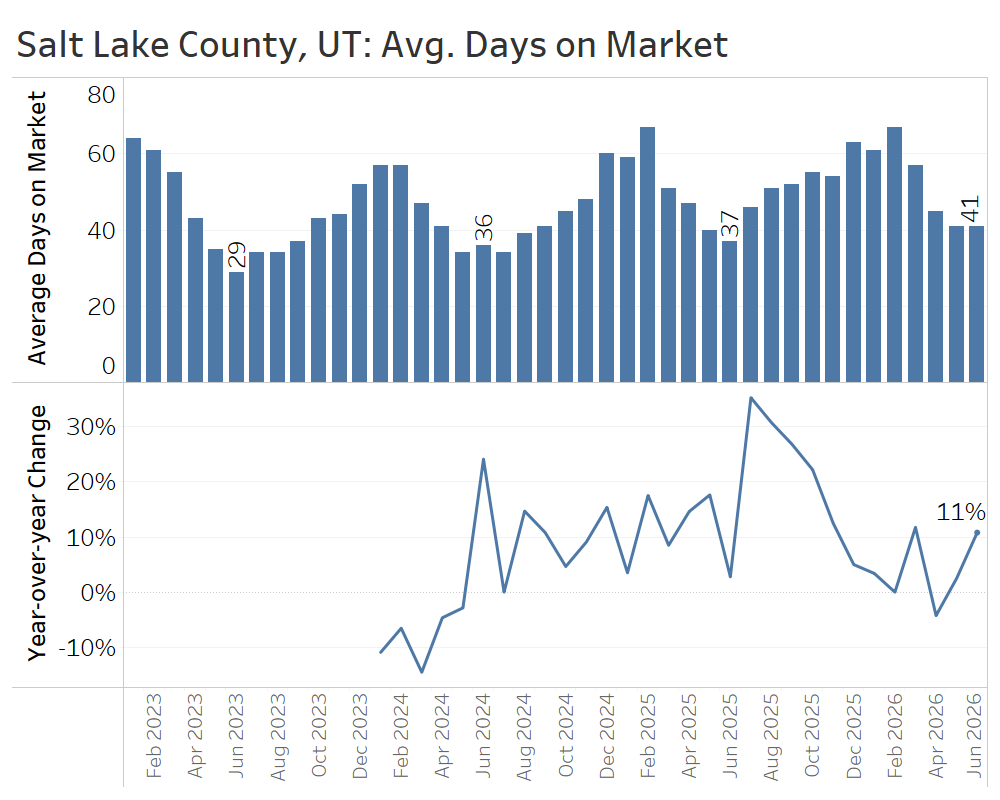

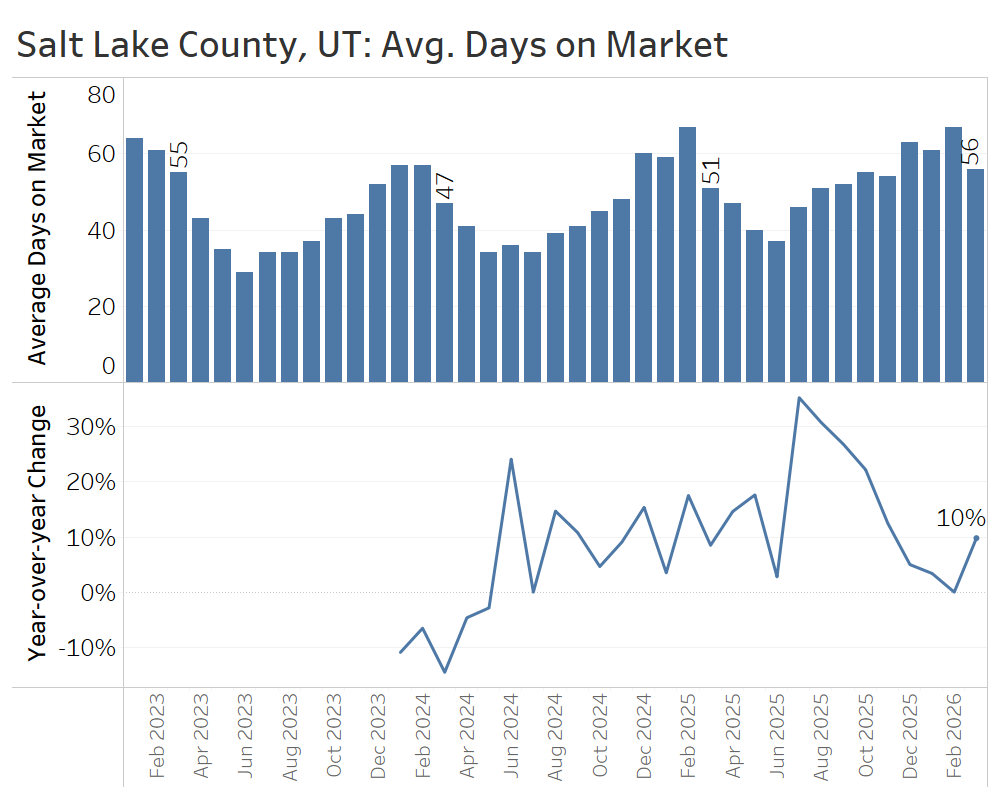

Days on market declined seasonally into the second quarter, but by the end of the quarter they remained near, or slightly above, year-ago levels. This shows the market is not decisively swinging in buyers’ favor.

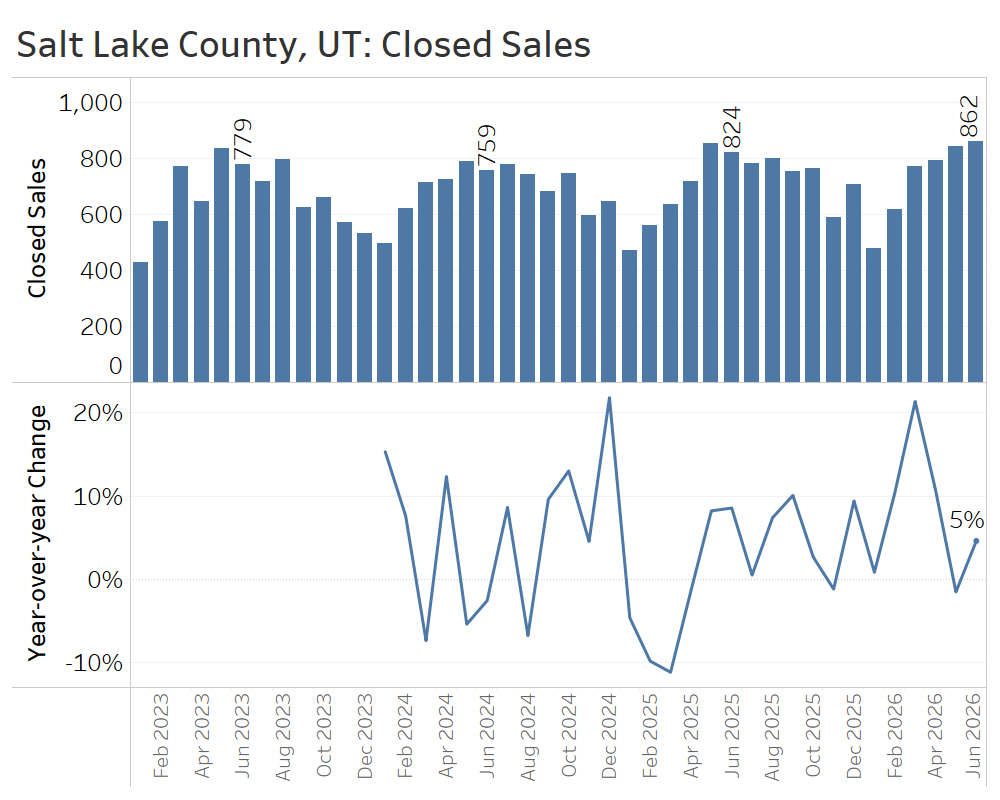

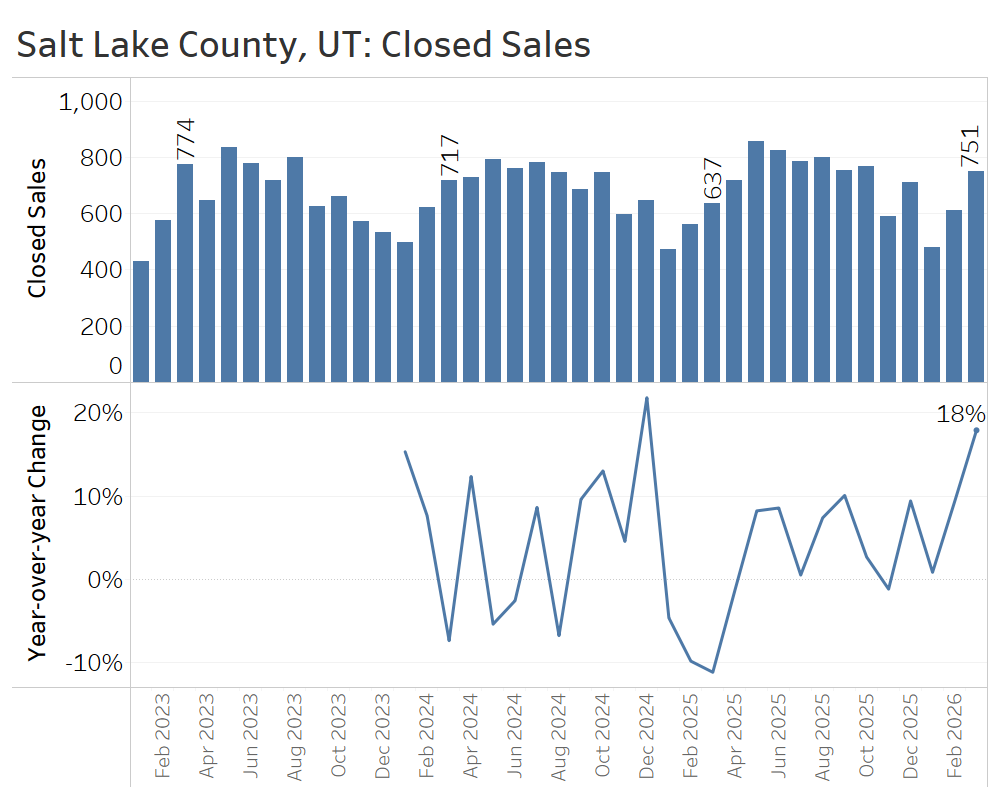

Closed home sales over the second quarter were 5% higher than the same period in 2025, continuing the rebound in buyer activity that began earlier in the year.

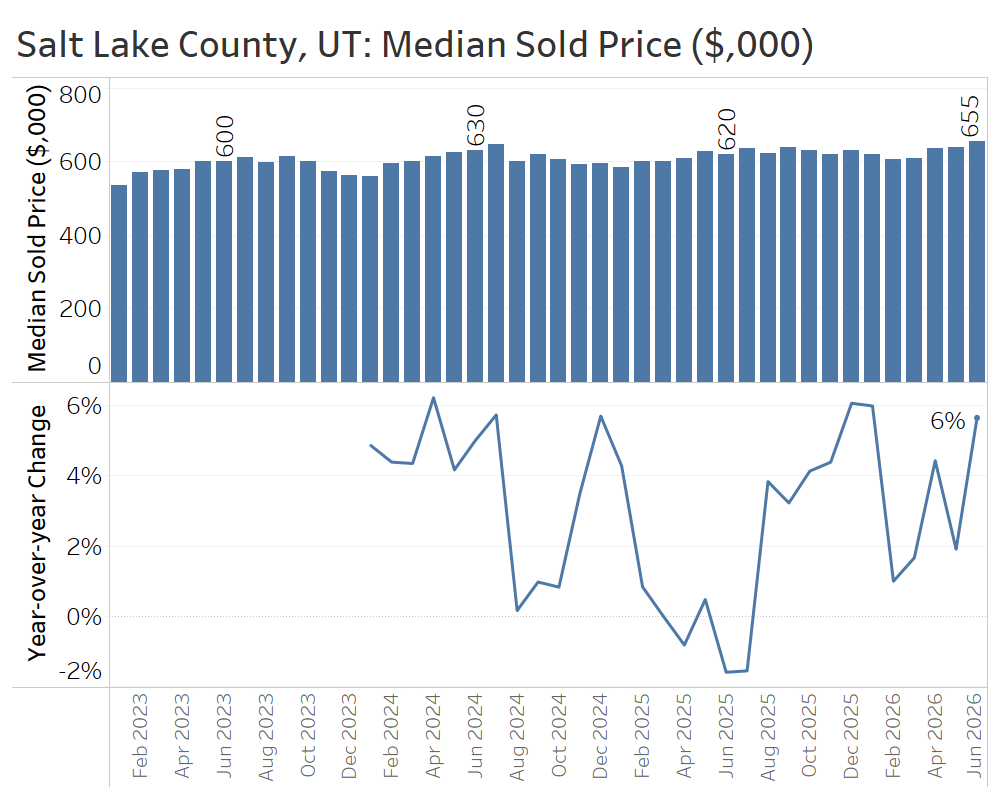

Median sale prices continued to post year-over-year gains through June, with stronger growth later in the quarter but lots of month-to-month noise.

Salt Lake County’s second-quarter market saw a healthy turn toward more sales activity without breakneck sale speeds. The decline in active listings, coupled with rising price appreciation, could suggest the beginning of a seller-friendly phase, but third-quarter data will help distinguish whether this is just a blip or a real inflection point turning back toward a seller’s market.

Conclusion:

Through mid-2026, the housing market proved remarkably resilient to the shock of rising mortgage rates and geopolitical turmoil. All of the markets highlighted in this report saw the usual spring lift in demand, and many outpaced year-ago comparisons. Conditions generally favored neither buyers nor sellers decisively, but the balance varied meaningfully by region. The Seattle area is still grappling with rising inventory and declining sales, while most of the other regions in this report have begun to turn the corner into a phase of flat-to-falling inventory coupled with growing sales.

These subtle shifts between buyer-friendly and more balanced conditions are making for a complex market to predict. Buyers will find more options and more room to negotiate in inventory-heavy areas, while still facing affordability constraints from elevated borrowing costs. Sellers need to recognize that a seasonal increase in buyer traffic does not guarantee multiple offers or rapid price appreciation, but many will still sell quickly with the right list price and positioning.

As the third quarter begins, it will be crucial for anyone trying to buy or sell a home to track local trends with the help of a skilled real estate professional. The ceasefire in Iran and easing inflation could bring more buyers into the market who sat out the spring, while sellers may become more motivated to sell rather than wait to re-list next spring. Summer is the least predictable season in the housing market, and this year looks to be no exception.

Sources: TrendGraphix analysis of NWMLS, RMLS, Spokane MLS, Coeur d’Alene MLS, MetroList MLS, and Wasatch Front MLS data. All charts are restricted to single-family residential home listings and sales.

Numbers to Know 7/15/26: Global Events Continue to Shape Housing

Hi, I’m Jeff Tucker, principal economist at Windermere Real Estate, and these are the numbers to know right now.

