Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

Windermere Real Estate is proud to partner with Gardner Economics on this analysis of the Oregon and Southwest Washington real estate market. This report is designed to offer insight into the realities of the housing market. Numbers alone do not always give an accurate picture of local economic conditions; therefore our goal is to provide an explanation of what the statistics mean and how they impact the Oregon and Southwest Washington housing economy. We hope that this information may assist you with making an informed real estate decision. For further information about the real estate market in your area, please contact your Windermere agent.

Regional Economics

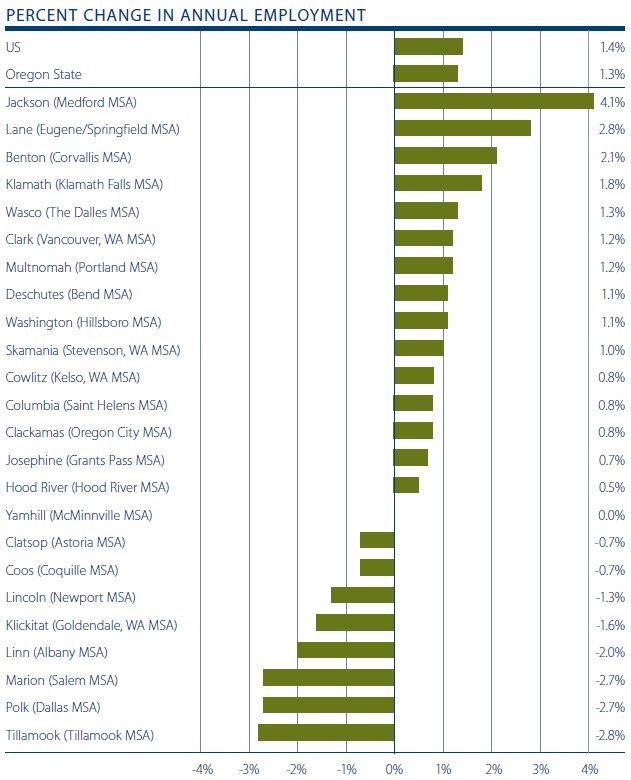

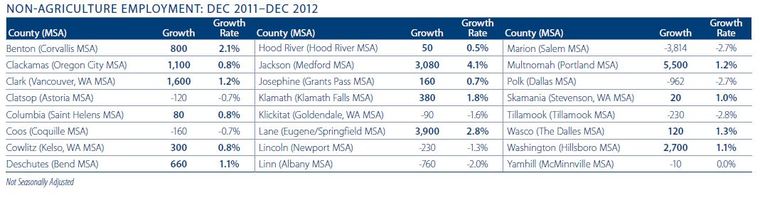

On a year-over-year basis, the Oregon counties covered by this report increased employment by 0.8%, or approximately 14,000 jobs—a modest improvement from the 0.75% annual growth that was discussed in our last report. On a year-over-year basis, 16 counties saw their employment base expand and just eight saw employment contract.

The greatest increases in employment came in Jackson County (+4.1%). This was followed by Lane (+2.8%), Benton (+2.1%), and Klamath (+1.8%) Counties. On an absolute basis, Multnomah County maintained the largest increase with 5,500 additional jobs. This was followed by Lane County (3,900) and Jackson County, where employment grew by 3,080 positions.

On the negative side, job losses totaled 6,376 jobs spread across nine counties. By far the greatest losses were seen in Marion County, down 3,814 jobs. This was followed by Polk (-962) and Linn (-760) Counties. Losses in other counties measured less than 230 jobs each.

When we compare the data to that seen at the end of the third quarter, it is apparent that the state is stuck in somewhat of a rut, with both the third and fourth quarters showing job losses in 12 counties. That said, the market did add just under 8,000 payroll jobs in the fourth quarter of the year.

Inasmuch as the unemployment rate at the end of 2012 was better across the board from that seen at the end of 2011, the last quarter of the year saw a drastic turnabout in the unemployment rate in all but one of the counties surveyed. In every county but Benton, the unemployment rate rose between September and the end of the year.

This is concerning as the labor force contracted in all counties other than Lane. It is one thing to see the unemployment rate rise as more people start to look for work, but to see it increase with fewer people looking for jobs is a worrying situation. I hope that it is temporary, but I will be keeping a close eye on these figures as we enter the spring.

