Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Windermere Real Estate is proud to partner with Gardner Economics on this analysis of the Oregon and Southwest Washington real estate market. This report is designed to offer insight into the realities of the housing market. Numbers alone do not always give an accurate picture of local economic conditions; therefore our goal is to provide an explanation of what the statistics mean and how they impact the Oregon and Southwest Washington housing economy. We hope that this information may assist you with making an informed real estate decision. For further information about the real estate market in your area, please contact your Windermere agent.

Regional Economics

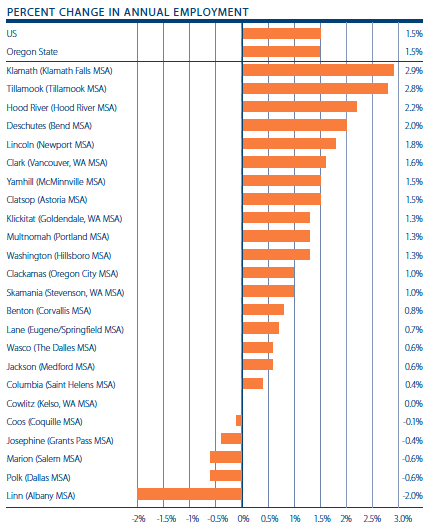

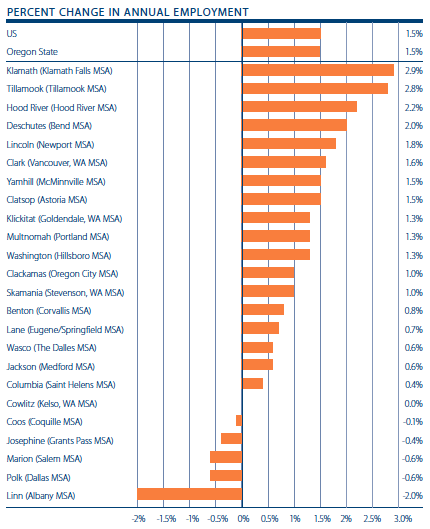

On an annualized basis, the Oregon counties covered in this report increased employment by 0.92 percent, or approximately 15,590 jobs, a further—albeit modest—improvement from the 0.8 percent annual growth that was discussed in our last report. On a year-over-year basis, 19 counties saw their employment base expand and five saw employment contract.

Employment growth was most pronounced in Klamath County (+2.9%). This was followed by Tillamook (+2.8%), Hood River (+2.2%) and Deschutes (+2.0%) Counties. Unsurprisingly, on an absolute basis, Multnomah County continued to contribute the largest increase in jobs with 5,800 additional positions over the past 12-month period. This was followed by Washington (3,100) and Clark (2,000) Counties.

On the negative side, job losses totaled 1,920 spread across five counties. Losses were most pronounced in Marion County, but the numbers were down by just 823 jobs. This was followed by Linn (-780) and Polk (-207) Counties. Losses in Josephine and Coos Counties were measured at 110 jobs combined.

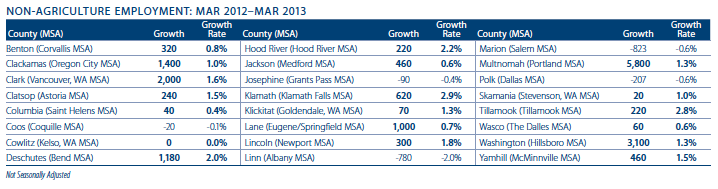

It is pointless to compare the current employment situation to that seen at the end of the year, as the data is not seasonally adjusted and, therefore, the decline in overall employment in almost every county between December of 2012 and March of 2013 was not a surprise. However, the number of jobs lost was. Employment shrank by almost 20,000 in the time period and I will be watching very carefully to see that this was just a function of seasonality and nothing to be concerned about.