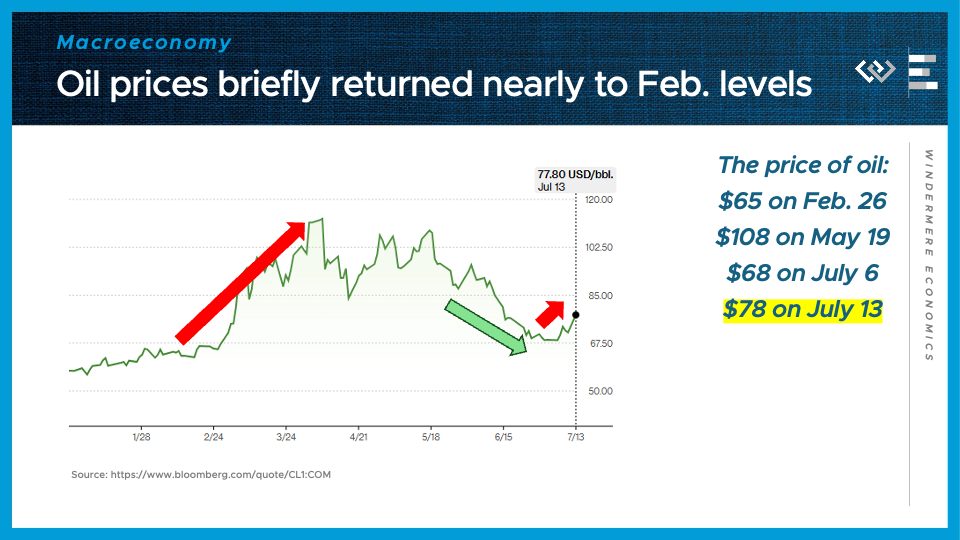

The first number to know this month: $78.

That is the price of a barrel of oil as of July 13, and it’s $10 higher than just one week earlier, when it had fallen into the ballpark of its late-February level of $65. The volatility in July just goes to show that improvement on energy costs can quickly be reversed when tensions flare back up and the ceasefire is called into question. That leaves markets of all kinds at the mercy of events in the Middle East.

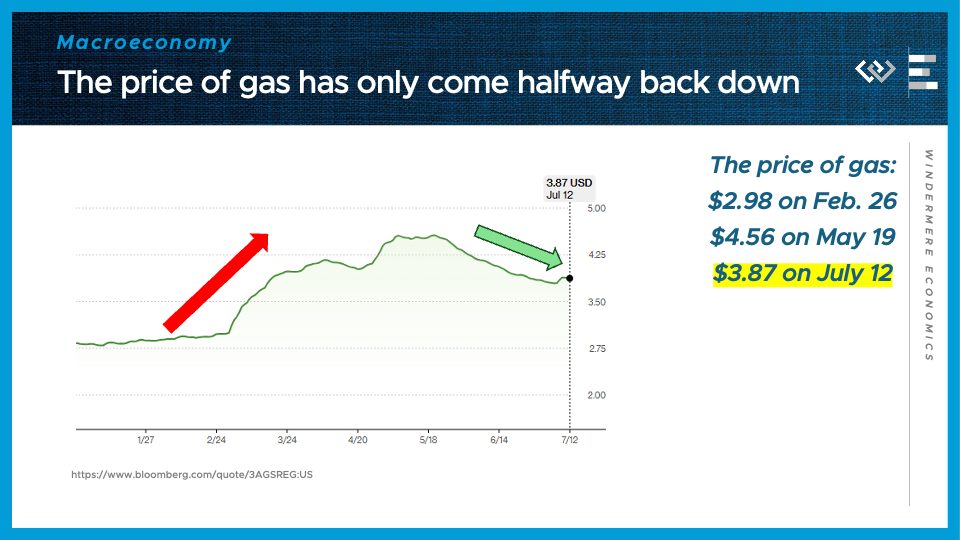

Which brings me to the second number to know this month: $3.87.

That is the average price of a gallon of gas as of July 12. Gas prices have come down from $4.56 in May, but they haven’t fallen by nearly as much as oil prices did – they’ve only given up less than half of their peak wartime gains. That’s in part because it takes time for the shortages caused by the closure of the Strait of Hormuz to ripple through the supply chain down to finished products like gasoline. And unfortunately, consumer-facing retail prices are usually downward sticky, because retailers have only weak incentives to slash prices even when their input costs drop. That’s a big reason that overall inflation is not expected to crash back down to 2% anytime soon.

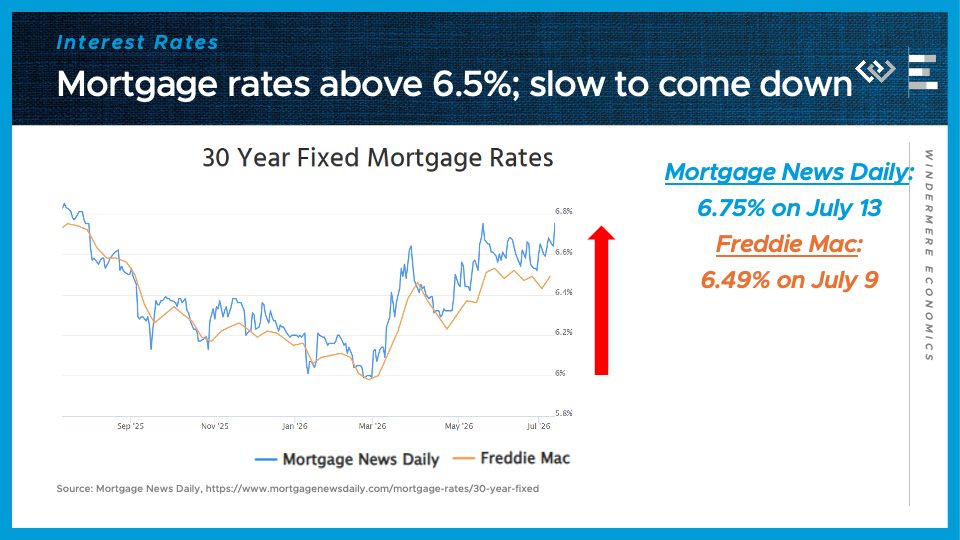

Another important figure that has barely come down at all: mortgage rates, at 6.75% on July 13, according to Mortgage News Daily.

Freddie Mac’s weekly survey was a little lower, at 6.49% on July 9, before the ceasefire was called back into question. That’s not JUST due to gas prices remaining elevated, of course – markets are also reacting to hawkish signals from the Federal Reserve, now that they have met and revised upward their expectations for inflation, leading to a new consensus that their next move will be to hike, rather than cut short-term interest rates.

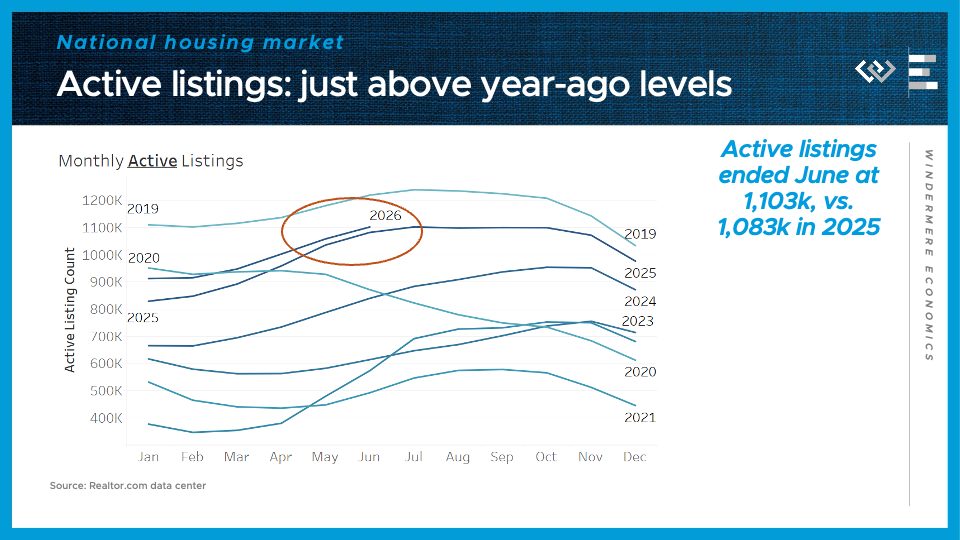

The fourth number to know: 1.103 million.

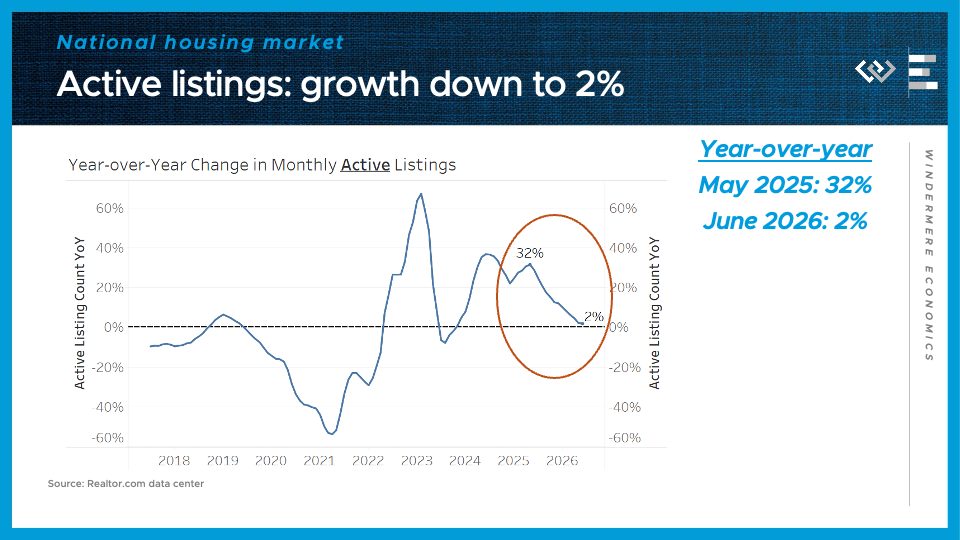

That is how many active listings were on the market nationally at the end of June, according to Realtor.com. That is just above the 1.083 million active listings from June of last year.

Put another way, active listings were up just 2% year-over-year in June.

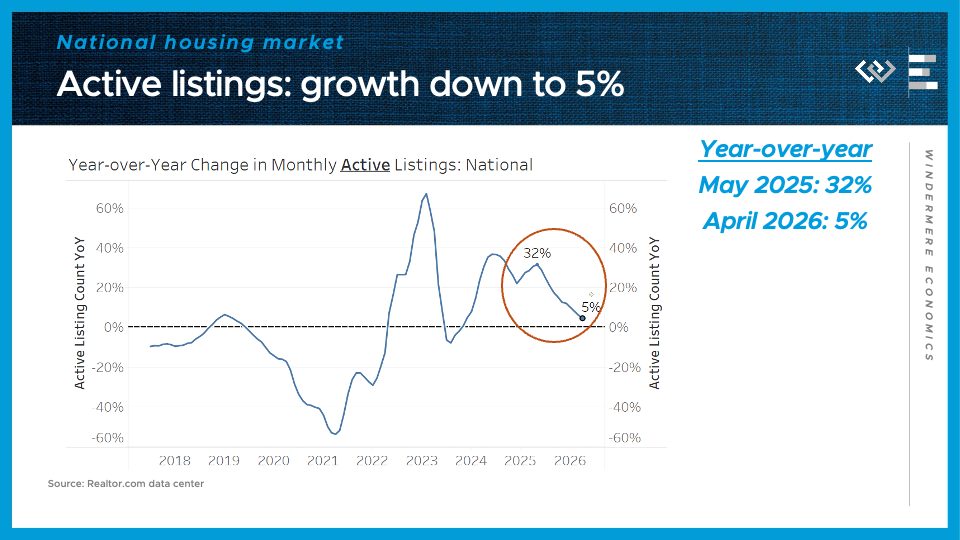

That matches last month’s gain, continuing a dramatic slowdown from May of 2025, when inventory was up 32% year-over-year.

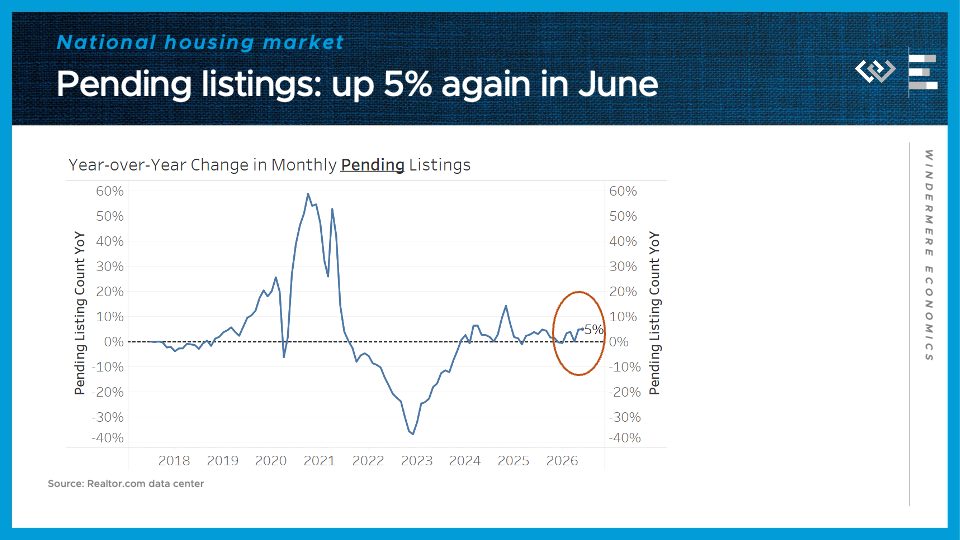

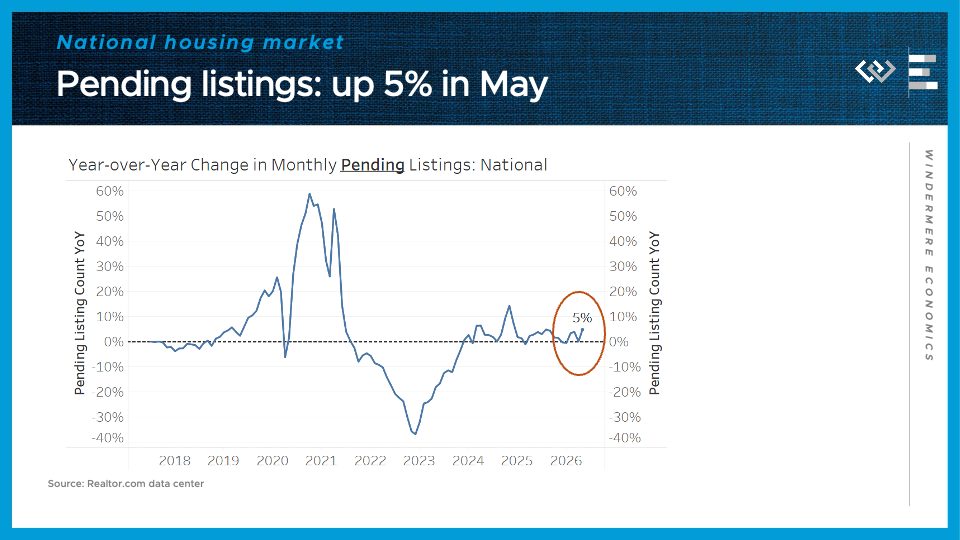

And finally, pending listings were up 5% year-over-year again in June.

So even with mortgage rates still elevated, buyer activity is holding up better than we might have expected. It could be that buyers are responding to the higher inventory availability and slightly lower prices of listings in much of the country. If mortgage rates do start to ease later this summer, that could build on this momentum and lead to some measurable sales growth.

Numbers to Know 6/18/26: The Market’s Latest Plot Twist

Hi, I’m Jeff Tucker, principal economist at Windermere Real Estate, and these are the numbers to know, right now.