It appears to me as if the Oregon economy is stuck in low gear. It is expanding, but at a rate that is well below its potential. As such, I am maintaining the “C-” grade this quarter that I gave it in the third quarter. At some point the job market has to gather steam, I am just not convinced that now is the time.

Regional Real Estate

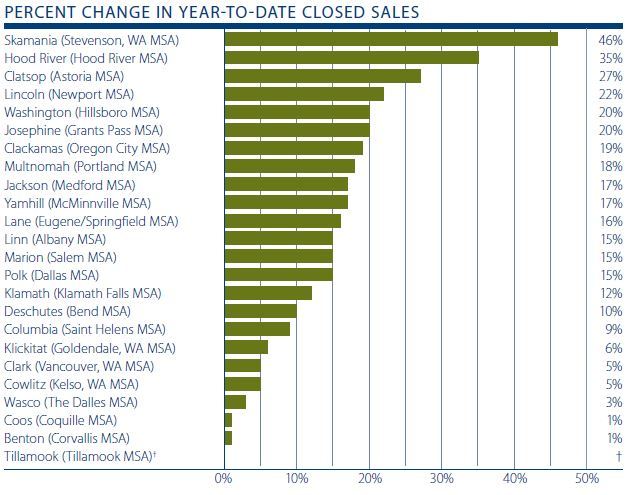

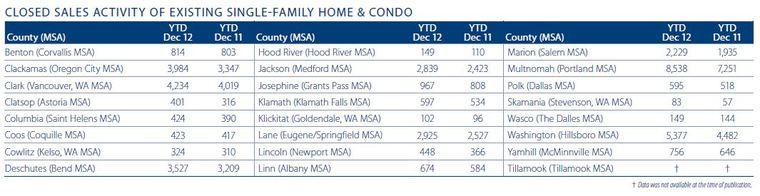

In the fourth quarter of 2012, the region sold 9,758 units of resale housing. Total 2012 sales amounted to 39,745 units, 13% more than were sold in 2011.

In 2012, the greatest growth in transactions was seen in Skamania County (+46%), Hood River County (+35%), Clatsop County (+27%), and Lincoln County (+22%). It was very pleasing to see that no markets saw sales volumes drop between 2011 and 2012.

Home sales continued to perform well in the fourth quarter, but quarterly sales shrank by 16% from the level seen in Q3. This is not a surprise, as seasonal fluctuations influence the figures. Additionally, I would contend that the worryingly low levels of homes for sale also contributed to the drop in sales.