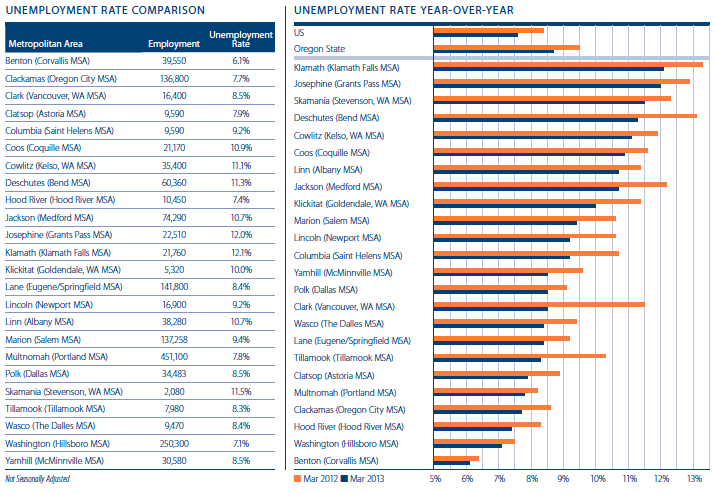

Continuing a trend that started in 2012, when compared to a year ago, the unemployment rate shrank in every county that was analyzed. This is positive and continues to suggest that the market is improving in a fundamental way.

The greatest improvement was seen in Clark County, where the unemployment rate dropped by a substantial three percent to 8.5 percent. This was followed by Tillamook (-2.0%) and Deschutes (-1.8%) Counties. The smallest improvements were seen in Benton (-0.3%), as well as Washington and Multnomah Counties, which both saw their unemployment rates reduce by 0.4 percent.

As much as this may sound like a broken record—having made this statement in previous reports—it remains true that the Oregon economy is stuck in low gear. Expansion remains well below its potential. I cannot, therefore, raise the grade from the “C-” that I gave it at the end of 2012.

I believe that the job market will continue to grow, but at a pace that is lackluster.

Regional Real Estate

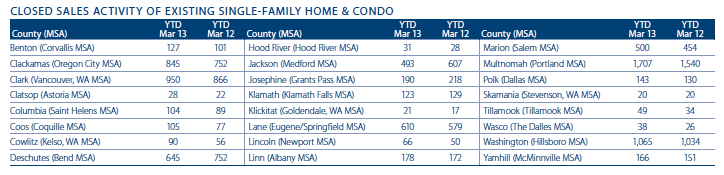

In the first quarter of 2013, the region reported 8,167 units of resale housing—a modest improvement of three percent from the same period in 2012.

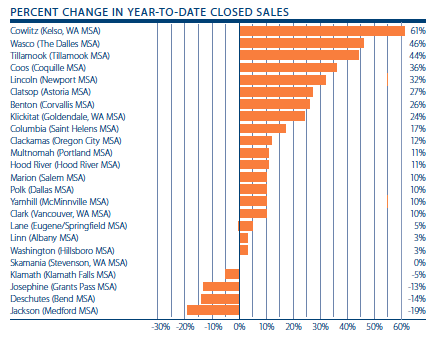

In 2012, the greatest growth in housing sales was seen in Cowlitz County (+61%), Wasco County (+46%), Tillamook County (+44%), Coos County (+36%) and Lincoln County (+32%). There were four counties that saw sales volumes drop when compared to Q1 2012. The most pronounced decline was seen in Jackson County, where sales dropped by 19 percent. This was followed by Deschutes (-14%), Josephine (-13%) and Klamath (-5%) Counties. As to whether this is a function of lack of supply, or lack of demand, is uncertain, but the drop was a fairly modest 255 units.