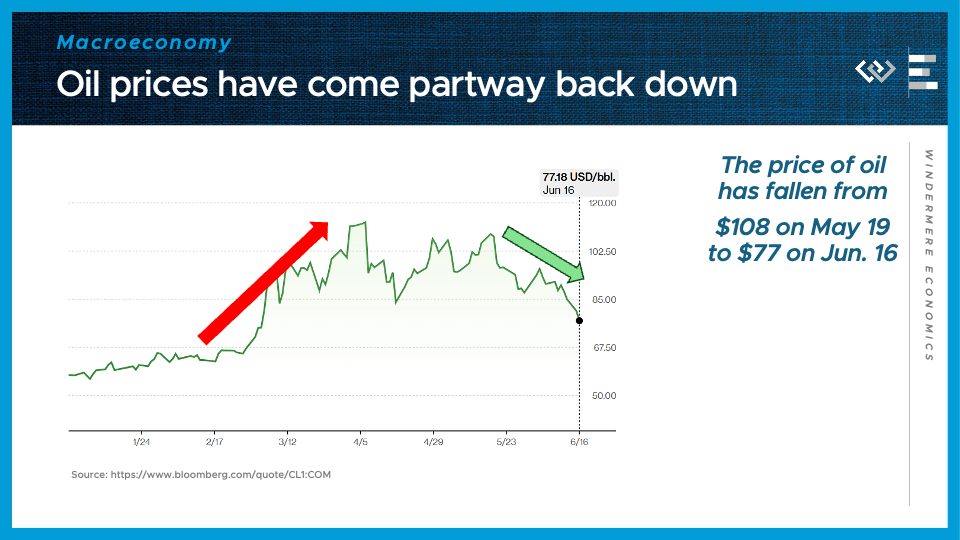

The first number to know this month: $78.

That is the current price of a barrel of oil as of June 16, after falling about $30 in just the last month. Much of that decline follows from the signed memorandum of understanding between the US and Iran, hopefully marking the beginning of the end of the war that has closed the straits of Hormuz.

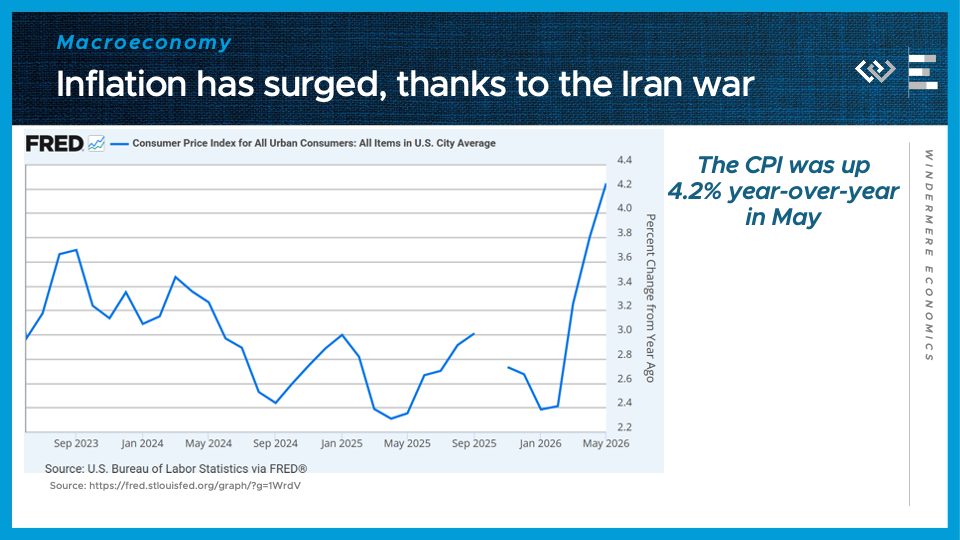

The second number to know this month: 4.2%.

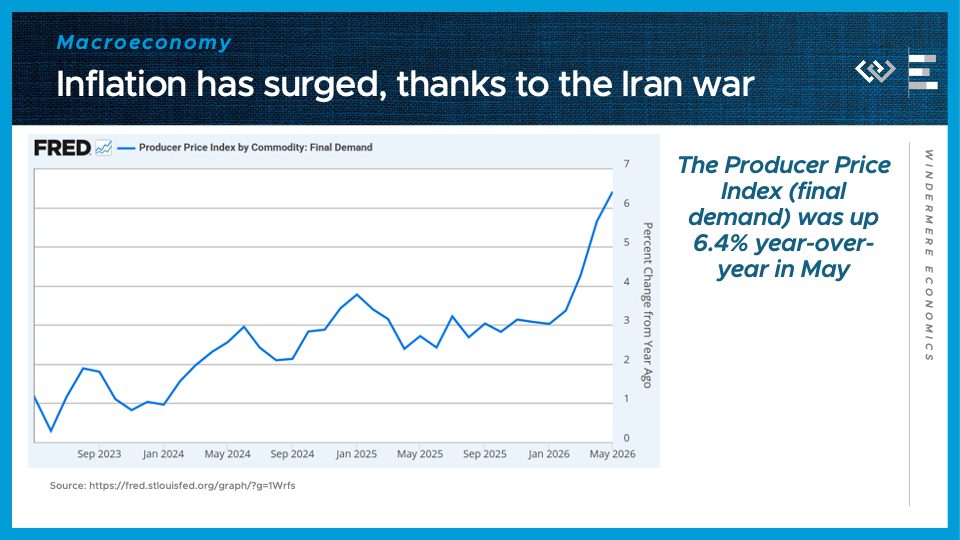

That is the current year-over-year pace of inflation as of May, and it’s the highest annual rate of inflation in over 3 years. It reflects the cost pressures from the Iran War disruptions still rippling out through the economy.

The Producer Price Index, which measures cost pressures further upstream in the supply chain, also continued accelerating in May, to 6.2%. Hopefully, this should begin to decelerate as lower oil prices bring down costs in the economy.

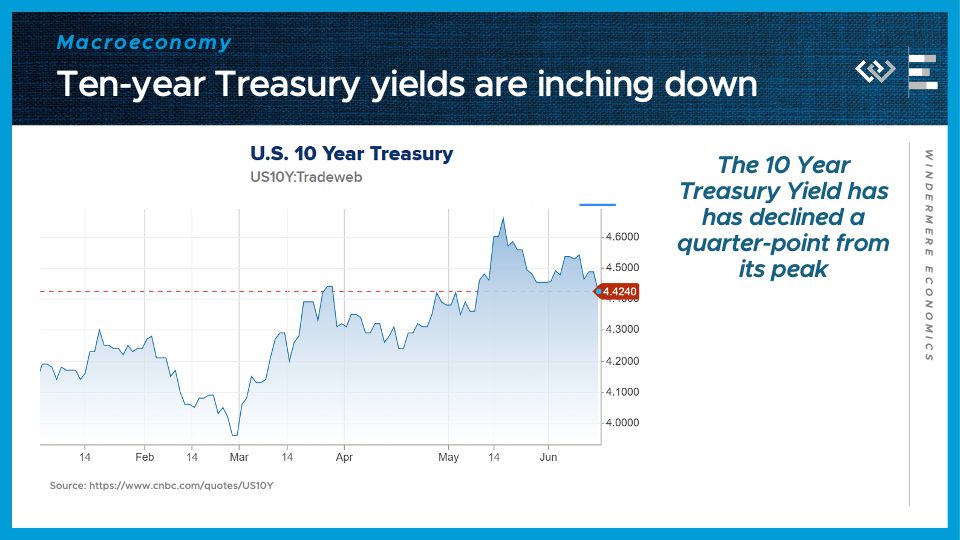

Bond yields are still elevated but they’ve begun to decline – the Ten-year Treasury yield has come back down about a quarter point from its peak in mid-May.

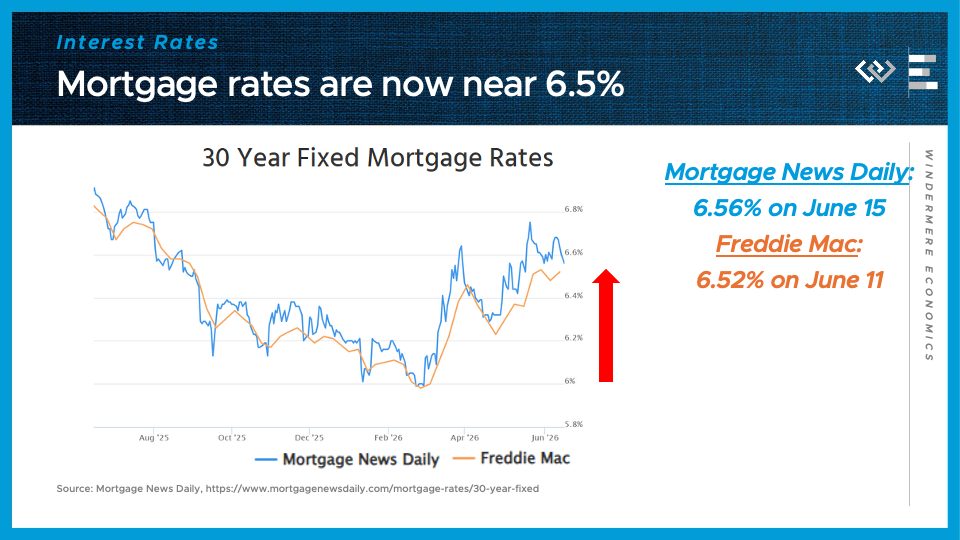

Similarly, 30-year mortgage rates are starting to come back down, but remain much higher than earlier this year: both Mortgage News Daily and Freddie Mac report average mortgage rates slightly above 6 and a half percent.

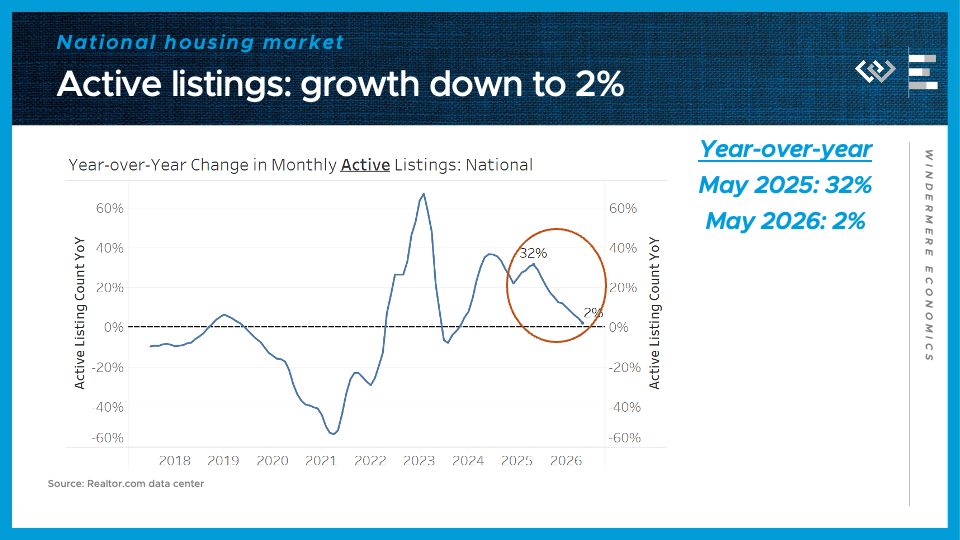

Speaking of the housing market, inventory growth slowed down again in May, which ended with just 2% more active listings than this time last year.

And most surprisingly, pending sales in May were up 5% year-over-year, according to Realtor.com, which marks a belated pickup in demand to close out the spring selling season on a higher note.

If mortgage rates continue to come back down, that strength in sales activity could continue into the summer.

Local Look Western Washington Housing Update 6/4/26

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the May 2026 data from the Northwest MLS.

As we approach the end of the spring selling season, we can now say it was a bit disappointing for sellers. On the flipside, that means this summer will likely provide some bargains for buyers who are in a position to act.

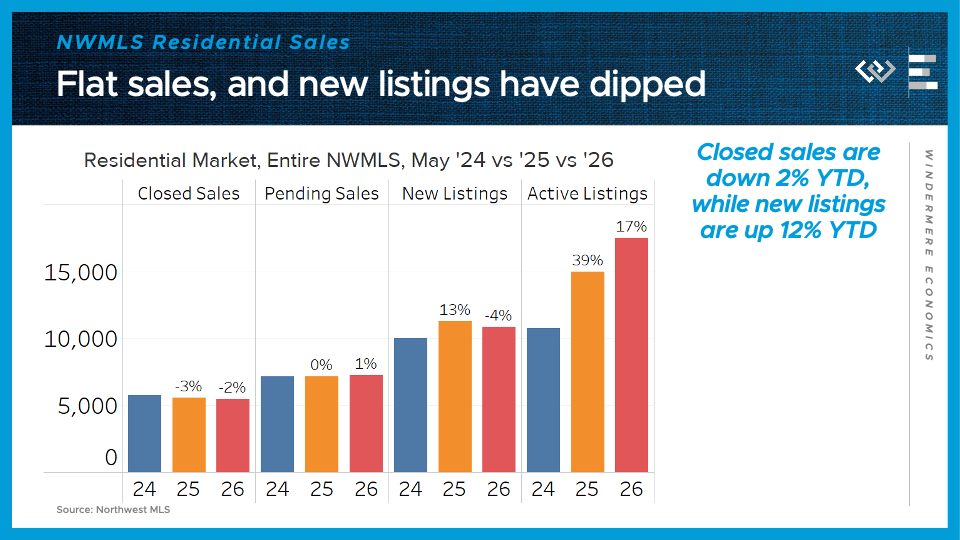

Across the entire Northwest MLS, there were 2% fewer closed sales in May 2026 than in May of last year – the same drop we saw in April. Pending home sales ticked up by 1% from last year.

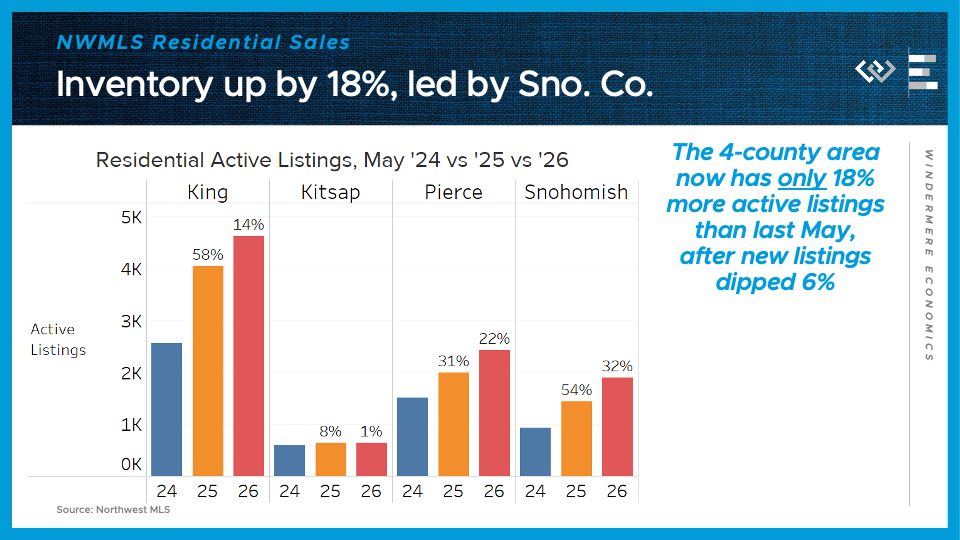

The big news in this month’s release was on the supply side, where the flow of new listings was 4% less than in May of 2025 – that’s the first slowdown in new listings all year. Finally, the month ended with just over 17,500 active listings around the MLS, or 17% more than last May, after it was up 30% in April. That tells me sellers have picked up on the softer demand signals this spring and they’ve begun to pull back. That’ll be an important trend to track in the months ahead to see if it continues.