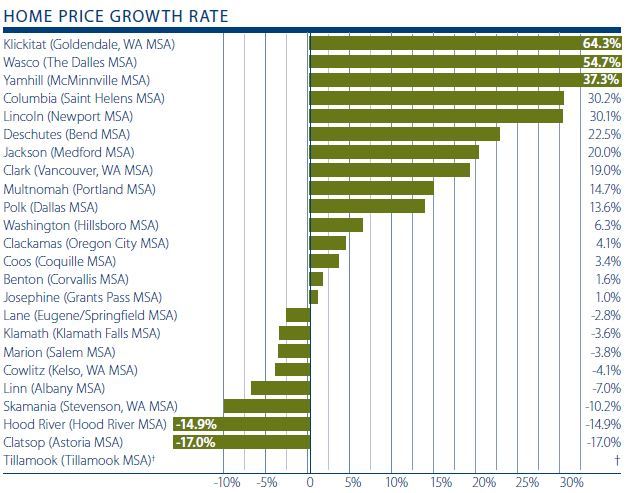

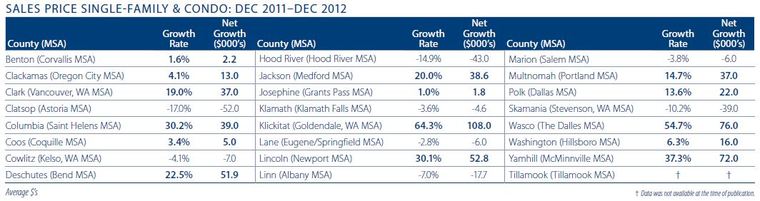

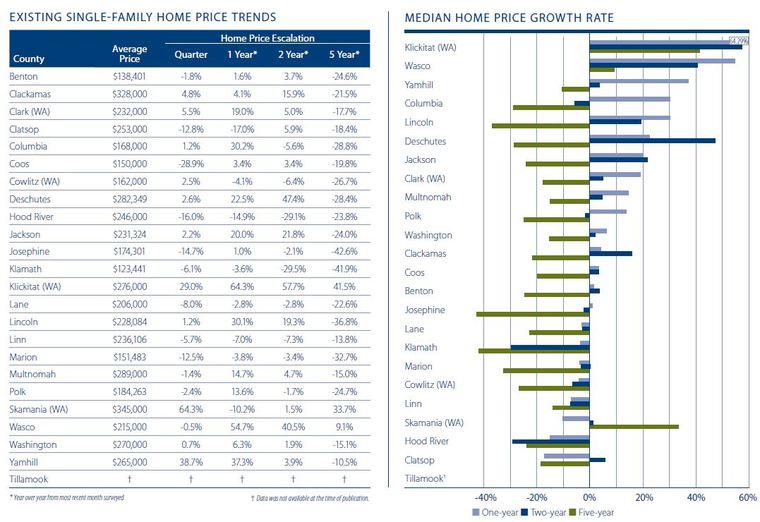

When we look at home prices, 15 of the markets analyzed registered year-over-year price increases (down from 16 in the third quarter) with just eight showing declines in values from a year ago. In aggregate, the markets surveyed saw values increase by 11.2% over the same period in 2011.

Other than the substantial 63% growth in the small Klickitat County market, ten other counties registered double-digit gains from December, 2011. When compared to prices seen in the third quarter of the year, 13 counties are higher, one was unchanged, and nine declined in value.

I was happy to see that there are 14 counties where prices are now higher than we saw two years ago. This is quite an achievement, as 2010 saw the market artificially buoyed by the Homebuyer Tax Credit. More surprising is that three counties saw home prices higher than at the end of 2007.

A “C” grade is appropriate here. It has remained static for three quarters now, but the lack of inventory appears to be having a negative effect on values. I want to see more homes for sale before I consider giving a better grade.

Conclusions

There are plenty of metaphors that I could use to describe the Oregon job market, such as “weak,” “sluggish,” or “slow” but, in all honesty, a better word is actually “average.” Certainly, the job growth that was seen in 2012 has hardly put a major dent in the number of jobs lost through the recession, but the economy has been improving.

I believe that the lackluster growth that has been seen is a function of two distinct, but related, issues. The first is that the Federal government is starting to realize that it cannot expand in the manner that it has been. Because of this, employment in government services has not been positive. This is particularly interesting as, from a historic perspective, job growth following recessions has traditionally been led by government hiring. As such, it has fallen on the private sector to pick up the slack and add to their payrolls.

Private industry has, so far, been doing its best to answer the call to arms, but industry looks to the government for some kind of assurances that we will not fall back into recession. The current issues revolving around fiscal cliffs, debt ceilings, and sequesters are not giving businesses the assurance that they so badly need. Until the outlook on a national basis is clearer, we cannot expect private firms to increase their hiring and, as such, improvement in the employment situation in Oregon, and in most of the rest of the country, is likely to be lackluster.

The housing market in the state remains on a more solid footing with steady improvement seen pretty much across the board. Interest rates remain at or near historic lows which, when viewed in concert with the stability in home values, has acted as a catalyst and allowed many would-be buyers to get off the fence.

This is, indeed, positive but I fear that the lack of homes for sale—unless we see a dramatic turnaround in the spring—will leave buyers disenchanted. Along with many others, my fingers are crossed that we will see improvement in listing activity soon. It is sorely needed.

About Matthew Gardner

About Matthew Gardner

Mr. Gardner is a land use economist and principal with Gardner Economics and is considered by many to be one of the foremost real estate analysts in the Pacific Northwest.

In addition to managing his consulting practice, Mr. Gardner is a member of the Pacific Real Estate Institute; chairs the Board of Trustees for the Washington State Center for Real Estate Research; the Urban Land Institutes Technical Assistance Panel; and represents the Master Builders Association as an in-house economist.

He has appeared on CNN, NBC and NPR news services to discuss real estate issues, and is regularly cited in the Wall Street Journal and all local media.

")