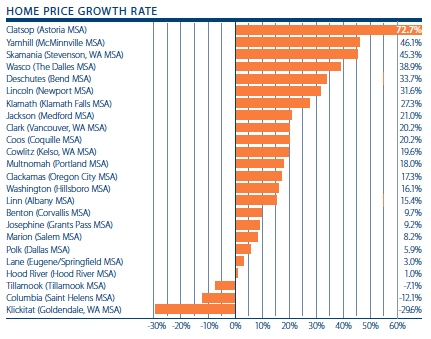

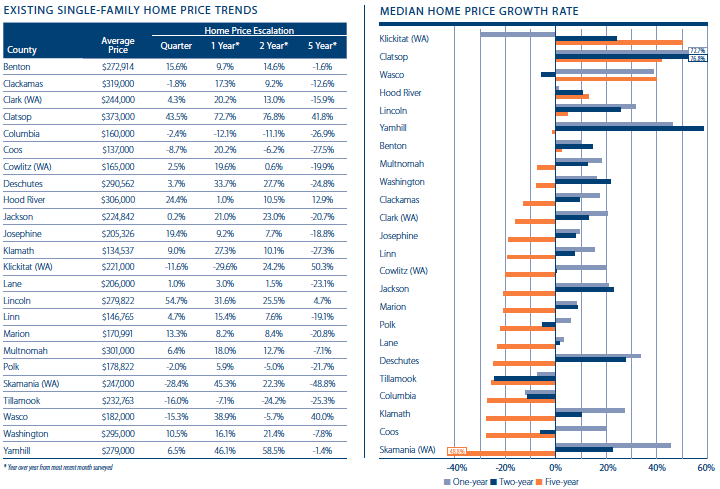

When we turn our attention to home prices, it is very pleasing to see that 21 of the markets analyzed registered year-over-year price increases (up from 15 in the last report), with just three showing declines in values from a year ago. In aggregate, the markets surveyed saw values increase by 17.9 percent over the same period in 2012.

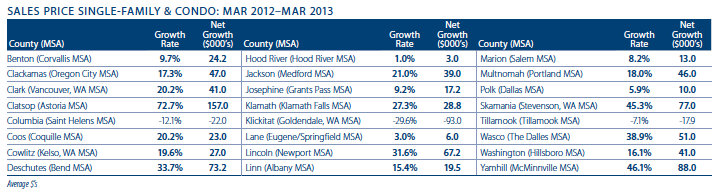

Other than the dramatic 72.7 percent growth in the very small Clatsop County market, 15 other counties registered double-digit gains in price between March 2012 and March 2013. When compared to prices seen in the last quarter of 2012, 16 counties saw prices rise (up from 13 in our last report) and eight saw sale prices drop.

As we look at longer term trends, I continue to be pleased to see prices generally trending higher. When compared to the same period in 2012, there are now 19 counties that have seen prices rise – up from 14 in our last report. When compared to March of 2008, there are now five counties where sales prices are higher.

I am giving the market a “C+” grade for the first quarter of 2013, up from a “C” at the end of 2012. Without a doubt, inventory constraints are affecting the market, but sales and prices are still higher.

Conclusion

In 2012, Oregon’s economic performance was very similar to both 2010 and 2011. In each case there were some cautious hopes for stronger growth and more jobs as momentum was building near the end of the previous year. However, each time the regional economy has encountered headwinds that slowed growth near mid-year. The usual suspects have been flare-ups in the ongoing European recession and sovereign debt crisis, weak housing-related industries, and cuts at all levels of government. The end result in each of the past three years has been slow, lackluster growth.

As 2013 opens up, unfortunately, there is little hope that Oregon will see much immediate improvement in economic growth. Federal government cutbacks and tax increases are weighing on the economy, and the pipeline of future orders has slowed among many local manufacturing industries.

That said, and despite the weak near-term outlook, I believe that the stage is set for stronger growth going forward, should the economy manage to successfully navigate the next few months. The primary reason for optimism is the strength of balance sheets for businesses and consumers alike. With financing costs low and corporate profits high, a great deal of spending and investment stands to be unleashed as soon as some of the uncertainty that is obscuring the near-term outlook is cleared away. Although household net worth is not back to pre-recession levels, it has been growing strongly. Home prices are rising once more, and stock markets have regained all of their recessionary losses.

Looking at the housing market, I am modestly pleased with its progress so far. Rising prices and slightly higher interest rates have been a catalyst to get would-be buyers off the fence and in search of a new home.

However, we are in dire need of inventory. As I mentioned in my last report, if there are not substantial increases in listings, there will be some buyers who will become disenchanted either with the lack of choice in the market, or with the desire not to get into bidding wars on homes that actually are for sale. This remains a mid-term concern.

About Matthew Gardner

About Matthew Gardner

Mr. Gardner is a land use economist and principal with Gardner Economics and is considered by many to be one of the foremost real estate analysts in the Pacific Northwest.

In addition to managing his consulting practice, Mr. Gardner chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; sits on the Urban Land Institutes Technical Assistance Panel; is an Advisory Board Member for the Runstad Center for Real Estate Studies at the University of Washington and is the Editor of the Washington State University’s Central Puget Sound Real Estate Research Report.

He is also the retained economist for the Master Builders Association of King & Snohomish Counties. He has twenty-five years of professional experience in the U.K. and U.S.

He has appeared on CNN, NBC and NPR news services to discuss real estate issues, and is regularly cited in the Wall Street Journal and all local media.

")