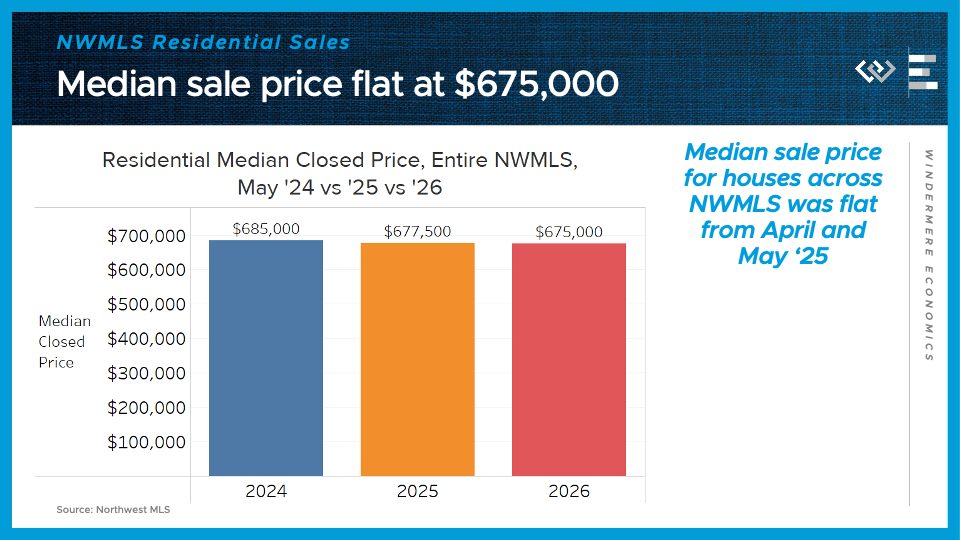

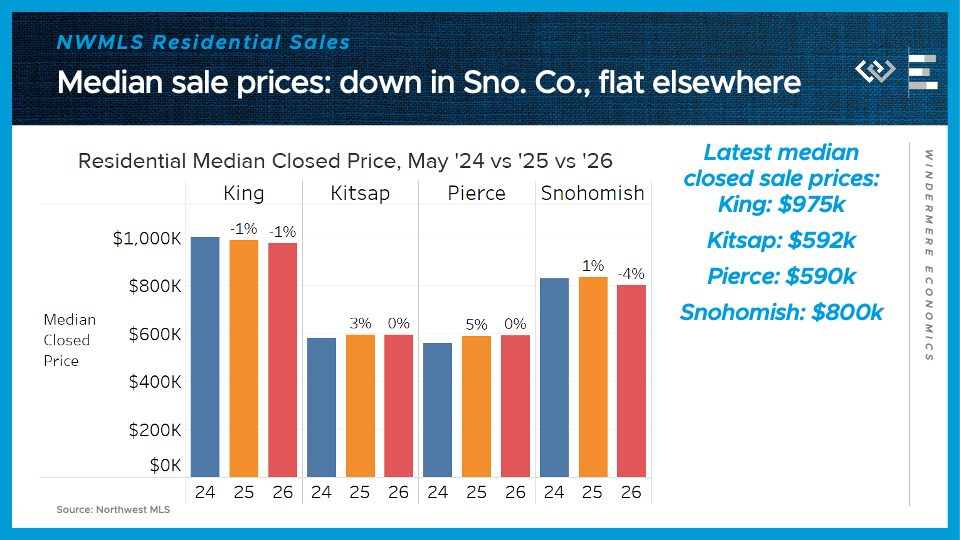

The median sale price ticked down from last May, by just $2500, leaving it basically flat at $675,000.

Now I’ll take a closer look at the four counties encompassing the greater Seattle area.

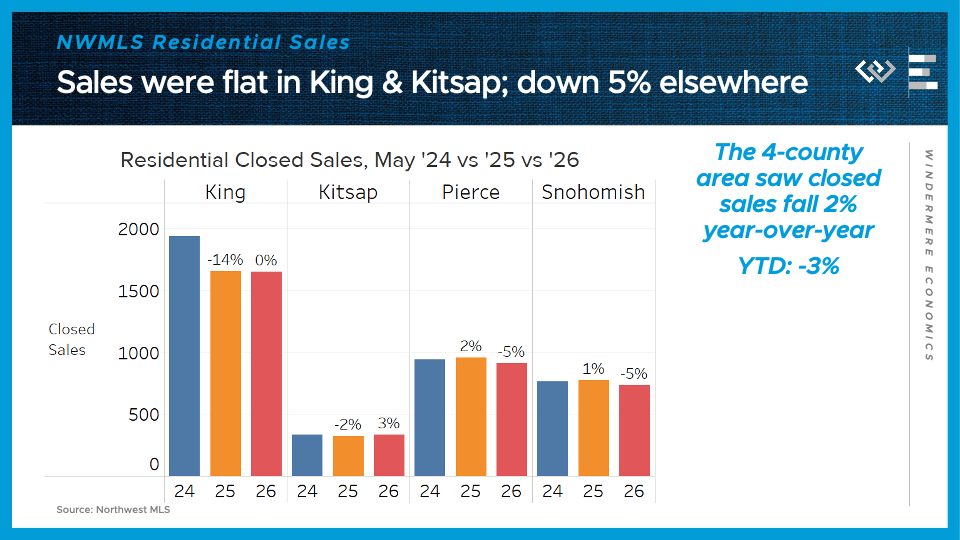

Closed sales declined by 2%, or about 80 homes, from last May around the region. Snohomish and Pierce Counties led that decline by 5% each, while King County was flat and Kitsap saw sales pick up a bit. Still, that left King County well below 2024’s sales volume.

Median sale prices were flat, or down slightly, all around the region – down the most, by 4%, in Snohomish County to $800,000, while they’ve inched down to $975,000 here in King County.

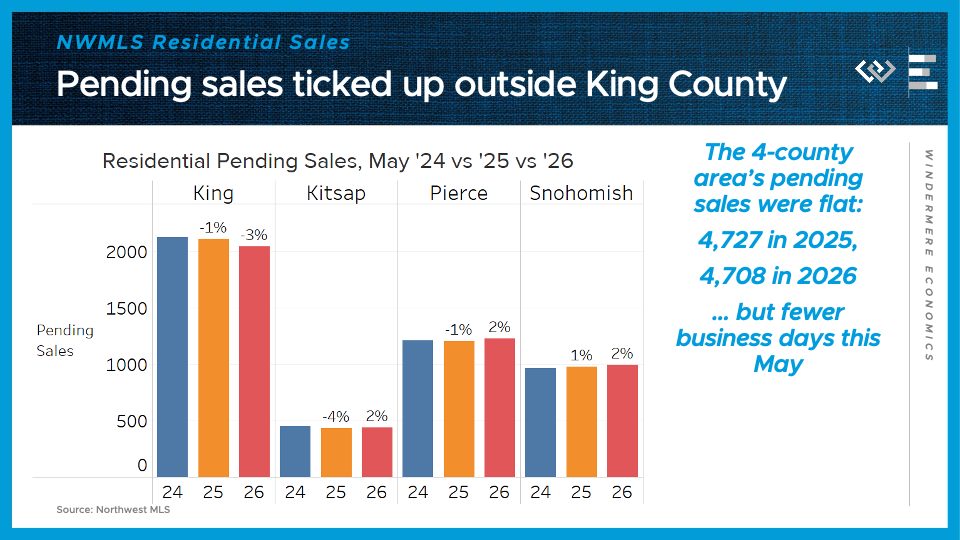

Looking ahead, pending sales were flat around the region, with a drop of 3% in King County. That’s a little ambiguous, though, because this May did end on a Sunday, when pending sales are rarely recorded. For that reason I expect a little pickup in pending sales in June.

On the supply side, the 4-county greater Seattle area ended the month with only 18% more active listings than last May, a sharp slowdown from the 37% growth in April. Every county saw a sharp slowdown in the growth of active listings, which could mark an inflection point in this cycle.

All in all, the local housing data painted a picture of an unusually buyer-friendly spring selling season this May here in the greater Seattle area, as prices cool down slightly and sales activity falls short of last year’s. Now we are approaching the time of year with peak inventory, and near-peak buying activity, so I still expect plenty of time for more buyers to find the right home, amid a slightly less frenzied setting. If geopolitical news improves and mortgage rates come back down toward 6%, the market could even catch a second wind; but in the meantime, the data suggests that sellers benefit now more than ever from a professional, polished listing when they go to sell their house in this quiet late spring market.

Numbers to Know 5/21/26: The Forces Impacting Today’s Housing Market

Hi, I’m Jeff Tucker, principal economist at Windermere Real Estate, and these are the numbers to know, right now.

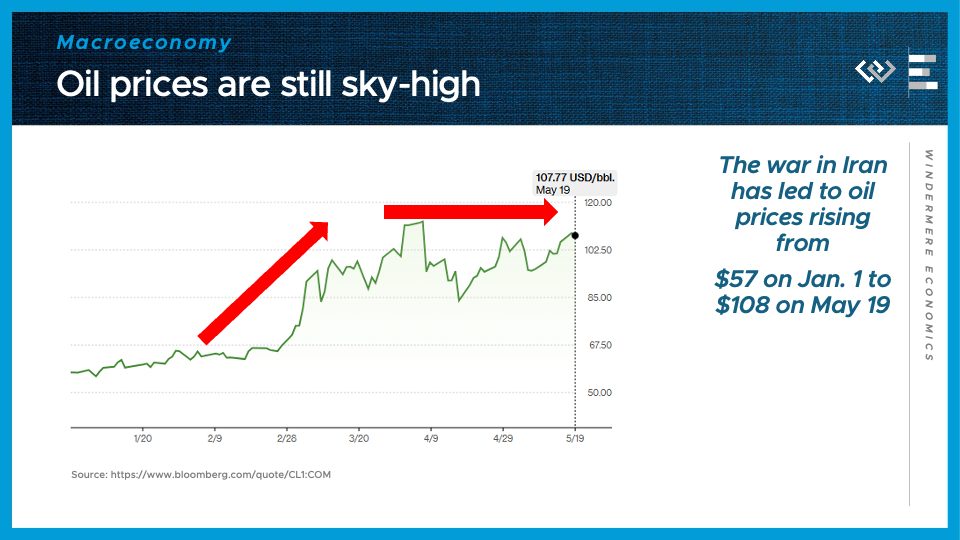

The first number to know this month: $108. That is the current price of a barrel of oil as of May 19, and it is still dramatically elevated from its price range below $60 before the U.S. launched a war on Iran this year. In fact, despite several tantalizing hints of the end of the hostilities tying up the Strait of Hormuz, prices have been over $85 a barrel pretty consistently for over two months now. As long as the flow of oil is constricted, those price pressures will stay elevated.

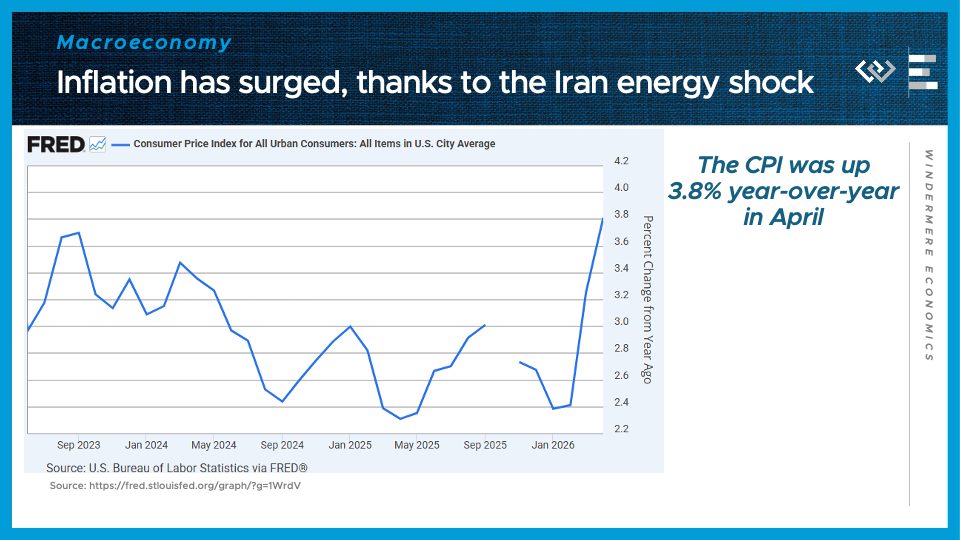

The second number to know this month: 3.8%. That is the year-over-year change in the consumer price index, representing a sharp acceleration of inflation from the 2.4% pace as recently as February. It reflects the higher costs of energy rippling through supply chains, and now inevitably raising prices for consumer products and services.

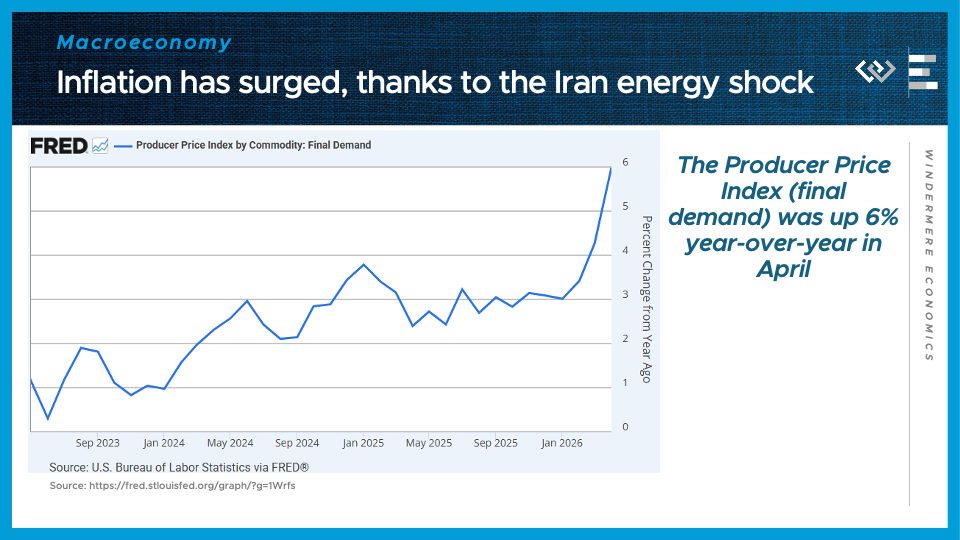

Moreover, the producer price index also just jumped sharply, to a 6% year-over-year gain, well above the consensus forecast, which is a good indicator of even more pain coming for consumers.

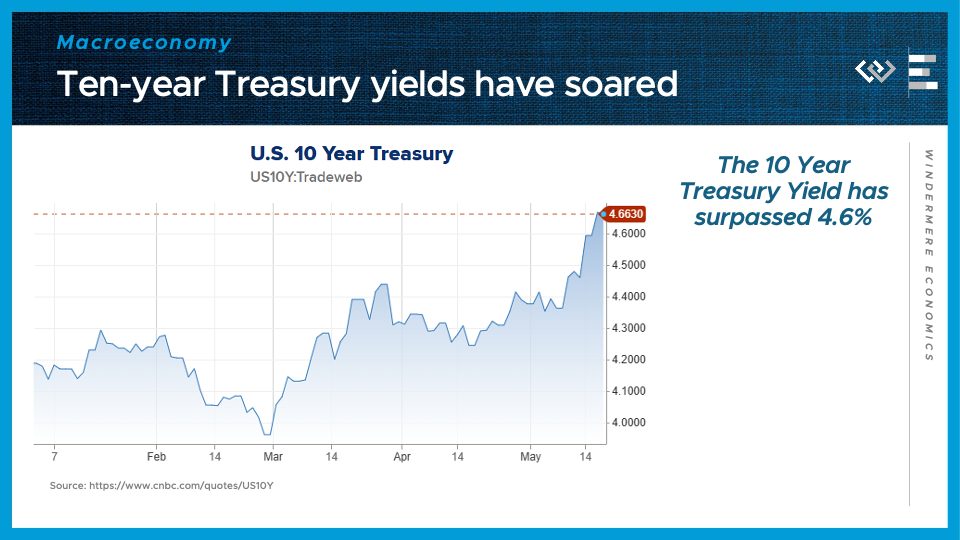

Higher inflation also tends to feed into the interest rates on bonds, and this spring has been no exception: now the ten-year Treasury bond is yielding around 4.6%, after dipping just under 4% on the eve of the Iran war.

