Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Windermere Real Estate is proud to partner with Gardner Economics on this analysis of the Western Washington real estate market. This report is designed to offer insight into the realities of the housing market. Numbers alone do not always give an accurate picture of local economic conditions; therefore our goal is to provide an explanation of what the statistics mean and how they impact the Western Washington housing economy. We hope that this information may assist you with making an informed real estate decision. For further information about the real estate market in your area, please contact your Windermere agent.

Regional Economics

The theme that appears to be most appropriate for this issue of the Gardner Report is “location.” As I pore through the data that is presented here, it is quite clear that after falling off the proverbial economic precipice in 2008, we have come out of the free fall and are starting up the long road to recovery on both the job front as well as in our real estate markets.

Between March of 2011 and March of 2012, the markets considered in this report added a very impressive 54,230 jobs—a 2.58 percent growth rate, which far exceeds that of Washington State as a whole, or even the United States average. As the charts to the right indicate, nine counties expanded their employment base with just seven shrinking. When I compare this to our last report where just six counties expanded while ten contracted, it is clearly a better picture.

Drawing on the aforementioned “location” theme, all markets are not created equal, and this is demonstrated by the employment growth figures, with major employment centers seeing the greatest increase in growth. When looking at year-over-year growth, Snohomish County (+4.6%) continues to lead the way followed by King (+3.2%) and Whatcom (+2.4%) Counties. Job losses were most profound in San Juan County (-2.8%), followed by Kittitas County (-2.3%), Grays Harbor County (-1.5%), and Cowlitz County (-1.4%).

For perspective, over the past 12 months, the region added 56,460 jobs in nine counties while losing 2,230 jobs in the remaining seven.

From an unemployment rate perspective, the improvement has been quite remarkable with all but one county (Grays Harbor) showing improvement over the past 12 months.

I glanced back on some old reports recently and shuddered at some of the numbers. In 2008, our region lost 27,370 jobs and in 2011 we grew by 24,350. This latest report shows that our growth rate is substantial when compared to a year ago, however I cannot see this rate of growth being sustained at its current pace. As a result, I am going to give the current employment situation a “B-” grade, up a notch from the last quarter, but at a level that it will likely stay for a while. My expectations for 2012 are still positive, but we may be disappointed by the speed at which we create new jobs as we enter the summer.

Regional Real Estate

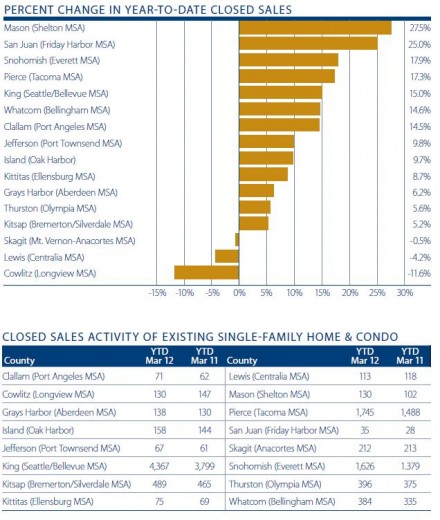

Our market reported 10,136 sales of existing homes in the first quarter of this year—an impressive increase of 13.7 percent from the first quarter of 2011. The most pronounced gains were seen in Mason (+27.5%), San Juan (+25%), Snohomish (+17.9%), Pierce (+17.3%), and King (+15%) Counties.

Declines in sales were found in just three counties—Cowlitz, Lewis, and Skagit—but most were were extremely small and, as such, not any real cause for concern.