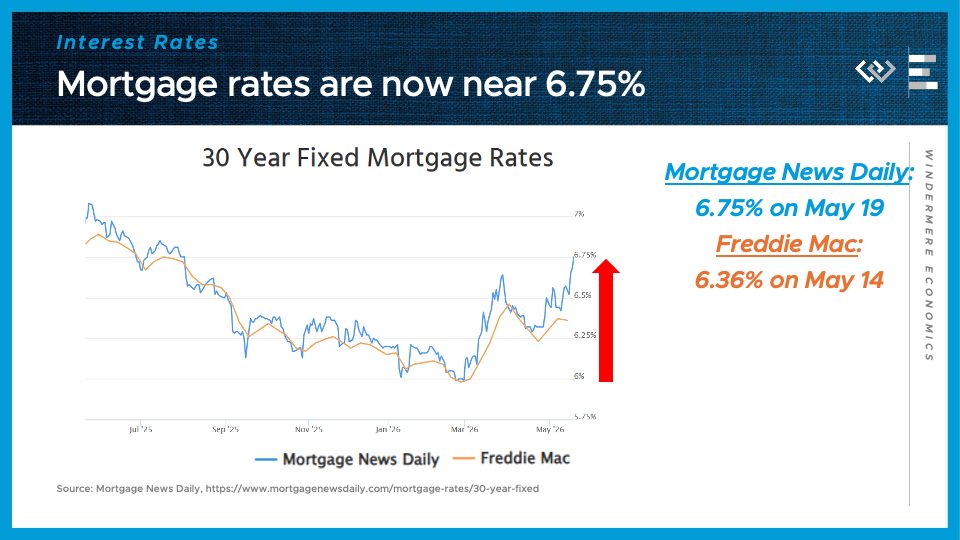

And we know higher Treasury yields usually mean: higher mortgage rates. After some volatility and false starts downward last month, mortgage rates have surged up even further in mid-May, approaching 6 and three quarters percent according to Mortgage News Daily. That will help to dampen homebuyer demand in the spring buying season, which is in full swing.

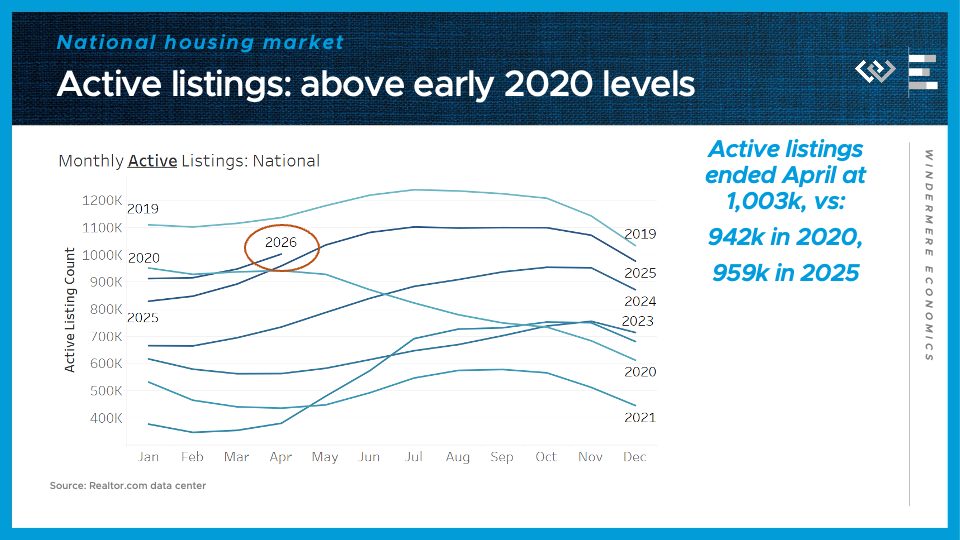

Speaking of the housing market, we saw just over a million active listings at the end of April—about 60 thousand more than this time in 2020, and 40 thousand more than this time last year.

That year-over-year growth rate of just under 5% helps continue a trend of decelerating inventory growth, as the market looks more and more balanced this year – with neither a glut of home listings building up nor a frenzied shortage condition, at least on average across the country. Pending home sales were also basically flat from this time last year, but if mortgage rates stay above 6.5%, I expect the months of May and June will look weaker than the same time last year. Once again, that means the forecast depends on whether durable peace can take hold, and whether oil begins to flow again, in the Middle East.

Local Look Western Washington Housing Update 5/7/26

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the April 2026 data from the Northwest MLS.

We are now in the heart of the spring selling season, and it is shaping up to be a little quieter than last year’s spring.

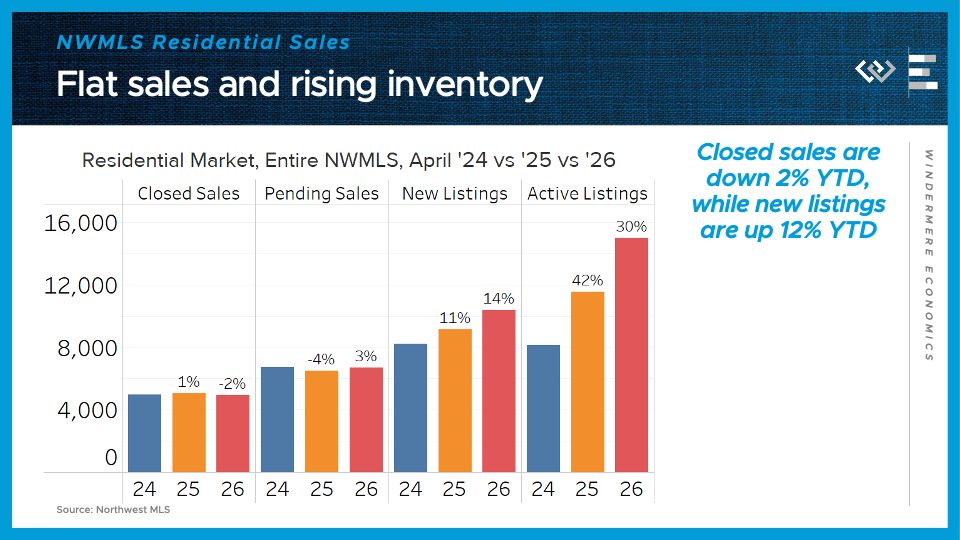

Across the Northwest MLS, there were 2% fewer closed sales in April 2026 than in April of last year. Pending home sales, by contrast, climbed by 3% from last year.

On the supply side, the flow of new listings was up an impressive 14% from last April’s pace, or 12% cumulatively, year-to-date. Finally, the month ended with just over 15,000 active listings around the MLS, or 30% more than last April. That continues the local trend of rising inventory, reflecting more sellers than buyers coming to the market this year.

The median sale price ticked down from last April, by just $5,000, or less than 1%.

Now for a closer look at the four counties encompassing the greater Seattle area.

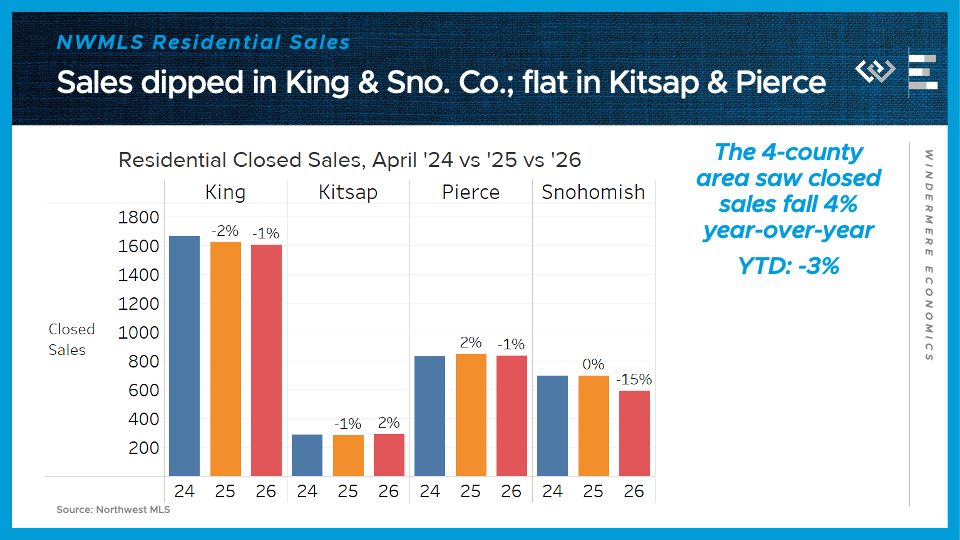

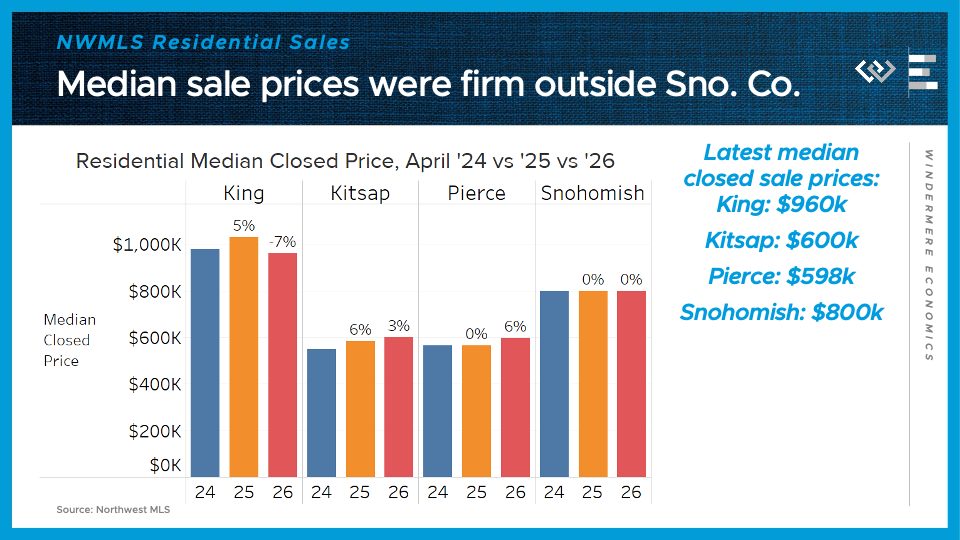

Closed sales declined by 4%, or 130 homes, from last April around the region. Snohomish County alone saw closed sales drop by 104 homes, or 15%, while King, Pierce and Kitsap Counties saw sales within a couple percentage points of last April’s totals.

Median sale prices, though, dipped the most here in King County, where they fell 7% short of last April’s $1,030,000 mark. Prices were flat in Snohomish, near $800,000; and up modestly to about $600,000 in both Pierce and Kitsap Counties.

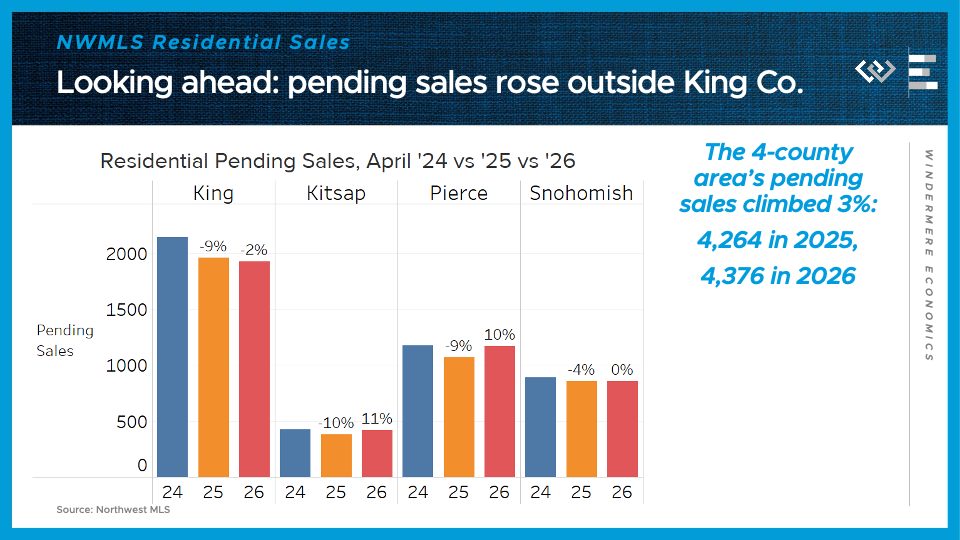

Looking ahead, pending sales actually climbed 3% across the region in April, led by strong growth in Pierce and Kitsap Counties, while only King County saw a modest dip in pending home sales.

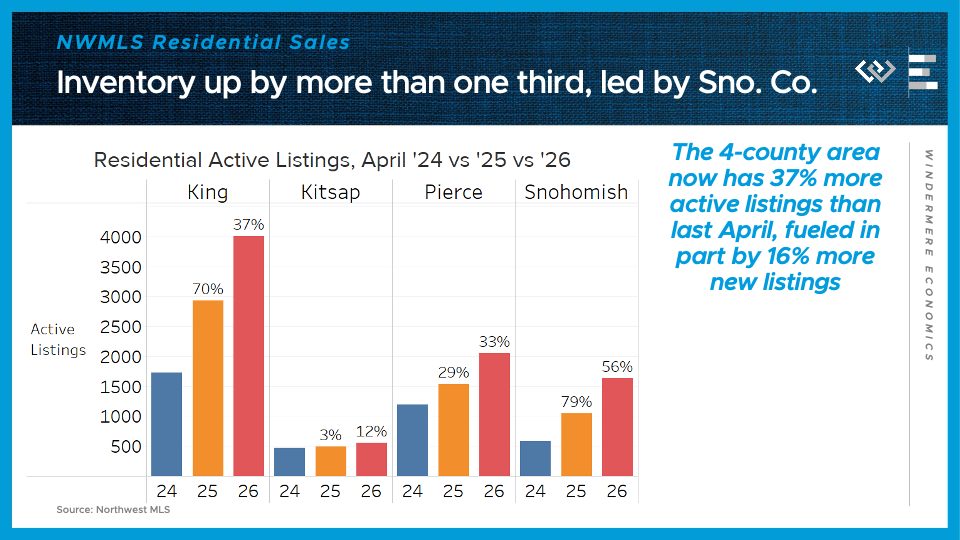

On the supply side, the 4-county greater Seattle area ended the month with 37% more active listings than last April, led by 56% growth in Snohomish County and 37% growth in King County.

Spring remains the best time of year to sell a house, but this spring also looks like an unusually good time to buy a house, thanks to unusually many listings, which are taking a little longer to sell on average, and in some areas selling for a little less than similar houses last year. Well-presented, appropriately-priced homes are still seeing a lot of competition, but plenty of other homes are lingering a little longer on the market, selling at or below list price. It seems that the negative effects of the war in Iran are discouraging some buyers, who may be taking a “wait-and-see” approach, which leaves the market a little more balanced for the many buyers who are still forging ahead this spring. If economic and geopolitical news improves, there’s still plenty of time to see a busy second half of the spring selling season.

2026 First Quarter Regional Real Estate Report

This is a recurring series of blog posts taking a closer look at the U.S. economy and several major regional markets in Windermere’s nine-state footprint. Updates will be released on a quarterly basis.

Economic Overview

At the end of February, the spring housing market appeared poised for a rebound. Mortgage rates dipped below 6% for the first time in over three years, driven by a combination of narrowing mortgage-Treasury spreads, falling Treasury yields, reduced interest rate volatility, and the FHFA’s announcement that Fannie Mae and Freddie Mac would buy substantial amounts of mortgage-backed securities.

Source: Freddie Mac via FRED.

Then the market was thrown for a loop by the sudden onset of the war in Iran. The effects on the economy, interest rates, and the housing market are only just coming into focus, but so far, the signals are negative. Mortgage rates jumped by as much as half a point in the six weeks after the war began, and March saw the highest one-month increase in the gasoline consumer price index in decades.

Source: BLS via FRED.

As the energy shock ripples through the global economy, it is likely to slow economic growth while pushing prices higher. The magnitude of those effects will depend on how quickly the Strait of Hormuz reopens to tanker traffic, as well as how long it takes to restart oil production and other industrial activity across the Gulf states.

Against that backdrop, local housing market data for the first quarter of 2026 largely reflect conditions before the impacts of the war began to take hold. By the second quarter, we should have a clearer picture of those effects.

The following is a detailed overview of housing trends across six regional markets within Windermere’s footprint during the first quarter of 2026. They include:

- Greater Seattle Area

- Greater Portland Area

- Greater Sacramento Area

- Northwest Washington State

- Spokane, WA and Coeur d’Alene, ID

- Salt Lake County, UT

Greater Seattle Area (King, Snohomish, Pierce, and Kitsap Counties)

While the spring selling season is typically the strongest time of year for sellers, conditions this year in the greater Seattle area look closer to a balanced market, as abundant listings are meeting only modest demand. Active listings at the end of March were 35% higher than the same time in 2025, a substantial increase and an acceleration from the pace of growth observed in late 2025.

Some of that growth in active listings stemmed from the growth of new listings. More than 13,000 homes hit the market in the first quarter, or about 12% more than in the first quarter of 2025. The flow of new listings may have been particularly strong this spring with the return of patient sellers who held off, or de-listed, late last year.

The usual seasonal acceleration in time-on-market took hold this spring, but the median home still took 35 days to sell in March, up from 31 days a year earlier.

Closed sales in March fell just short of their level one year ago, and for the quarter as a whole, 4% fewer closed sales were recorded than throughout the first quarter of 2025. This is a clear indication of softer demand this year.

Cooler demand this quarter showed up in prices, too. Median home sale prices hovered 1%-2% below year-ago levels throughout the first quarter.

The first quarter of 2026 brought a seasonal bump in demand, as usual, but it was smaller and more selective than the increase observed in the first quarter of last year. In this environment, sellers need to put their best foot forward and enter the market with realistic expectations, given the competition from other homes.

Greater Portland Area (Multnomah, Washington, Clackamas, and Clark Counties)

The greater Portland Area edged toward a balanced—or even a buyer’s— market in the first quarter of 2026, as inventory growth slowed to near zero, leaving active listings up only slightly from last year at this time, and sales rebounded modestly.

There were 3,925 active listings at the end of the quarter, which was 6% higher than one year earlier. That continues a trend of decelerating inventory growth since May of 2025.

New listings in the first quarter jumped for the first time in several months, with a total of 8% more new listings in the quarter than in the first quarter of 2025.

The average home sold after 63 days on the market—about 10 days longer than in March 2025. Nonetheless, that represents an acceleration from the seasonal trough for selling speed in January, when time on market topped out at 74 days.

Closed sales of single-family homes jumped 10% year over year in March, offsetting a decline in January and bringing total first-quarter sales to 2% above the same period in 2025.

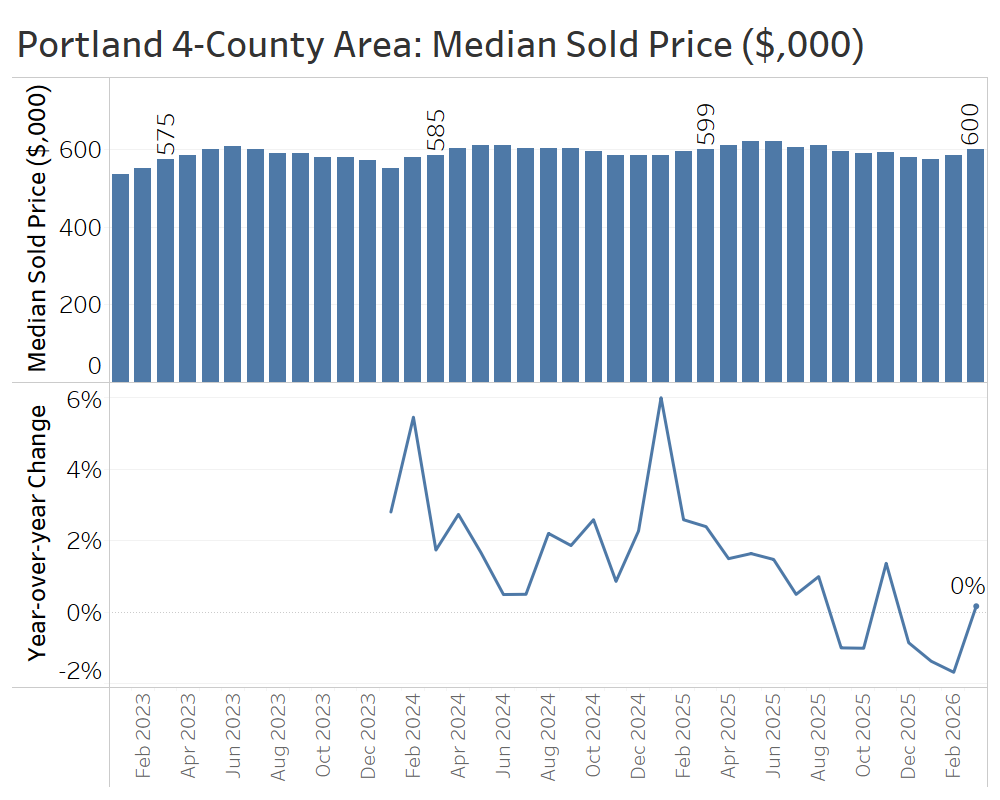

Median home sale prices in the Portland area were flat year over year at $600,000 in March, following slight declines of 1%-2% in January and February. While demand may be starting to pick back up, it is not yet translating into price appreciation given the high inventory levels.

Portland’s first-quarter market looked balanced this year, with flat pricing, modest sales growth, and renewed activity from sellers jumping into the market.

Greater Sacramento Area (Sacramento, Yolo, El Dorado, and Placer Counties)

The greater Sacramento area appears to be at a possible inflection point after swinging in buyers’ favor in 2025.

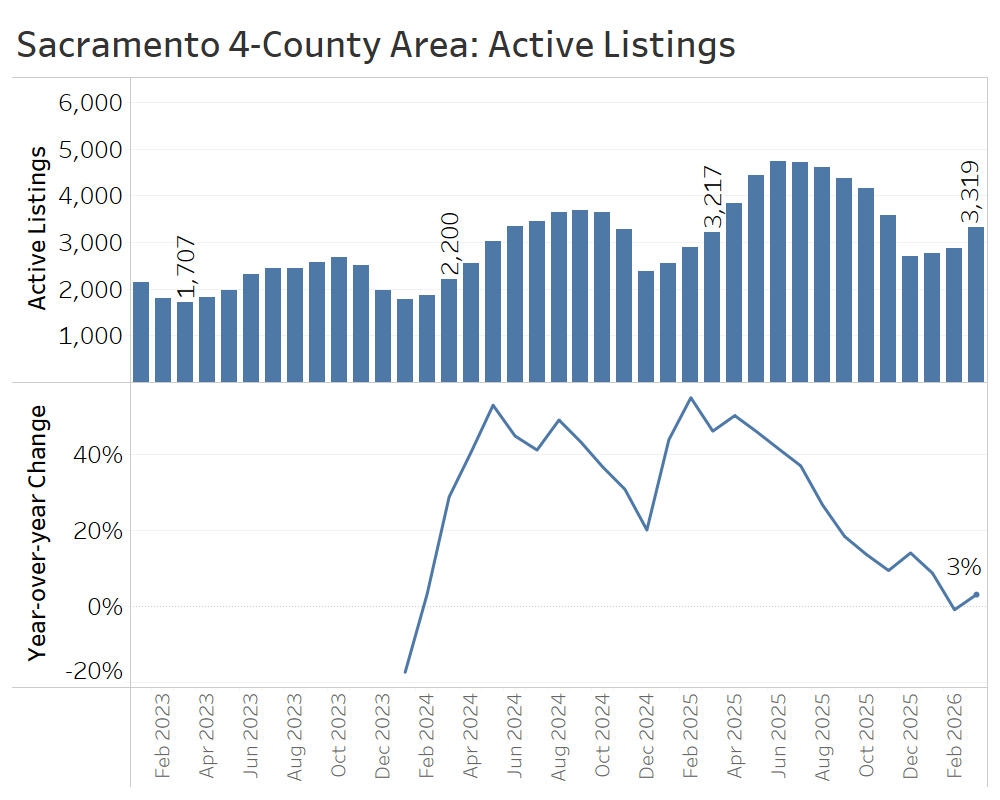

At the end of March, there were about 3,300 active listings—an increase of just 3% compared to March 2025—continuing a trend of decelerating inventory growth over the past year.

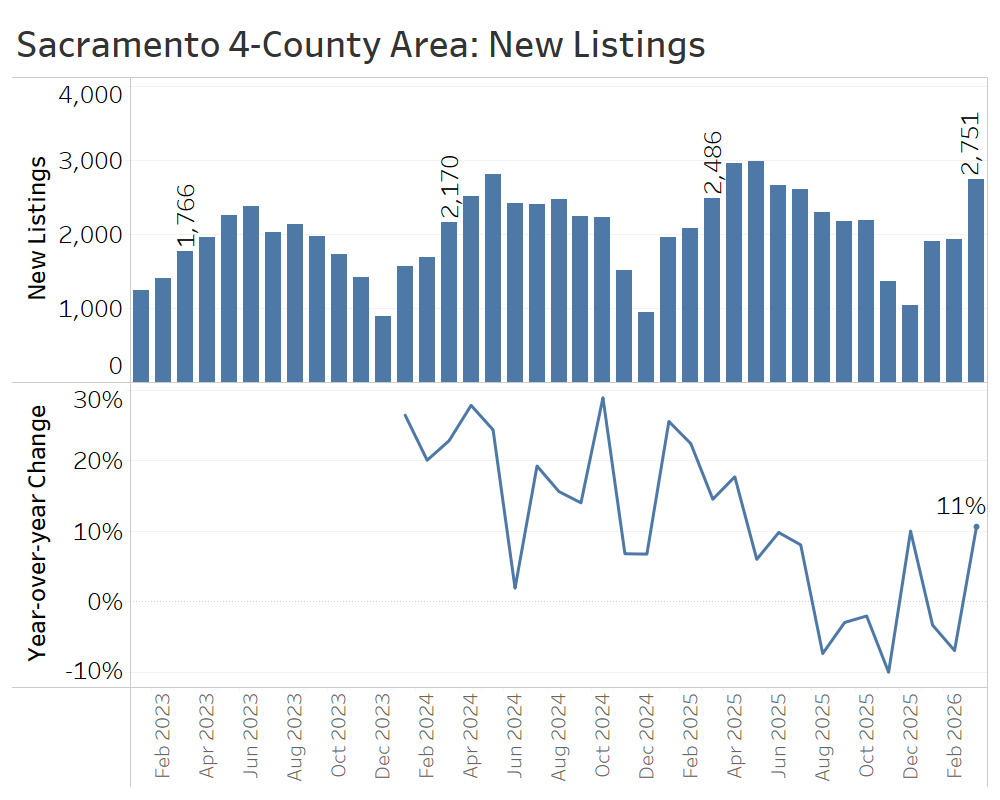

On a monthly basis, the new listings data has been volatile, with small declines in January and February followed by an 11% year-over-year jump in March. Overall, the quarter saw just 1% more new listings than that of the prior year.

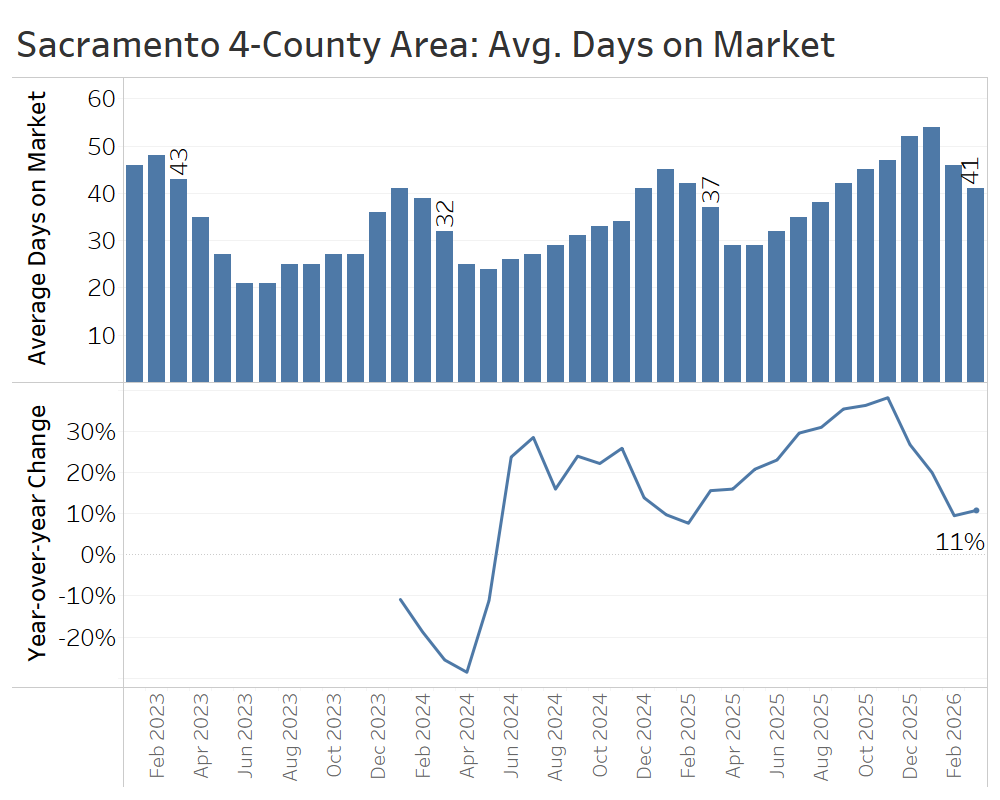

Average days on market rose by about four days compared to March 2025, reaching 41 days. That is a much more modest increase than the larger gains in days on market seen in late 2025.

Much like in the fourth quarter, total closed sales for the first quarter were almost identical to the prior year: about 3,840 so far this year compared to roughly 3,850 in the first quarter of 2025.

The median sale price of $605,000 in March was higher than the seasonal winter lows, but still 1% below the March 2025 median.

Overall, last year’s inventory growth around the Sacramento region led to a cooldown in pricing over the winter and into spring. Looking ahead, more modest inventory gains suggest that the pendulum won’t swing much further in favor of buyers.

Northwest Washington (Skagit, Whatcom, San Juan, and Island Counties)

The market conditions in the four northernmost counties of Western Washington are still shifting toward buyers.

At the end of March, there were 1,223 active listings, up 20% from a year earlier. While that is slower than last summer’s inventory growth of 30% or more, it’s also no longer clearly decelerating.

The flow of new listings slightly exceeded the first quarter of 2025, with a total of 1,669 new listings in the quarter, up 3% from last year’s 1,622. That is far from a flood of listings and likely reflects some discretionary sellers waiting until spring to list.

Days on market continued to climb compared to a year earlier, with homes in March taking nine days longer to sell than in March 2025.

Closed home sales in the first quarter generally trailed first-quarter 2025 levels, except for a bump in February. In total, the 981 closed sales for the quarter fell 2% short of the 1,001 homes sold in the first quarter of 2025, but as the quietest quarter of the year, that statistic is prone to random variation.

Median sale prices actually ticked up in January and March, reaching a recent high of $652,000 in March. That likely doesn’t reflect true price appreciation, given the lack of growth in sales volume, but rather reflects a shift in the composition of sales toward higher-end segments.

Overall, the first-quarter data has shown that the Northwest Washington housing market is off to a sluggish start this year.

Spokane, WA and Coeur d’Alene, ID Area (Spokane and Kootenai Counties)

The greater Spokane-Coeur d’Alene region, spanning the Washington-Idaho border, is experiencing many of the same market trends seen in Western Washington, including higher inventory, softer buyer demand, and flattening home prices.