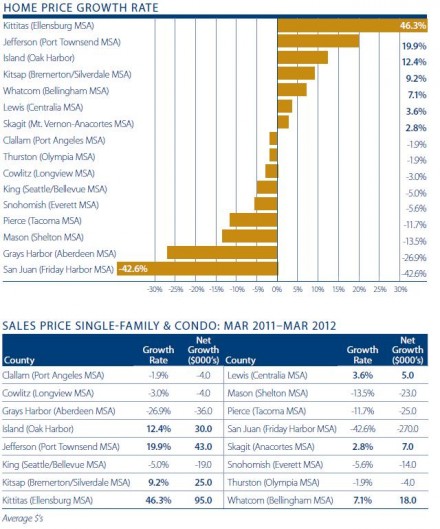

As can be seen in the chart to the right, there were seven counties where home prices were at levels above those seen a year ago, and nine where prices were lower. In aggregate, home prices in the counties analyzed were 4.5 percent lower than in March of 2011, but there is a big disclaimer here. If we exclude the highly volatile San Juan County, home prices actually rose by 2.9 percent year-over-year.

Of the counties that saw the most appreciation, the most pronounced price gains were seen in Kittitas (+46.3%), Jefferson (+19.9%), and Island (+12.4%) Counties. The greatest declines were seen in the previously mentioned San Juan County (-42.6%), followed by Grays Harbor (-26.9%), Mason (-13.5%), and Pierce (-11.7%) Counties.

As I dig into the data, it is clear that distressed sales still comprise a substantial piece of the market, which is functioning to hold down price growth as sales of these homes are almost always below market value. Getting through this inventory is a process, and it can be a painful one. That said, it is an important part of any recovery. We know that the percentage of “all cash” sales are far higher than we have ever seen, which indicates to me that investors are now buying, and this will likely help in depleting this inventory.

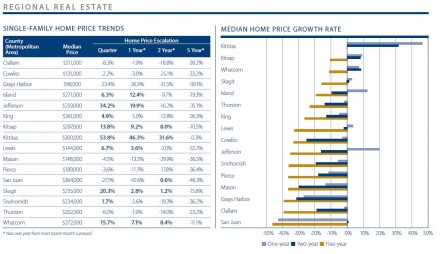

Movements in the real estate market are now best described as “local.” The recovery in prices will not be equal across our region, rather areas that are closer to employment centers, as well as those that did not see egregious increases in value back in the heyday, will likely see their markets improving the fastest.

I am raising the housing market grade marginally to a “C” this quarter. Improving stability in prices is occurring at a faster rate than I had anticipated, but as I have stated previously, further improvement in the grade will be very dependent on whether we see an increasing supply of homes for sale. So far, the spring season has not replenished the market with new listings, as is typical for this time of year, and inventory levels remain at levels not seen in several years.

Conclusion

The national, regional, and local economies fell off a cliff in 2008 and into an abyss that was deeper than any seen since the Great Depression. Since that time we have clawed our way forward and are making solid progress, but there is still a long way to go.

I believe that our own state is likely to see its job recovery occur earlier than that of the United States as a whole, which is a function of our exposure to the Asian markets more than anything else. We are not out of the woods yet, but the forecast is a positive one.

Our real estate markets are also in the throes of an about-face, but some areas are faring better than others. Bank owned and short sales are still high, but the number of non-distressed houses for sale is at a level that is worrisome. Choices are not what many buyers are expecting to see, which may put a further damper on select markets.

Overall, I am still looking to 2012 as the year that we emerge from the recession and, in our own inimitable Washingtonian manner, stride forward in the belief that the way ahead is a good one. (After all, who else wears shorts when it’s 50 degrees outside?)

About Matthew Gardner

Mr. Gardner is a land use economist and principal with Gardner Economics and is considered by many to be one of the foremost real estate analysts in the Pacific Northwest.

In addition to managing his consulting practice, Mr. Gardner is a member of the Pacific Real Estate Institute; chairs the Board of Trustees for the Washington State Center for Real Estate Research; the Urban Land Institutes Technical Assistance Panel; and represents the Master Builders Association as an in-house economist.

He has appeared on CNN, NBC and NPR news services to discuss real estate issues, and is regularly cited in the Wall Street Journal and all local media.

")