At the end of March, there were 1,921 active listings, up 17% from March 2025.

The greater Spokane area has seen strong growth in new listings since December. During the first quarter, there were 3,688 new listings, up 9% from the first quarter of 2025.

Days on market fell from its seasonal winter high to 61 days in March, though that is still 8 days slower than in March of 2025. That average also masks a wide gap across the state border, between 94 average days on market in Kootenai County compared to roughly half that—46 days—in Spokane County.

Closed sales were up 5% in March, helping to offset a weak January so that first-quarter closed sales totaled 1,817, about 1% more than first quarter of 2025.

Compared with March 2025, the average sale price in March rose about 6%, from $528,000 to $559,000. For the quarter as a whole, prices increased 2%, rising from $537,000 in the first quarter of 2025 to $550,000 in the first quarter of this year.

Altogether, the greater Spokane-Coeur d’Alene area has looked like a balanced market so far this spring, with modest year-over-year gains in both sales (1%) and average sale prices (2%).

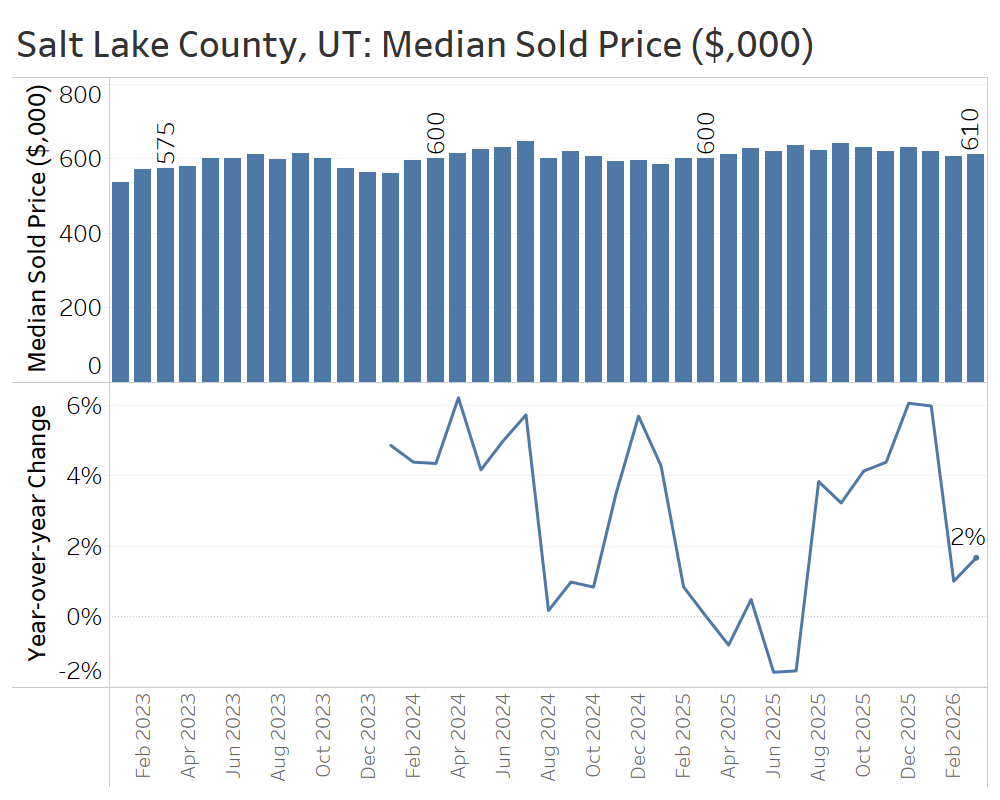

Salt Lake County, Utah

In the first quarter of 2026, the Salt Lake County market saw strong sales activity and the clearing of an inventory overhang. That continues a broader shift in Utah’s largest market, from conditions favoring buyers in early 2025 to a more balanced market—and in some segments, even a seller’s market—by spring 2026.

Active listings at the end of March stood at 1,361 homes, virtually identical to a year earlier. That completes a round trip from rapid inventory buildup last spring to slowing year-over-year growth last fall, suggesting that supply and demand have returned to a more balanced state in the Salt Lake market.

New listings dipped 6% year over year in March, but strong growth in January and February meant the flow of new listings still rose 7% in the first quarter compared to the year prior.

The average number of days it took to sell a home in Salt Lake County ended the first quarter at 56 days, up from 51 days a year earlier. This reflects the typical seasonal pattern of declining days on market in spring, but the year-over-year increase suggests the market has not yet shifted into a decisive seller’s market.

Closed home sales in March 2026 rose 18% compared to March 2025, capping a strong first quarter with about 10% more closed sales in total than in the weak first quarter of 2025.

In March, the median sale price in Salt Lake County rose 2% year over year—from $600,000 to $610,000. That marked the eighth straight month of price gains but reflected a slowdown in the pace of price gains from late 2025.

Salt Lake County’s strong start to the spring selling season was driven by growth in unit sales, not big price gains, suggesting a broad-based growth in activity as buyers return while having plenty of inventory to choose from. The lack of inventory growth year over year suggests Salt Lake County has completed its transition from a buyer’s market early in 2025 to more balanced conditions today.

Conclusion:

The housing market is cyclical, with predictable seasonal swings in demand alongside less predictable longer-term shifts. At the end of the first quarter of 2026, many of the markets highlighted here are in a somewhat unusual balance, where the seasonally strongest period of demand—the spring selling season—is meeting a broader market cooldown marked by higher inventory, longer time on market, and slower price appreciation.

That combination makes for a more difficult market to navigate than usual. Buyers may feel whiplash, moving from being outbid by a dozen offers on one home to getting a below-list offer accepted on another down the street that just needs a fresh coat of paint. Sellers, meanwhile, may decide to list their home at an aggressive price after hearing about nearby homes selling far above list price, only to wonder why they’re not receiving any offers.

In a market like this, it pays to work with a skilled real estate professional who can cut through the noise of local data to determine a home’s fair price, while also understanding the nuances of which homes are selling quickly and which are selling at a discount in this unusual spring selling season.

Sources: TrendGraphix analysis of NWMLS, RMLS, Spokane MLS, Coeur d’Alene MLS, MetroList MLS, and Wasatch Front MLS data.

Numbers to Know 4/13/26: Global Tensions Drive Rates & Market Shifts

This is the latest in a series of videos with Windermere Principal Economist Jeff Tucker, where he delivers the key economic numbers to follow to keep you well-informed about what’s going on in the real estate market.

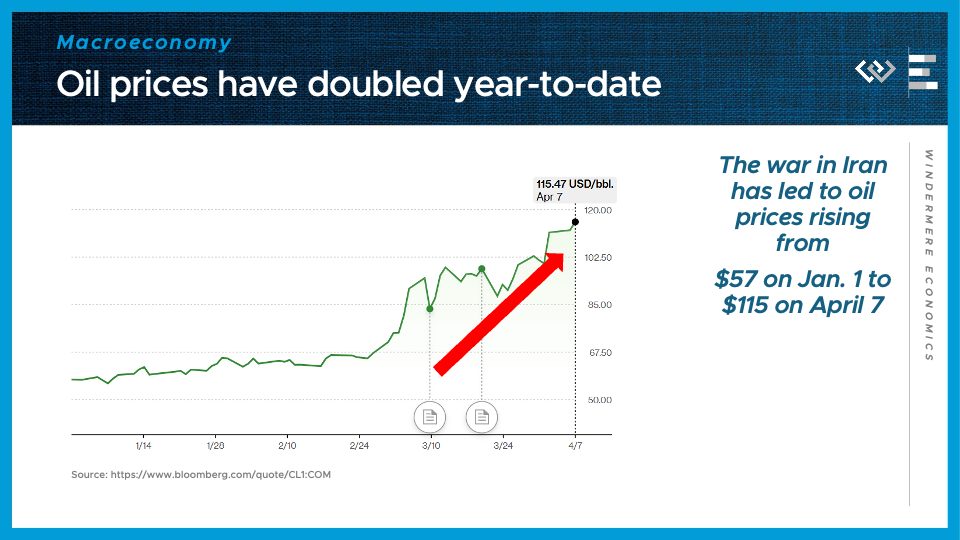

The first number to know this month: $115. That was the level that price of a barrel of oil reached on April 7, and it happens to be exactly double the price of oil at the start of 2026. The war in Iran has dragged on into its second month now, and it’s continuing to cause an energy crisis that’s rippling out through the global economy. An energy shock like this raises the costs of making and transporting almost everything, so the longer this goes on, the more inflationary pain it will inflict this year.

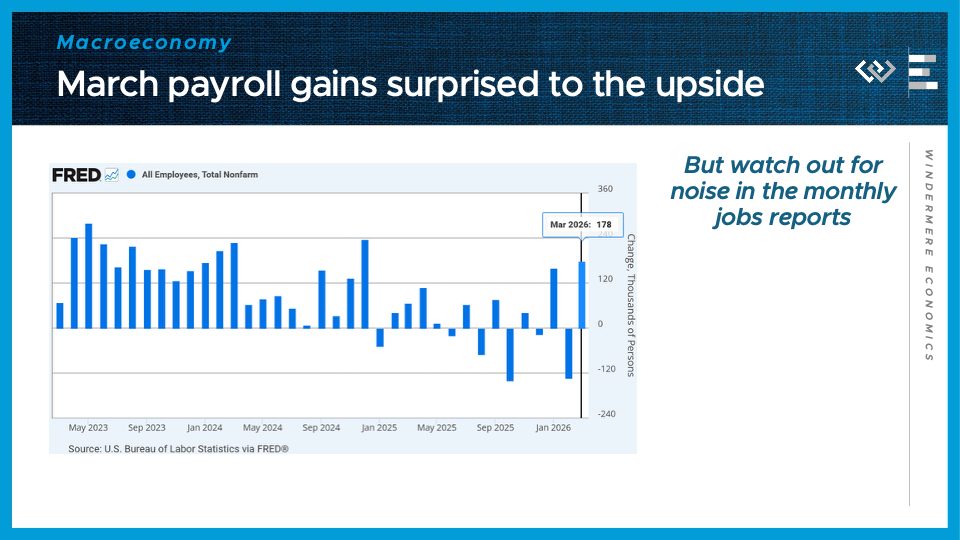

The second number to know this month 178,000. That was the number of jobs added in the economy in March, which would make it the single best month for job gains since late 2024, if it survives the usual rounds of revisions. If we look at the trend of the last 15 months, though, it’s pointing both toward a slowdown in job gains, and a increasing month-to-month volatility, as we’ve now swung between job gains and job losses for 11 months in a row. One upshot of this strong jobs report is that it provides further cover for the Federal Reserve to keep interest rate cuts on hold for now – if the labor market isn’t looking too distressed, they don’t need to be rushing to the rescue.

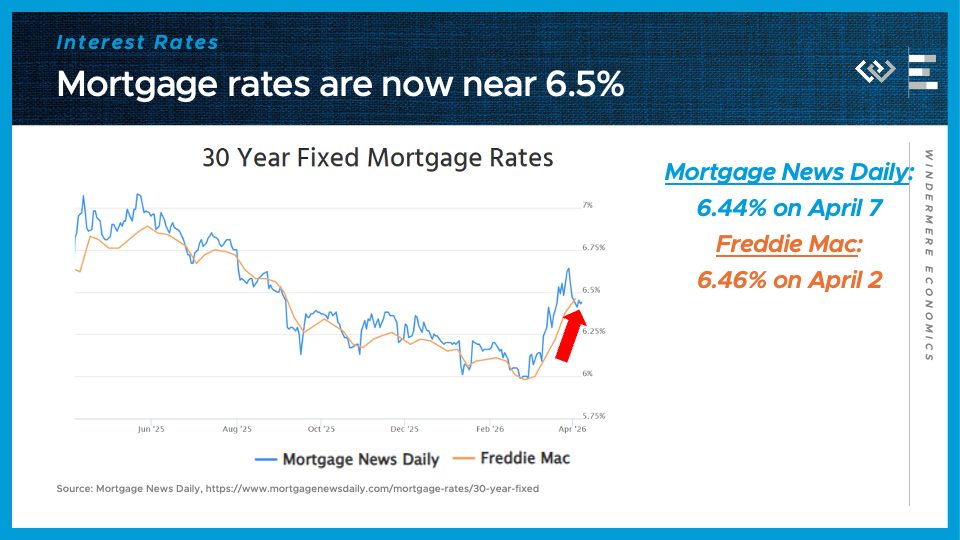

The third number to know this month: 6 and a half percent. That’s the ballpark of where 30-year mortgage rates are now bouncing around, after jumping almost half a point from multi-year lows they reached just back in late February. The combination of higher inflation and tighter monetary policy triggered by the war in Iran has set interest rates back up to where they were last summer, and frankly into the range of where they stood last spring. This is undermining homebuyer demand in what should be the busy spring buying season, leading instead to more balanced conditions in the housing market.

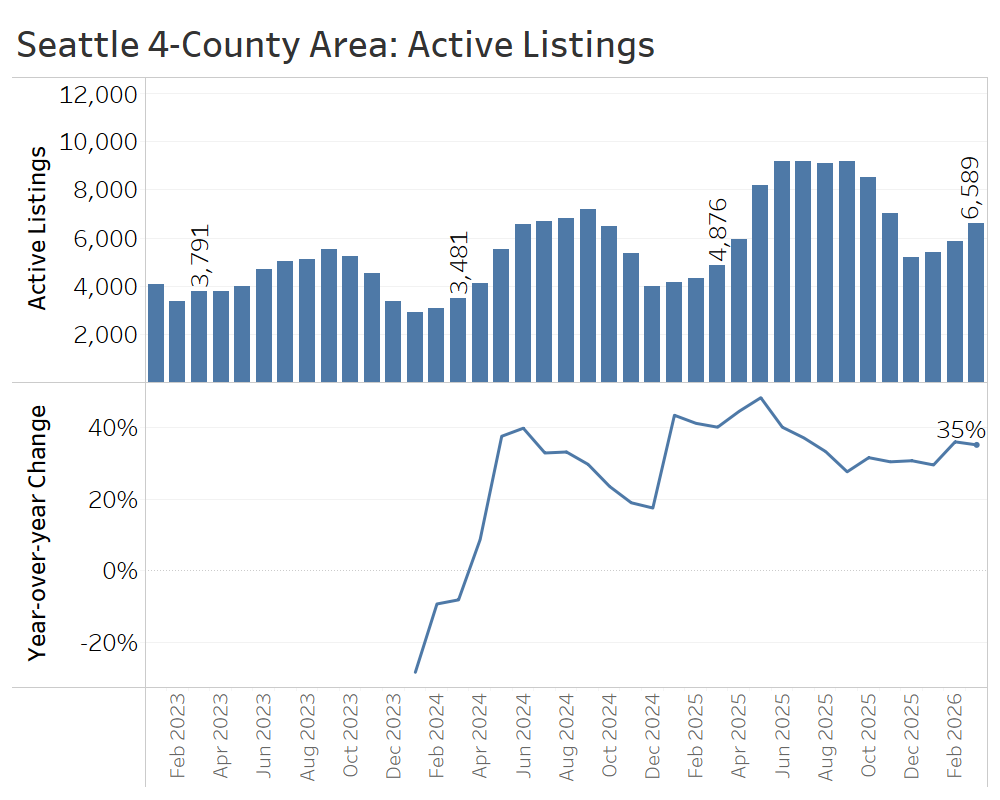

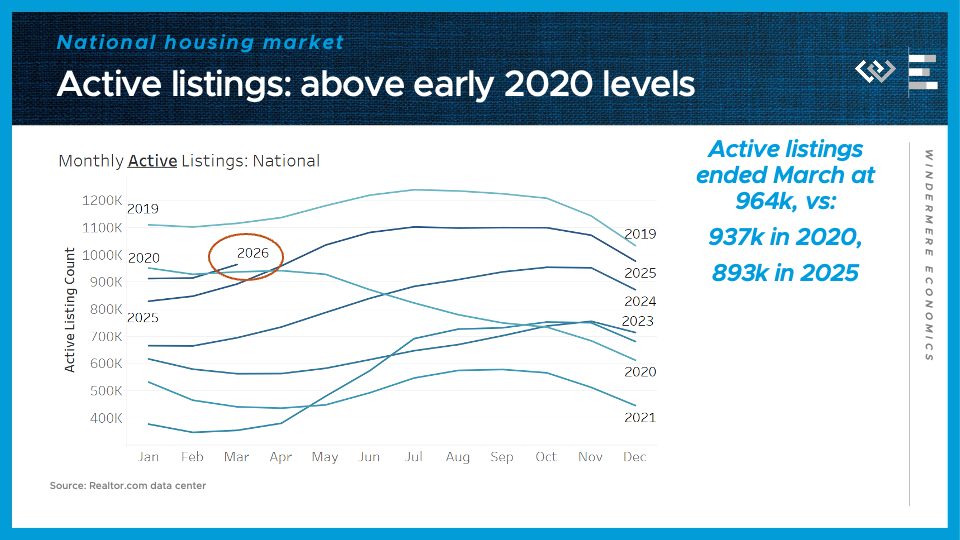

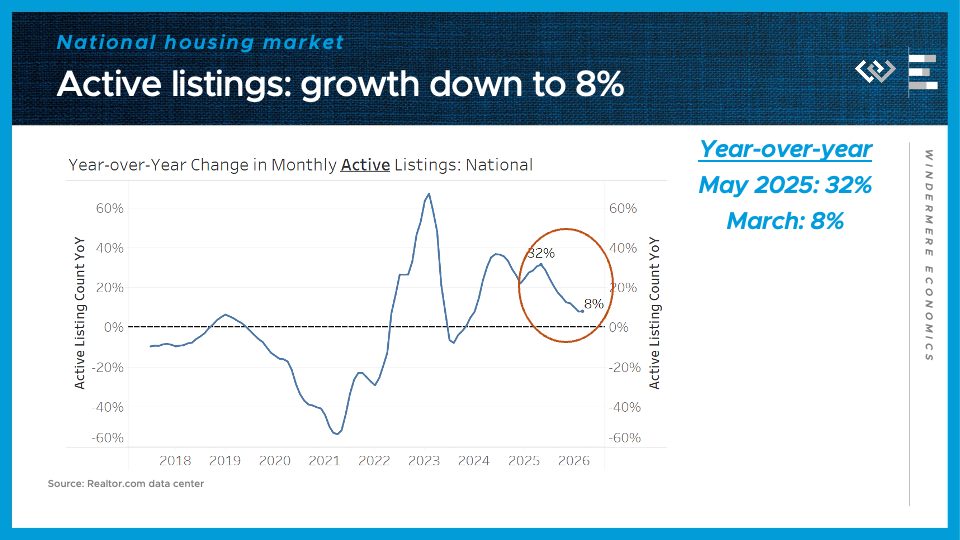

Finally, turning to the housing market, we saw 964 thousand active listings at the end of March—somewhat more than at this time in 2020, and about 8% more than last year.

That 8% year-over-year gain basically matches what I reported in February, bringing an end to a trend of decelerating inventory growth since last May. It’s a little early to call this a turning point, but it may be an indication that inventory gains are picking back up. If that continues, buyers could really see a plethora of options on the market this summer. In the meantime, sellers should be aware that buyers are comparison-shopping, so it still pays to put your best foot forward, listing with an agent you trust, even in the busy spring selling season right now.

Local Look Western Washington Housing Update 3/11/26

Hi. I’m Jeff Tucker, principal economist at Windermere Real Estate, and this is a Local Look at the February 2026 data from the Northwest MLS.

We are now on the cusp of the busy spring selling season, and the data so far in 2026 point to a market that’s relatively balanced for buyers … for this time of year.

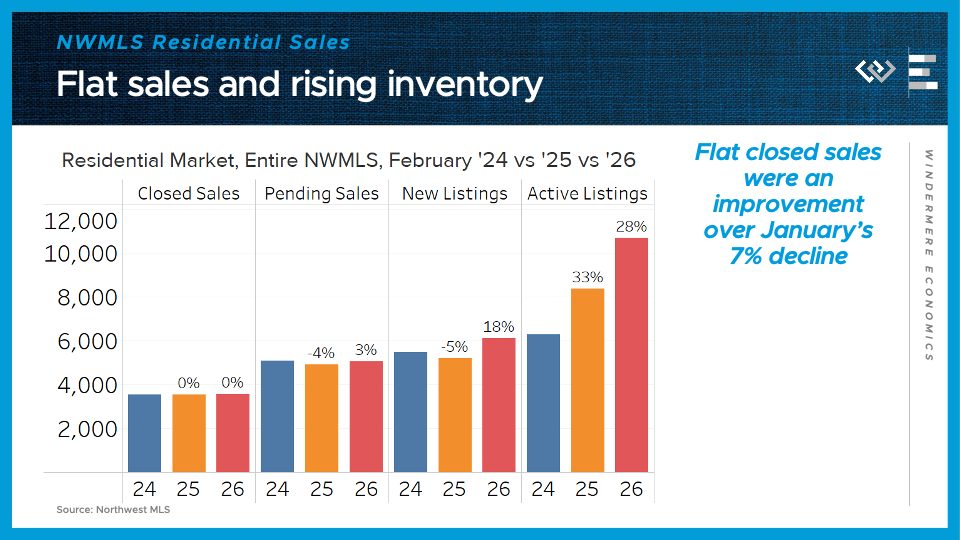

Across the Northwest MLS, there were almost exactly the same number of closed home sales as in February 2025, or the prior February for that matter. And pending home sales ticked up by 3%.

On the supply side, the flow of new listings was up a whopping 18% from last February’s pace. Finally, the month ended with 28% more active listings than last February. That’s a major uptick in inventory, and even the pace of that growth has now accelerated.

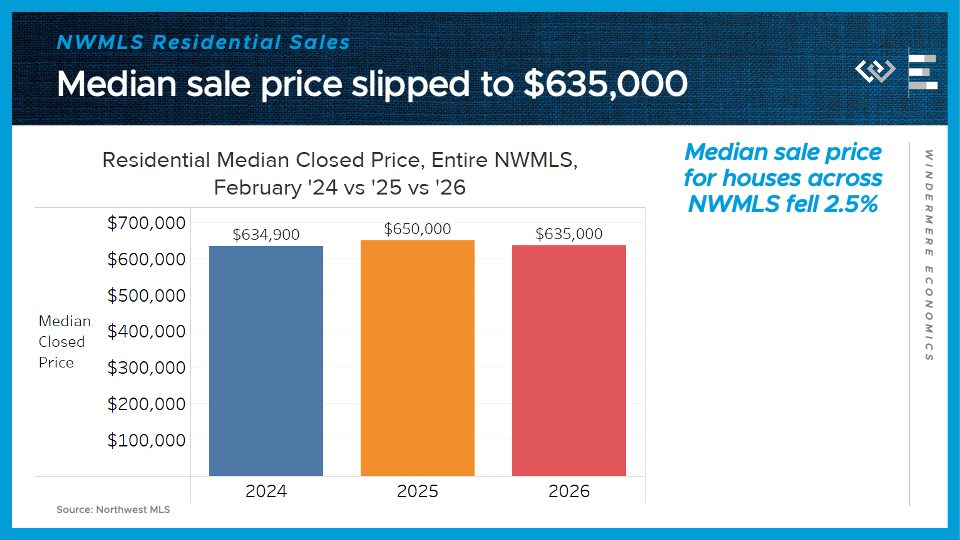

More negotiating leverage for buyers translated into lower home prices in February: down 2 and a half percent from last year, or basically back to 2024’s level.

Now for a closer look at the four counties encompassing the greater Seattle area.

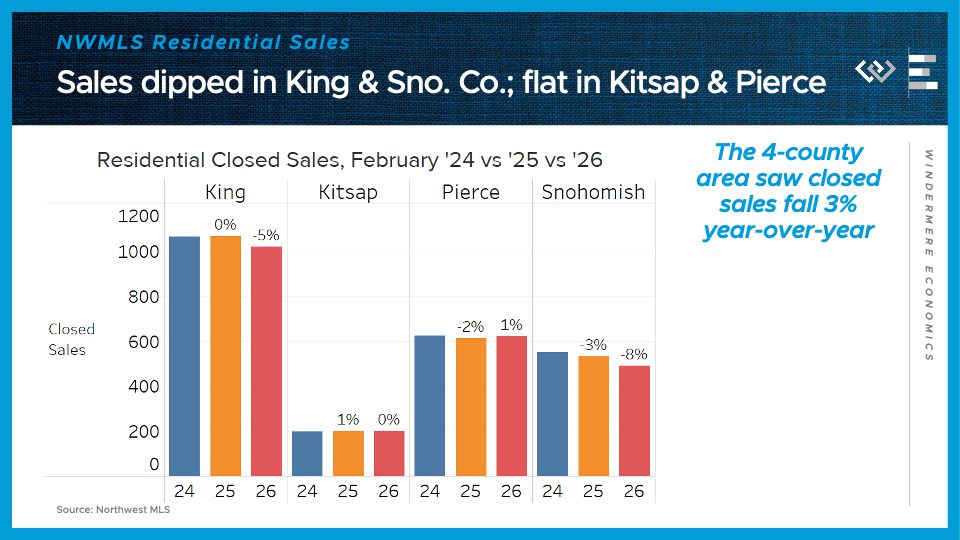

Closed sales dropped by 3% from last February around the region, which looked like a modest dip compared to January’s 9% decline. Once again Snohomish County had the biggest decline, followed by King County, while Kitsap and Pierce Counties’ sales volumes have held steady.

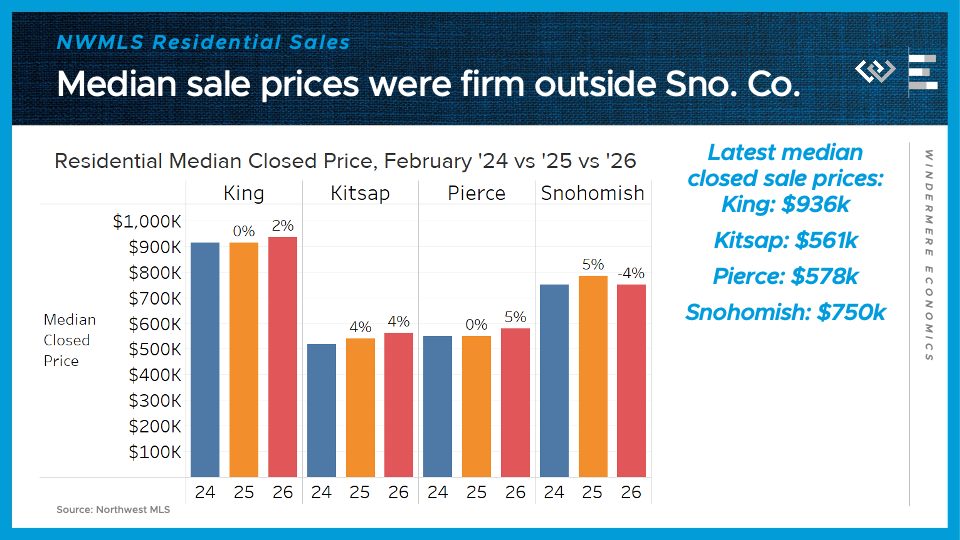

Median sale prices were mostly firm around the region, combing 2% in King, 4% in Kitsap, and 5% in Pierce County. Snohomish County, though, saw prices step back down to 2024 levels.

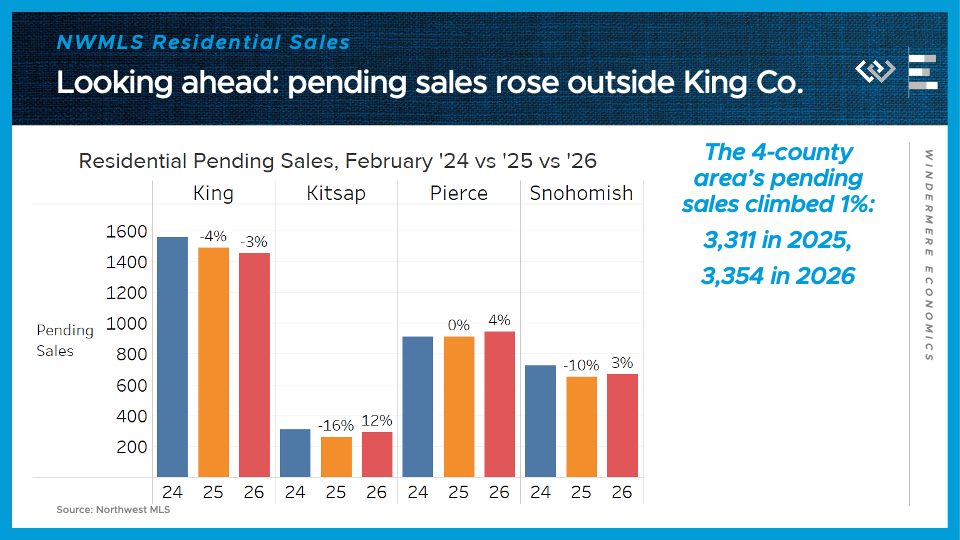

Looking ahead, pending sales climbed 1% across the region in February, buoyed by a big bounce back in Kitsap, and modest growth in Pierce and Snohomish Counties. Only King County saw a modest dip in pending home sales.

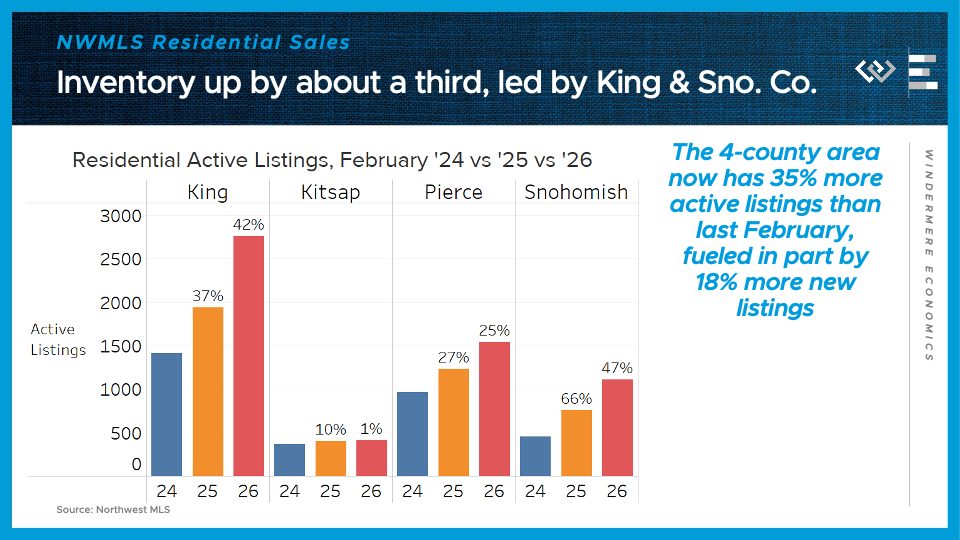

On the supply side, the 4-county greater Seattle area ended the month with 35% more active listings than last February, led by 47% growth in Snohomish County and 42% growth in King County. I think in those two core, higher-cost counties, buyers will see an unusually favorable spring buying season, thanks in part to a boost in listings from homeowners who de-listed last year and are now returning to the market.

Looking ahead to March and April, I think the big question is whether buyers feel emboldened by higher inventory and lower mortgage rates, or spooked by geopolitical turmoil and rising gas prices. As it stands, they will have more homes on the market to choose from than any spring in recent memory.

")